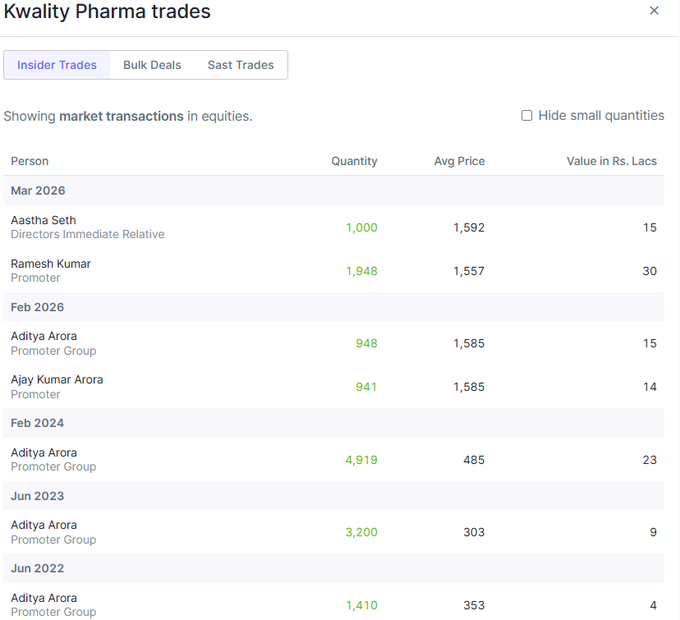

First institutional investment in Kwality Pharma by Ark Global Emerging Companies. As more institutions including mutual funds enter stock will be rerated.

09 Jan 2026: Deepak Bansal Sale 69,3531,122 Ark Global Emerging Companies, Lp B76,4001,130

With mcap at almost 1,500 cr hopefully mutual funds start buying leading to rerating of stock.

this may be correct as price has run up a lot in past few years.

however for medium to long term company is going to do well. my estimates of numbers based on management guidance are given below. With every quarterly result price should go up. Price could be higher if multiples are higher than 22 which i have assumed.

Thanks for sharing this. But one sincere request, PLEASE put conservative growth of say 15% and OPM of 20% and PE of 20 and then see how the market cap evovles.

Thanks once again. But of course, we can allow some margin of safety [MOS] (maybe 25% less) for sales and margins and calculate accordingly, if you don’t mind. Management will always try to give higher estimates. It’s we, retail investors, who should apply MOS, as we don’t know the ins and outs of the company.

Capacity expansion is being done through internal accruals - no/minimal debt. New capacity (Biologics) will take it to 1,500 cr turnover - please refer to the last AGM video - Aditya Arora mentions that Biologics will be 500 cr plus. they have not accounted for Biologics in the 1,000 cr guidance for FY 29.

Thanks for sharing this. I am just copying the summary generated by Comet Browser here. Hope you find it useful.

Kwality Pharma looks like a niche, high-ROCE, export-focused injectables player aiming to scale from ~mid-size today to a ₹1,000+ crore revenue, ~30% EBITDA business by FY29, with most capital intensity front‑loaded and guided PAT of ~₹100 crore by FY27.[youtube]

Snapshot: Business and Positioning

Core: Injectables and oral solids, oncology, cephalosporin, beta-lactam, hormones; largely export driven with domestic as a small, higher-margin oncology niche.[youtube]

Model:

Out-licensing in RoW (dossiers and brands owned by Kwality, sold via distributors).

CDMO for Europe (added as alternate site to existing dossiers).

Biosimilars/biologics (big optionality, not in base guidance).[youtube]

Edge: Multiple specialized plants, 800–900 products registered globally, strong regulatory machinery, and willingness to do bioequivalence (BE) where many Indian peers hesitate.[youtube]

Numbers and Timelines: FY27–FY29

FY27 revenue:

Guided: at least ₹650 crore, internal range ₹650–700 crore.[youtube]

Key growth drivers:

Mexico, Colombia, Algeria: ₹150–200 crore incremental by FY27.[youtube]

Better utilization in injectables and general tablets, oncology expansion, early hormone ramp-up.

FY27 profitability:

PAT: management explicitly guides to ~₹100 crore and calls it “100% expected.”[youtube]

EBITDA margin: ~25–26% at ₹650 crore sales.[youtube]

FY29 ambition (implied, not always hard-guided):

Revenue: ~₹1,000 crore (management repeatedly links margin targets to this level).[youtube]

Geography: Mexico/Colombia/Algeria alone could be ₹600–700 crore combined if 50% success rate on registrations plays out.[youtube]

Oncology: Three new lyophilizers; management talks of ~₹500 crore oncology sales potential by FY29.[youtube]

Cephalosporin + beta-lactam: ~₹200 crore by FY28.[youtube]

Hormones (Unit 6): Commercial around Sep–Oct 2026; ~₹200 crore revenue potential by FY28–29.[youtube]

Biosimilars: Very large capacity but kept out of formal revenue guidance due to pricing/regulatory uncertainty post patent expiries (around 2028+).[youtube]

R&D and Product Engine

R&D intensity:

Historically ~2% of sales; targeted 5–6% by FY27 to fund pipeline.[youtube]

BE pipeline:

Targeting ~40 BE molecules, aiming to be first/second generic in RoW and in some cases Europe.[youtube]

Plan to complete 60–70 BE studies before end-FY28 to support FY29 revenue.[youtube]

Organization:

~80-person R&D/regulatory team for out-licensing (doctors, pharma specialists, dossier experts).[youtube]

Biosimilar science largely outsourced (US cell lines, Gujarat scale-up, Kwality for final production).[youtube]

Capex, Balance Sheet, and Working Capital

Capex FY27–28: ~₹160–170 crore in total.[youtube]

~₹60 crore hormones plant.

~₹40 crore oncology expansion.

~₹20 crore for BE work (plant-related).

~₹40–50 crore for biosimilar clinicals and related plant over FY27–28.[youtube]

Funding: Largely internal accruals; management mentions only ~₹10–15 crore possible additional debt if cash flows disappoint.[youtube]

Working capital:

Currently >200 days, driven by ~150 debtor days (sea shipments, long approval cycles in importing countries).[youtube]

Aim: improve to ~170–180 days by pushing more business to Mexico/Colombia with faster payments and more air shipments.[youtube]

Inventory days already starting to decline as mix and throughput improve.[youtube]

Governance, Capital Allocation, and “Soft” Factors

Governance / comfort:

Plan to appoint KPMG as statutory auditor, likely from next financial year.[youtube]

Current “issuer not cooperating” rating is due to company not pursuing rating; they indicate willingness to get a proper rating next year.[youtube]

Listing and shareholder returns:

No dividend/bonus until scale and capex cycle are largely done; they explicitly say payouts are post-₹1,000 crore revenue and post capex (i.e., after FY29).[youtube]

NSE main-board listing considered around FY29.[youtube]

Track record vs guidance:

Acknowledge minor miss vs earlier quarterly topline guidance (₹124 crore vs ~₹140 crore earlier indication), attributing ~₹10–15 crore to holiday-season shipping delays.[youtube]

Stress that FY27 PAT ₹100 crore is realistic and already visible in the orderbook/pipeline.[youtube]

Risk–Reward Cheat-Sheet

Key positives (what’s interesting):

High-margin export injectables/orals franchise with strong RoW presence and growing European CDMO leg.[youtube]

Clear 3-year visibility: guided path to ₹650+ crore revenue and ~₹100 crore PAT by FY27, with detailed plant- and geography-level levers.[youtube]

Operating leverage: multiple underutilized blocks (general tablets, some injectables) that can sweat with the 40 BE products and new registrations.[youtube]

Optionality from biosimilars and hormones not fully baked into near-term guidance, giving upside if execution is strong.[youtube]

Management appears aggressive but numerate on capex sizing and debt discipline (prefers internal accruals, low incremental borrowing).[youtube]

Key risks / things to track:

Regulatory and registration risk: main execution bottleneck is speed of ministry/authority responses; even with strong dossiers, approvals can be slow and lumpy.[youtube]

Working-capital drag: 170–200+ day cycle structurally keeps cash tied up; thesis requires improvement via better geography/product mix.[youtube]

Concentration in a few new markets: a lot of FY27–29 growth narrative leans on Mexico/Colombia/Algeria ramping as planned.[youtube]

Biosimilar uncertainty: patents, pricing pressure, and regulatory timelines can significantly shift economics vs current assumptions.[youtube]

Execution stretch: managing six plants, 800–900 products, and 60–70 BE studies while scaling governance (big-4 auditor, rating, listing) is operationally demanding.[youtube]

In the call they also mentioned new markets like South East Asia. Export market is so large that 1,000 cr sales is not difficult at all.

Kwality has been successful in getting many regulatory approvals (even European) which shows their products are good. they have capacity to meet the 1,000cr target and also adding capacity to go beyond that.

one should visit Kwality pharma’s plants. My colleague has visited and found the plants very good.. and you can see for yourself the expansion which is happening.

*The successful study of Liposomal Amphotericin B is particularly significant. Liposomal formulations are complex injectables with high entry barriers and superior pricing power compared to conventional generics.

With Bioequivalence studies being successful, they can increase sales to regulated markets at high margins. Once US FDA approval (for vet products) is obtained sales and margins will improve further. I hope they go for US FDA for human drugs as well which will open a huge market for the company.

One important point is company has not factored in sales from Biologics business in the guidance given. they are increasing capacity of Biologics from 100KL to 600KL. this it self can add 500cr sales (was mentioned by Aditya Arora in AGM). So if we include biologics sales can go up 1,500 cr and so EBITDA at 450 Cr (30% margin)… PAT of ~300cr. mkt cap 6,000 cr.

Request others to share their views on the numbers i have projected. thanks.

PS - once mutual funds start investing this stock will get rerated.