History

Started in 1983 when its founder Mr. Ramesh Arora was inspired to begin his own venture leaving behind the already flourishing family business of spinning and aromatics. With little background of finished pharmaceuticals and high held spirits and will, he started this business.

He received his first drug license in 1981 approved for liquid oral manufacturing. Climbing ladder of success, till date, Company has 48 different sections available at their production centres.

In the time span spread over a quarter of the century, the Company has not only established world-class quality standards but also has been able to offer customized products to their vast clientele spread across the globe.

What does the company do?

Kwality Pharmaceuticals Ltd. is a manufacturer of finished pharmaceutical formulations in a dosage form. It is a leading manufacturer & exporters of pharmaceutical formulations in Liquid Orals, Powder for Oral Suspension, Tablets, Capsules, Sterile Powder for Injections, small volume injectables, Ointments, External Preparations, ORS and many more… in various categories like Beta Lactam & non-Beta Lactam, Hormones, Cytotoxic (Oncology) and Effervescent as per new GMP norms.

The company specializes in handling customized business as per the requirements. The company has registered its products in different countries of Europe, Africa, Asia, Central American, and South American Countries & CIS Countries.

Company market capitalization: Rs505 crs

Shareholding structure

Promoter holds 54.43% stake and has been constantly increasing stake post Sep 2019.

Ashish Kacholia has been increasing stake in the company over last 3 quarters. See below

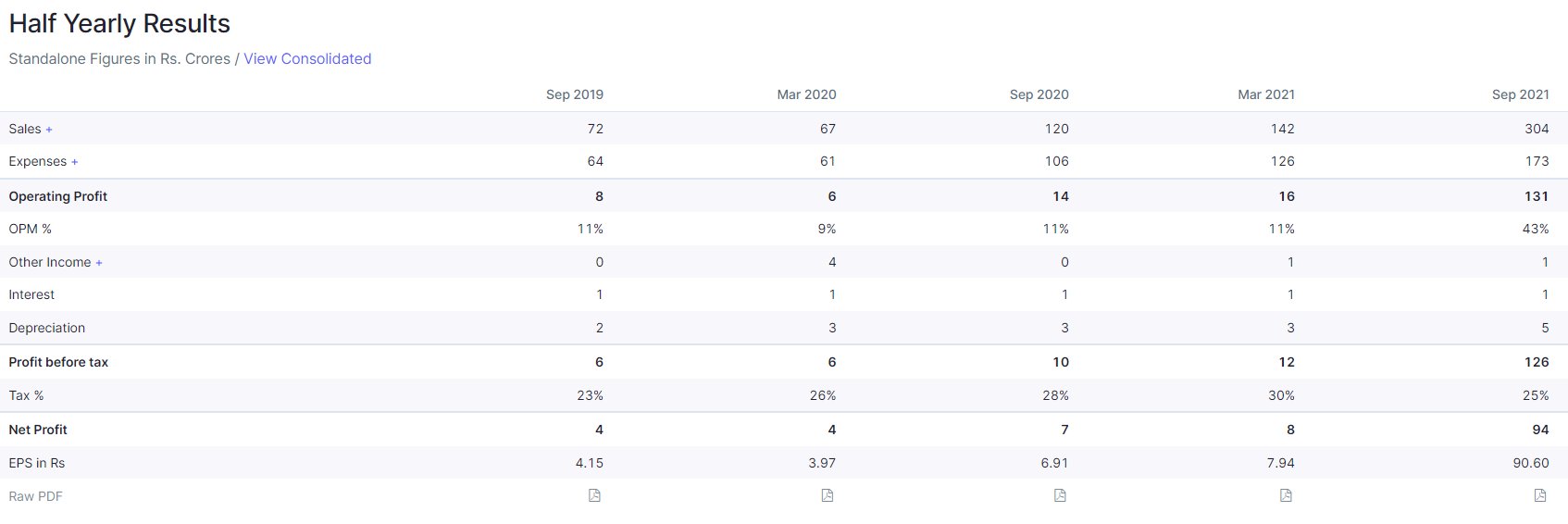

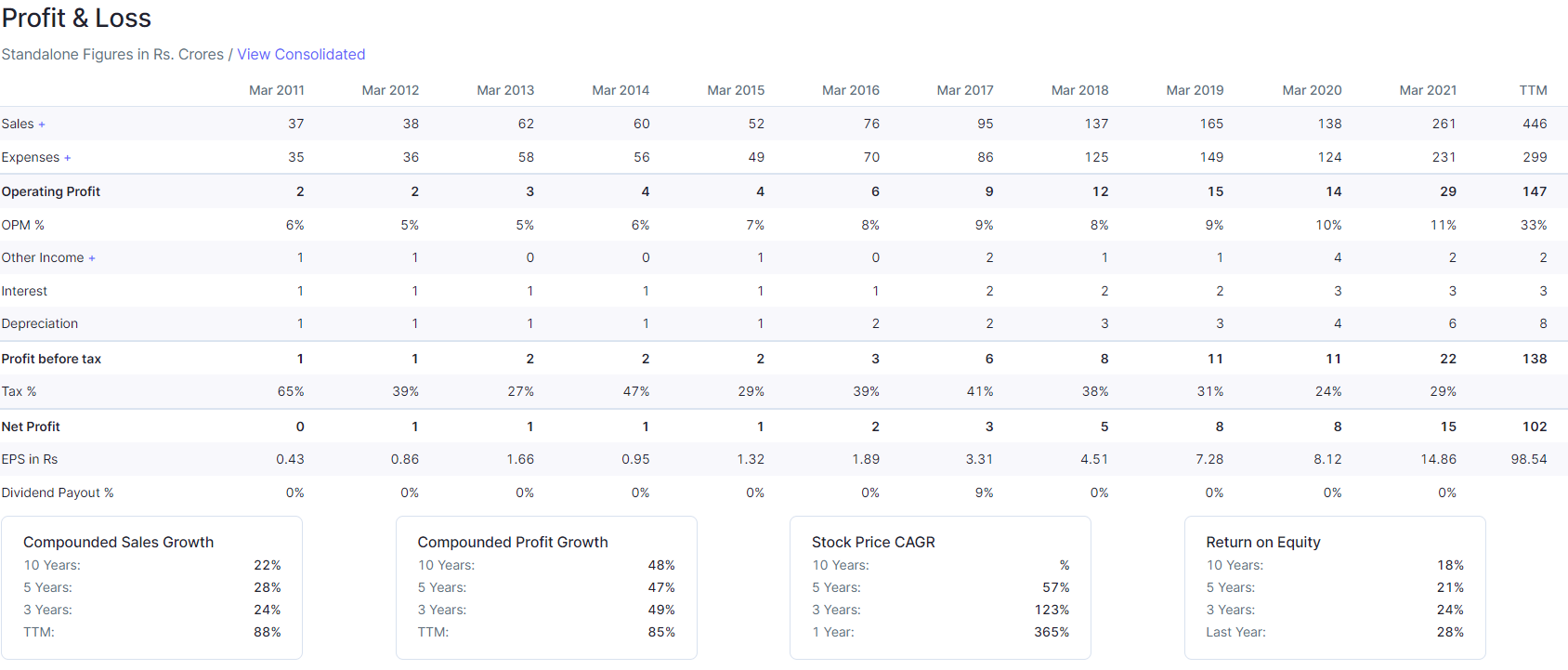

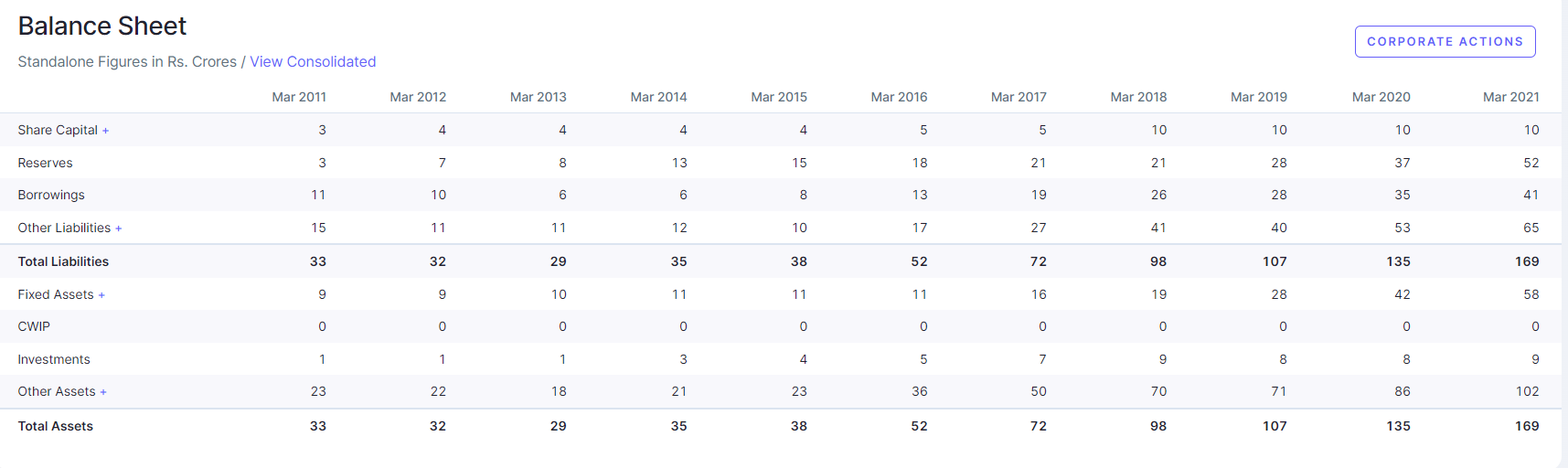

Financials

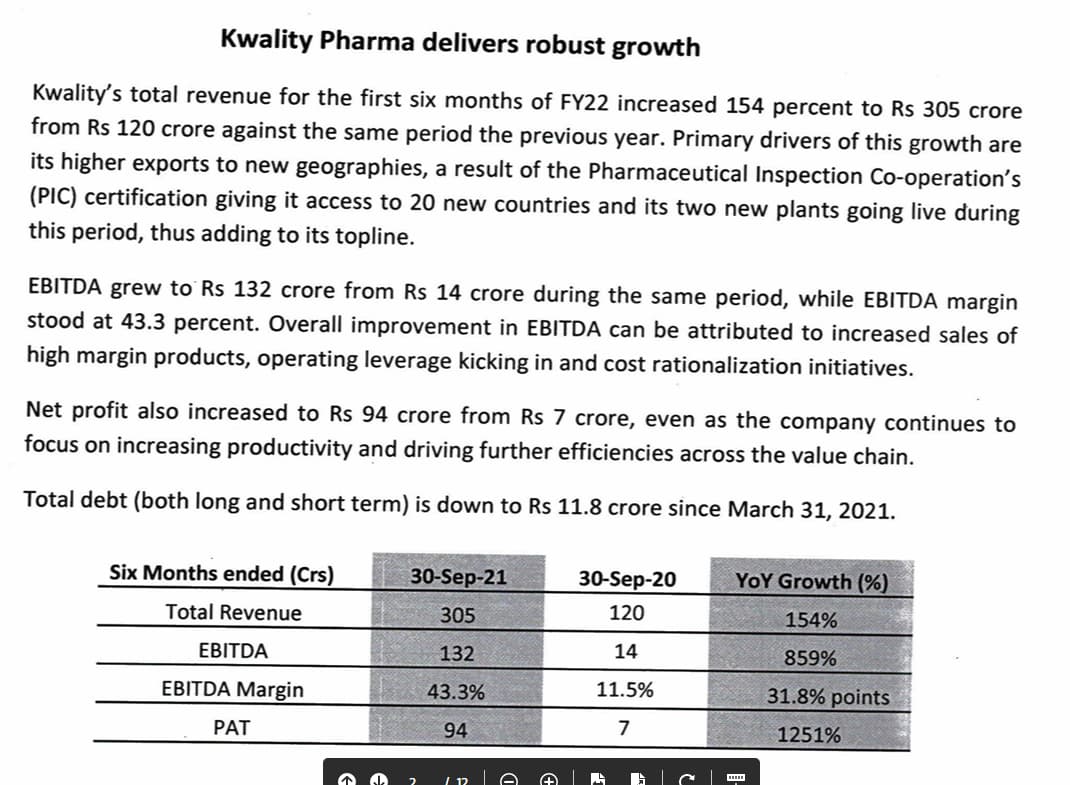

Performance in 1HFY22

Outlook for 2HFY22

If company repeats 1H performance in 2H as guided we are looking at profits of Rs198crs for the full year. Company’s market cap is Rs505crs which implies the stock is trading at < 3x P/E and looks super cheap and has the potential to be a multi-bagger

Key downside risks

- Information is limited on the company with no research reports

- Stock trades in lot sizes of 200 and is illiquid

- Company could potentially be impacted by rising raw material prices

Corporate Video

Disclosure: Invested

5 Likes

Thanks for starting this off… as you’ve mentioned practically no information in the open domain except Ashish Kacholia has invested.

Read elsewhere that practically this is due to Remdevisir exports related to COvid. (Thanks to Remdesivir, Kwality Pharma’s stock is up from ₹59 to over ₹922 in just over nine months) Maybe a one-off sales. And with Half yearly reporting there is less communication from management except stating that order book gives confidence for repeat of historic H1 performance.

1 Like

I don’t think 1H was one off because of remdesivir exports. Otherwise the company would not have guided for similar numbers in 2H. Also please note the key risk they highlighted for 2H was covid related disruption.

If 1H was covid led then shouldn’t covid be a positive for 2H rather than a risk?)

Please read the link I’ve shared above. It’s primarily due to export of Remdesivir sales is what I infer.

Extract from the article,

Kwality Pharmaceuticals as an exporting company has supplied Remdesivir Injection to the global market… The sale has gone up and it will keep on growing as many traders and the government have come to know about the medicine(s) of Kwality Pharmaceuticals.The company has also improved the infrastructure and plant & machinery which can meet the global demand,” the company said in its annual report.”

Management chose to highlight sales of one drug.

Please correct me if I’ve inferred incorrectly.

I’m cautious as the shares of several pharma players who very in the right segment addressing Covid malady like Paracetamol or Ibuprofen have corrected.

1 Like

“Kwality Pharmaceuticals as an exporting company has supplied Remdesivir Injection to the global market…The sale has gone up and it will keep on growing as many traders and the government have come to know about the medicine(s) of Kwality Pharmaceuticals.The company has also improved the infrastructure and plant & machinery which can meet the global demand,” the company said in its annual report.

This is mentioned in the annual report and talks about sales for FY21. Look at the press release for 1HFY22 which talks of they are confident of repeating 1H performance in 2H. Was 1H because of Covid. Will 2H be because of Covid I am not sure. Let’s wait and see the results.

1 Like

Yes… let’s wait and watch… and hope management gives an interview or MDA in AR throws light…

2 Likes

Promoters bought from the open market in the month of Feb 2022, increasing their holding by 0.19% to 54.43%.

Disclosure: Invested.

On this… I’ve a rather generic query… wondering how much increase in promoters stake deserves attention

1 Like

The buy price in Feb 2022 is around the current prices. Some buying by promoters is much better than nothing. It means that the promoters expect to make money by share price appreciation even from these levels. Even 0.19% is a huge number of shares. It would be great if the promoters buy again—this will make the support at the current levels stronger.

I’ll put it this way…. I’ve read elsewhere that since increase in promoter holding is always watched it maybe used by unscrupulous management as more of a bait for gullible retail investors, thus masking the intent… hence my query as to what quantum would signal a real intent

1 Like

My apologies for droning on the same issue… I’ve checked with a doctor friend who said that Remdesivir demand dropped after the 2nd wave in April May 2021. So I’m wondering how a company got into export business after the bus has taken off. And even if that’s true… will this be a secular trend which can extend beyond FY 22e

2 Likes

more of a bait

Quite possible but they would do better to buy around 800 levels around the end of the previous calendar year, not 450. There is no rule that works unqualified in the stock market, and this applies to promoter buying as you suggested. Ultimately it comes down to the investor’s calculation of the risk-reward and willingness to speculate.

This particular stock definitely comes under speculation (at least for me) given the lack of information about the products and manufacturing facilities in the public domain.

1 Like

I did further investigation into the company.

-

Web search reveals an order by Bureau of Pharma PSUs of India blacklisting Kwality Pharma for 2 years.

-

The company seems to have been blacklisted by or in trouble with Kerala and Odisha State Medical Corporations as well.

-

This 2012 news suggests that forged certificates were involved. No data from the company can be believed if forgery is involved.

My views have changed drastically due to the above. I think it is best to exit and I will do so.

17 Likes

Kwality Pharma has received approval For Migration Of Company From BSE SME Platform To BSE Main Board.

34b10ff2-e82b-4030-84d3-db6be79e168d.pdf (481.5 KB)

Since we have the complete picture for FY 2021-22, did a little digging on publicly available info on this company

- Didn’t read MDA before commenting on this company, in the earlier post

Annual Report:

Financial Year 2020-21 has been a challenging year for the company where COVID-19 spread globally. Kwality Pharmaceuticals Limited as an exporting company has supplied Remdesivir Injection to the global market and similarly Propofol injection was short in supply in various high profile countries who normally accept US FDA companies’ products. But in shortage of medicine, they have procured these injections from our company and after seeing the performance and efficacy, they registered the product of the company. The sale has gone up and it will keep on growing as many traders and the government have come to know about the medicine(s) of Kwality Pharmaceuticals Limited. They also started procuring the other items of the company. The company became world recognized and now the booking has been growing which may yield more sales and more profit. The company has also improved the infrastructure and plant & machinery which can meet the global demand. The various new R&D projects are initiated."

So Remdesivir is the topline driver and possibly even the bottomline… with Covid receding… except for pockets like NZ or China, repeatability is anybody’s guess.

- H2 & H1 results of FY 2021-22

management over-guides and under-delivers…

While releasing H1 results, management believed it can repeat its H1 performance (Sales - 330 cr; EBIDTA - 132 cr; EBIDTA margin - 43% PAT - 94 Cr) in H2 aided by (a) Strong Order book; (b) Commissioning of 2 new plants.

Cut to H2 results and the results.

(Sales - 152 cr; EBIDTA - 41 cr; EBIDTA margin - 27% PAT - 26 Cr)

Sales down by 50%, EBITA by 66% and PAT by 72%. The results are no way closer to the projections.

But there’s no candid discussion on why the projections went haywire. Instead the commentary shifted from H-o-H to Y-o-Y, which is optically appealing due to exceptional H1 performance, sustainability of which appears doubtful now.

and even the reasoning behind the excellent H1 performance varies:

@Oct 2021: Higher exports due to PIC certificate access to 20 countries and 2 new plants.

@May 2022: Increased exports to new geographies and sale of COVID products in H1.

- But a few major ponderables which flew under the radar…

i) No. of employees. 500 (March 2021); 1000+ (Oct 2021) and 1500+ (March 2022).

ii) Fixed assets trending up… 103 Crores up from 60 Crores in March 21.

iii) Inventory position (35 Crores) & receivables (35 Crores) shot up. may be in line with sales volumes.

iv) Long term loans jump by 6 Crores. may be 51% Mozambique subsidiary.

v) Short term loans jump by 50 Crores ???

vi) company has not co-operated with ICRA for the latest credit reporting. (red-flag)

Need to monitor Cash Conversion ratio.

With aggressive recruitment and doubling of fixed assets, company seems to be in expansion mode…

but P/E of 3.38 is misleading. If even accept H2 EPS of Rs. 25 as normalised (till March 2021 EPS in single digits) P/E immediately raises to 8. Considering that company operates primarily in Africa market (ICRA latest report), it is definitely not a steal. Relatively well known name like Lincoln pharma operating in similar markets trades at 8 P/E. Much well established Caplin Point Labs trades at 18 P/E.

expecting critical responses

10 Likes

the revenue visibility is precisely missing… and without guidance, wondering why would market acknowledge this stock over a Lincoln or a Caplin which are all trading at 9 and 18 PE. 15 PE for this unknown unpredictable stock when peers are trading at lower levels, the risk -reward ratio favours known devils… my thoughts… i may be completely wrong analysing this way…

3 Likes

Kwality Pharma,

Some of the Key Points (Thesis Pointers)

-

Undervaluation (as the market is perceiving it to be a COVID stock) according it’s FY 23 Sales estimate.

-

Their balance sheet size has doubled to 340 Crore (their market cap is at 392 crore)

-

Sales has been growing steadily Fy 21 sales 262 - Fy 22 Sales 315 ( without covid) - Fy 23 - 350 to 400.

-

They are reporting the better than industry margins as a formulation player (Talking in respect of Fy 23)

-

Brilliant fundamentals - Top of the class ROIC, PEG ratio, ROE.

5.Ashish Kochalia has been on continues buying spree and not only under his name but from his business firm’s name as well

-

Getting its products registered across new geographies - Pending approval by year end from Europe, Brazil and Mexico.

-

Currently 260 products are registered as mentioned in the Presentation and 140 under registration ( that is a growth of more than 50% in a year)

-

Due to their windfall profits from covid sale - now their are able to head to bigger markets which will also act like a catalyst.

1 Like

The company is now positioning itself as a specialised injectable player with advanced capabilities. How many of us believe that ?

1 Like

I read that there is going to be capex expansion but could not find timeline about its implementation. Can anyone throw some light on this? Has capex already taken place and revenues already now in statements? If not then when will capex come online and how much revenue will it add and when? @praveens

Hi @Aarti you mentioned that revenues will be 400 Crs in 2023. Can you please justify/elaborate on what basis you have arrived at this number?

1 Like