@Chins, thanks a lot for putting all important information together.

My only comment will be on “loss of any other tenders” as you are aware it will be lumpy in nature so it will be more that 2.5 crs and can have significant in case if there is no new win or company faces challenge in implementing these new projects e.g. Punjab

Hopefully it’s large scale in future, will make this loss of any project revenue insignificant but if you see FY22 loss of revenue from Rajasthan project is ~15% of total revenue (though they have won it back but there will be case project will go to other company). I think company has edge while it rebid for project but we need to consider this as risk.

I don’t think tenders expiring are lumpy: it’s a matter of fact on whether they’ve expired or are extended. This is something I was adamant on when I last met management. They say there are no other large tenders expiring (akin to Rajasthan in FY23), and the 2.5 Cr. is on account of one small CT contract in Nashik that can expire by FY25.

To the best of my knowledge, this is the only tender expiring. If you have data to believe otherwise, please do share so we can better the model.

No, I do not have any additional data other than Rajasthan experience. I have suggested IR department to include data for the project that are going to expire in next 2-3 years as they are including projects which will go live in next year or so - this should give to investor additional info and avoid knee-jerk reaction.

Just to point out, Mr. Nikhil Deshpande (company secretary) has resigned and Ms. Pallavi Bhatevara, Managing Director of the Company has been designated as Compliance Officer of the Company for temporary though I think this responsibilities should have been given to some one else as MD will have her plate full with BMC, Odisha and Rajasthan project or hopefully they will find someone for this position soon.

and also when they appointed Mr Ravinder Sethi they filed exchange filling and I think he was on concall as well but I could not see any filing when he left company (it is not mandatory by law) but I was expecting them to disclose.

In no way, I am saying these are CG issue but just to let forum know about recent development on this front as well.

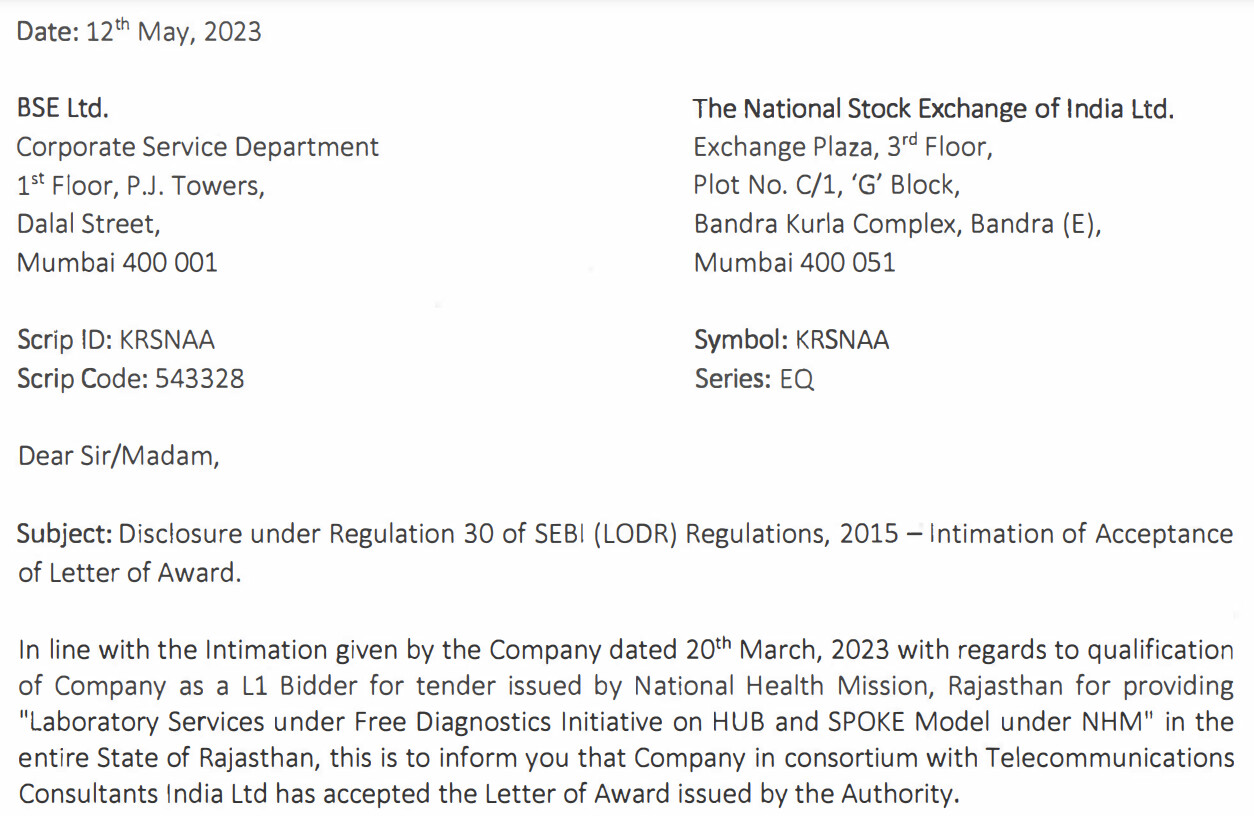

This isn’t a new win. Its the acceptance of LoA by Krsnaa for the tender in which they emerged as L1 on 20th March. Its the same RJ tender which they announced on 20th March.

After the L1 bid is announced for any tender, the government enters into a discussion with the winning bidder. They discuss each site, viability, space, etc. and then file the LoA after ironing things out.

The significance of the LoA for investors is that they now have to operationalise the Rajasthan tender within 120 days.

This means we should start seeing revenue come in from the end of Q2, and ramp up through Q3 and Q4.

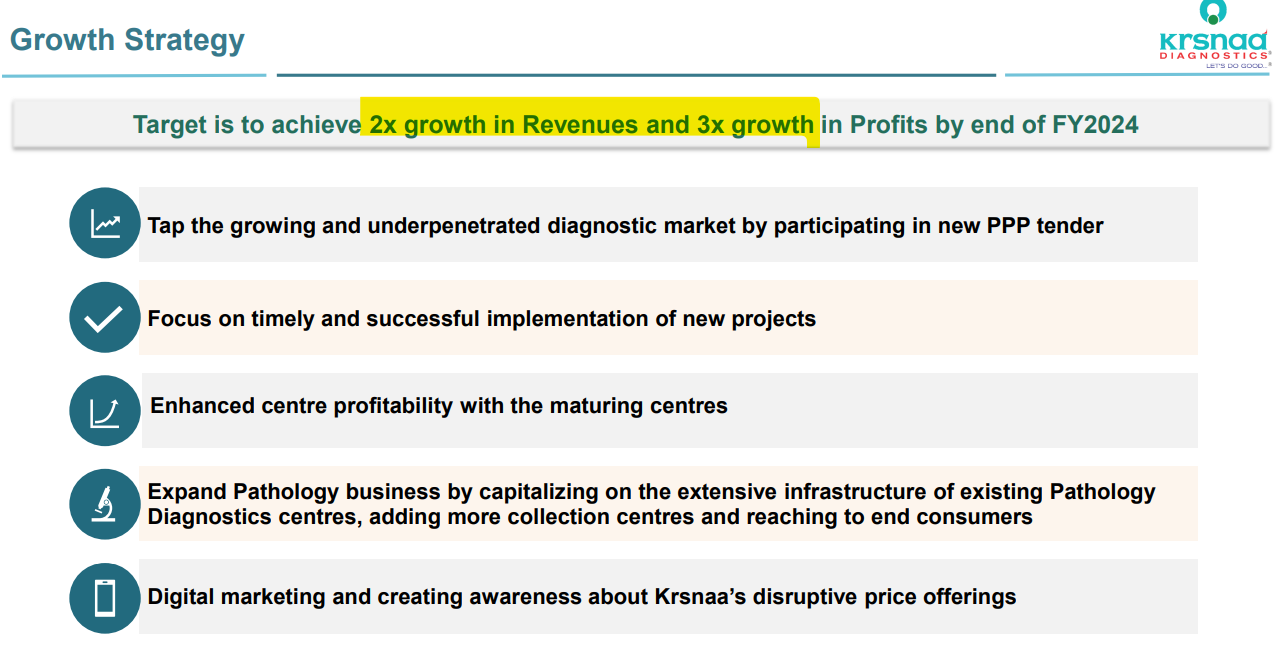

So there are a number of significant triggers that should start playing out in Q3/Q4 before ramping up through FY25: 70-100 Cr. of potential from Maharashtra CT, 180-220 Cr. of potential from Rajasthan pathology, 60-100 Cr. from Odisha pathology, and 40-50 Cr. from Assam pathology.

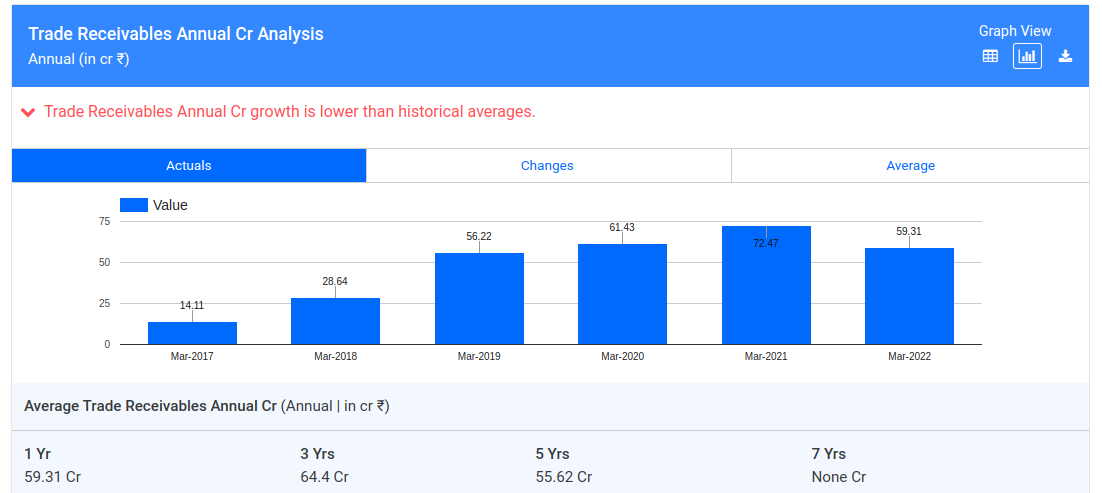

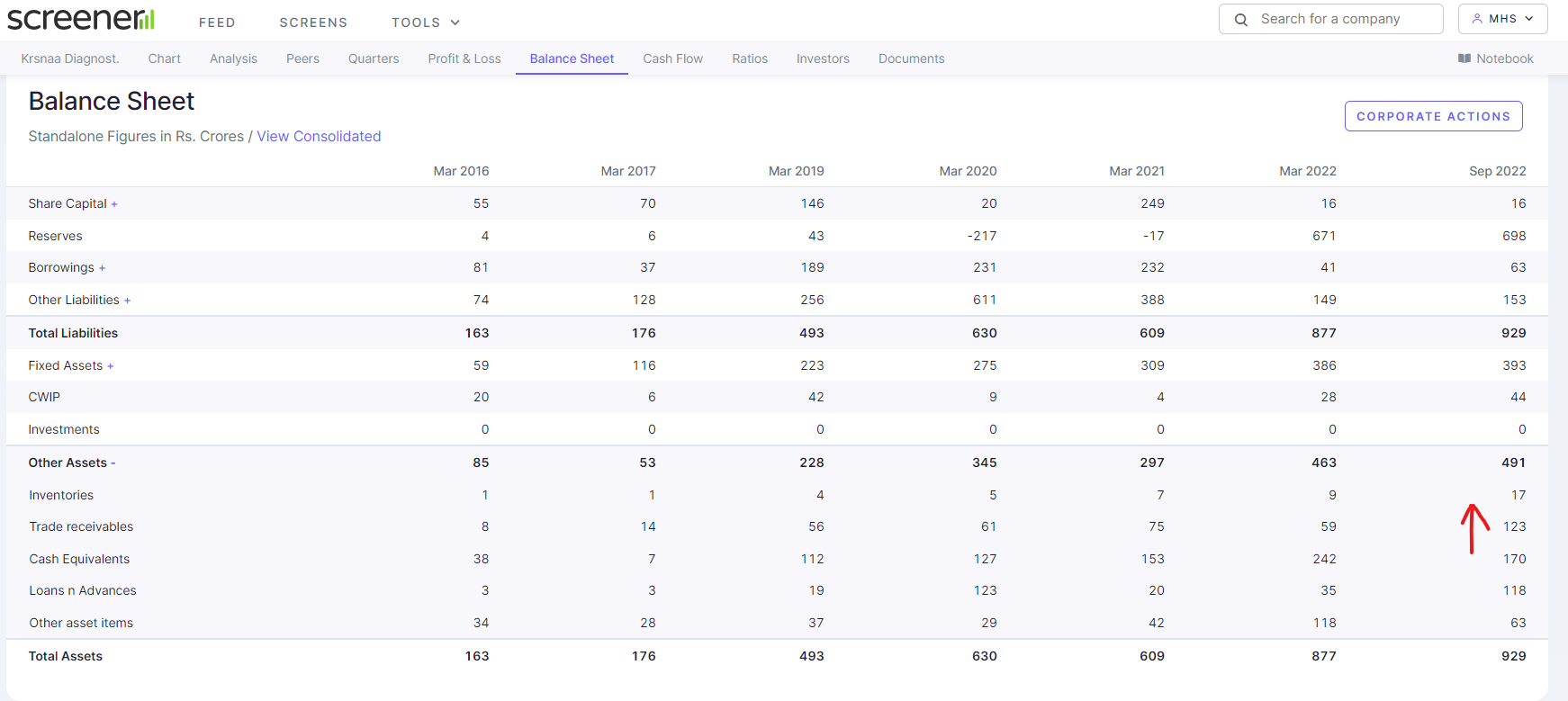

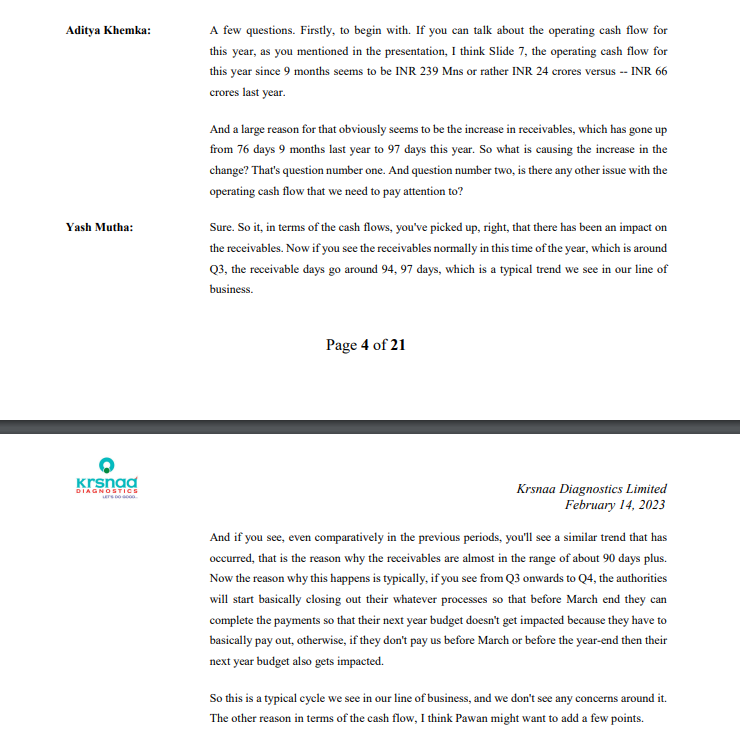

As I recall Old Rajasthan tender ended in some time FY23 which impacted around 70cr for the company. As I recall this new tender is bigger than old on – should Krsnaa operationalize this faster?

Winning Orders is not key , even generating so called profits is not important esp when one is dealing with Govt as customers .

Realising Cash in hand is key and very important . Classic is to look at Antony Waste management and problems with receivables they are having … Same problems are with State Discoms , Road contractors and many others

All this has surfaced in last 2 quarters in case of Antony Waste … Municipal corporations and State Govt just don’t pay in time and additionally refuse to give price hikes in line with Inflation .

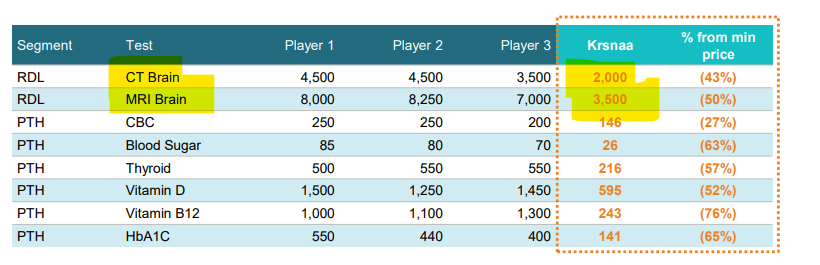

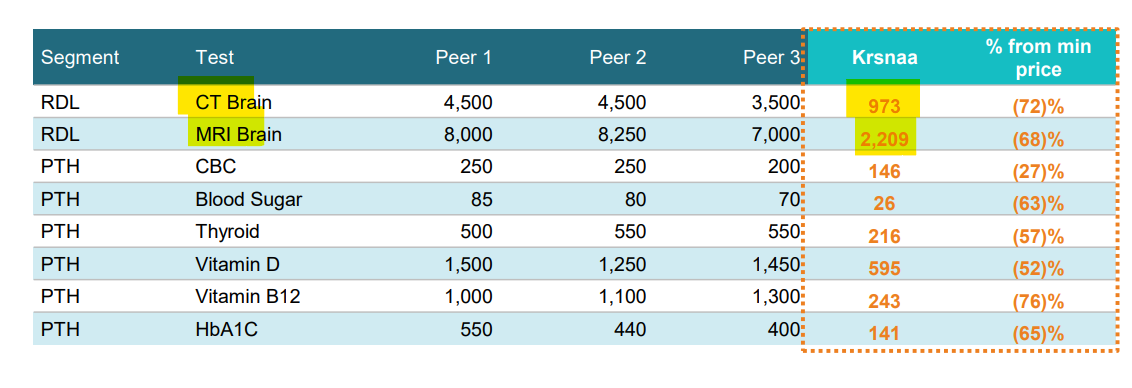

If Krsnaa can make money on subsidised rates which are 1/10 of market rates because of volumes , then that is great , otherwise be aware of skeletons will come out one day …

Comparing with Antony Waste mgmt’s receivables, it is evident that Krsnaa is able to crack the problem of govt payments. Besides, they are not only limited to govt centers and are using these to expand into retail biz (free marketing).

Krsnaa does seem to be “too good to be true” and a significant part of my brain is seeking for the skeletons in the closet. But, I haven’t figured out much issues yet (request any member to share anything fishy on Krsnaa’s balance sheet).

So far, Krsnaa seem to have a moat on operating at scale and also to manage govt contracts. If any of these thesis fails, then we are in trouble.

As for Antony, I think if they scale out and if the issue of receivables are managed as a project on its own, this might not be much of an issue. But, they will need to manage working capital till then.

Disc: Invested in Krsnaa at 5% pf. Tracking Antony

Note that this has been approved on July 2020, which is before Krsnaa got listed.

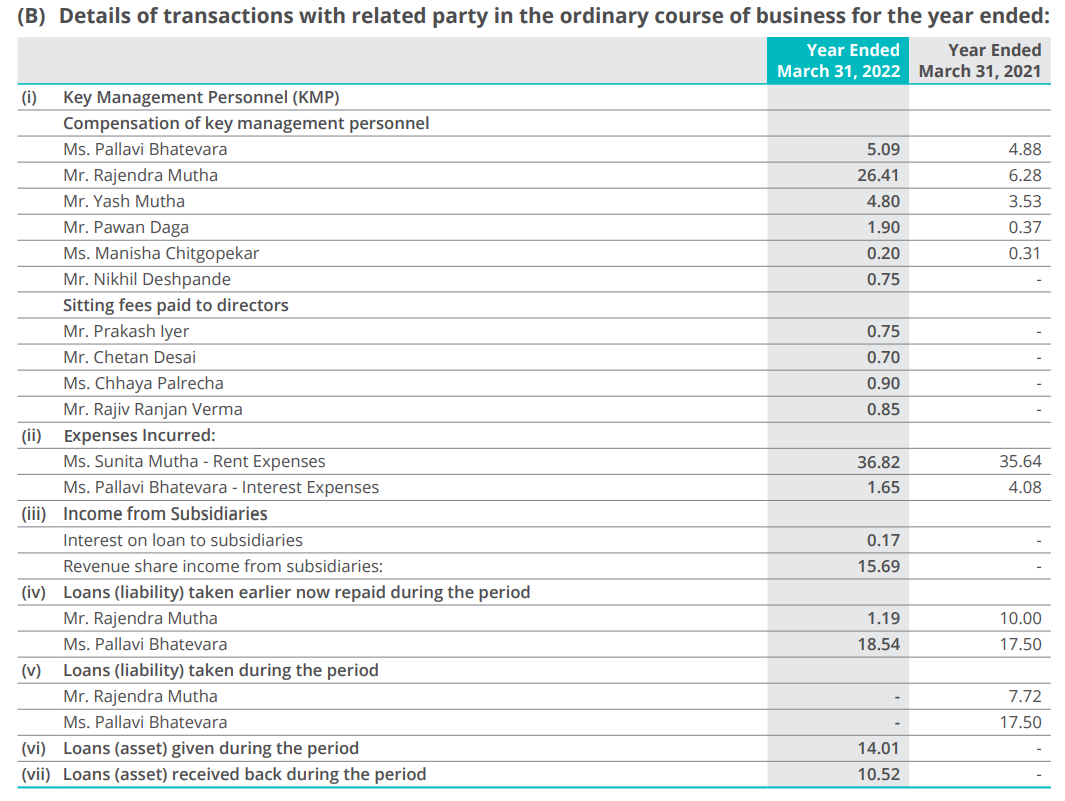

If I am correct, this is the corporate office for which the rent is paid. Krsnaa Diagnostics, Mahavir Chowk, Chinchwad, Pimpri-Chinchwad, Maharashtra 411019, India

The rental price is similar to last 2 years as you can see from AR FY22 disclosure. Good thing is that the rental payment didn’t move much in last 3 years. I am not sure of market rate for office buildings in that area. Still, this related party transaction does seem unusual and is something to ask the management in earnings call if anyone is planning to attend. As long as it is within agreeable market rate, I don’t mind this as it exists before listing of Krsnaa.

Thats not completely true…

it has risen From. 2.1Cr In fy2018-19 to 3.6 Cr in fy 2021-22… A rise of about 18% per annum ?

I am sure none of the real estate rates rise this fast !

As far as i understand from their latest RPT disclosure, they have paid 18.41 Million for 6 months, that is 36.82 Million for a whole year…

so my understanding is, the rent for FY 2022-23 is same as that in FY 2021-22 at 36.82 Million (3.6 Cr)