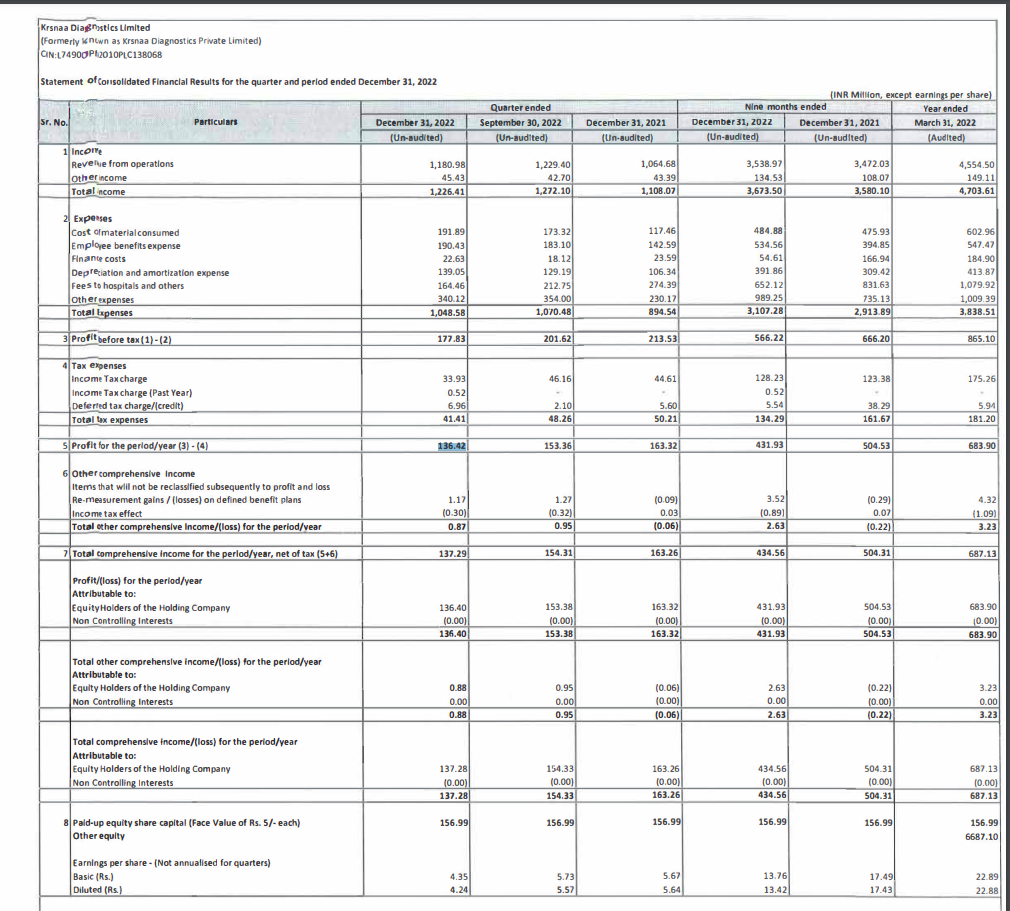

Have been meaning to share my investment thesis for Krsnaa on VP for quite sometime now. Finally, managed to write it down - Here it is:

The diagnostic industry has always been one with low barriers to entry. It is one of the biggest reasons why the market is still fragmented - with the unorganised players having 80%+ market share.

Before answering why Krsnaa, let us go to the first principles to understand the macros of the business - What does it take to set-up and run a lab successfully?

- Setting up a lab - Almost every manufacturer/distributor offers their devices at zero capex - where they bear the cost of the device and charge the lab owner only on the reagents - also known as a reagent rental model. The reagent pricing is a function of the volumes. So labs with a higher workload would have much lower cost per test and can be much more competitive in their pricing.

In-spite of a significant pricing (supply-side) advantage, then why have the large players not been able to corner most of the market share by now? To answer that, we would need to understand the demand cycle.

- (Price inelasticity of) Demand - 90%+ of the market is still doctor/trust driven. Often in these cases the patient/customer doesn’t shop around for pricing. They rely on the doctor’s recommendations to choose their lab.

It is this demand side behaviour, which has resulted in the limited market share gains for the efficient operators and has allowed the small/inefficient players to survive (and thrive) - based on their doctor relationships. This also explains why even the established laboratory networks have found it difficult to expand organically and have often resorted to acquiring the regionally dominant player, when they decided to expand in that region - Dr. Lal acquires Suburban for entry into West; Metropolis acquires HiTech for entry into South

While COVID exposed the shortcomings in our diagnostic infrastructure, which in-turn brought in a lot of rhetoric for investments in this space, the last year was when the euphoria died down. Looking beyond the hype and lull phases - following are the key changes expected in coming months:

-

Accelerated formalization of the industry - From incumbents (Dr. Lal, SRL, Metropolis, etc.) planning to enter into Tier 2/3 markets leveraging their brand, to pharma giants (Mankind, Lupin, etc.) setting up diagnostic labs and utilizing their on-ground sales (Medical Representatives) team, to emerging startups (Redcliffe, Orange Health, etc.) building on their convenience proposition - there seems to be an unprecedented rate of setting up new laboratory infrastructure.

Here, it is very difficult (at-least for me) to identify the potential winner(s).

-

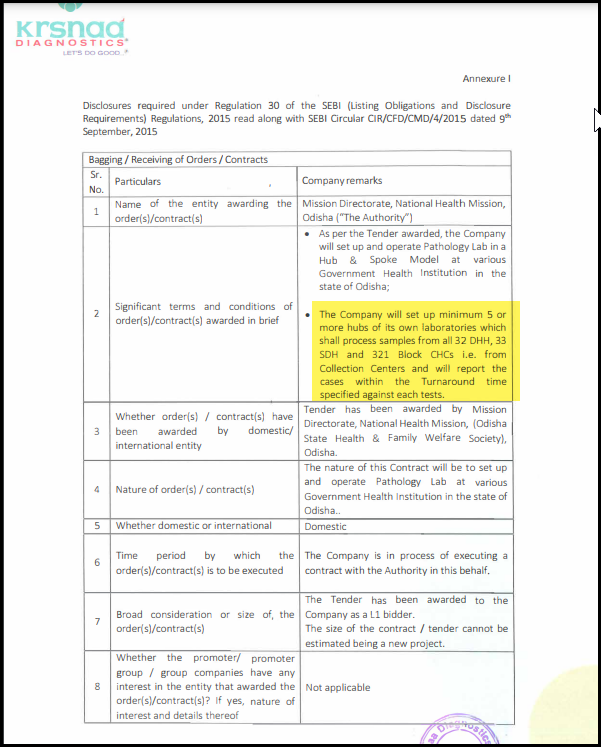

State governments being hands-off - The success of the various PPP (Public-Private Partnership) models in delivering quality healthcare at affordable prices has created a playbook for other states to outsource their laboratory infrastructure set-up and management to dominant private companies.

Counter-intuitively, the government business is one where the moat for dominant companies (read Krsnaa) is the strongest, based entirely on their economies of scale - given that demand is no longer dependent on doctor relationships and is driven through the humongous crowds visiting the government hospital set-up every day.

Advantages Krsnaa has:

- Minimal rental costs on laboratory infrastructure (similar to DMart)

- Lowest reagent pricing - driven by high volumes

- Lowest reporting costs - driven adoption of technology (tele-reporting)

- Negligible CAC - access to patients coming in government hospitals

Now, Krsnaa has plans to leverage their dominant position in the B2G space to disrupt the B2C space - however there is a massive execution risk in the same - IMO it has to be a franchisee led model targeted at forging doctor partnerships, focusing on illness and not on wellness!

Even assuming that if they fail on the B2C side, the B2G business itself has massive growth levers which could allow the firm to deliver 30%+ growth (could be lumpy though) over the next few years.

Disclosure: I had started a diagnostic startup (home collection) in 2014, and I currently work in a MedTech company, where Krsnaa is one of our customers.

Invested and biased. No transaction in the last 30 days