Following on from previous posts, one goal in this thread has been to chart out the landscape of tenders that are currently being floated by the government. @Deenar_Toraskar has done fantastic work on finding a number of them.

Key points:

The current tender landscape is around 600 Cr. conservatively. These tenders close by the end of the month, and should be awarded in 2023.

Rajasthan is the largest tender at 200-300 Cr. Following this is a large pathology contract in Odisha worth around 100 Cr., and a couple of smaller tenders worth 50 Cr. each.

Cancellations of tenders and subsequent re-tendering happens all the time for various reasons. We found 3 tenders on this list that are up for re-tendering. One in particular has been in the works since 2020.

Therefore even if things are up for re-tendering, it’s fine. There are many on the table at any given moment.

There are lots of smaller tenders in the 5-25 Cr. range that individually add up to around 100 Cr.

This is a work-in progress sheet. It will be updated when we find more details.

Assumptions in value: I’ve assumed each CT scanner gives around 3 Cr. of revenue, and each MRI gives around 2.5 Cr. of revenue. Pathology tenders are harder to ballpark, but have been done by reasonably extrapolating from Rajasthan data that we had above, and comparing the number of district hospitals in each contract, and the population of each state.

Tenders won in 2022, to be implemented

Largest win has been the operation of 39 CT scanners in Maharasthra, providing around 100 Cr. of revenue.

Uttar Pradesh contract is second largest at around 20 Cr.

Himachal Pradesh path contract is statewide, but I assume revenue is not very high as HP is not a populous state.

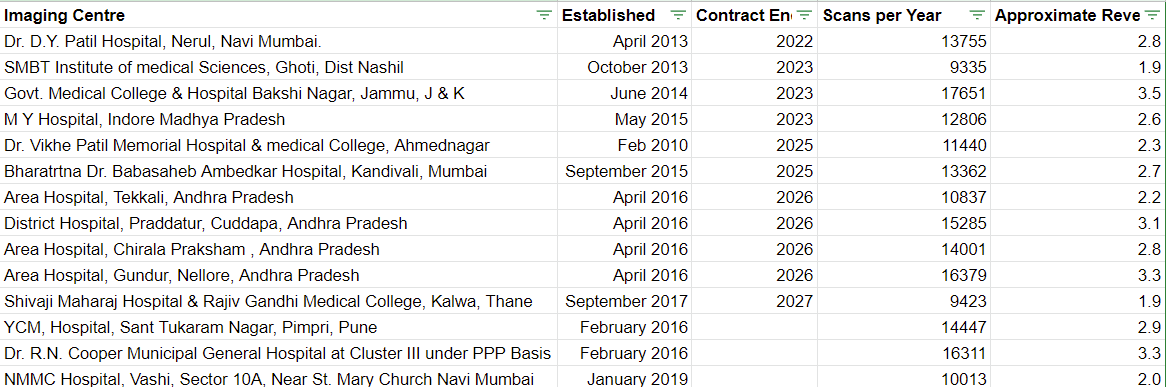

I have found Krsnaa’s yearly throughput for some existing CT scan centres, along with dates of when contracts end.

The median number of tests done per year is around 13,500. At Rs. 2000 per test, this comes out to around 2.7 Cr. of revenue per CT machine, and around 36 scans per day. (Further points to my assumption on CT revenues being in line.)

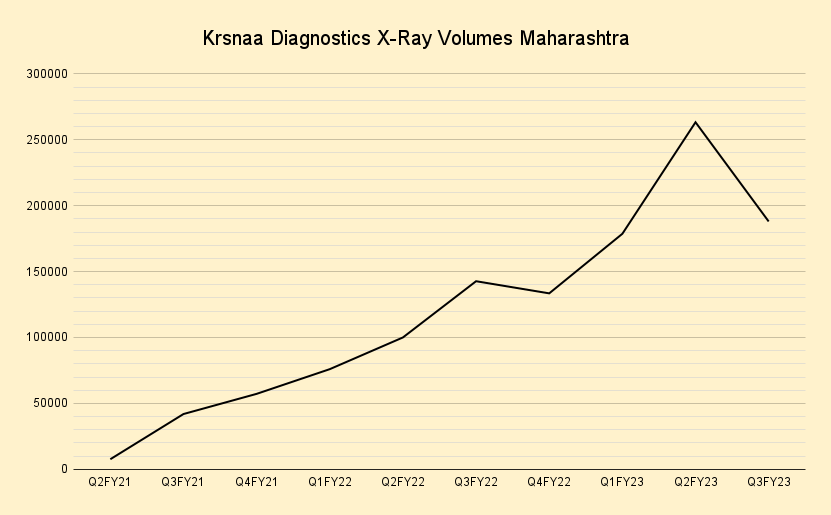

Note Q3FY23 data is current, as of 3rd December 2022, and therefore the quarter looks weak. At this run rate, quarter will end at around 300,000 tests.

District

Q2FY21

Q3FY21

Q4FY21

Q1FY22

Q2FY22

Q3FY22

Q4FY22

Q1FY23

Q2FY23

Q3FY23

Total

7604

41901

57211

75959

100016

142688

133476

178694

263327

188033

AHMEDNAGAR

8

888

1050

1400

2238

2524

2484

3569

4633

2936

AKOLA

1

1013

1170

1700

3621

4359

3341

3680

7943

3755

AMRAWATI

5

1677

3139

3624

5587

6776

6259

8113

11078

6161

AURANGABAD

3

3190

2662

2336

3724

3992

3929

5984

9504

6597

BEED

7

225

576

686

1569

3307

3346

5502

8254

5706

BHANDARA

19

36

265

537

1486

4213

1622

1858

2799

2262

BULDHANA

9

475

984

1128

2410

2690

3101

2926

7397

6212

CHANDRAPUR

313

1981

906

1423

3372

6763

4817

7206

9023

6212

DHULE

1

206

427

433

1275

1847

2276

2983

3394

2388

GADCHIROLI

305

653

1287

2180

2934

4169

3129

3650

7209

6053

GONDIA

118

439

543

594

1629

2960

2015

2796

3120

2153

HINGOLI

6

383

472

724

783

1429

1198

1484

5009

3515

JALGAON

16

850

1034

981

1324

1457

1249

2054

3299

2594

JALNA

2

3732

2114

2433

2248

4228

3730

4997

8089

6561

KOLHAPUR

11

3670

3707

3717

4231

7593

7208

8984

14078

9853

LATUR

2

895

1626

2451

3928

4923

3918

6005

8498

4011

NAGPUR

2

461

885

904

1862

4154

4006

5334

6894

4310

NANDED

126

997

1578

1698

2016

4354

4100

4854

6853

4589

NANDURBAR

19

121

1040

844

1410

2012

1512

1458

1885

2250

NASHIK

1738

2519

3051

3200

6791

8151

8888

11931

16079

13522

OSMANABAD

4

513

907

1799

2745

4346

2581

3796

7122

5551

PALGHAR

2

133

869

752

1190

2842

3374

3859

5625

4433

PARBHANI

2

66

341

1930

998

2153

1728

2336

4095

3069

PUNE

18

2257

4232

6337

5518

7236

9512

13262

18708

12823

RAIGAD

1227

1557

3205

3852

3662

4197

3271

4270

6125

4934

RATNAGIRI

2009

1834

2020

2572

1752

1674

1846

2441

3554

3167

SANGLI

0

1060

843

2508

2524

5587

4341

8060

13611

4940

SATARA

2

988

1753

4109

4184

3838

3210

6634

11946

9685

SINDHUDURG

1243

3514

3925

4985

4439

4426

5350

5400

6968

5632

SOLAPUR

3

571

700

410

870

2872

3711

6324

8593

6337

THANE

345

3116

6056

6917

7692

9162

10677

12341

13985

11872

WARDHA

36

898

2025

2723

4962

6404

4649

5927

7563

5907

WASHIM

1

703

718

1907

2723

2896

3300

3996

4641

3680

YAVATMAL

1

280

1101

2165

2319

3154

3798

4680

5753

4363

I have found teleradiology data for 8 states, will compile and upload when I work on this again.

All the data we have is compiled at the following sheet:

Disclosure: Invested, Krsnaa forms 10% of my portfolio.

Thanks for this detailed research. The last concall, management mentioned that the combined optimal revenue for Maharastra + HP + Punjab is 100 Cr. annually. Do you think it is conservative guidance, or are we missing anything?

I think investors need to ignore management guidance and just look at the data. This is a company for which there is quite a lot of data publicly available, but not many people are working on it.

Punjab has 25 CT centres. In general, mature CT centres give around 3 Cr. of revenue. This adds up to 75 Cr. potentially from these centres.

An MRI machine adds around 2-2.5 Cr. of revenue. Punjab has 6 of these machines. That’s around 12-15 Cr. of revenue.

Adding all of this up, 100 Cr. from Punjab + HP Pathology + Maharashtra is very reasonable. By my own calculations, I think it is conservative, and they should be able to do 130 Cr. from these 3.

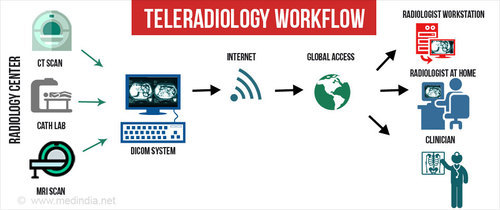

Teleradiology is where X-rays or other scans (like CT, MRI, etc.) are done at local hospitals by technicians. These are then scanned and digitally transmitted over the internet to a central server usually on the cloud. Then the radiologists at Krsnaa’s teleradiology hub (or working remotely) analyse and interpret the images and prepare a report. The report is then sent back to the patient/prescribing doctor.

Usually in this model Krsnaa provides the imaging equipment, scanning operators, and connectivity to their hub at each tele-reporting centre. The scans are the responsibility of the local hospital.

For tele-reporting contracts, the MRIs, CT, X-ray equipment, and their scan operators are the responsibility of the hospital, not Krsnaa. Only the image/scan digitisation equipment and the operator of this equipment are the responsibility of Krsnaa.

Great input.

Right now I understood Krsnaa made 10% of their revenue via Tele reporting.

However, this has the potential to grow as more Private / government hospitals go towards this model.

One of the interesting thing to note is the number of radiologists (2087) , Total colleges- 329 coming out every year in the country.

The NEET score for Post Doc Radiology is very high and most likely the students who pursue that will prefer to stay in cities. From my point of view the TeleRadiology can act as a operating leverage due to the shortage of doctors

Source: MD Radiodiagnosis - MBBSCouncil

I have just starting analysing Krsnaa diagnostics. Can you please let me know where to get data on revenue for FY23 and expected revenue for FY24 from different states?

Hi Bhavana,

Till Q2FY23 quarter wise revenue, you can get it in screener / Quarter results published by the company.

For the expected revenue you can go through the concalls where the management provides some information

Regards

Gourab

Currently the stock appears to be undervalued at ca. Rs.460 and can be bought for long term. The company is making the right moves. All of the diagnostic sector is under pressure. Time to accommodate in large quantities if possible.

The equipment is owned by Krsnaa and the long term AMCs are awarded respectively almost immediate. The downside of equipment is limited as all the machines are from high end branded players with long term warranty- where available.

I know some of the operators are on Krsnaa payroll, but I am not sure if that’s the case for every operator.

the ramp-up of operations in the new centres shall remain a key monitorable.

capex plans of over Rs. 100.0 crore in FY2023 for setting up new centres.KDL is also exploring asset-light expansion (pay-per-use or deferred credit from original equipment manufacturers) over the near to medium term.

KDL’s high debtor days with ~70% of its debtors being receivables from various Government entities. The debtor days improved to 46 days as of March 31, 2022, from 69 days as of March 31, 2021, backed by improved collection from Government debtors. However, its debtor holding period remained at 88 days as of September 30, 2022, in line with the cyclical trend in Government receivables witnessed during the fiscal.

KDL’s established position in the PPP segment mitigates the competitive pressure to a certain extent.

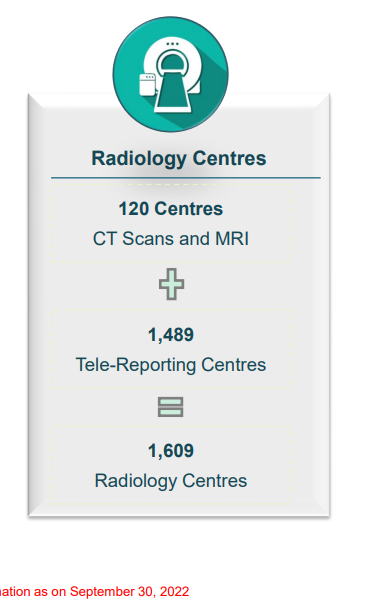

The company has an established market position in the PPP segment with over 2,020 diagnostic centres across 15 states and two union territories (UT; Delhi and Chandigarh) in India. KDL also has tie-ups with private hospitals and operates 27 centres under this segment (as on September 30, 2022).

OPM improved to 28.9% in FY2022 from 23.8% in FY2021, backed by significant improvement in the core business. During H1 FY2023, additional manpower costs for the newly launched centres (which is yet to fully ramp-up) led to contraction in OPM, while remaining healthy at 24.8%.

As on September 30, 2022, the company had over 45 active PPP contracts, with the contract tenor ranging between 3-12 years(including renewal clauses). Additionally, the PPP contracts have an embedded price escalation clause (mandating yearly price increases of 2-7%), which is expected to support the realisation levels, going forward.

The company witnessed a healthy bid-win ratio of ~78% in the past four years and the same is expected to remain healthy going forward as well, backed by its strong market position.

60% of its revenues coming in from western India. With new centres in Punjab, Himachal Pradesh, Uttar Pradesh, Maharashtra, Tripura, Chandigarh, Rajasthan and Delhi expected to generate revenue from FY2023-FY2024, the geographical diversification is expected to improve, going forward.

The company derives ~73% of its revenues (FY2022) from the PPP segment.

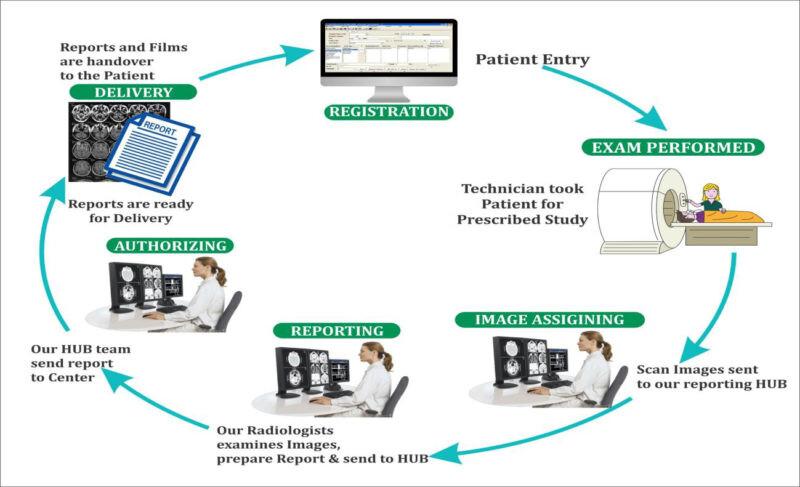

The company operates a teleradiology hub in Pune with a team of over 200 radiologists. This addresses the shortage of fulltime doctors and staff in the diagnostic industry, and considerably increases the turnaround time for diagnostic test reports. In addition, it also allows KDL to serve patients in remote locations where diagnostic facilities are limited.

This looks like a Krsnaa B2C franchise. It will be useful to track progress and how much this contributes to the top and bottom lines in the coming years.

Concall extract Q4 21-22 : 'Looking ahead we are confident that we will be able to maintain our growth momentum and therefore we have started a clear strategic roadmap to double the revenue and triple the profitability in next two to two-and-a-half years."

Management had guided 40% growth for next 2 to 3 years vis a vis flat growth delivered during first half year. Management needs to be more realistic in its guidance.

Constant selling pressure is visible in the stock price.

Disclosure : Exited my positions at around 500.