I was just scrutinizing RPT of Krana … And I come across this fact that the registered office of Krana in Pune is owned by Sunita Mutha (wife of Rajendra Mutha) and company pays her a rent which has increased at a rate of 18% per annum…

From. 2.1Cr In fy2018-19

To. 3.6 Cr in ft 2021-22… A rise of about 18% per annum ?

Is this a conduct of highest integrity on part of promotors?

There is seldom single cockroach in kitchen !

Promotors have to come clean if they would like to see the business grow and stock fly. Investors are smart gen folks, wont take time to divert the funds to other avenues.

Yes this is worrisome. Dont know why Indian promoters find such stupid ways of taking out money from the company when market is ready to reward good governance.

Thank you for sharing this. It is important and worrisome - the promoters seem to be siphoning out money at the expense of minority shareholders. I intend to ask the management about it if I attend the next concall, but in case I am unable to attend I hope that someone on this forum does that and shares the response.

Disclosure: Invested - had initiated a tracking position.

I have already asked about unusual hike in salary of Mr. Rajendra Mutha. Company said earlier it was a way below compare to industry standards and then investor (before IPO) have advised company and it’s chairman to make it standard so my best guess is that this is something on those line. we should keep eye on increase in rent for this year which should provide more clarity.

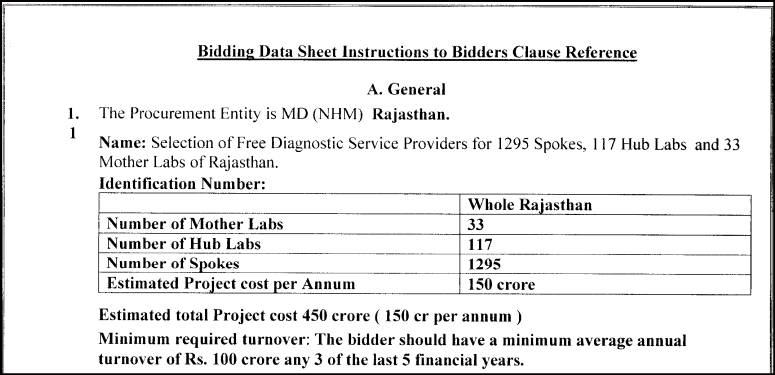

Krsnaa Diagnostics has emerged as a L1 Bidder with regards to tender in consortium with Telecommunications Consultants India with the Tender Estimated Size of Rs 450 crore by the National Health Mission, Rajasthan for providing “Laboratory Services under Free Diagnostics Initiative on HUB and SPOKE Model under NHM” in the entire State of Rajasthan

I have observed incomplete information in the today’s press release. I’m not sure why this incomplete information is published to the investors.

Duration of the contract was not mentioned and percentage of share in the consortium is not mentioned.

On the other hand in the last conference call management mentioned 225 -250 crores revenue from this contract but in press release its mention that 450 crore revenue. I wonder how this revenue is doubled in the matter of 1 month.

These days everything is a stick with which to beat management.

The nature of the disclosure follows SEBI’s circular, seen below. They’re free to put out a press release in addition to this, but they’ve already addressed this in previous concalls.

Let me go over the basics for where this 450 Cr. number comes from. The government in each tender puts out an estimated cost, (not revenue!) for each tender. The estimated cost for this tender is 150 Cr. per year. The standard practice is to report government figures in the contract size estimate.

So when asked, management tells us the estimated revenue is above 200 Cr. I don’t see why this is a problem.

Lastly, every single RFP, bidding stage, bid details is in the public domain. Why don’t investors read what’s out there (or even scroll up higher up in this thread) before complaining about disclosures?

On lighter note, This is due to stock price underperformance so what’s missing and wrong with management and company could get more attention.

I noticed since last few concalls /press release , management has been conservative as they have beaten down on their guidance to 3x of profit and 2x of revenue on base FY22 as they are going to miss guidance and their experience during last year or so they have had a lesson to give lower guidance and outperform. I really hope BMC and Rajasthan project help them to reach at least 80-90% of their earlier guidance.

So Rajasthan project is for 3 years (150*3) so cost will be 450 crs and revenue around 675 crs so gross profit could be in vicinity of 225 crs for 3 years (just approx. calculation and need to deduct TCIL’s share).

I think the correct way in modelling Krsnaa’s B2G side is similar to an EPC business in terms of orders in - orders out.

Order

Type

Value

FY22 Revenues

455 Cr.

Loss of 2022 Rajasthan Contract & Covid

-70 Cr.

Punjab + Himachal IPO Project

X

Tenders won in 2022

Himachal Pradesh

Pathology

A

Chandigarh

Radiology

B

Uttar Pradesh

Radiology

C

Maharashtra

Radiology

D

Rajasthan

Radiology

E

New Delhi

Radiology

F

Tenders won in 2023

Odisha

Pathology

G

Maharashtra BMC

Pathology

H

Rajasthan

Pathology

I

Tenders currently being evaluated

Rajasthan

Radiology

Andhra Pradesh

Teleradiology

Punjab

Teleradiology

West Bengal

Radiology

Madhya Pradesh

Radiology

Assam

Pathology

Haryana

Radiology

Expiry of other tenders

Z

I am biased, so I leave it to the reader to think about the value of these tenders from your own scuttlebutt and estimates, which tenders are likely to be more successful to ramp up/execute than others, and when each is expected to go onstream.

In my opinion, Krsnaa can do 700-800 Cr. of revenues without the Rajasthan tender, and without winning any additional tenders going forward.

Tracking tenders currently being floated adds a lot of visibility (see Krsnaa Diagnostics - what is the diagnosis? - #114 by Chins) but is still a lagging indicator of the direction governments will take under the free diagnostics mission.

I realised almost every state publishes their budget and targets within the PPP diagnostics mission.

Case Study: Assam and Rajasthan

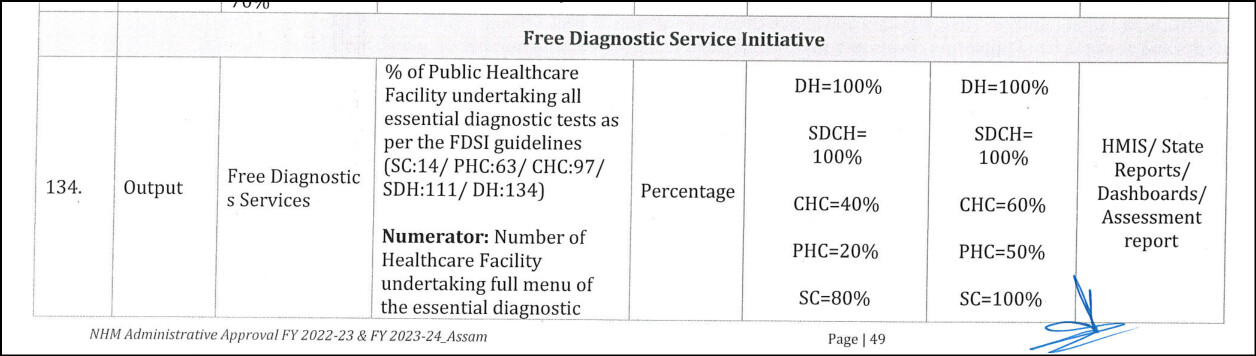

Snippet below is taken from Assam’s FY24 budget. Note how the targets for the scheme go from covering 40% of Civic Health Centres, 20% of Public Health Centres → 60% of CHCs, 50% of all PHCs in the state. This is confirming evidence from scuttlebutt above.

@Chins I will be more than happy to pitch in. I picked up my state and browsed the Haryana’s Budget 2023-24. I am only pasting the relevant portion on Diagnostics.

I had earlier announced that all families whose annual

income as per PPP is upto ₹1.80 lakhs will be provided free

annual health check-up. The NIROGI Scheme has since been

launched and the benefit of the Scheme has begun to be felt by

the Antyodyay families

The Nirogi Haryana scheme will cover 1.82 lakh beneficiaries from 42,000 families enlisted under the Antyodaya Yojana in Panchkula

Enlisted beneficiaries will be approached by ANM or Asha workers and handed over an ‘amantran patra’ (invitation) to visit the health facilities on a particular date.

The health check up includes a complete general and physical examination, some mandatory tests, and tests advised by doctors

The reports will be shared within two working days through e-Upchaar or through the ASHA or ANM concerned

As many as 51 health facilities in the district have been allotted to enlisted Antyodaya families.

With promoter stake of only 28%, what’s in it for the promoter to grow the company? Hardly any skin in the game IMHO. I would exercise lot of caution for any microcap company having such a low promoter stake (unless I know the promoter integrity, through other means)

Let me flip this and ask you the same question with more nuance.

In the last decade, a large number of founders have gone to VC firms for capital, especially in a business where radiology machines are expensive and is harder to bootstrap.

How much dilution happens across funding stages, and what is the norm for founder stake at the end of the dilution?

With around 20% dilution at each stage of funding, here’s how ownership usually changes:

With this in mind, Krsnaa’s ownership of around 33% (including family) doesn’t look too bad and is actually in the upper quartile amongst other VC exits.

While one wants promoters to own as much as possible, wanting 50-75% ownership without thought to context is unreasonable in my opinion.

So I flip the question to you. Where in Krsnaa’s funding rounds do you think they sold for cheap, and in your opinion what was fair valuation?

With promoter stake of only 28%, what’s in it for the promoter to grow the company? Hardly any skin in the game IMHO. I would exercise lot of caution for any microcap company having such a low promoter stake (unless I know the promoter integrity, through other means)

Disclosure - not invested.

Skin in the game is better assessed by gauging what % of a promoter’s net-worth consists of equity ownership in the publicly listed company i.e. Value of equity stake in company/Total NW of promoter. Even if a promoter holds 2% of a publicly listed company, but that 2% holding represents 90% of his/her wealth, the promoter has much more skin in the game than a promoter who owns 70% of a listed entity but that stake represents only 20% of his/her net-worth (Maybe by virtue of holdings in other unlisted or listed entities).

After a year of trying to understand the business better, the greatest jumps in understanding have come from analysing each state granularly.

Some updates on current understanding:

Punjab potential is likely to be capped at 70 Cr. of revenue as the tender payment is cash based, not cashless. The centre may choose to make this cashless after a few years, even if the ruling party in the state is different. One should price in 70 Cr. and move on.

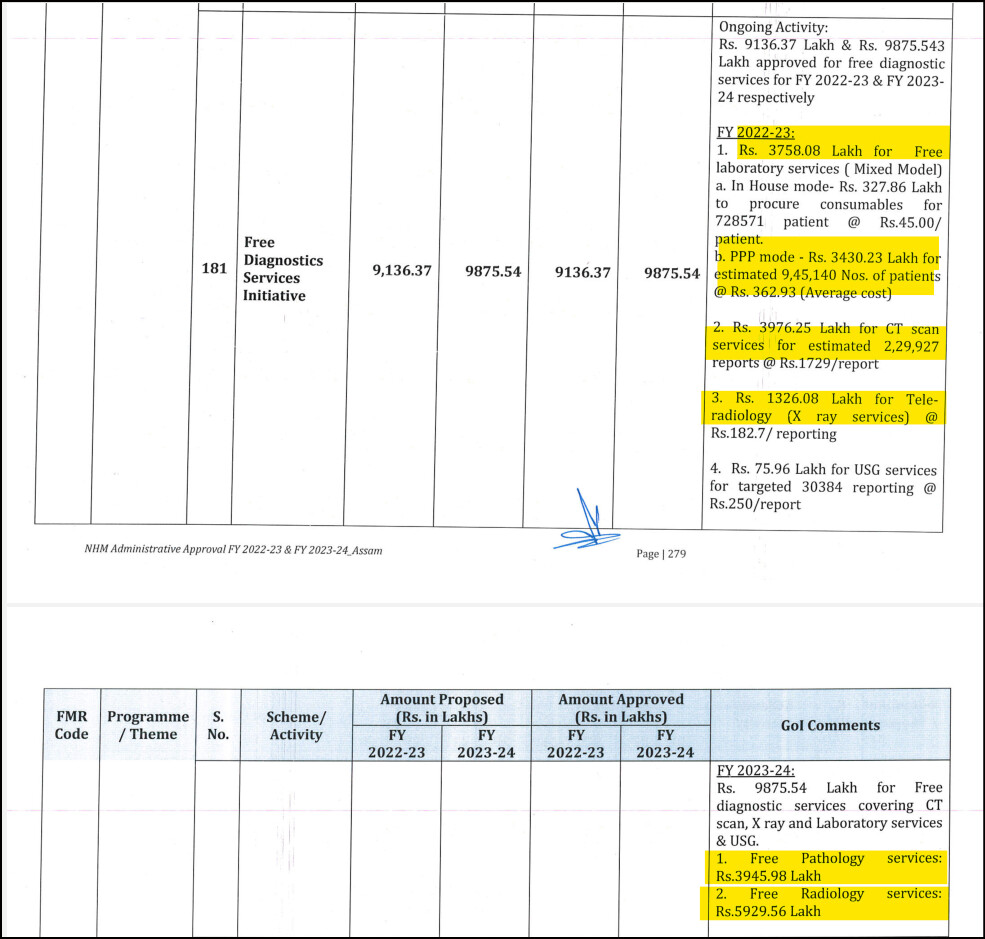

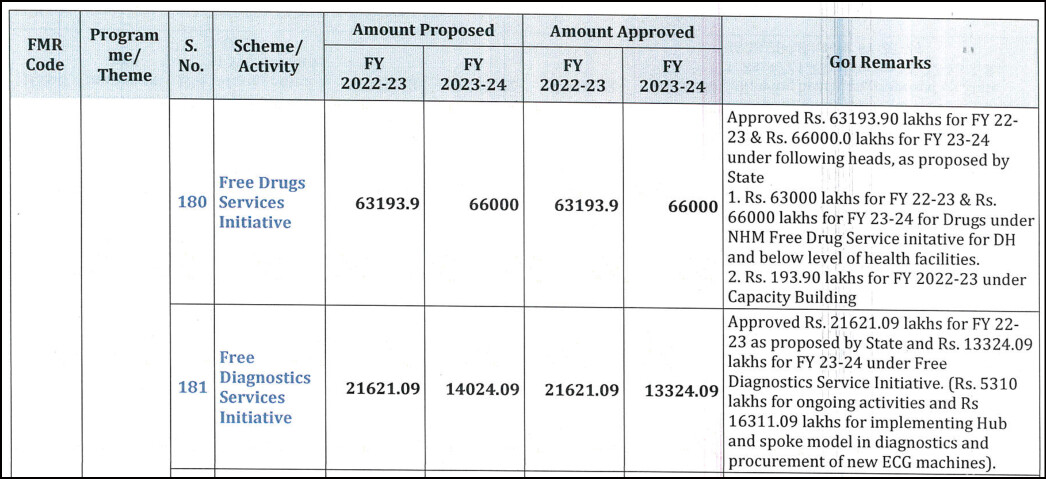

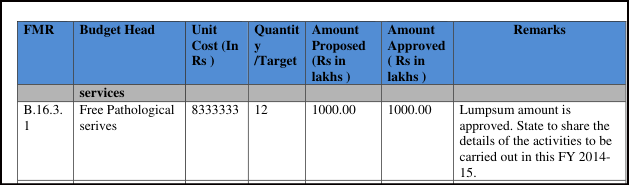

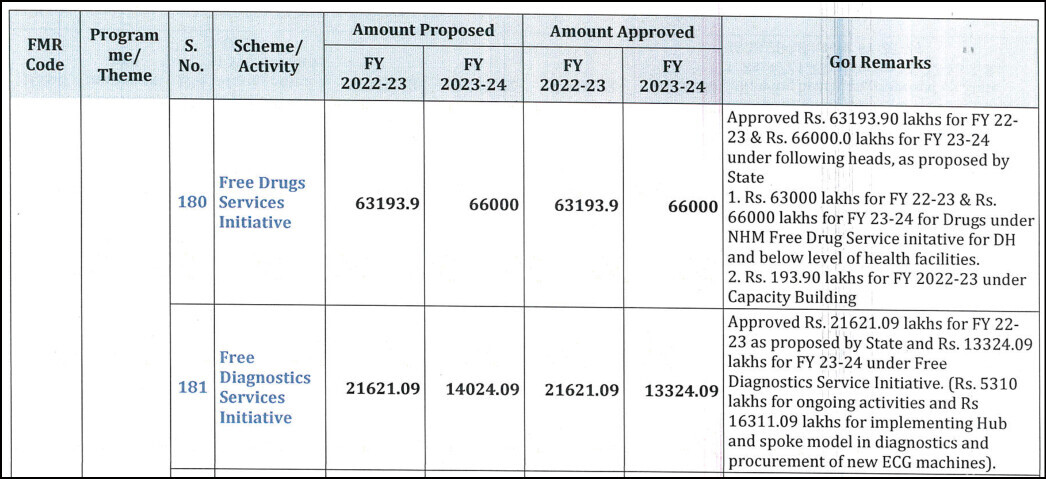

Rajasthan’s execution for the free diagnostics mission has been incredible, and is possibly the greatest case study of what could go right. Two pictures below are worth a thousand words: Centre’s contribution for PPP diagnostics in 2014, and the same in 2022:

The budget requirement went from 10 Cr. in 2014 to 220 Cr. in 2022, over 20x in 8 years.

The obvious next questions are to pin down what factors lead to this, and the answer depends on two parameters:

Number of locations.

Number of tests offered.

Over time, the free diagnostics initiative went from a few district hospitals in 2014 to over 1000 locations in the 2023 tender. Government does audits during each run of the PPP outsourcing and gets reports on where things have been successful.

In each state, NHM contributes 50-60% of the funds for free diagnostics, and the state pays the rest. Therefore the actual market size is of course a lot higher + you have other ministries aside from the NHM that float tenders. (Example BMC tender is not NHM sponsored).

In my opinion, Odisha is an example of a state that could replicate Rajasthan in a few years.

Krsnaa won a statewide tender a month ago. My estimate then for the revenue from the tender was around 40-50 Cr. I now think this could be a minimum of 2x of my estimates for the following reason:

In the RFP, the government required the tender partner to provide 38 blood tests at district hospitals. Now, they have doubled down and made 146 tests available in each district hospital, and have included more families within the scheme.

B2G questions posed by investors are memorable (and valid), it’s nice to hear some good news from the same B2G angle, and have this data on budgets.

Krsnaa may have just won a state-wide tender in Assam. Will look for confirmation soon from the authorities and in exchange filings in the next few days.

Thanks @Chins for your excellent work on Krsnaa so far.

I wanted to share a perspective on Krsnaa that I thought of over the last coupe of days: I have begun to view Krsnaa as arguably one of the growth stories that is most uncorrelated to everything that is going wrong with the global macros. B2G in an election year in a systematically important sector where spending is only going to increase. No real competition (so far), no real impact of a global slow down on demand, no raw material pressures or supply constraints, no dearth of capital for growth (with already low debt) and clean and steady growth.

This could be a place to hide while the global financial environment remains uncertain, and I feel the perception towards this unique kind of B2G may change pretty quickly and could rerate the company in this FY. Lets see how it goes.