It’s naive to expect B2G business transactions “above board”. Also since governments are involved, politics is never far away. Hence market values such stocks accordingly.

Coming to the specific case, it is too early to know whether how material this event would be for company. But the risk is there. As long as one bakes in this risk in the calculations, all stocks are attractive at some price.

Depreciation also increased.

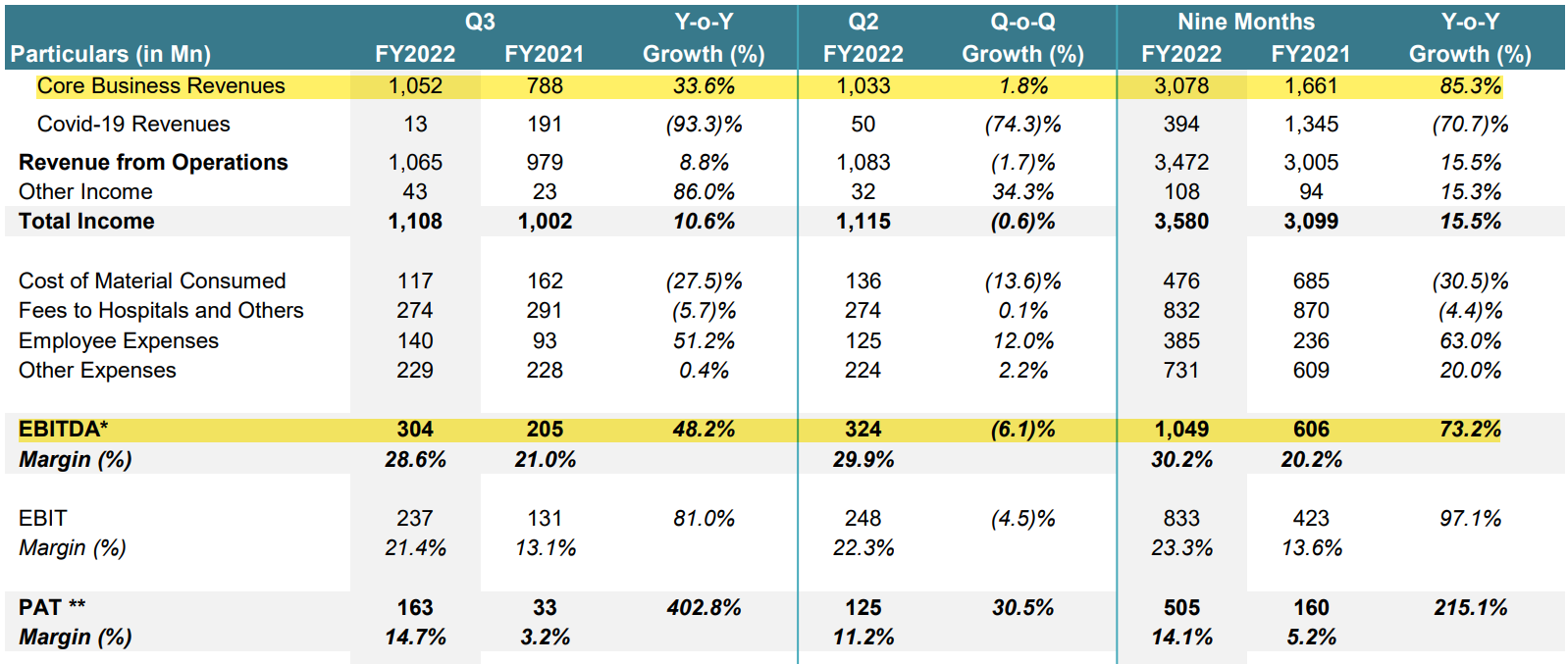

Punjab centers are causing loss on PBT basis. Because standalone PBT is qoq same (220 cr) but Consolidated basis PBT has reduced from 198 cr to 186 cr. Once they break even Consolidated level PBT increase should happen. Hope soon they make enough revenue so that operating leverage happens.

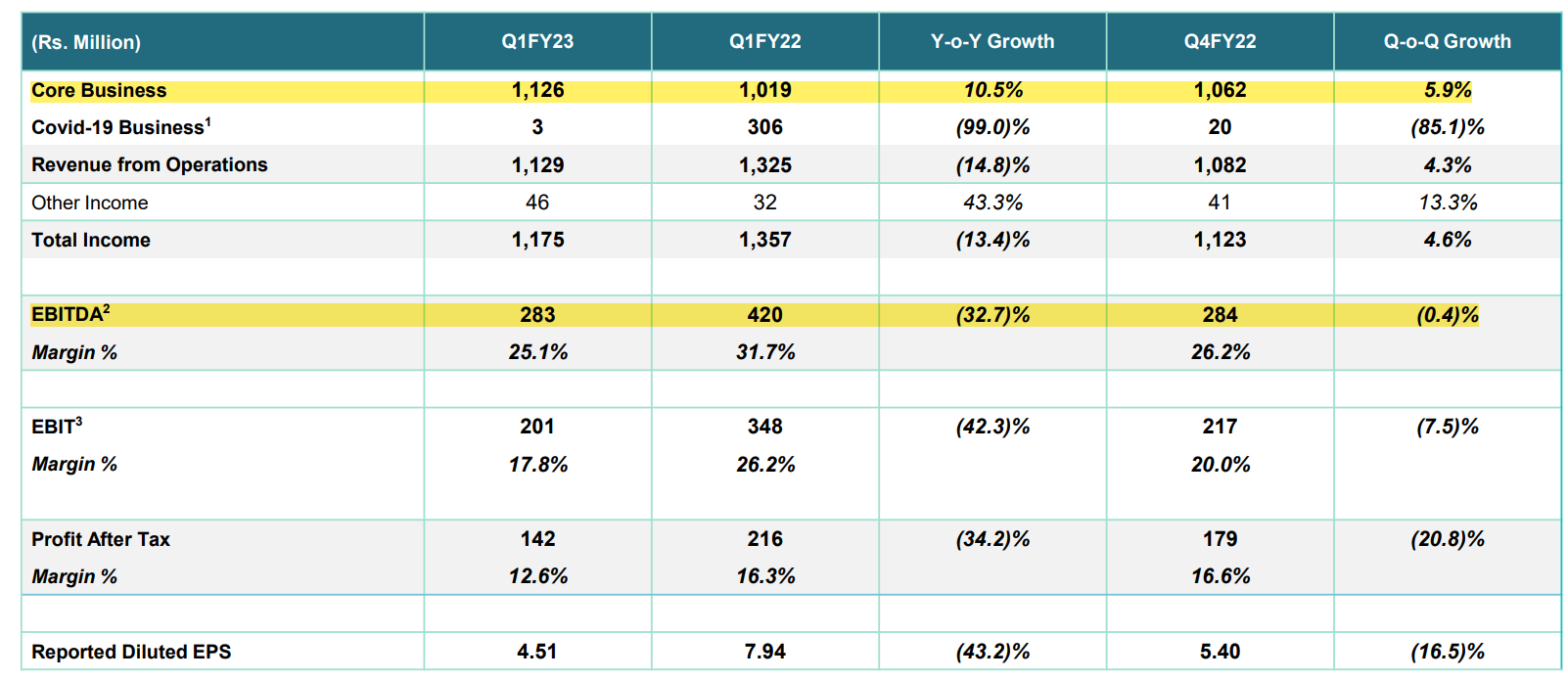

If some one notes the QOQ core revenue growth slowly it’s accelerating. In Q2FY22 to Q3FY22 it was 1.8%, from Q3FY22 to Q4FY22 it was 1.0% and now Q4FY22 to Q1FY23 it’s 5.9%. So slowly it’s accelerating. Maybe PBT level it will be subdued but EBITDA level soon it should make difference. Here other income component also varies quarter to quarter so if we see the core business revenue it’s accelerating IMO. @Chins see this.

10.5% revenue growth in core business revenue is low in my opinion. Let’s see what they mention is tomorrow’s investor meet. While disclosures are ok it does look like management is overcommitting.

IMO, revs can easily grow at 25%. But margins will likely remain subdued as company is aiming for rapid growth and the ROCEs and utilization rates will take time to mature amd fixed costs which don’t show immediate results stay elevated on account of constant expansion and new tenders.

Need to wait for expansion to slow down for margins to hit 30-35% and ROCE to grow to 25-30%.

Quarter was definitely muted and below average margins.

For all these costs that the company is incurring, the centres that are newly opened needs to slowly garner enough footfall before the rewards can be reaped. Operating leverage is atleast 2 years out imo, mgmt doesnt look like they will slow down on setting up new centres as long as they see the demand. Long term great but short term pain(how much pain and for how long is to bee seen).

Secondary thoughts, compared to normal diag companies engaging in b2c, I feel like even thought capacities present are more than enough, utilization rates may not ramp up as expected, aren’t they dependent on patients from public hospitals? So footfall might be limited as in rural areas, there maybe only a certain number of people in rural locations where technically Krsnaa’s capacities may be there to do more tests per day but it is practically impossible to increase them as it is dependent on population nearby who use the govt hospital. Whereas on b2c side, more people enter based on name(like lal path labs) and footfall in individual diag centrest increase that way. Please correct me if I’m wrong.

The number of bids and the scale of capacities show enough opportunities for company to scale up but revenues are still not hitting 150 crores atleast. Lets see how mgmt responds.

Disc - invested. largest position. Margins and roce and slower growth definitely concerning.

I live in a town which is similar to places where krsnaa sets up their diagnostic centers. my town has a population of 1 lakh. I was checking the population of places where krsnaa has centers and the population is more or less similar. Hence I came to the conclusion. Once I admitted my father to the hospital but to do xray i had to take him outside. usg was done in the hospital but there was a huge queue for it. The hospital is of a sub divisional level hospital to where patients from nearby villages (actual villeges) come. calling my town as rural area will be very wrong. it has a college, 6 high schools. There are no shortage of patients in the hospital. Very often for critical cases or serious cases patients are referred to district level hospital. so I don’t think krsnaa has centers in rural areas or villeges.

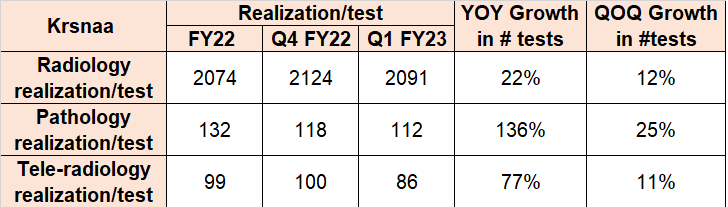

While #tests have been growing rapidly for Krsnaa, the realizations in Pathology and tele-radiology have come down significantly, by 15% and 14% in Q1FY23 compared to FY22 full year numbers. Realizations in radiology have remained more or less flat.

I can understand the reason for lower realizations in pathology - they may be trying to grab market share faster. What’s the reason for lower tele-radiology realization?

Test volumes going up by 51% BUT revenues going up 10% is a concerning issue. We need to clear out the exact reason for such a huge drop in realisations.

yet to listen to it. @sahil_vi tweeted their growth guidance lowered from earlier 50% to 20% now.

IMO this is quite reasonable because if u see core revenue growth qoq is 5.9% so should be able to do a 15-20% topline growth. But with negative operating leverage PBT/PAT will degrow.

When investor started it was a co creating value in B2G segment. Since then 2 key triggers have played out:

IT raid across multiple locations. From my channel checks, an IT raid is a big deal & impossible to orchestrate without some prima facie evidence that IT dept has of some sort of tax evasion.

Thesis was for 40% CAGR growth. For 40% CAGR growth the B2G risk was worth owning IMO. If growth guidance is reduced to 20-25%, why would an investor still want to own krsnaa? There are 100 other cos who have a 20-25% growth guidance without the added negatives of downward test realisation, downward growth guidance, Corporate governance risks playing out live in front of us. Writing is on the wall & there for everyone to read. Even if co grows 20% but derates 30%, investor makes negative returns.

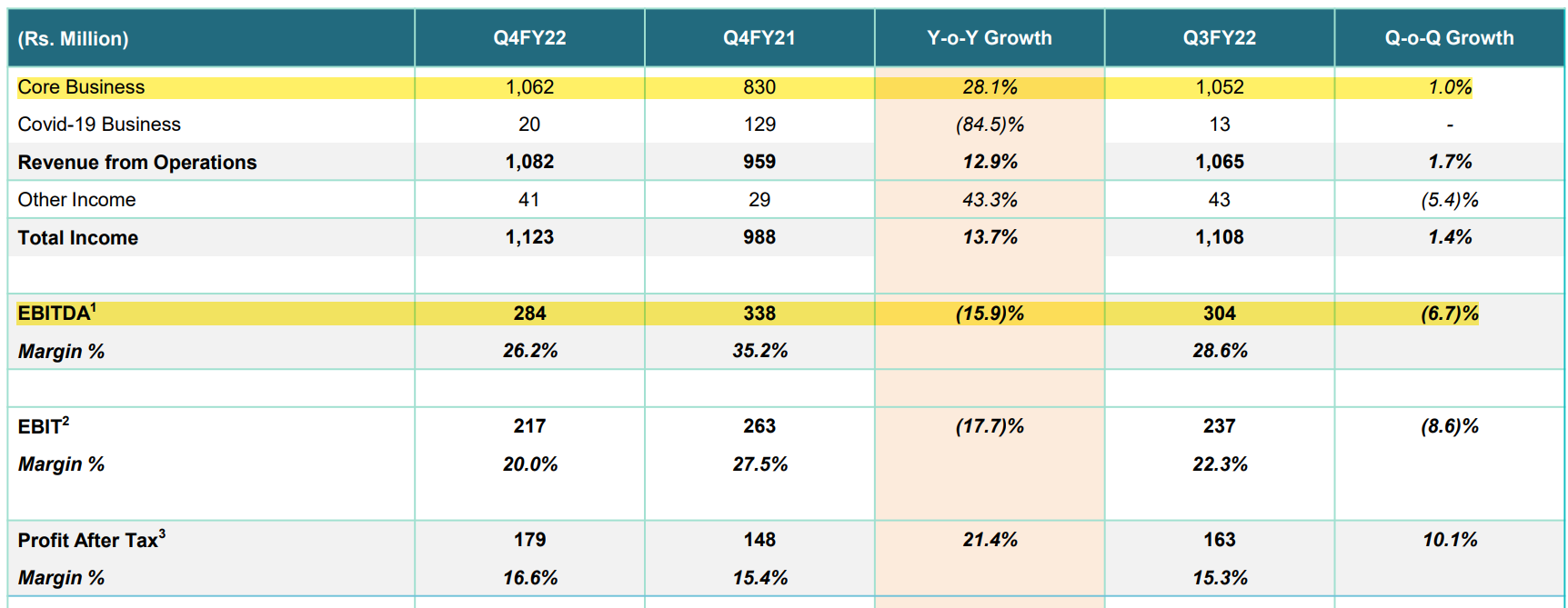

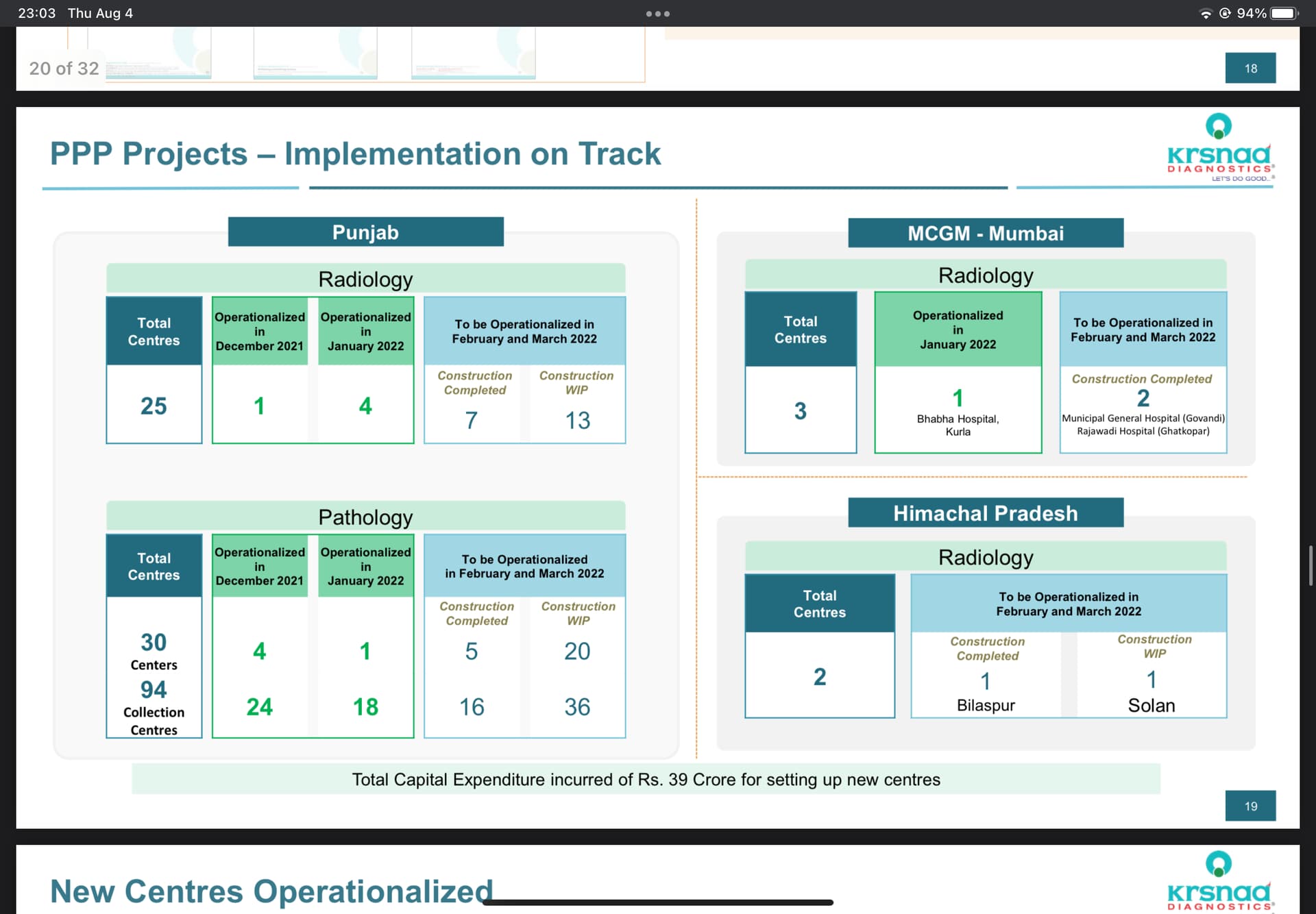

Punjab ramp up has been quite lacklustre.

Disclaimer: was invested, sold out, tracking closely & still in the krsnaa cheer leading squad (of course i want co to do well).

Don’t know about consequences of IT raid but bottomline will degrow given the negative operating leverage. Stock won’t move if bottomline don’t grow. But once positive operating leverage plays out bottomline will grow much faster. But don’t know when that will happen. Sold completely on news of IT Raid. The earnings slowdown was a negative surprise!

I think “Self-analysis and own thesis” serve one the best and true picture. There are many investors who invested in businesses these were not cyclical, concentrated geography, demat tailwinds etc. and created a lot of Twitter gung ho before investing and then moved out at slightest headwinds. Depend on your analysis because you don’t know what kind of analysis others did and what kind of investment duration they had planned for. There is a quote for every kind of market action.

Disc: Invested, don’t love my stocks but also don’t enter before considering all risks, have a medium term duration view, understand cyclicality and geographic concentration headwinds.

It was quite apparent from previous quarter results. thought of some 20-25% growth to happen…but mgmt kept on lowering guidance since q3fy22. Hence the doubt came…and it was a right one

Is the Q1 concall audio uploaded somewhere? The company hasn’t uploaded it to the Exchanges yet and I couldn’t find it on Youtube or anywhere else online.

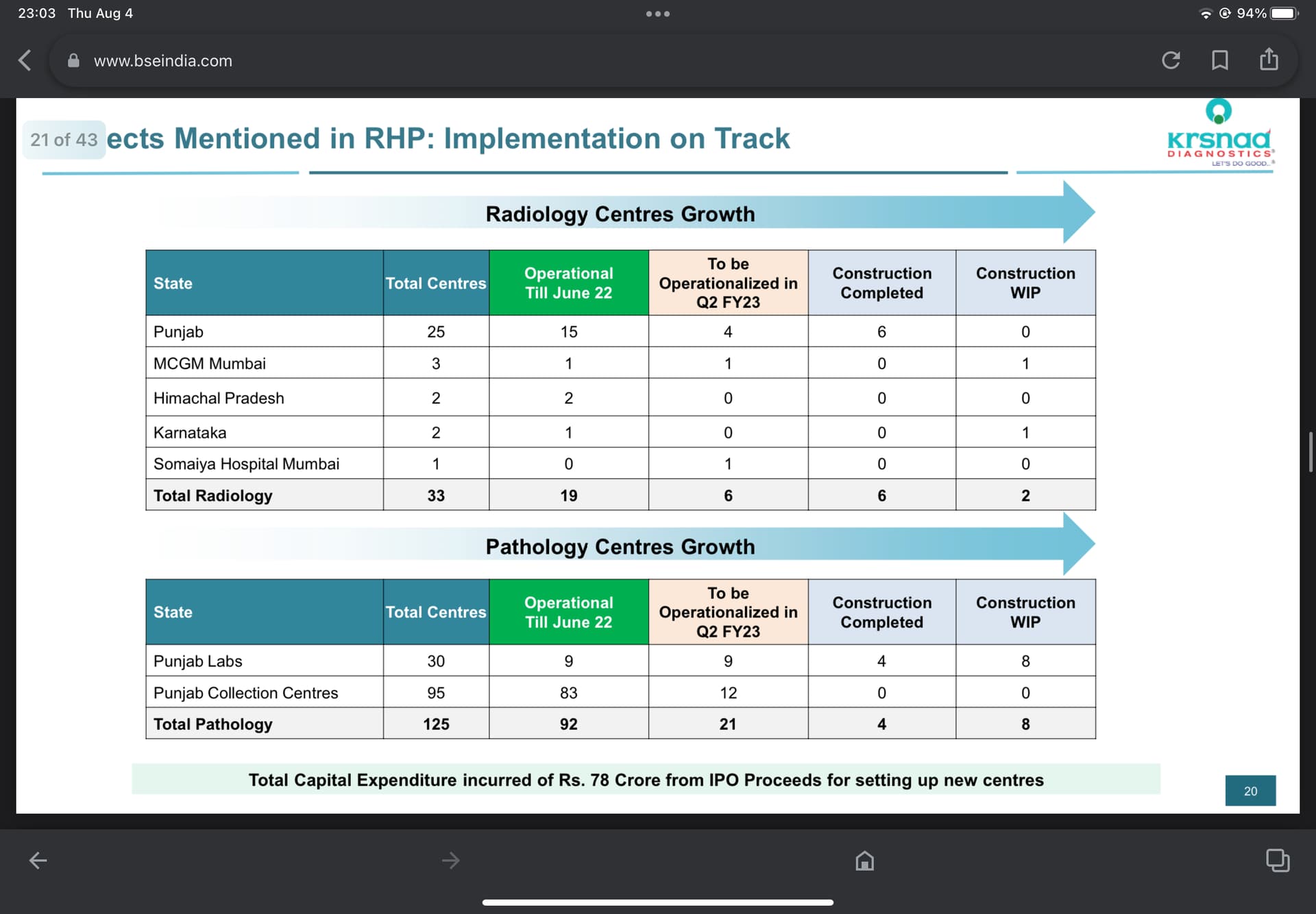

Guidance: 20-25% topline growth expected for the 2023FYE. Punjab PPP project saw some delays due to changes in government and approvals but should be functional by the end of September.

Centers take 6-9 months to ramp up and functionalize fully with higher footfalls.

Punjab (100) and the new Maharashtra+Delhi+Tripura+Rajasthan-R&D (100Cr, Maharastra project is expected to commercialize in the next 9-12 months, and others in the next couple of months) contract has a potential of 200+CR. of revenue.

We are also bidding for a massive, state-wise Rajasthan project with a 200cr+ potential.

We had high volume growth in test count, but the realization was less as we renewed the Assam contract with competitive pricing due to the ease of doing business, and all facilities are already in place.

We have 70% contracts where the pay model is through govt and 30% (like Punjab) where we directly collect cash from patients.

2024FY guidance of 2x revenue and 3x profits is intact but will be reviewed in the next quarter.

IT raid is under investigation, and they falsified the media reports. The financials shown in those reports are also not legit.

Disc. Invested. (Apologies if I am missing anything, it is my first post since I joined this community!)