once they start showing the revenue growth in possible it cannot be available at 10:15 PE, rerating is possible for sure maybe it may jump up to 30 40 PG and then we have revenue growth of 25%…will add once sell off absorbed

Hello,

I read this thread with interest.

As per my understanding, broadly diagnostic services are for either indoor patients or outdoor patients.

Indoor patients are usually more sick and hence, have limited choice. Hence, usually they shall utilise in-house hospital diagnostic services only, which provides hospital pricing power.

Outdoor patients will go either on doctor recommendation because of quality or cost/ convenience.

So, KRSNAA is looking at tapping outdoor patients except for government hospitals where it has tie ups.

The problem with central reporting is it’s difficult to create a repo with local physicians and hence, difficult to get physician recommendation and hence, premium charging.

So, essentially, it is going to compete on basis of cost advantage and perhaps ease/ access.

Isn’t is like a D-mart model where one needs to be most cost effective and has ability to cross sell higher margin tests to be able to be a multi beggar.

And as far as I understand, it is still launching basic radiology and pathology services and trying to compete on price.

Thanks

3 Likes

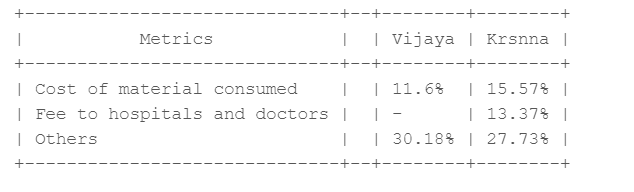

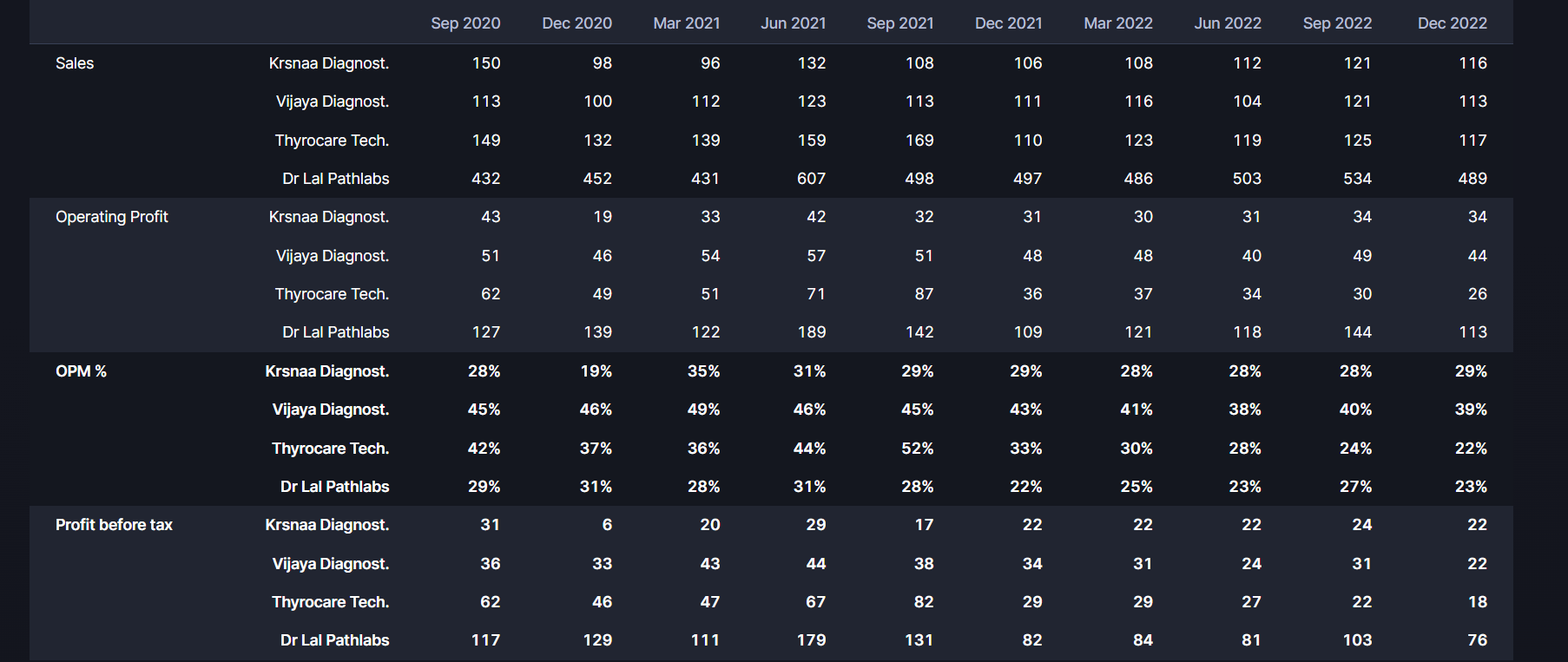

Why OPM margin of krsnaa is lower when compared to Vijaya diagnostics? Below, I have captured the split-up of major expenses incurred by both Vijaya and Krsnaa.

Sales of Krsnaa and Vijaya Diagnostics are similar. My thought process, Krsnaa will have more patients from government hospitals and that reduce the costs of reagents and other materials consumed. But Krsnaa’s cost of material is higher.

Also, major part of both diagnostic players is in Others. Do we have any idea on what are those expenses?

3 Likes

Good observation you have made. My thought on your question is following

- Krsnaa revenue is more in Radiology as specially teli-reporting. (according to me hard to compare teli-reporting with pathology)

- Krsnaa is PPP player they keep telling that they are lowest bidder - the better margin only possible with scale.

1 Like

All the follow-up queries I got in replies are addrrssed to sm extent in recent con-call; which is why I referred to it and urge others again to go thru it. Running in ur assumptions without checking the facts is sure shot recipe for disappointment. I can address broader themes here, bt again it vl be useful only if good counter points cm up w.r.t the biz( not whr the stock price is nd it deserves that validation)

- Topline growth : -

The growth looks tepid on reported figures bt once u adjust for COVID nd Rajasthan tender earnings, u’ll get the true growth picture of underlying earnings. Khemka saab(Aditya Khemka frm Incred) got these nos. dissected and confirmed from the mgmt.

- Compressed Margins : -

The opex in getting the new centres up nd running is wat’s keeping the margins low\stable at the moment. Nd again, a 25% EBITDA margin in low range is indicator of a good biz model IMO( Moat, No Moat, Commodity, Non-commodity however u classify it)

- Misc : -

B2C diagnostics biz with home collection facility is a different ball game and an altogether diff. logistic setup which the mgmt dont want to dilute thr Focus to.

Lowest cost Moat is also a type of Moat and no harm in pursuing that strategy if the mgmt is confident of execution. Now whn and wat multiple mkt assigns to it is anybody’s call

Patients coming to them directly, thru health schemes, doc referrals etc. all boils down to and can be tracked thru the vol. of tests they’re doing. Nd that is the major metric to track. How the co. is acheiving that vol. growth nd wat’s the best way to pursue it is an endless debate.

Disclosure :- Invested recently. Above is my understanding of the biz nd not a reco in any sense. I hv been very wrong in my assessments in near nd distant past…![]()

4 Likes

I am not a very experienced investor. And I am pretty new to this company. So please share your thoughts

The below line from Concall caught my attention.

We are happy to announce the launch of its new Genexus system, the first fully integrated Ion Torrent NGS platform in PPP model and offers a fully automated specimen to report workflow with unparalleled turnaround time. The Genexus system sets a new standard is NGS technology, and we are confident that it will have a significant impact on the molecular pathology community.

Blockquote

NGS stands for Next-generation sequencing

Molecular pathology - Molecular pathology seeks to apply gene expression against morphology and use gene expression analysis to validate large numbers of targets

Next generation sequencing (NGS) technology has revolutionized genomic and genetic research. The pace of change in this area is rapid with three major new sequencing platforms having been released in 2011: Ion Torrent’s PGM, Pacific Biosciences’ RS and the Illumina MiSeq.

Ion Torrent next-generation sequencing

Next-generation sequencing (NGS) utilizes massively parallel sequencing to generate thousands of megabases of sequence information per day, opening doors to new research studies that were once difficult to accomplish in a practical manner. Powered by semiconductor chips, Ion Torrent next-generation sequencing technology helps you implement a fast and simple workflow that scales to your research needs across multiple applications including inherited diseases, oncology, infectious diseases, reproductive genomics, human identification, agrigenomics and more.

Here is a blog from Dr Lalpathlabs - Next Generation Sequencing(NGS) in Cancer Diagnostics and Treatment (lalpathlabs.com)

So basically, Krsnaa seems to be adding capability of Genome sequencing which can help in Cancer diagnosis. Technology is from Thermofisher which is good. Such a capability would be difficult for smaller competitors to come up with.

The question is, is something like this demanded in the PPP contracts or is it some kind of moat that Krsnaa is building to ward off future competition. I couldnt find anything like that in my limited reading of the PPP bids. And will the babus writing those RFPs be even aware of such latest technology.

What do you people think.

7 Likes

Krsnaa Diagnostics Q3FY23 earnings call notes.

-

As of today, Krsnaa is a leading PPP diagnostic player with 127 radiology centers, 1,522 telereporting centers, 97 processing labs and 741 pathology collection centers.

-

On the B2C side of business, we have launched wellness packages at affordable rates, which help us to expand in the B2C side. The wellness package is Ayaksham, which covers basic tests as well as special test.

-

receivables normally in this time of the year, which is around Q3, the receivable days go around 94, 97 days, which is a typical trend we see in our line of business. Q3 onwards to Q4, the authorities will start basically closing out their whatever processes so that before March end they can complete the payments so that their next year budget doesn’t get impacted because they have to basically pay out, otherwise, if they don’t pay us before March or before the year-end then their next year budget also gets impacted.

-

INR 107 crores of the capex we have already incurred till 9 months. INR 22 to 25 crores, which is as per the plan, which we have to get executed by this Q4.

-

Rajasthan new tender, which we have bid and awaiting results, it’s roughly about around INR 450 crores, INR 500 crores for couple of years. So basically Rs. 250 cr per year revenue potential.

-

Comparing between radiology and pathology, certainly, pathology margins, EBITDA margins are a bit lower than the radiology. But I think the difference will not be significantly high between radiology and pathology, over around anywhere between 5% to 7%. And also one of the reasons why because there have been more pathology tenders. And also to like we’ve been saying, we want to have a healthy balance between radiology and pathology. That is the reason why we’ve also participated in these tenders and continue to win them. And of course, from an ROCE perspective, pathology is better compared to radiology.

-

BMC, where we are looking for annualized revenue of INR 30 crores to INR 40 crores, considering the 600 collection center and 1 processing lab.

-

Orissa, INR 50 crores to INR 55 crores annualized revenue, which we are expecting from 5 labs and 360-plus collection centers.

-

BMC to be operationalized by Q2 next year. Orissa will take time as there is wider area to be covered.

-

Depreciation: So for the equipment, we do as per the life of the equipment, but for the infrastructure and other things, which we do for the life of the project.

-

Punjab, we expect about close to INR 60 crores to INR 70 crores annualized revenue in the next fiscal. Revenue from Punjab in this quarter was INR 12 crores.

-

One of the key things that is kind of putting an interest to the revenue ramp-up is the Punjab is purely cash business. Now typically, in government business, when it is under the free diagnostic scheme, then you will see a very good ramp-up because patients come and they avail these tests because it is entirely cash driven. That is one of the reasons that we are seeing where the ramp-up has not happened the way we had anticipated.

-

FY22 had Rs. 70 cr sale from Rajasthan & Rs. 32 cr sale from Covid testing, these are down to Rs. 36-40 cr from Rajasthan & Rs. 2 cr from Covid. Taking these into affect, FY23 has shown very good growth.

-

FY '24, I think from a guidance perspective and considering the Punjab experience, we are looking at about INR 700 crores, INR 750 crores is what we are currently looking. I think by end of this year, when you will have more clarity in terms of given these projects, Punjab completely getting deployed and other projects. I think maybe I’ll be able to give a much more realistic guidance in the next quarter.

-

Krsnaa has been awarded with two major pathology tenders, one in the State of Maharashtra for setting up one lab and 600 collection centers and another one in the State of Odisha for setting up 5 labs and 386 collection centers.

-

Punjab. We have operationalized 24 out of 25 radiology centers and the remaining 1 radiology center will be operationalized by Q4 FY '23. All the 30 laboratories and 95 collection centers in Punjab are now fully operational.

-

We have operationalized entire pathology project in the State of Himachal Pradesh, and additionally, we have also successfully implemented the telereporting project in the State of Tripura, thus extending our reach to the Far East corners of India.

-

We are progressively expanding our presence. And during the quarter, we have added 7 radiology, 33 telereporting, 25 pathology labs and 64 collection centers.

-

what gets captured under the fees to hospital is, there are 2 components. Like one is we are also currently tied up with various medical colleges and private hospitals, where we have a center. So there’s a certain revenue share that we do to these hospitals. And then there is an element that we have in some of our bigger projects like Punjab or Rajasthan locations, where we have business associates as we call them, with whom we work in serving these patients. These are very remote locations. So in tribal areas or the remote corner, for example, if I give you Himachal Pradesh we have a center, which is near the Tibet border. So it’s absolutely impossible for people to go there. So we leverage these local partners to help us in terms of the logistics, in terms of sample collection. And these are the partners to whom we – it’s a straight away arrangement of revenue share. So basically, it doesn’t become a fixed cost. It is linked to the revenue. And at the same time, they’re also incentivized in terms of helping us not only increase our revenue, but also ensure that quality service is being delivered. So this is how the business partners and the revenue or the fee to the hospital arrangement works.

12 Likes

What does this mean? Not very clear

In Punjab tender customer has to pay in cash for the testing, generally the trend is that government pays for the testing services instead of the customer. Ramp-up is quick when the customer doesn’t have to pay. It’s one of the reasons that the ramp-up is slow in Punjab.

6 Likes

So does Punjab not have free diagnostic checks for a chunk of its people, unlike other states under the PM Jan Arogya Yojana, or any state scheme? Or do people claim reimbursements for the cash they have paid, or is there some other mechanism? Basically want to clarify whether Punjab centres are also free checks as far as the patient is concerned.

2 Likes

Finally, Punjab project is fully operationalized. Last center operationalized at Fazilka, Punjab. Management was right as they mentioned about some issue being faced at center located near India-Pakistan border.

Punjab project contains:

25 CT Scanners,

6 MRI Machines,

30 Pathological Laboratories and 95 Collection Centers,

1 Referral Laboratory

Disc. Invested so might be biased.

2 Likes

Since I wrote this post there is definitely more Interest in Krsna Diagnostics. It seems the company has made good strides in small state ( HP). Can this model be replicated if not totally at lest with some degree of success… in other states. ?

Forum guys can opine… the idea seems to be how to sweat assets which is very constructive for investors…

Malolan…

1 Like

The managemnt commentary is not consitent and they do not seem achieving the renenue target which they have also admitted. I see lack of management bandwidth and consistency.

5 Likes

One of the major reason for under performance apart from average results is the holding by DII and FII which is constantly reducing:

| FIIs + | 6.00 | 4.44 | 4.49 | 4.27 | 4.06 | 4.14 |

|---|---|---|---|---|---|---|

| DIIs + | 30.16 | 30.14 | 28.64 | 27.36 | 20.43 | 19.41 |

If the poor performance continues there will be selling pressure from FII as well as DII and they still have a very large holding of around 23.50% (reduced from 36%)

Disclosure : Exited all my positions around 500

2 Likes

My biggest fear is the terminal value decline for Krsnaa. Since most of tenders are 5-10 years long, there is no visibility beyond that. Hence, the fair value can be at max 10 PE (because revenue visibility is limited). I know that it might win further tenders & re-bid successfully for expiring tenders but that is just an optionality. In other words, there is no certainty of that happening. The government will grant the tender to the lowest cost bidder. Period. It doesn’t care about who is the most qualified or how good of a job the previous bidder did. Hence, there is no assurance that Krsnaa will be able to match its current 78% win ratio or that it will be able to successfully re-bid for expiring tenders.

4 Likes

WITH FALL OF MORE THEN 60% FROM IPO PRICE, NEITHER PROMOTERS NOR INSTITUTIONAL INVESTORS ARE FINDING VALUE IN THIS STOCK.

If institutions do not want to add it his level then they would in all possibility like to exit at every higher level.

It seems there are some concerns which retail investors are not aware of as the fall has been uniformly in one direction from 1000 to 370 levels…

5 Likes

You have answered your own question regarding terminal value and long-term revenue visibility by talking about lowest-cost bidder. If you try to understand their business model their true moat lies in being signifantly cost effective as compared to the other bidders. And PPP is the future, government has understood how its a win win for both the govt and private players and going forward this model will only gain more traction.

P.S: Tracking closely, not invested.

5 Likes

IMO, it is better to analyse the fundamentals than speculating on fall from IPO price. Most IPOs are priced high and it is natural for market to rerate post IPO. Also do note that these companies were cash generating machines during COVID and commanded premium valuations. For example, more establish Dr. Lal Pathlabs has corrected 50% from peak.

Krsnaa has many factors that can become a significant moat. Some of them:

- Good grasp of pricing

- Knowing how to win bids (linked to above)

- Strong process for managing B2G contracts (evident from low receivable days)

- Leveraging economies of scale

- Baseline capabilities from which to grow new biz (almost no marketing needed)

- Started generating cashflows sponsoring growth by internal accurals

- Fast growth in expertise and workforce (can see in LinkedIn)

- Large market opportunity (even if bid win rate comes down) with first mover advantage

Of course, there are some concerns, which are raised by some of contributors here

- As with any company, the op margins would compress as the sector matures and competition intensifies. So, there could be some discount given on that.

- B2G is usually associated with dirty transactions or long receivable days. So, the market can take a long time to rerate the stock.

- Company’s new ventures into pathology and bet on franchise model might turn out to be a spending frenzy of COVID money.

- Employee reviews indicate that pay is one of major issue.

For me, it is starting to appear as good value at this price if you remove all of COVID generated money. The key is to see how they use their capital going forward.

Disc: Invested recently.

7 Likes

Thanks to @aga.ayush11, have been doing more groundwork on Krsnaa with him.

Sharing high level takeaways from a call with an industry expert.

Context: They are a low cost diagnostics company, they participate in PPP

tenders where the group overall has 80 Cr. of revenue. They have around 20 years

of experience in the diagnostic industry, and have gone head to head with Krsnaa in the past.

On the PPP landscape in India

-

PPP in India has seen huge success in the last 5 years, currently it is in a

growth phase that will last for 10-15 years. It is not nascent, and is not yet

mature. -

There are two drivers of growth:

- So far PPP tenders have been in radiology, increasingly, tenders in pathology

are being rolled out. The next gen of PPP tenders will be in mammography,

dialysis, etc. - The size of these tenders is now growing as states have finished one iteration

(generation 1) of PPP tenders from 5-10 years ago.

Governments start by rolling these out in medical colleges → super speciality hospitals → district and sub-district hospitals.Generation 2 tenders are larger as evidenced in Rajasthan. Any large player who wins these can grow at 30-40% CAGR for the next 6-7 years unsurprisingly.

- So far PPP tenders have been in radiology, increasingly, tenders in pathology

-

For example, West Bengal alone has a 1000 Cr. of PPP diagnostics market size per year. Larger

states have a market size of 2000 Cr. +. Overall market landscape in India today is probably close to 15 - 20,000 Cr. -

States can choose to do in-house, or go down the PPP route. Eventually, more states will do PPP.

On the nuances of tender bidding

-

The authorities that float the tender, and the authority that carries out the day

to day operations are two completely different bodies. -

The largest challenge currently in PPP tenders is meeting the technical

criteria. This is a significant barrier to entry. Governments have stopped

floating tenders where you do not need experience. Now you need 3+ years

of MRI experience under PPP. New players get stuck here. You may have

resources and funding, but meeting experience criteria is tough. Even if you

choose to make a consortium with someone else, governments have killed

consortiums by saying leading players need experience. -

There is no chance to influence the outcome of a tender in any way. These are carried out in a transparent manner.

-

Tenders are awarded on largest discount to CGHS rates. CGHS for MRI is

2000 rupees, but you have 40 different MRI tests benchmarked to this rate.

Different body parts, contrast, etc. The weighted average of these 40 tests on

a CGHS rate of 2000 actually comes out to 3000 rupees. -

The unit economics can be vastly different depending on the type of hospital. If it is a medical college, one can expect higher number of scans per day. If it is a super speciality hospital, the test mix will be different. The game in bidding for a tender is to think about what test mix one expects, and bid accordingly.

Working with the government, and receivables

-

Budget for National Health Mission is given by the centre. The states where centre + state

have the same party in power, adoption of PPP is not a challenge. For other states like Punjab or West Bengal, state governments try to portray the scheme as theirs, not the centre’s. State-centre politics play a large role in successful PPP adoption. -

We have never had to write off any receivables. Governments have a healthcare budget and have to make sure budget spend is accounted for, so receivables is not a problem.

-

The largest external driver of how quick receivables comes to you is whether

the centre + state have the same ruling party. Centre wants very specific data

for PPP tests: 1. Sex of patient, 2. Age, 3. Name, 4. Condition. If centre and

state are the same party, this is done quickly.

Operational Highlights

-

There are two kinds of implementations of PPP: citizens pay at a discount to CGHS rates, and free diagnostics initiative. Ultimately, even if tests are life or death, someone who doesn’t have purchasing power will think 20 times before getting a 2000 rupee test done. For this reason, scaling centres is much faster when this is done via free diagnostics.

-

More states are going down the free route as it gives you immense political capital to pitch free diagnostics to your citizens.

-

Private walk-ins is a very reasonable model to target for someone like Krsnaa. OPD patients are all seen by 5pm, and as long as you prioritise hospital clients first, no one objects to private walk ins. 5pm - 11pm is a great time for this.

-

Awareness of free diagnostics is a critical theme. We’ve seen in our state that it took 3-4 years from the centre starting to seeing peak footfalls.

PS: there are a couple of large tenders currently being floated by governments. One closing in a week is a statewide pathology tender in Assam:

Disclosure: Invested, in top 5 positions, transactions in the last 30 days.

36 Likes

what is the revenue potential of this Assam pathology tender