Yes. I was looking at last 3 years, which is from year ended 2021 (rent 3.564 Cr) till year ended 2023 (3.682 Cr).

There is definitely a question on why the rental increased from prior period. While we can assume that management integrity is an issue here, we can also assume that the building is owned by Sunita Mutha and Krsnaa gradually expanded to take on additional floors based on previous rental agreements.

It is best to ask this question during earnings call as I don’t know how else to ascertain a fair rent being paid for corporate office (unless someone from Pune can dig out the going rates). When I look at the corporate office location, it doesn’t look like a premium location.

The points raised by @Khanemc2 bothers me more than rents. If the business model is not sustainable, then that is a larger risk to capital.

Disc: Invested. Will need to figure our how to dig more

Certain Positive Things like test volumes :

FY 23 vs Fy22

MRI : 9.17 v/s 7.27 Lakhs

CT : 3.82 v/s 2.31 Lakhs

Tele Reporting : 55 vs 34 Lakhs

50% growth in Tele reporting and CT and more than 20% in MRI.

Diversified in North India. In FY22 revenue share from West was 61% now its in 40’s. North India increased from 10% to 28%. Number of districts covered increased from 70 to 120.

India’s 1st NABH Accredited Teleradiology HUB.

ROCE will be under pressure for FY24 too as share of new launched gross block has increased by 11%. Key thing i.e Receivables is under control.

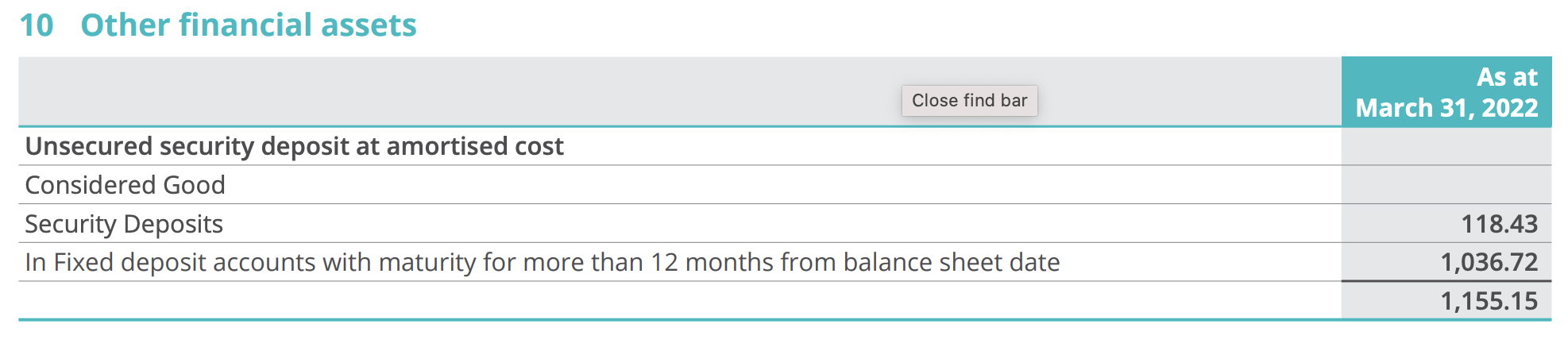

Can someone please throw some light on, why there is no correlation between the capex done in past 2 years visible in Assets (Property, plant and equipment )

Capex: 131cr (FY22), 135cr(FY23)

Total Capex: 266cr

Property, plant and equipment: 307cr(FY21), 383cr (FY22), 468cr(FY23)

Other financial assets: 15cr, (FY21), 115cr (FY22), 171cr(FY23)

Change in Capex (Fy23-FY21) : 161cr

change in Other financial assets: 156cr

What does Other financial assets include? Why there is jump from 15cr to 171cr?

Hello @Areif46. May I know where you got the CapEx numbers from?

If we compute capex using indirect method, then the amount should tally with PP&E difference. However, if it is done directly, then it is expensed wrt the money spent on assets less money gained by sale of assets. The PP&E might not reflect exact value due to fair value recognition and deprecation.

From what I can understand, majority of capex is being used to setup new centers. There can be costs that are not accretive to balance sheet when setting up these centers.

WRT other financial assets, here is the list from AR FY22

Capex: 131cr (FY22), 135cr(FY23)

Total Capex: 266cr

Change in Capex (Fy23-FY21) : 161cr

Property, plant and equipment: 307cr(FY21), 383cr (FY22), 468cr(FY23)

Depreciation: 41cr(FY22), 54cr(FY23)

Total Depreciation: 95cr

Now things ~add up : 161+95 = 256cr.

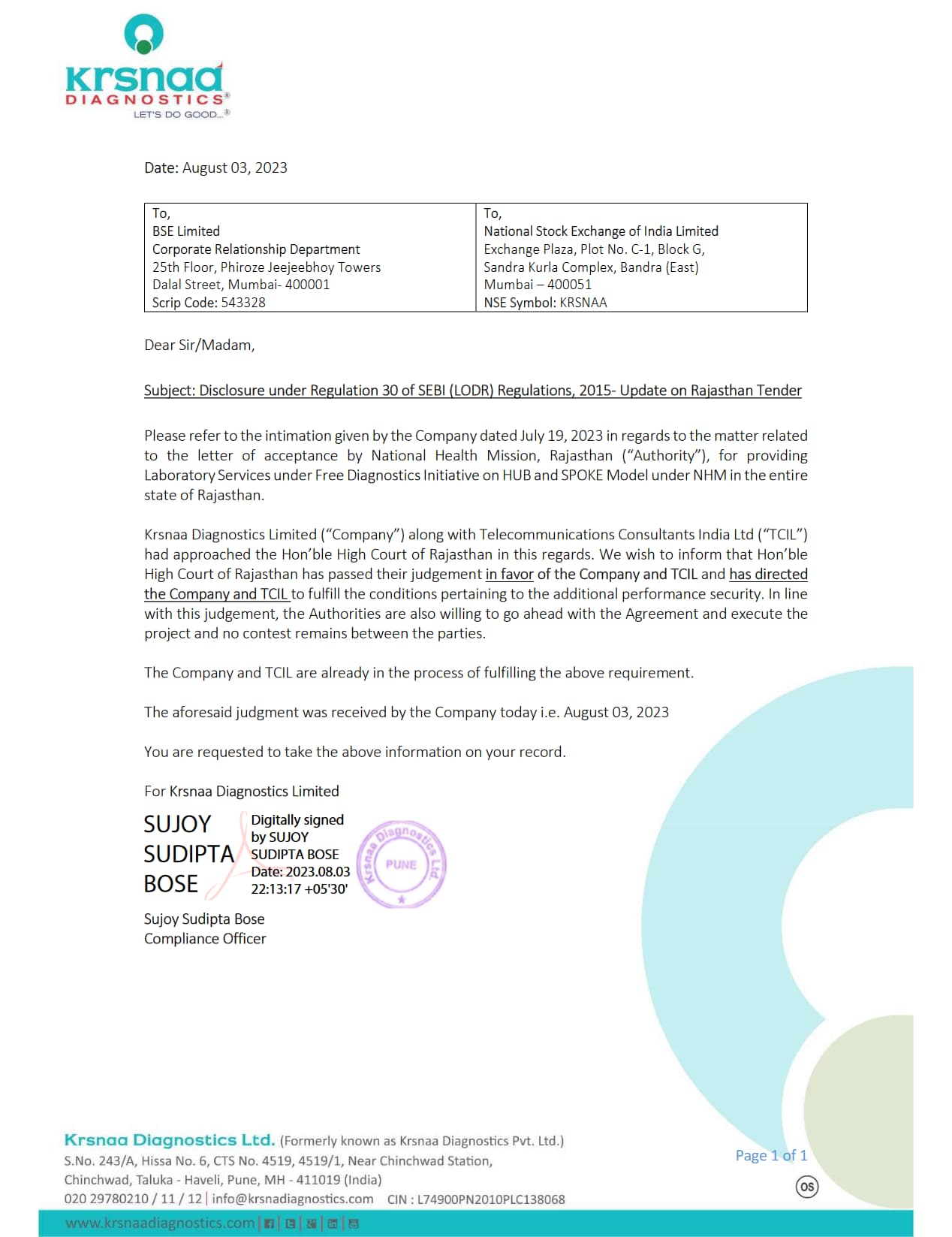

"Letter of award issued by National Health Mission, Rajasthan has been cancelled.

There were requirements of provision of submitting additional performance security. There are disagreements over providing of this additional performance security due to certain technicalities.

We assure you that our legal counsels are actively pursuing this matter with utmost dedication and diligence."

Krsnaa Diagnostic raced up on order receipt and now order cancellation -

Taking Legal course may upset its other Quasi Govt customers . No one likes to deal with company that files cases against you …

Cases like this takes long to time to resolve even after favourable judgement . There are many such examples when company has won thousand go crores as compensation from high court , but they case then get stuck at SC for 6 - 7 years … … in meantime company may turn near bankrupt

If you are buying any company who has GOVT as primary customer pay less than 5 times OCF ( last 5 years Avg OCF is better metric )

The same point came into my mind for the Olectra Deal.

Too big of a deal and over 10-12 years if im not mistaken.

Govts can change, ideologies can change seeing how ESG is now being given up on.

Adding to above, the desire for people to own cars - for convenience and status symbol. They rather go for EVs over taking buses. If many investment thesis are based on India’s consumption growth then why can’t we expect people to buy more cars, even in tier 2 and 3 cities ? and across social hierarchies ?

Dealing w govts is always a risk. They are not answerable to you. Suing them is well, a waste itself. If you don’t have the connect like TATAs do ? its a big risk.

I didnt understand. Krsnaa contested the additional performance guarantee right? But not it needs to make that payment. so how is the judgement in its favor.

Krsnaa would be fulfilling the conditions pertaining to additional performance security and the NHM Authority has no choice but to go ahead with the tender and let Krsnaa run the project. So basically the deal is back to the ‘win’ state.

As part of the tender requirements, there were requirements of provision of submitting additional performance security. There are disagreements over providing of this additional performance security due to certain technicalities. Whilst we have made various representations to the authorities on the same as well as communicated our willingness and commitment to execute the agreement. However, to our disappointment, the authorities decided to cancel the letter of acceptance

Though Krsnaa was initially contesting the performance guarantee demanded by the authorities, they had finally agreed to pay it. Despite this, the tender was canceled. Since TCIL the bid partner is a mini Ratna and quasi govt entity, it got the Additional Solicitor General of India to mediate.

Thanks a lot! It means that Krsnaa wanted to test till where it can defend and finding no way than other submitting performance guarantee for 3 years + 60 days so accepting it…by any chance, anybody know what is disputed amount?

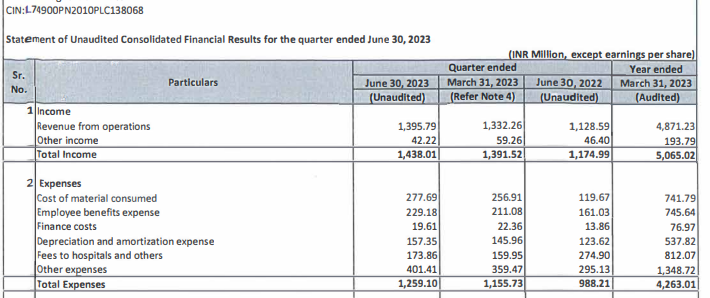

Q1FY24 results. Sales have increased YoY 24%, which shows tests volumes have increased, ramp up of Punjab, himachal, maharastar centers etc. But cost of material consumed has doubled. Employee expenses and other expenses, depreciation increase is obvious considering new centers are setup. Cost of setting up new centers, radiology machines cost etc are capitalized. But I think gross margins are getting eroded. Pricing pressure ? Concall will be interesting.

Gross margins 80% versus 90% YoY. It can be pathology v/s radiology mix.

Press release says :-

In terms of financials, our Normalized EBITDA reached Rs. 345 million, accompanied by margin of 25%.

Normalized Net Profit amounted to Rs. 169 million, with margin at 12%. However, the regular EBITDA

margin was 23% and Net Profit margin was 11%. It is worth noting that our profitability margins

experienced an impact in comparison to the previous quarter. The impact on EBITDA is due to the

ongoing expansion activities due to the various projects underway whose revenue contribution is not

commensurate to the expenses being incurred. We anticipate a positive trajectory in margins as these

centres mature over the upcoming quarters.