so they lost all of the 50M+ clients and one 30 M+ and most of the additions are in 1M+ bracket. Revenue loss of 50Mn+ in Telecom segment while Medical devices , plant engineering and transportation grew at 20% while Medical devices grew at 50%.

Q1 would be severely hit due to covid and Q2 is still uncertain at this point of time. Last year revenue grew by ~9% constant currencies basis.

Considering mostly flat or negative outlook for the most of FY21.Stock at the current valuations of 15 times of FY20 and 16 times of FY21E looks fairly valued or over valued (Un fortunately there are no peers to compare and LTTS itself is newly listed to compare against historical PE. This is first downturn after the company got listed so how it reacts to this adversity is yet to be seen). I am not comparing it with traditional service companies like TCS , Infosys etc because the business model is slightly different. In case if anyone interested TCS was trading at 10x time during GFC.

Disc : Tracking

What is the hit they have taken on Other Comprehensive Income Rs.191 crore for the quarter and Rs.248 crore for the year? Does anyone have any idea what this pertains to?

LTTS has started a new podcast series on their youtube channel named #EngineeringForTheNewReality which gives insights on how businesses are sharping up in post-Covid world in Health care, AI, Cyber-security etc. Good series to get updates on each area.

Not really. LTTS is more diverse than Tat Elxsi. They have more verticals than Elxsi. Elxsi is mostly into automobiles and automobiles are cyclical in nature so is Elxsi so you should know when to get in and when to get out. LTTS is into more diverse fields and transportation is just one part of it

Yes TEL is in Automotive Design however it has other business segments also namely VFX (Special Effects in Movies), VLSI, Design services for FMCG, Medical Devices, Electronics and Electrical appliances

Medical devices is highest growth segment for Tata elxsi and their main focus area now to diversify. LTTS is so diversified and digital tech new age company, but not sure why it doesn’t show in growth rates and in development of any major breakthrough platform or product

Key business updates:

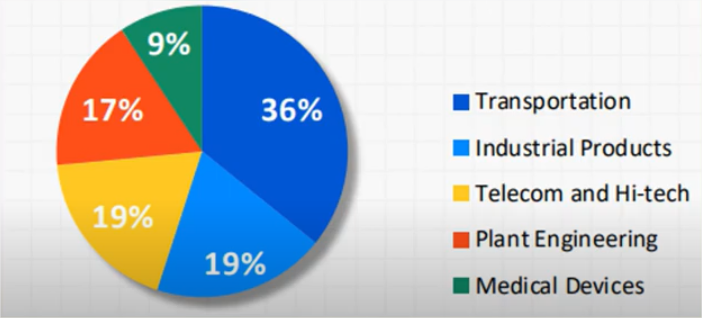

• Technology company present in 5 verticals

o Transportation (35% of revenue, operating margin up from 17% to 18%)

o Industrial Products (19% of revenue, operating margin up from 25% to 26%

o Telecom and Hi Tech (20% of revenue, operating margin up from 15.6% to 16.4%)

o Medical Devices (9% of revenue, operating margin up from 25% to 27%)

o Plant Engineering (16% of revenue, operating margin up from 23% to 25.4%)

• Total 168843 employees and 270 global clients across 25+ countries

• 51 innovation labs and 502 patents (103 last year)

• Industrial, Plant engineering and medical devices are high margin business

• Ability to leverage parent engineering experience and know how

• Clients include 67 fortune 500 companies and 53 of world’s top ER&D companies

• Rated as leader in IoT engineering and managed services by IDC in 2020

• Leader in automotive engineering services by Everest

• Opened design center in Illinois for aviation

• IoT based smart building system i-BEMS deployed in Telaviv for a global technology giant

Financial Performance:

• Rs 5690 crore of revenue and Rs 819 of profit in FY 20 with a revenue growth of 11% YoY and PAT growth of 7% YoY. Resulted in 75-rupee EPS from Rs 66.7

• Export incentive is up from Rs 27 crore to Rs 91 crore

• 40% revenue from fixed price contracts and 60% is time and material basis

• 16.5% EBIT margin

• Medical devices showing very good growth

• 61% revenue from North America vs 55% last year, 15% from Europe vs 18% last year, 13% from India and remaining from rest of the world

• Only North America showed revenue growth YoY

• No client is more than 10% of revenue and group contributes to less than 2% of revenue or outsources service expenses (to L&T infotech and others)

• 3 of above verticals – transport, plant engineering and medical equipment have shown more than 20% growth. Telecom has degrown and industrial products had single digit growth

• Share of digital revenue is up from 33% to 40% in last 1 year

Other Important Points:

• Rs 800 Crore + cash on books

• Total Rs 21 dividend for FY20 which is approximately. 20% of profit

• 75% shares held by promoter, 15% by institutional investors (FII is up from 5% to 8.3%) and 7% by retail

• Company has not given much hike to management and employees this year. 1.9% increase in median remuneration. India employees’ hike is 5.91%, outside India 1.85% and average decrease in management hike is 9% due to lower payout of variables and commissions

Risks and Open Questions

• There is 50% increase in computers but not much increase in headcount

• Rs 389 crores of goodwill on balance sheet

• Rs 100 crore plus investment in 2 subsidiaries which are not generating enough profit

• Rs 26 crore of doubtful debt expensed, this was negligible last year

• Some loans and corporate guarantees have been given to holding company and subsidiaries though on interest rate basis

• Holding company charges Rs 8 crore of trademark fees

Below is my attempt to summarize about the company. Please feel free to add risk or comment on growth as you feel. Description

L&T Technology Services Limited (LTTS) is a global leader in Engineering and R&D (ER&D) services. With 502 patents filed for 53 of the Global Top 100 ER&D spenders, LTTS lives and breathes engineering. Some of the innovation includes – World’s 1st Autonomous Welding Robot, Solar ‘Connectivity’ Drone, and the Smartest Campus in the World, to name a few. Company is present in five main areas – Transportation; Industrial Products; Telecom and Hi-Tech; Medical Devices; and Plant Engineering. Company has 51 innovation labs.

Company can benefit from Covid since small customer might not have budget to invest on innovation lab and can outsource it to the company since LTTS has 50+ innovation lab

Budget cut typically happen on R&D spending first. So it might impact company revenue. Need to see if company can retain existing projects and customers for next 1-2 quarters

Around 50% onsite presence. With H1B and L1 restrictions on travel to US, it might impact their business. But it seems temporary as restrictions will be lifted by year end.

Any other risk?

Price

Company is available at 16 PE. Since I dont have any knowledge on calculating intrinsic value, so I am not sure if company is providing good margin of safety at current price or not.

Conclusion

Overall I believe customer will keep spending money on automation, smart equipments and LTTS being niche player in this area can benefit and grow in coming years.

The financials of LTTS look good, it belongs to a well respected Business Group and is involved in innovation / R&D. Yet, the market hasn’t really valued it richly.

The biggest question that arises is who is controlling the Intellectual Property (IP)?

From what I understand, their client controls the IP created through the R&D work. The value generated by commercialising products don’t go to LTTS.

Therefore it can only be viewed as a well

managed ER&D outsourcing company. The fruits & failure of this work are harvested by their clients and therefore valuations may continue to remain muted.

From my viewpoint, the trigger for a re-valuation would be if LTTS contracts include any clause where they have revenue sharing arrangement with their clients for successful commercialising of IP. Such contracts would increase both risks and rewards as compared to pure outsourcing contracts.

If someone has any information on the nature of their client contracts then please share it.

Disc: Owned it for less than a year and sold it off during the market crash.

The work they do is tailor made for each client’s specific requirements, they do not make packaged products which can be deployed off the shelf. Owning IP in such a case is neither feasible nor useful.

From financials if you see employee cost trend it looks on higher side compare to TCS , OPM is less than TCS . Even if LTTS claim to be niche it is not reflecting in numbers. Rightly it is valued less than TCS.

I think you are mixing two things here. LTTS is not typical IT company like TCS even though TCS has one of its arms catering to ER&D services. LTTS is more into software led by engineering R&D.

@Viral Nobody owns IP in outsourcing industry not even our IT giants. LTTS owns its patents. Some of them they own exclusively and some with their clients. How much they can monetize them is to be seen but generally such patents are not of much use financially based on what i have observed. Just like IT industry, fortune of ER&D players like LTTS depends on spending of their clients.

LTTS’ strength lies in their engineering DNA. They have some of the marquee list of clients from the ER&D industry and their fortune depends on how the spending is evolving in ER&D post COVID. You need to go through annual report of some of their customers like Intel, Rosewell automations, John Deer etc to understand that. Out of the five verticals they are operating Medical and Plant engineering should do well as per management where as they might see reduced demand in Transportation, Process and Telecom verticals.

If you observe recent data, GM’s class 8 truck sells did not fall as anticipated during June quarter and UK is reporting high rise of usage in electric cars. All these cater well for their Transportation business. Overall they are well diversified and one of the leading players in ER&D with an able management.

I have been spending some time on the business. Thanks @suru27 for the AR notes. The Export incentives have been a high number for the last 3 years.

Other Income

209

223

193

58

-Export Incentive

93

28

65

0

-Forex Gain

74

93

115

42

-Others

42

102

14

16

Forex gain I think is largely a non-cash increase owing to translation changes etc. The export incentives I think see a sunset from this FY if my understanding is correct.

What is certainly interesting is their sales engine, going through the con-calls it seems that they have a robust engine going on.

However what is worth spending some time on thinking is that the growth is quite lumpy and driven by many a things which can be quite specific and short term in nature - for example the medical devices segment growth is driven by regulations change that is happening across the geographies. Tata Elxsi also talks about the same in their recent con-call. The issue I have is that some of these things change quite quickly - like what happened in Telecom vertical when some of the things that they were working on were de-prioritized by the customer.

This year could be an interesting time to understand more about the business. Will post more as I finish my work

@amishra if possible can you please share the source of this? I feel that for this company a couple of critical factors would be:

Size of the opportunity. Size of growth of opportunity (industry size and Industry growth).

Competitors and LTTS’s positioning vis-a-vis its competitors.

As per my reading of this thread, the closest competitor for LTTS is Tata Elxis. They certainly compete

in medical devices segment. Do we know about competitive advantages of either of the companies in this segment? Is any of these products differentiated? I will try to find answers to these questions and would suggest other investors to also think along these lines.

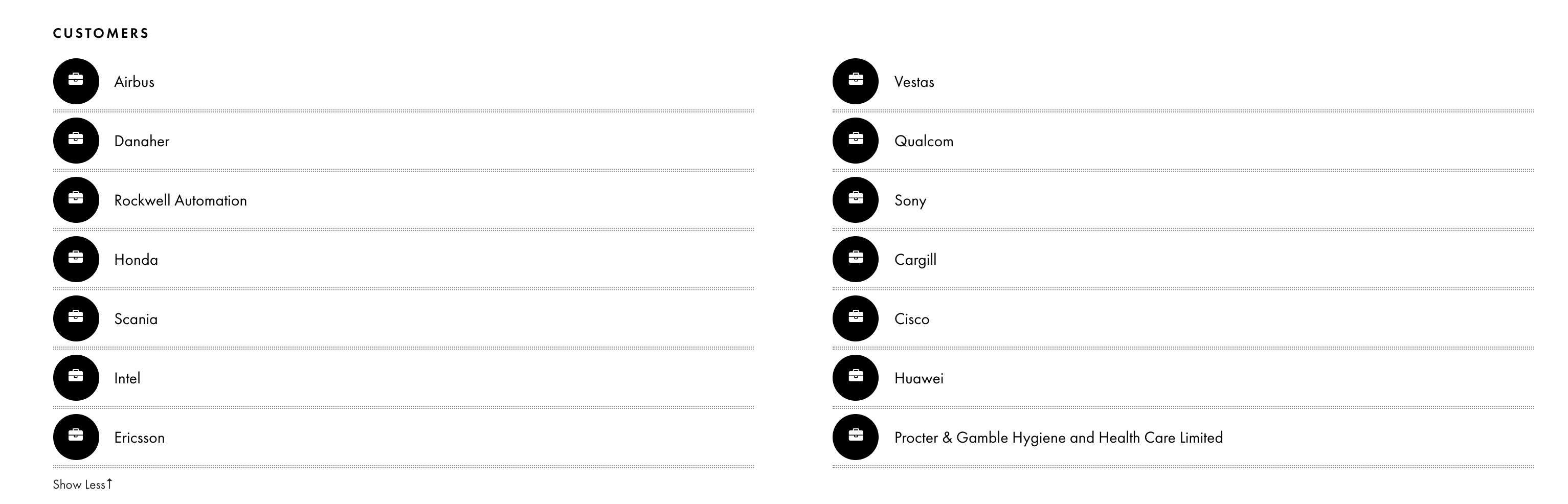

Here are some of the customers of LTTS courtesy tijorifinance.com

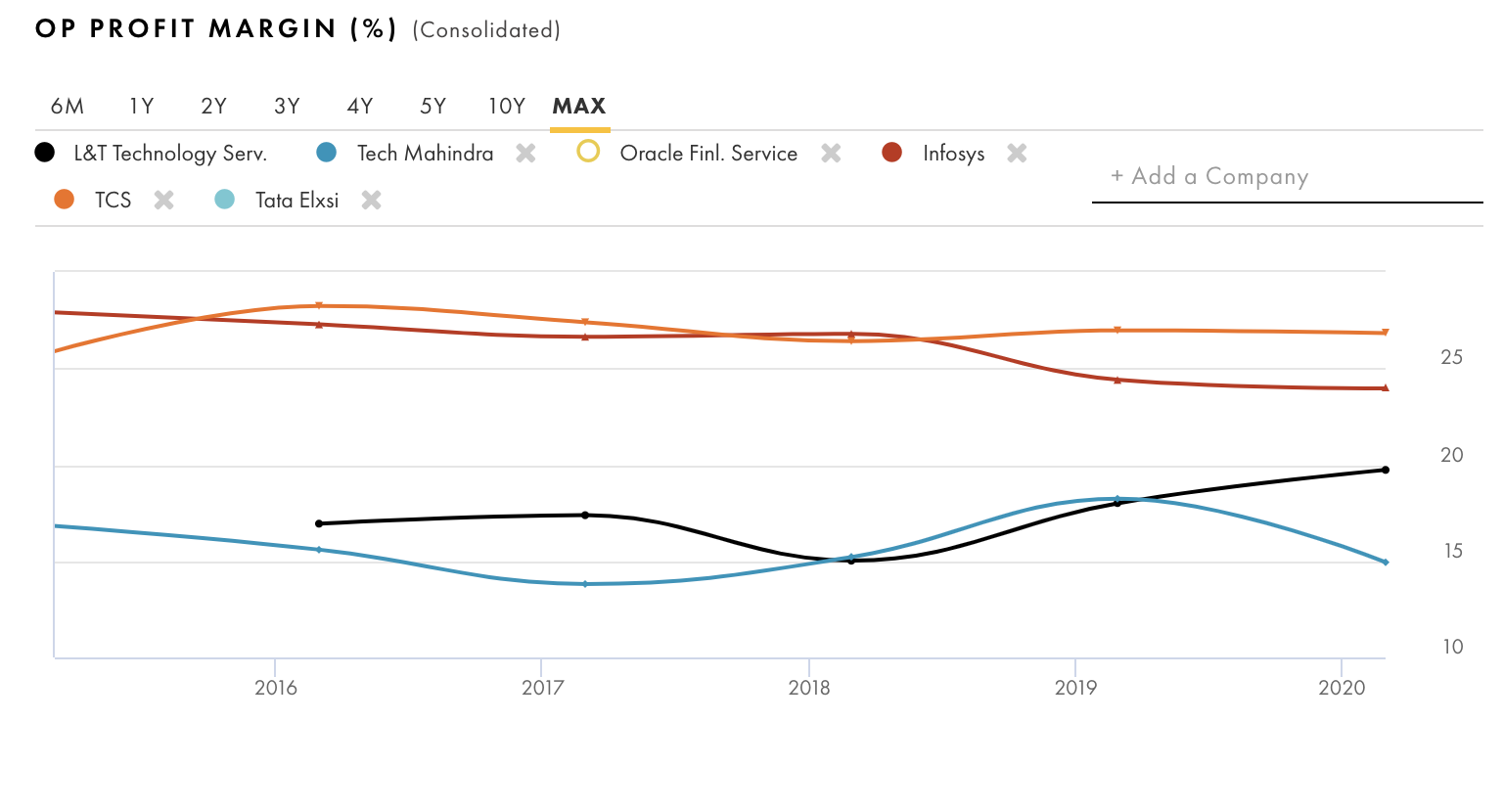

While the big companies are in a overall downward trend, LTTS seems to be in an upward trend.

The key risks are the presence of a management which does not really want to grow or more appropriately probably could not care either way (whether company achieves growth or not). Right now i’m seeing LLTS as a company which can possibly grow its financials by 15% for probably 10-15 years. But probably not in a category where it can grow its financials by 20%+ for 10 years.

The example you mentioned about telecom is nothing specific to LTTS or the industry they operate in. Its a normal phenomena across industries. If your customer decides to do captive there is nothing much you can do. I am going through one such transition personally right now after having a close to 17+ years of relationship with the customer.

Coming back to Medical, LTTS is definitely a first mover there at least among its Indian competitors. They have been growing in that segment since last 2-3 years and that has lot of steam left. EU medical regulation changes and Tele-Medicines getting traction in post COVID world will give enough opportunity to LTTS and other companies in that field to gain business rapidly. You can watch #EngineeringForTheNewReality series of LTTS on health care and you will see how quickly things are changing there. In fact its a good series to understand their different verticals and how they are preparing themselves for the new normal.

@sahil_vi ER&D spend of some of the LTTS customers have been flat in last two years. However, they are big enough for you to get business. Post COVID, spend is expected to rise in Media and Entertainment (Work from Home), Medical Devices (Tele Medicine) and Plant Automation. Where as we may see some short team hiccups in Transportation and Process engineering.

For ER&D spend, you can refer Zinnov consulting reports and go through annual reports of some of the LTTS customers.

For the last year AGM issue you highlighted, even though that was not a welcome move, LTTS does regular con-calls where questions are answered in detail. They are very prompt in sharing business updates as well.

Insightful article on whats happening with LTTS in transportation and connectivity business. They are opening a EV testing lab in Bangalore which will be able to test almost all EV components.