If you go through this thread from the beginning, many forum members kindly shared their research and views about this company. From these and based on your own research, you may arrive at your own conclusions.

Is there any chance for rebound?

Nobody in this forum wants to (or can) predict pricing trends. We want to mainly focus on just two things: Understanding this company’s story, and its future prospects.

I have bought these shares at higher levels

What are your views about the company that made you invest at higher levels? We would appreciate if you can share your research or thoughts behind this investment.

Some pharma grapevine that Kwality Pharma continues to manufacture counterfeit/spurious medicines and exports to Africa and Mid-East. I knew of these types of bribery issues in the past, but you would expect them to learn from these types of transgressions (if proven)

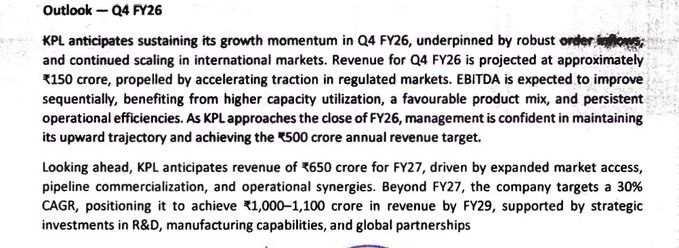

Outlook for FY 23

The company is lowering its revenue guidance to Rs 300 cr while it expects the EBITDA margins

will increase to be in the range of 24% to 26%. It expects its R&D driven complex injectable

portfolio, new partnerships & product registrations and expansion into new geographies will

drive growth in the coming years.

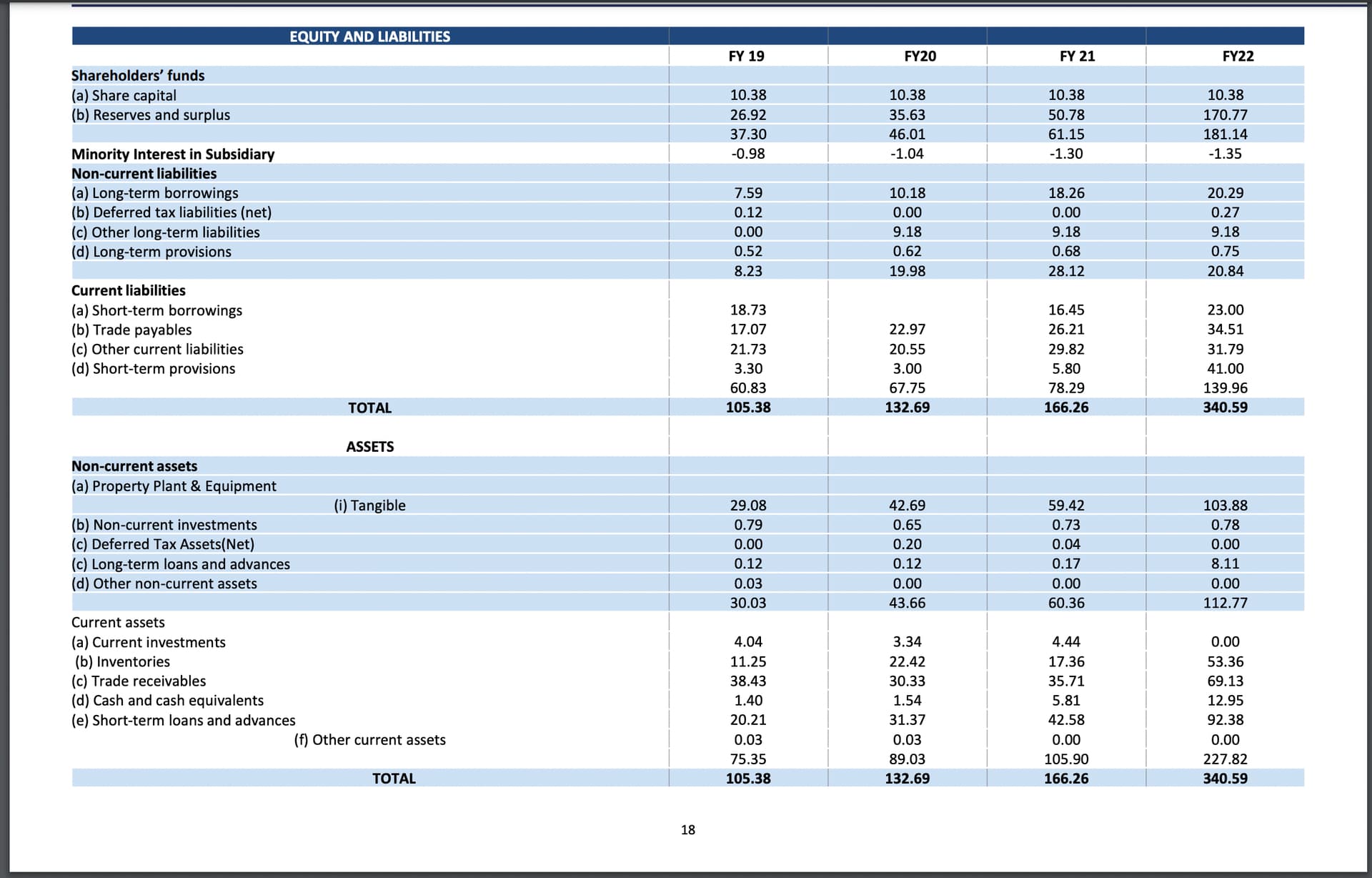

The biggest redflag for me in this company is the cash flows ,despite earning 115 rs a share ,no amount of money was distributed as dividends and same has been the case for the past many years.

Why do you need capex ,if the revenues are falling.

Disc :no positions just tracking as how the stock pans out in the coming years.

I would’ve thought the owner getting arrested for bribing officials (2019) and company continuing to export counterfeit medicines would be a bigger red flag

I had bought some shares today. Quickly got out after reading the report of the MD’s arrest. What has been dinned into us as the first mantra of investing is: quality of management matters.

One can’t invest in a company whose MD gets arrested (unless he was falsely implicated), and expect to be treated decently. A chor is a chor.

This is the gist of the report:

Those accused in the FIR are inspector Ankur Bansal, Kwality Pharmaceutical Limited managing director Ramesh Arora, its director Ajay Kumar Arora and chief pharmacist Karunakar Tiwari, besides unknown public servants.

The CBI registered the case following a source information about alleged conspiracy between certain CDSCO officials, working under the Health & Family Welfare Ministry, and owners/representatives of companies manufacturing drugs to manage adverse test results.

I read the whole discussion. The only thing that cries for attention is @Aarti is pushing this company with all efforts. I see a dumping process in progress,when I check the charts. So, its a no-go for me. Following for educational purposes.

i find certain red flags in this high growth and cheap valuation pharma business. Their working capital cycle has doubled in the recent past and almost 50% of sales are in the form of receivables, I think most of the sales are stuck there. doesn’t exude confidence to me. Anyone can clarify on it

Company has successfully obtained SFDA GMP (Good Manufacturing Practice) approval for two of its manufacturing units in Amritsar.

These units produce various pharmaceutical products, including generic sterile injectables, lyophilized injectables, beta-lactam sterile products, and dry powder injectables.

Company has successfully received regulatory approval in Mexico to sell and distribute Cyclophosphamide 1gm, a cancer treatment drug.

What is Cyclophosphamide? (For a Non-Medical Person)

Cyclophosphamide is a chemotherapy drug used to treat various types of cancers, including leukemia and lymphoma. It works by slowing down or stopping the growth of cancer cells in the body.

Additionally, it is sometimes used for treating autoimmune diseases like rheumatoid arthritis or lupus, where the immune system attacks the body’s own cells.

In simple terms, it is a powerful medicine that helps kill harmful cells (whether cancerous or immune system-related) and is now approved for use in Mexico by KPL.

This video is the FY24–25 AGM of Kwality Pharmaceuticals Ltd, where management and shareholders discuss growth plans, capacity expansion, and guidance.tunestotube

Business performance and guidance

Management reiterates confidence in achieving a ₹500 crore topline by FY26 with EBITDA margins of about 20–25%, driven mainly by exports rather than domestic sales.tunestotube

Beyond ₹500 crore, the company targets ₹700–750 crore revenue with margins rising toward 25–30% as operating leverage kicks in, and sees potential to reach around ₹1,000 crore by FY29 if product registrations and biologics scale up as planned.tunestotube

Capacity expansion and capex

Over the last two years, capex was about ₹30–35 crore, largely supporting registrations, dossier development, and R&D rather than big greenfield projects.tunestotube

Over the next two years, planned capex of roughly ₹70–80 crore will focus on completing the hormone plant, expanding oncology capacity, and funding biologics development and clinical trials.tunestotube

Regulatory approvals and new plants

EU-GMP auditors could not visit earlier due to inspector shortages, so oncology and cyclosporine plants received an extension of EU-GMP validity to July 2026, with a fresh audit planned in October that will also cover the general and beta-lactam plants; management expects four facilities to get renewed approvals by October-end.tunestotube

The dedicated hormone plant is expected to be mechanically completed by April–May next year, with local FDA manufacturing license and pilot/stability batches by May, followed by WHO-GMP and commercialization around August–September.tunestotube

Products, markets, and mix

The company has filed several niche molecules for Europe (including oncology and peptide/complex injectables) and already replied to queries from some EU agencies, expecting the first European registrations by late FY25.tunestotube

Near-term incremental growth is expected to come more from Mexico and Colombia, where multiple registrations are in process and together could add about 10 million USD (roughly ₹80–85 crore) of sales and eventually 25–30 million USD over two years.tunestotube

Biologics and oncology roadmap

In biologics, three products are under development; the lead molecule erythropoietin is in advanced clinical stages and is expected to complete clinical study by November–December, allowing commercialization by year-end, while the other two are in stability and preclinical stages.tunestotube

Management believes erythropoietin can generate ₹150–200 crore annual sales by FY27–28 under a moderate scenario, with long-term upside toward ₹500–1,000 crore if global registrations succeed, citing an edge from having followed post-2016 guidelines unlike older Indian competitors.tunestotube

Portfolio, margins, and working capital

Current top five products (including liprolyte and propall) together contribute about 15–20% of sales, with liprolyte alone expected to be around 5–6% of a ₹500 crore topline; the overall product mix is stable and is expected to shift once biologics scale.tunestotube

Around 40% of revenue comes from injectables, which carry roughly 25–30% EBITDA margins excluding some lower-margin beta-lactam and cephalosporin injectables; receivable days, currently ~150, are guided to normalize toward 110–120 days as post-Covid terms stabilize.tunestotube

Shareholder engagement and closing

Shareholders request more frequent investor interactions such as half-yearly calls and facility visits to understand the evolving biologics and regulated-market strategy, and management agrees that investor relations will be a key focus going forward.tunestotube

The meeting closes with reminders on e-voting, confirmation that unanswered questions can be sent via email to the company secretary, and thanks to shareholders, directors, auditors, and invitees for their participation.tunestotube

the main issue with the stock is there are no institutional investors. they should come in when market cap increases to 1,500 cr. but the challenge is there is not much free float available for them to buy. this is a peculiar issue with this stock.

In the investor call Kwality Pharma has reiterated guidance of 650 Cr sales in FY 27 at 25%+ margins and will reach 1,000 Cr+ sales by FY 29 at ~30% margins. This is at 50% success rate of sales pipeline. Implying will reach 100Cr profit next year and 200Cr by FY29