since delay in pubjab project, i think Q2 will also be a muted quarter. Unless any drastic thing changed. and IT raid is also still under investigation

1 Like

The management seems aggressive in sharing the guidance like x2 Rev and x3 Profits. It is still unclear to me how the Assam contract can impact the overall realizations, and I don’t buy the reasoning on that front. Then there is a risk of this raid on the investor sentiments.

The only positive which I can derive is looking at the peer comparison to the likes of Lal path and thyrocare; even though the nature of our business is not precisely similar, the topline and margins impacts are significant there. In comparison, our business was more resilient owing to the growth in the core business. I also understand some ambiguity concerning realizations with the test counts, but the management has still not changed the 2024FYE guidance. So I guess, I lack some understanding of the business, and any interpretations or opinions are well appreciated.

Disc. Invested.

3 Likes

Based on discussions of ICRA with Management, no adverse impact on credit rating as yet - https://www.icra.in/Rationale/ShowRationaleReport/?Id=113737

1 Like

Some additional pointers from the con-call (including forward looking statements as this might be helpful in evaluating walk the talk by management),

- Assam realisation issue - Realisation is low due to reason of low bidding which was done to match the lowest price (regulation issue by the government). This low bidding was feasible only because there is no need for capex on equipments and setup which was done as a part of previous tender win which lasted 5 years. The realisation going up from Assam is not mentioned and the realisation is expected to go up from contribution of other states.

- Punjab Business - Delays due to setup not being completed in time (eg. electricity connections, etc.{Reasons including change in Govt. in PJ}). This led to a delay from being total implemented in Q1 to being delayed to Q2 or Q3 atleast. Revenue growth is steep from Punjab (“we have started off with just a mere 50 lakhs on a quarterly basis, it has almost gone up to three crores per month”). Peak revenue expected from Punjab projects - INR 100 Crore annually (Expected - 6 months after all centers start running)

NOTE - Delays in Punjab projects has changed the revenue growth forecast from 30 - 40 % to 20-25%

3.INR 100 crores incremental revenue from non- punjab projects

4. Rajasthan Tender (Big project / More competition compared to other bidding tenders) - 3500 collection centers. Annual revenue expected - INR 200- 300 crore.

5. Non PPP projects - 20 such establishments in Maharashtra. Rolling of this current model in states of Rajasthan and HP for the second phase. Projects being taken up in Punjab as a part of phase 1.

6. Revenue breakup in between direct payment from patient / payment from Govt. authorities - 30 % / 70% respectively. Debtor days are in check due to timely payments from govt, authorities.

7.Guidance of 2x revenues by the end of 2 years - Current operational centers will contribute to 20% -25% of this growth. Rest is expected to come from new partnerships and avenues.

8. Recently won MH tender ( 9-12 months for going live) - Capex - INR 65-70 crores , Annual revenue expected at maturity - INR 70 crores

9. Margins - Expectations is of 30%. Dent from previous quarters mainly due to on boarding of new employees for PJ projects and with delays.

Summary and personal opinion - Krsnaa is operating in an area which has exposure to regulatory authorities which might change from time to time and hence play a role in overall business growth (BIG RISK). But on this aspect, every investor who entered Krsnaa always knew about this. The bet is on the aggressive growth which seems little bit over ambitious (imo) but apart from that as an when the tenders are won, it will add to the growth in overall business. Finally it will boil down to valuations and money being paid to invest in the business.

Discl. - Invested

10 Likes

Sector scan:

| Company | Q1FY23 Revenue Growth (YoY) | Q1FY23 Margins | Q1FY22 Margins | Q1FY23 Covid Revenues | Core Business Growth |

|---|---|---|---|---|---|

| Dr. Lal | -17% | 23-25% | 31% | 4% | 25% |

| Metropolis | -14% | 24% | 31% | 6.4% | 26% |

| Krsnaa | -15% | 26-28% | 31% | - | 10.5% |

| Thyrocare | -22.4% | 28% | 43% | 2% | 33% |

| Vijaya | -15% | 38% | 46% | 3% | 11.6% |

- 3/5 companies posted core business growth of 25%+, Vijaya and Krsnaa are at the bottom of the pack.

Other KPI:

-

Krsnaa and Vijaya offer pathology, but have consolidated data in exchange filings.

-

Krsnaa’s average revenue per path test in Q1 is 111 rupees, and 2080 rupees per radiology test.

-

Data above does not include teleradiology for Krsnaa. Teleradiology has a revenue per test of 85 rupees and 0.13Cr. patients.

8 Likes

“Krsnaa Diagnostics, one of the largest differentiated diagnostic service providers in India, started off the first day of trade on a positive note on August 16, 2021, as it listed at 1,025 a 7 percent premium on the bourses.”

1 year lock in for pre IPO investors has ended today. those who are waiting to buy, Please provide your inputs if the supply will increase going forward?

disc: started buying today

4 Likes

Positive:

- Launching the center of excellence in Genomics

- Implementing the CRM, will help in efficient, automated business process to increase productivity.

- Rajasthan bid is big one and can give 200-300 crore revenue per year. Waiting for result.

Negative:

- Recent IT raid

- Management is not walking the talk. 2X revenue and 3X profit growth seems far from reach. In order to achieve this current FY revenue growth needs to be 25% then 60% in next year.

- 70% payment done by government, even though the receivable days were lower in previous quarter. This is big risk that payment gets delayed.

- No bargain power in quoting project (even in re-tendering, recent example Assam where they quoted below the previous quoted price)

- Project getting delayed, can be seen in current to previous investor presentation.

Tracking.

Disc:Was invested, no position now.

6 Likes

This is going to benefit KRSNAA as their pricing is very competitive as compared to other players and hence would direct customers to them…

2 Likes

1 Like

Here is the press release. Looks like these are collection centres only operated by franchises. The interview and press release are contradictory.

P.S. BTW the interview was quite poor.

1 Like

https://twitter.com/CNBC_Awaaz/status/1578261159048011776

Summary

- Management expects 3-4% growth from their B2C foray

- Asset light franchise model

- Phase 1 - 200-250 collection centres in Maharashtra, Himachal Pradesh and Punjab

- Phase 2 - up-to 600 centres total, extending reach to West Bengal and Rajasthan

- Margins would be maintained

My take: B2G is still the mainstay. PPP wins and execution should drive the most growth. This is just icing on the top.

8 Likes

I think management statement and press release are not contradictory. The Company wants to venture into B2C business through franchise model to leverage its existing facilities. The franchise would also be in the form exisitng hospitals as well as new centres but on franchise model which would be asset light.

Disclosure : Invested.

5 Likes

- SigTuple’s AI100 in action at Krsnaa’s Mohali centre. Krishna Diagnostics ने पंजाब में पहली बार सिगटपल(SigTuple's)के AI100 को प्रसारित किया - YouTube.

- Machines are also present in Jallander and Amristar centres and 6 more are on the way.

- Krsnaa has placed an order for 45 AI100 machines with SigTuple

- CEO Pathology operations Manish Karekar is in the video. He comes to Krsnaa from Metropolis.

- The machines would allow Krsnaa to set up tele-pathology capability, increasing the utilisation of Pathologists. The slides are digitized and sent to the cloud where the pathologist can perform an AI-aided remote review

7 Likes

I think it has already expanded to Rajasthan have seen its one in my area ie jaipur rajasthan

Have a small chat with one of there staff and he said you will see many more in next few months.

As a small review personally fell much better service here with better and more test then my nearest lal path lab

8 Likes

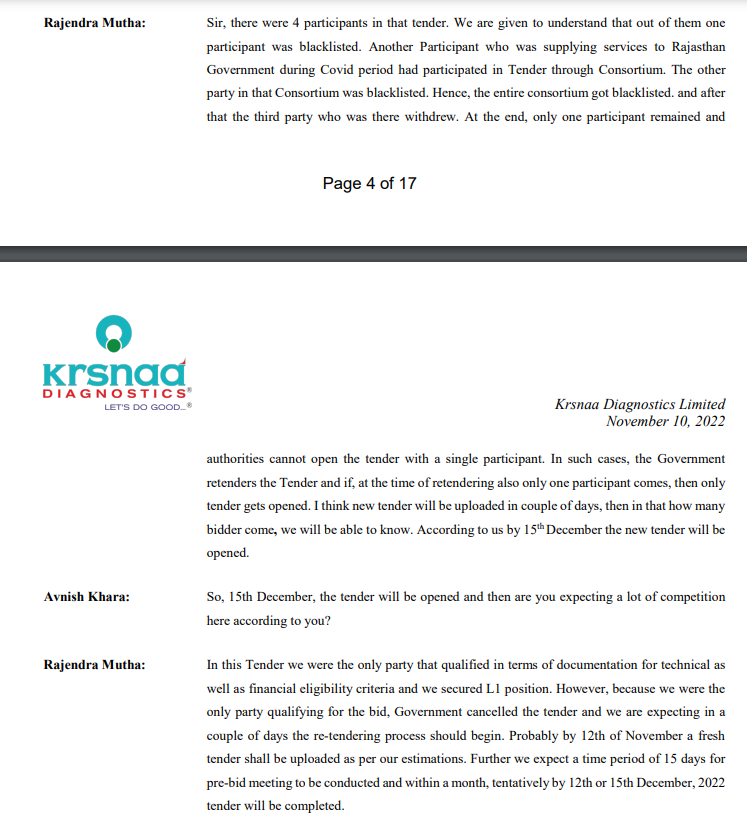

Unfortunately the Rajasthan Govt seems to have cancelled this tender on 27th Oct citing “No bidder having qualified technical bid requirements” as the reason.

Attaching the cancellation notification.

TCN.pdf (53.1 KB)

Another potential growth trigger for Krsnaa gone.

I am surprised that Krsnaa was found wanting in technical aspects? Is it possible that the RJ Govt. re-thought the entire initiative or looked at Krsnaa’s bid unfavourably due to the IT raids? We can only speculate.

Definitely a question to Management in this Q concall.

Disc : Invested with a small position

16 Likes

5 Likes

Latest Presentation:

But the mind boggling thing is that CFO has been shown as “-19cr” for H1FY23 . The corresponding figure last year was “717cr” . Is this a presentation misprint or some major thing that I’ve missed.

Would appreciate any answers. Thanks.

1 Like

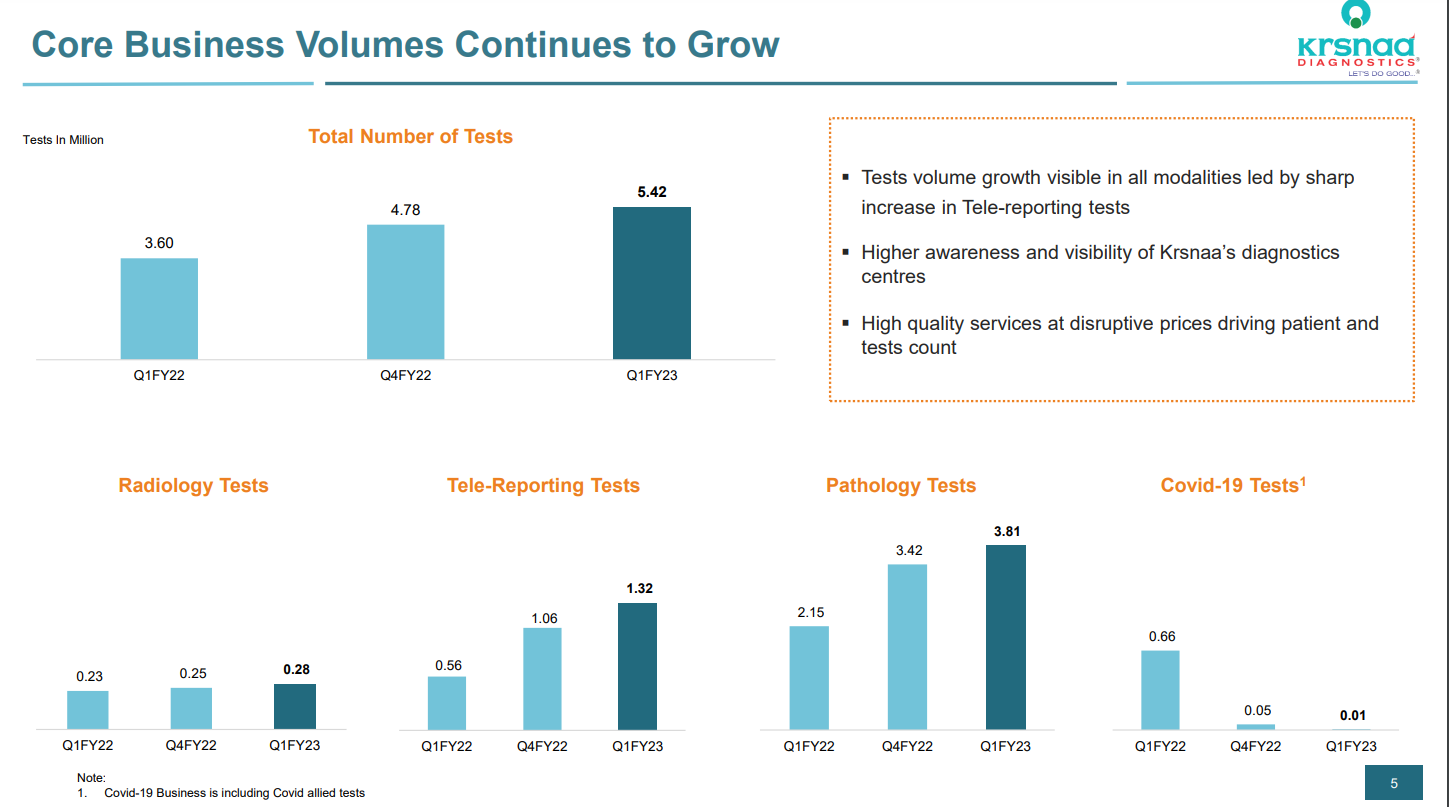

They have discontinued disclosing data regarding # of radiology/pathology/tele-radiology tests done each Quarter. So now observing test realization trends will no longer be possible. Below slide from Q1FY23 presentation is missing in the latest one

IMO, this indicates poor corporate governance. A new company like them shouldn’t be reducing transparency.

Investor presentation here.

15 Likes

Update on this : Management has clarified on the concall that the tender was cancelled because apart from Krsnaa the other participants did not qualify the technical/financial criteria for bidding. They expect the contract to be re-tendered in Nov and results to be declared in Dec. So it seems like the growth trigger still exists for Krsnaa and on the basis of the no-shows in the last tender, Krsnaa are in pole position to win the contract.

Concall snippet below

4 Likes

Also the management has quoted a additional revenue of 100 to 150 cr from punjab from these tenders when the sites mature combined with margin improvements as well .Also i believe they will win this tender by default ,looking at prospective Cagr at current valutions ,i belevive this trades at a Pe of 10 ish which i believe is quite low for business like this specially in growing rural healthcare markets in india ,i have seen many times our relatives have to travel to tier 1 cities for better healthcare.So there is huge scope of requirement and market for healthare in tier 2 cities.

Another interesting thing i noticed in the con-call were franchise stores which will generate similar margins with very low capital investment just like patanjali imagine stores of krsnaa being opened.

I think this is a great scalable business which is trading at super low valautions with low downside protection.

Disc :Invested at 460 levels will buy more seeing if mangament is able to walk the talk with margin and revenue increas in punjab.

3 Likes