Hi, iam new here and new to investing

Is there a concern that Krssnna has 5(or more) private limited subsidiaries in the same line of business

2 Likes

Hi Dr., welcome to the community.

It’s definitely good to consider what subsidiaries a company has, and subsidiaries often tell a large story that isn’t seen unless one goes through them granularly.

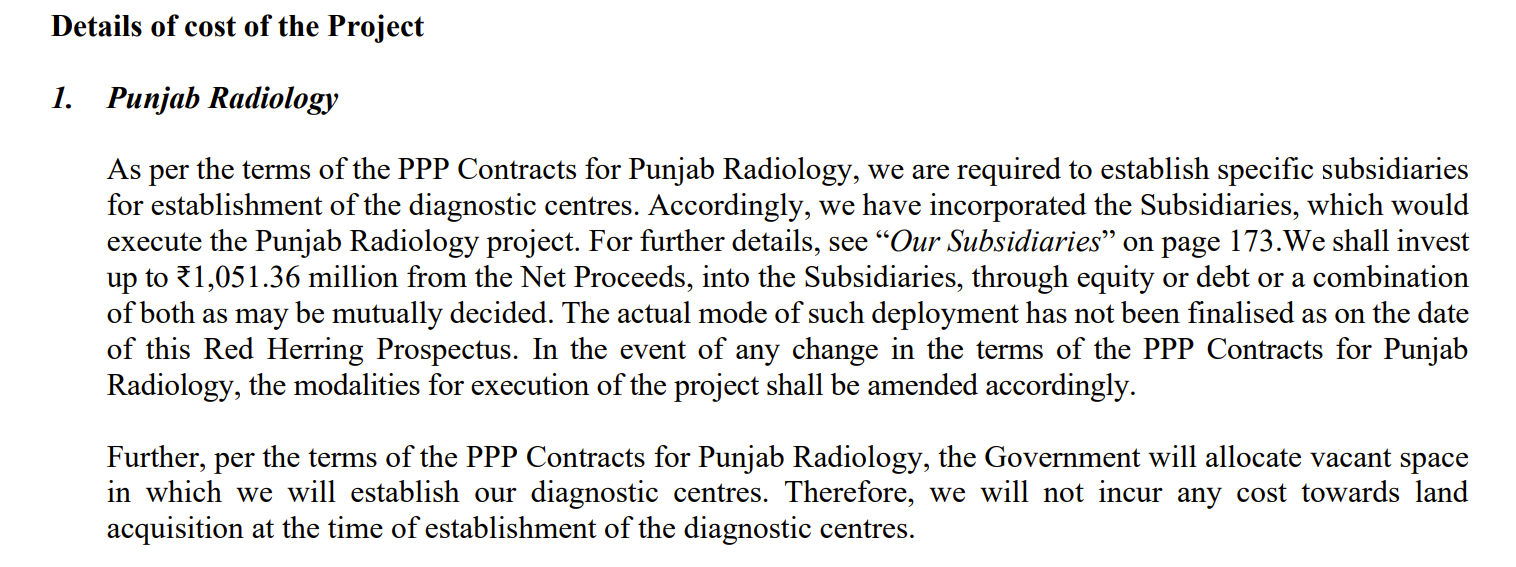

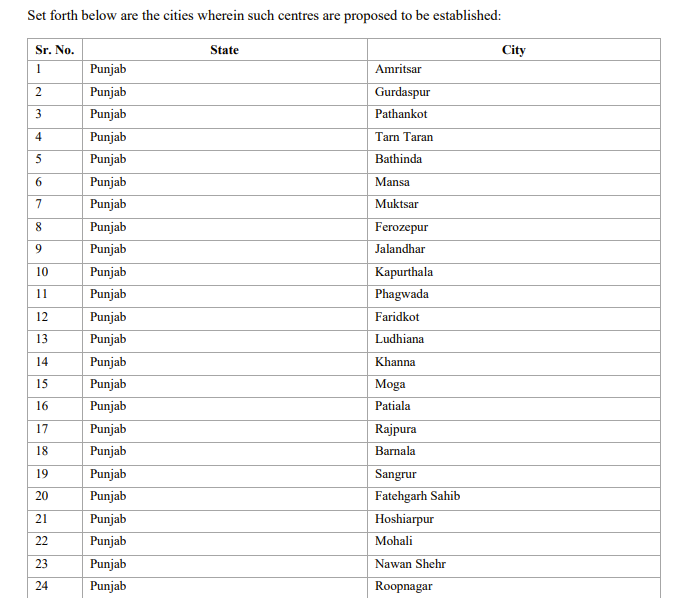

In Krsnaa’s case, I don’t think there is any story to the subsidiaries. The red herring tells us why:

All five subsidiaries are in Punjab, and since they’ve actually won tenders for more than 5 centers, I would not be surprised if more subsidiaries are incorporated until we exhaust the list below:

6 Likes

@Chins ,Thankyou very much for the prompt reply. That helps…

1 Like

Have been studying the co all day. Also talked to a few seasoned investors to understand why they have it a miss.

The thesis pointers are clearly standing out: differentiated lowest cost business model .perhaps one of only few instances where a private party might have leverage or position to negotiate with governments since healthcare is something which impacts populace directly (as against infra or defense). This reflects in their relatively strong working capital position currently. This lowest cost is aided by unique business model where owner of the healthcare center provides rent free space, electricity, electrical equipment like step down transformers, water etc. Captive patient supply is maintained & co does not need to spend on marketing. In addition their scale enables them to do bulk purchases which also enables them to get good costing on the MRI/ct machines. All of these enable a cost which is 20-30% lower than CGHS rates at least. This is a win-win-win.

Government gets to save on capex & opex & deliver quality healthcare to people.

People get good quality healthcare at affordable rates.

Company gets to make decent margins.

I was actually surprised to see working capital cycle being quite mean. For around a 400cr runrate their wc is hardly 30cr…this is quite low. The receivables are almost completely offset by payables which makes the wc lean.

Actually I did my own roce computation and it seems to be around 30%.

300 cr fixed asset. 30cr wc. Around 25cr ebit per quarter. This works out to around 30% roce. Am I missing something? We have to take the normalised interest cost since lot of interest in older Q was due to debt which has been repaid.

A couple of other things which I could understand which are very interesting… The radiologist are employed on a variable pay wherein they get paid per test analyzed. That is amazing because it does 2 important things :

- Incentivises radiologist to analyse more tests. Aligns them to companies growth.

- Converts a fixed cost into a variable cost so that any disruption does not lead to large depression of margins. In a way the doctor is a DAAS : Doctor as a service. Pay as you go model. That is nice.

- Their Pune tele radiology hub enables their radiologist to monitor & diagnose many many cases which enables them to improve their precision. 190 radiologists all learn from the cases which are complex & enables company’s quality to go up significantly. Lot of focus on machine learning these days. Human learning is actually the bottleneck in radiology. And krsnaa seems to be solving for it. Will be interesting to read the technical papers they have published just to see what their key learnings have been.

Let’s also look at the anti-thesis pointers which imo are keeping valuation depressed.

- Government is perceived to be a fickle player. Just because no problems have come in last X years does not make the business model robust against failures. The perception of government being fickle in payments sticks. & For good reasons. In a b2c like Dr lal your customer is a retail person who does not have option to pay or not. In some of krsnaa contracts the customer is govt which might wake up one day to decide previous govt contracts were too liberal & need to be revised downwards. If we see a latest example of meituan in china & take rate capping by Chinese government we can immediately see some evidence for government across the world not being behind in taking a bad idea to it’s logical conclusion. That risk will remain imo. The absence of evidence is not the evidence of absence.

- Scuttlebutt talking to doctors tells me today it’s very easy to set up diagnostics centers. Anyone with 2cr rupees can set up a lab. Barrier to entry is low. Dr lals return ratios & valuations are seen. Competitive intensity needs to be monitored like a hawk as stated by someone else in the thread.

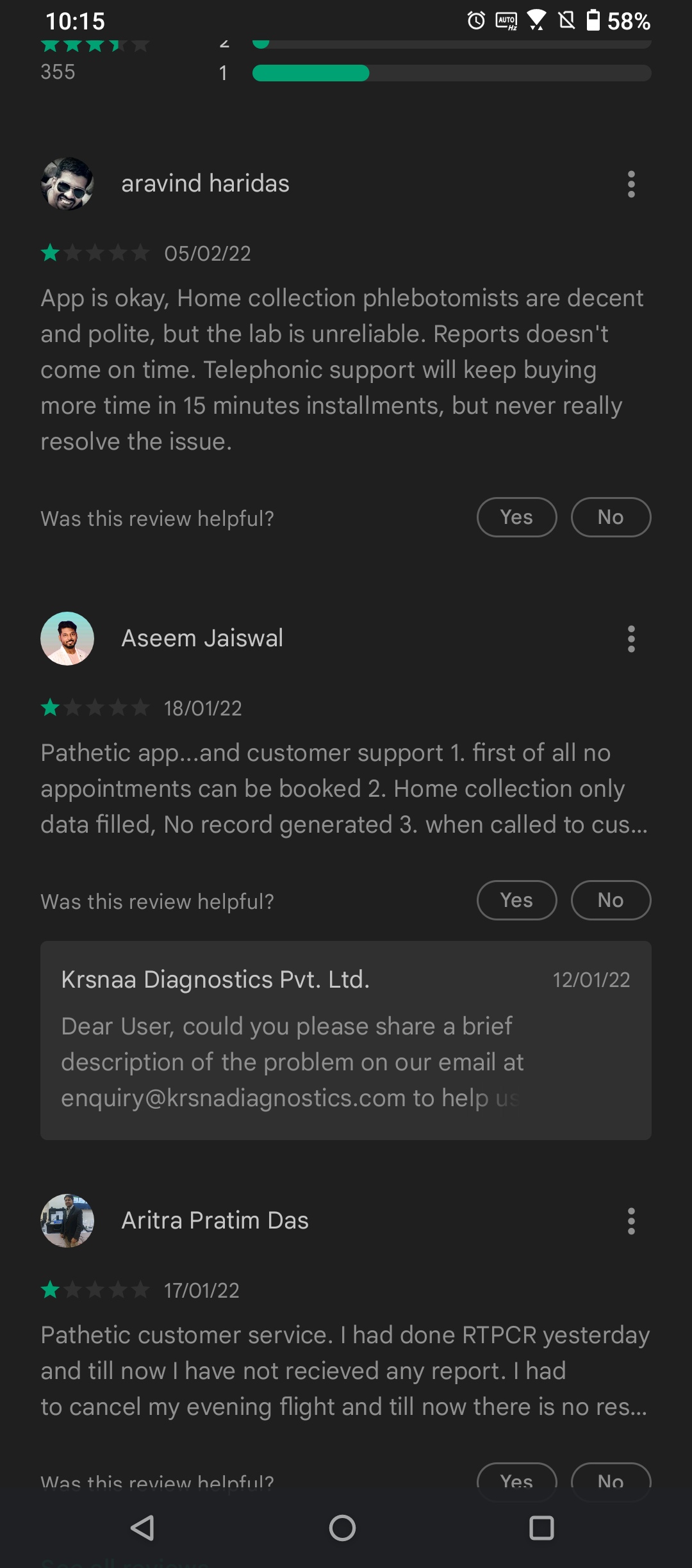

- Look at krsnaa diagnostics rating on Google Play. You will find many reviews which talk about their horrendous experiences. Attaching a few.

The backbone of a b2c brand is good customer service. In the absence of that, you are simply waiting for someone to come & offer a better service than you do & poach your customer. They don’t have that yet, as far as my digital scuttlebutt tells me. Dr lal is way ahead. Hope that are learning from their experience & understanding what it takes to crack b2c. The biggest trick of b2c is building reliable processes which ensure low Variance of outcomes. Customers want reliability. Trust. If i do my rtpcr yesterday I want my results today.

4. Some of the payables could be channel financing for vendors in which case the roce could be lower. Need to dig a little deeper to understand this better & get an accurate picture.

All in all looks like an interesting co worth studying deeply & understand the picture more clearly.

Disc : own a small quantity bought today for tracking & to ensure I have skin in game while I research.

31 Likes

Documenting some of my learning from various readings

My primary hunch was we are doing a mistake in considering all diagnostics as similar. In fact they are not.

Source : Dr. Lal’s FY21 AR

"Diagnostics can be further classified as pathology based and

radiology/imaging based offerings. The organised, branded, national

chains exclusively offer pathology based solutions predominantly.

Radiology and imaging based set-ups being capital intensive are

spread out far and thin and are primarily associated with hospital

establishments."

Source Thyrocare Call :

Radiology segment revenue contribution is 6.16 cr out of 117 cr. and they conducted overall 4691 scans vs 5722 scans YoY (degrowth). compare this to Krsnaa which did 4.79L CT scans and 1.45L MRI scans in FY 21.

So, seems prominent national players haven’t yet got their act right in radiology segment where Krsnaa is prospering.

My hunch was, national diagnostics players have reached a level where they seem ubiquitous and the growth headroom is limited, but seems they are not.

Source : Dr. Lal’s FY21 AR

“While standalone diagnostic centres account for nearly 47% of the

industry capacity, national organised chains like Dr. Lal PathLabs

(DLPL) account for ~16% share.”

From the above one can only imagine, the Radiology/diagnostic imaging industry is in infancy in it’s transition to national level organized players.

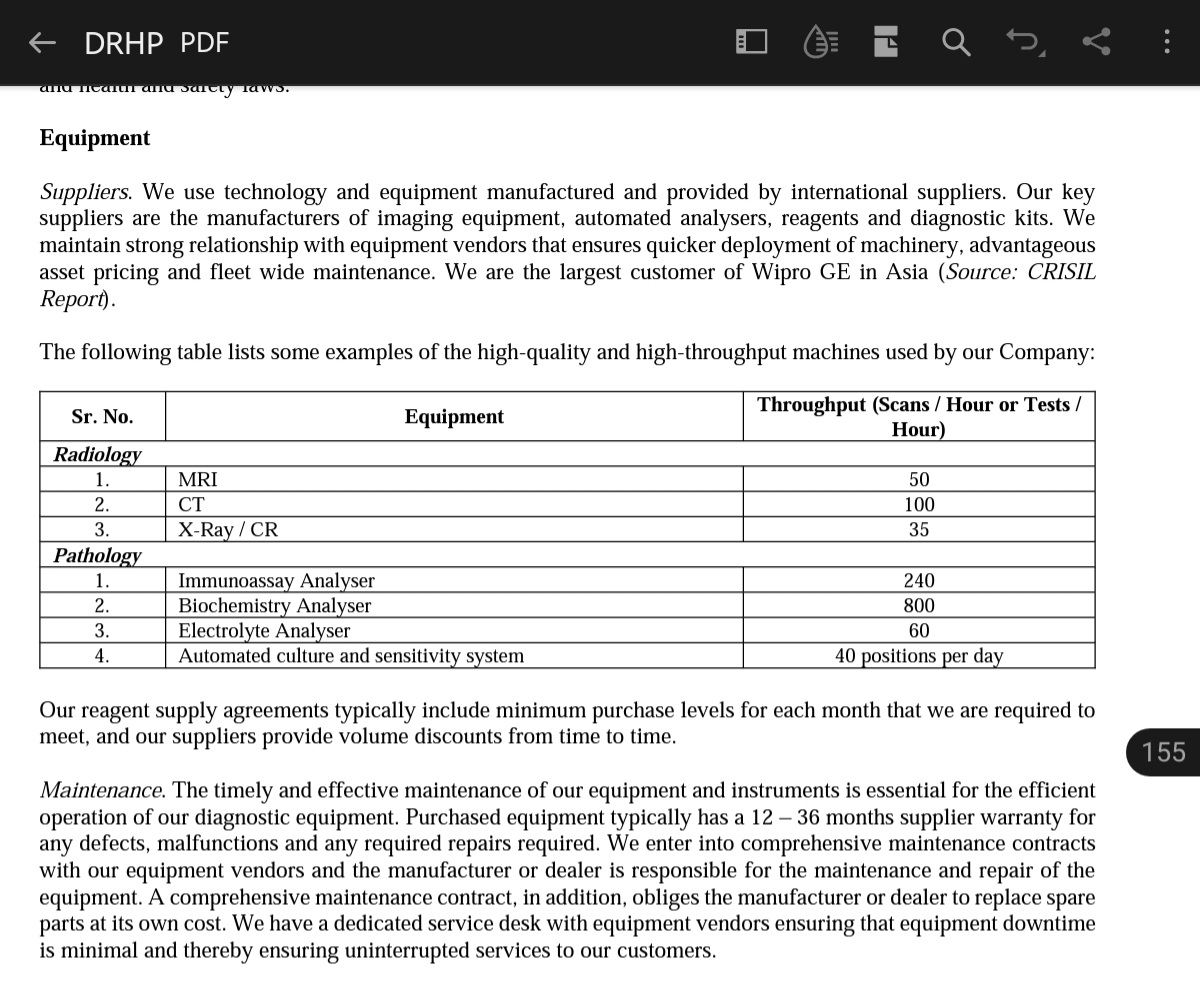

My understanding at this point is, the Radiology based diagnostic industry is not only capex intensive, but also needs skilled human resource to operate. My guess is, it needs a radiologist to run a radiology center. for a standalone center that’s a quite cost!! Compare this to a standalone pathological diagnostics labs collection center which anyway sends the sample to some central processing unit and needs only very basic skils at collection center level. So it’s this mix of high opex+capex which makes this part of diagnostic industry little tricky for new entrants.

Krsnaa has devised a solution, which seems to be working for now. They have India’s largest radiology tele reporting hub based out of Pune, which houses 190 plus radiologists. This gives them a unique value proposition of not having to employ a radiologist/doctor per center. Which is part of the reason for the operational cost advantage.

21 Likes

Another point that I wanted to add to above post, which differentiates the characteristics of radiology diagnostic industry from the pathology diagnostic industry is:

The competitive landscape of pathological diagnostic industry has become highly intensive in recent days because of the trend of “service at your doorstep”. People kind of expect every service that can be delivered at doorstep to be done so. Pathological diagnostic industry lends itself to door delivery model well. A person with a basic kit can come to home, collect samples and then the report can be delivered later. This has led to a mushrooming of these collection service centers in most residential areas. Almost every standalone medicine store in my area seems to have woke up to this opportunity and has tie up with some diagnostic lab and is ready to send over someone to collect sample. For a customer, it has become harder to differentiate one from another based on service.

Whereas for, radiology diagnostics that’s not the case because of the heavy machinery and the need for the person to be physically present at the diagnostics center which means this industry is very less likely to lend itself to mushrooming in every neighborhood and the centers will be concentrated around hospital where the footfall are likely to make economic sense. Plus they will have to pay commission to doctors for referral. Large hospitals are more likely to have their own radiology setup or will refer to some center based on commission. However when it comes to govt hospitals, specially the district HQ hospitals, there are a bunch of private players just in vicinity to capture the ‘theoretically unreferred’ patients. This is where Krsnaa now becomes a force to reckon. For govt hospital patients, the diagnostic service provided by Krsnaa is now as good as govt. provided service instead of relying on some unorganized player. Plus the lower cost makes it a no brainer choice for them. Govt. hospital services are open to all citizen so it’s only natural that some patients who are NOT availing govt hospital services will still prefer to get their diagnostics done with Krsnaa for the cost advantages.

So broadly it seems this industry will have a completely different characteristic compared to pathological diagnostic industry,

9 Likes

Here is another anti thesis pointer:

If we listen to q2 concall, we find management talk about vendor financing being something like credit lines of 100 crores. Their payables are also 100cr. They were asked multiple times by the participant what % of payables is vendor financing but evaded the question. In worst case let us assume all the payables are vendor financing & so should not be included in roce computation.

96cr annualized ebit assuming q4 is steady state. 307 cr fixed assets. 117 cr working capital. Gives us 22.6% roce. Not looking as much attractive now.

What is even more important is the direction of unit economics. 200cr capex happening in next year. Utilisation is already only around 30%.

We have prior from many related sectors like hospitals that a large capex & not waiting for it to turn profitable is a recipe for derating & value destruction. Pointed out by @Worldlywiseinvestors in his webinar on hospitals.

Aster healthcare is the canonical example here. HCG until now is another.

Not a direct 1:1 comparison but if we see sequent , vaibhav, poly Medicure all of them investing for long term get derated in short to medium term. Best time to buy such cos is when the capex starts reaching high utilisation. Many examples show us that markets are not efficient & actually do not price the capacity utilisation ramp up a priori.

I think to my mind the largest anti thesis here & a clinching one for me is the large uncontrolled capex will will drive return ratios down at least in the short term. Growth in domestic healthcare is not a problem, but profitable growth is. Figuring out what % of payables are vendor financing, what are the terms of the receivables, what % of them are over 90 days are probably most important from a clinching high conviction investment thesis here because growth, demand, business model are all more or less sorted.

On the upside, for a diagnostic center the journey from start to ramp up should possibly be much faster / much quicker. But definitely worth keeping an eye on that capex, vendor financing (capital deployed) piece. The p&l will be wrekt in the short term as the depreciation hits the p&l and the revenues do not.

22 Likes

Hello,

Putting in my two cents:

-

Demand.

Till date, problem with Government Hospital patients was paying capacity.

With the advent of Ayushman Bharat// State Sponsored Healthcare Schemes, that is / will get resolved.

Moreover, since these schemes have lower rates, only the lowest cost player will survive first and thrive later. -

Service extension

So there is already a Radiology centre.

Rather than setting up an own Pathology unit which may not provide the economy of scale and synergy, they can associate and become a franchisee for a pathology chain - thereby removing any CapEx need, but earning collection fees for tests outsourced. This may improve unit returns and directly flow to bottom-line. Collaborate rather than compete !!

Regards

5 Likes

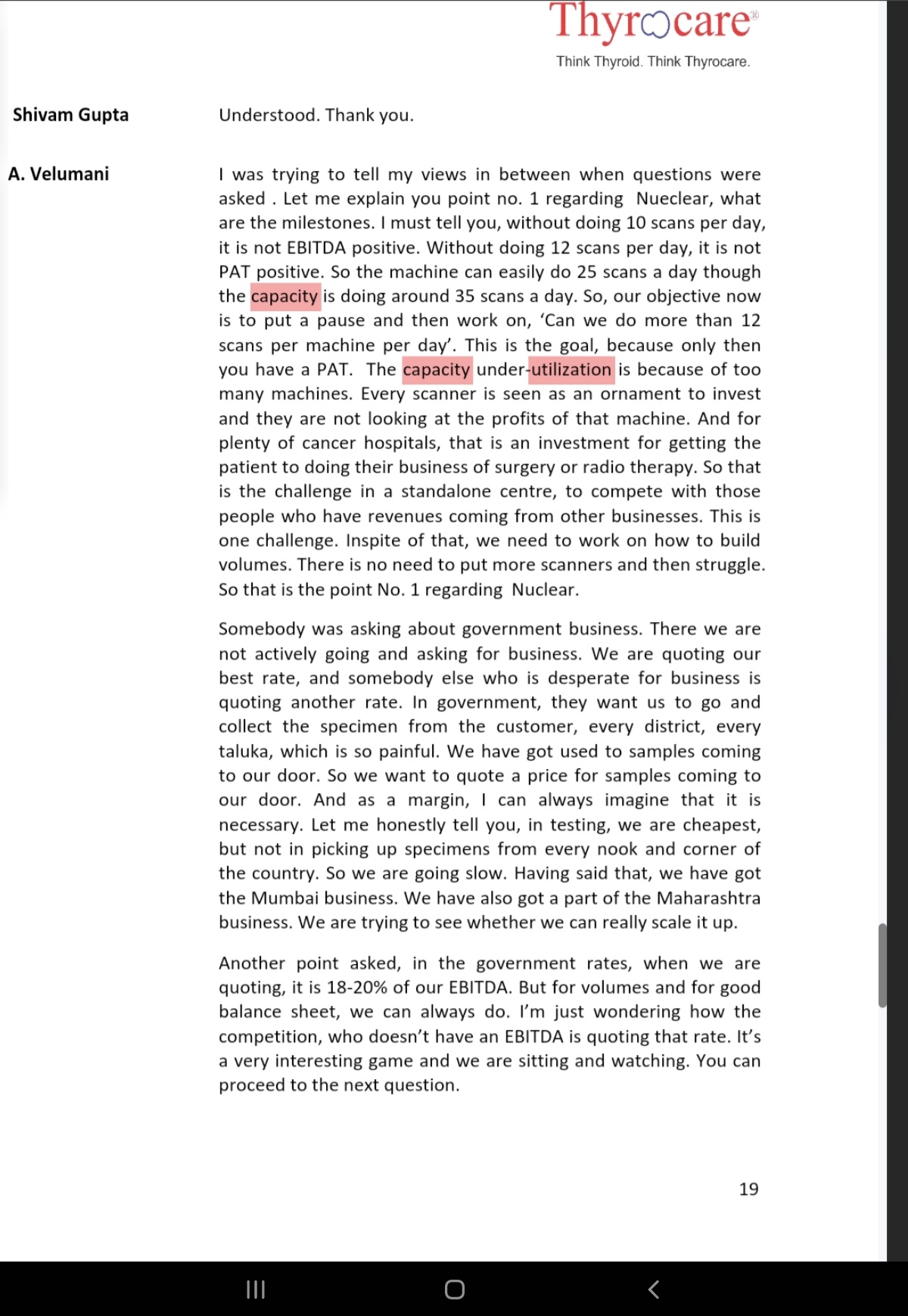

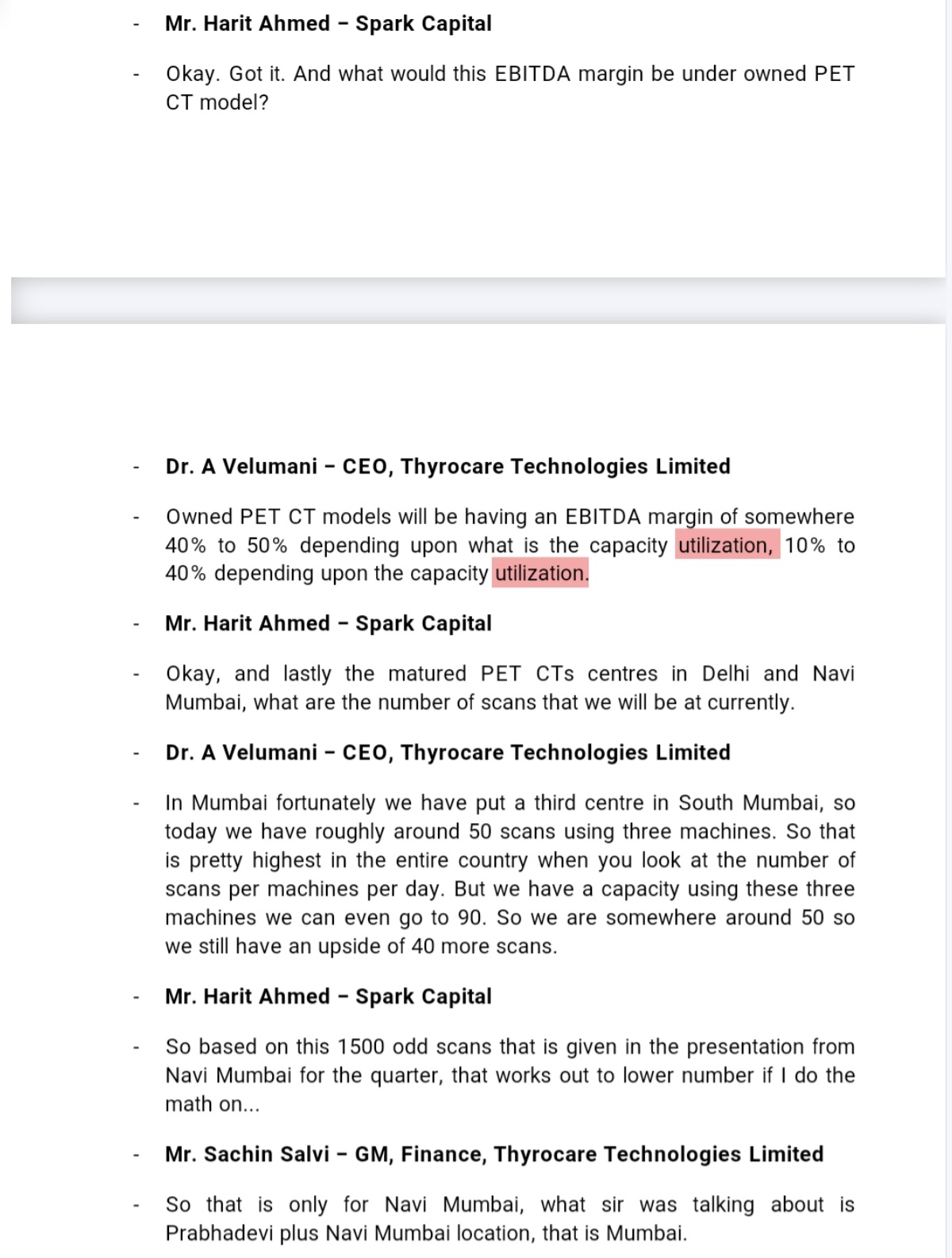

- Capacities utilization - peer view - Dr Velumani( Throcare) has shared some good insights on Radiology capacity utilization model, Govt business uniqueness( and admitting lower EBDITA for their way of working)

-

Another observation from Velumani response in above on Govt business being low margins and model challenges is equally imp to appreciate Krsnaa model success

-

Capacity utilization in Radiology seems to be low as model itself, and still possible to do healthy margins- Thyrocare view here

-

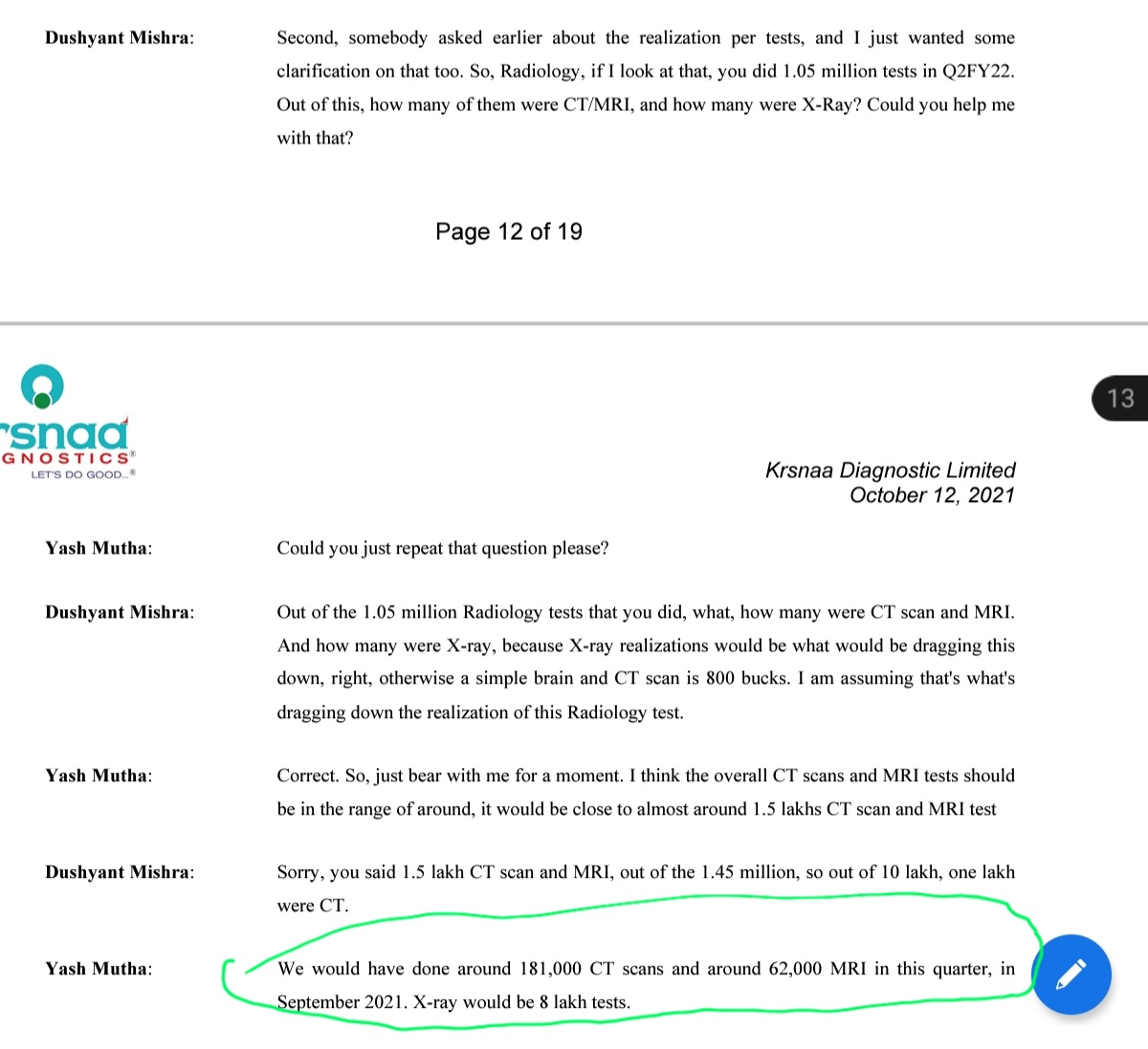

Lest see if Krishna used capacities alright - in Q2 22 Krisnaa had 65 CT machines and they did total 181000 CT scans in 90 days, I.e. average 2000 CT scans per day , 30 Scans per CT machine per day = now compare that to Thyrocare commentary of peak 90 scan capacity by 3 scanners. Krsnaa seem to have got execution right as those who follow Thyrocare, their Radiology business was considered a mis allocation due to losses pre corona

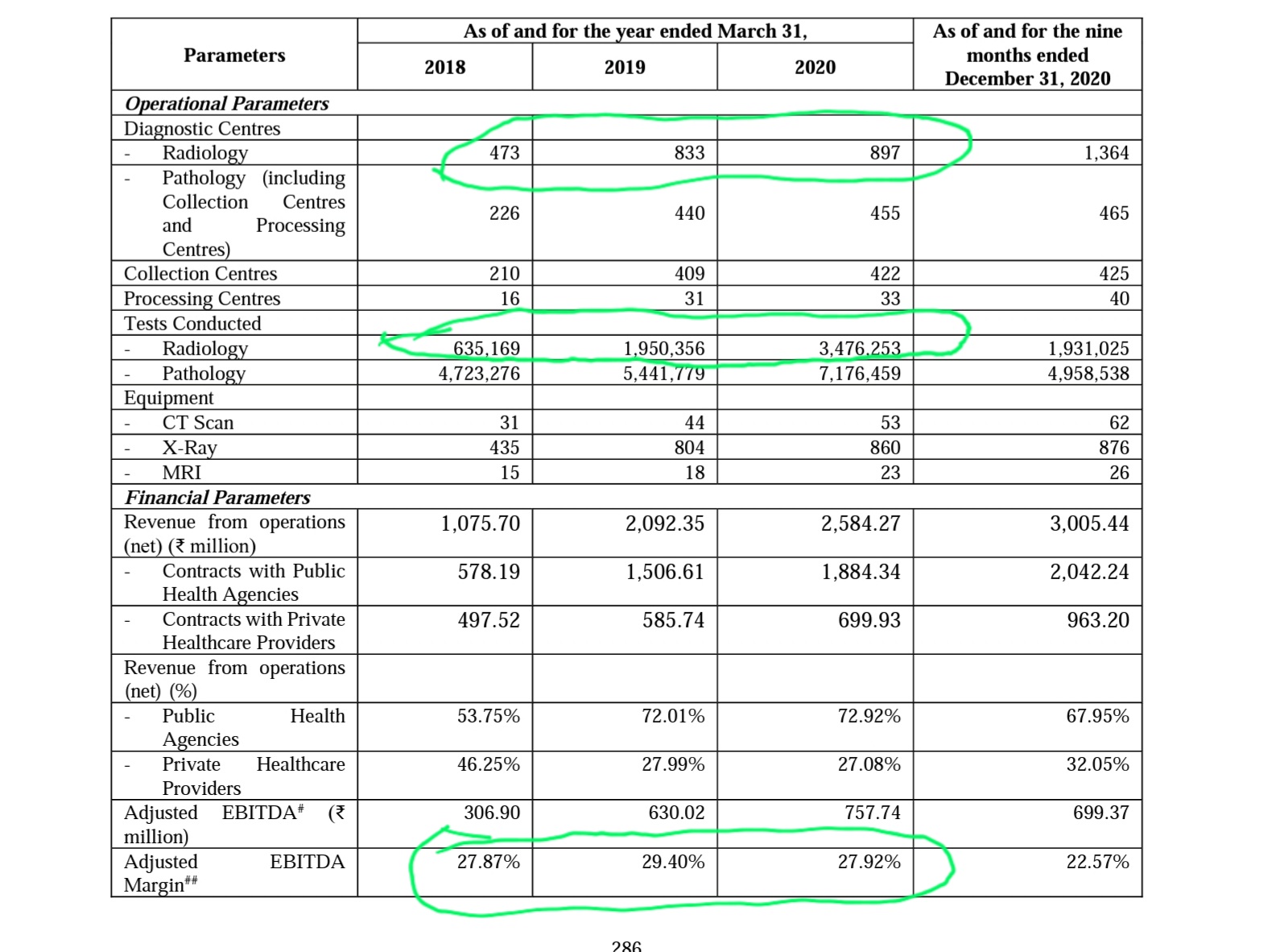

Krsnaa historical performance Capex vs Margins - Capacity utilization - Test realization vs EBDITA

-

Now let’s see their growth trajectory pre corona and how it impacted margins, remember key growth focus is Radiology as shown

-

2018 to 2020 - near 2X capacities in Radiology ( centers, equipment) and still margins were 28% vicinity - magic lies in no of tests and utilization **

-

Let’s revalidate if current Equipment base utilization and FY 2020 are comparable

3.5M Radiology tests in FY 20, 4.2M Radiology tests ( Q2 22 annualized ) - Given similar capacity increase( e.g. FY 22 - 53 CT & 23 MRI - 65 CT & 30 MRI now)

- Let’s do another validation on capacities utilization vs theoretical through put possible

CT scan they are doing 181000 in Q2 on 65 CTs = 30 scan( against benchmark of 100)

MRI scan they are doing 62000 in Q2 on 30 MRIs = 23 scans( against benchmark of 50)

Significant upside of operating leverage, also considering the Pune central model making scale in terms of Radiologist non linear.

-

Blended realization and co relationship with EBDITA - Let’s also see blended realization trend in FY 18, 19 ,20 was respectively 200, 280, 250. Same in Q3 22 is 230. For these periods EBDITA is 27.9, 29.4, 27.9 and 30%+ currently - there is certain degree of range consistency - irrespective of growth capex.

-

How to see if current round of expansion will/will not affect margins - by Q4 22 from IPO proceeds they are adding 29 CT & 8 MRIs - thus approx 40% and 25% respectively capacity increase - we know that they did 181000 CT & 62000 MRI in Q3 at current capacities.

Key monitorable will be corresponding growth in tests with some lag, and short term quantum of EBDITA in ramp up phase - in past margins in growth spikes have been stable at annualized basis

17 Likes

True there capacity utilisation is low but does it matter? ,when you don’t have to pay rent ,the fixed cost are next to none ,each and every bid win leads to reach to more areas more revenues while you don’t loose out much as investment size is not that high.

one thing i am really concerned about is what moat does the company have ,what if in future a large player finds this lucrative and outbid them and they can’t win more tenders or they have reduce margins to sustain the competitive edge.

6 Likes

If you read the concalls you will find many reasons why this is unlikely. Being large is not the only requirement. There are many reasons krsnaa is able to bid lowest :

- Centralized radiologist pool + per test payment to radiologist together ensure that the utilisation of radiology machines is best in class. Many stand alones + non centralized can’t run the lab if radiologist is out sick. Krsnaa can.

- The actual reason others are unable to compete on govt contracts is because their playground has been the tier 1 cities. Their cost structures are elevated due to that. Even in paints industry you can see asian paints totally dominate in tier 1. But in tier 2/4 they were unable to compete with indigo paints. Why? Because a player who emerges from the hinterlands has processes & cost structures optimised for operating in hinterlands. The essense of strategy as per portar is not to be “the best” it is to have a differentiated unique value proposition. Imagine if Dr lal does a ppp and offers a 50% discount to own center in government hospital. Then wouldn’t their customer prefer to do the test in government hospital?? This is primary reason that even from brand pov they cannot afford to be perceived to be lowest cost. Their entire brand is substitution for government infra. Krsnaa strategy is to empower government institutions by becoming their backend.

21 Likes

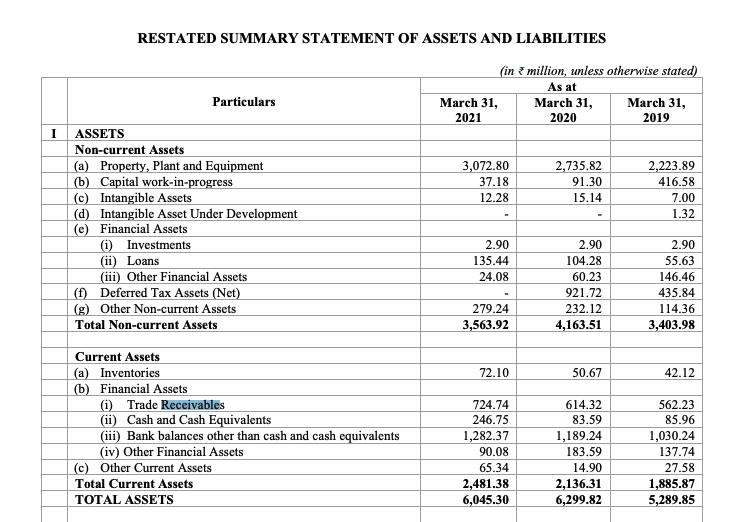

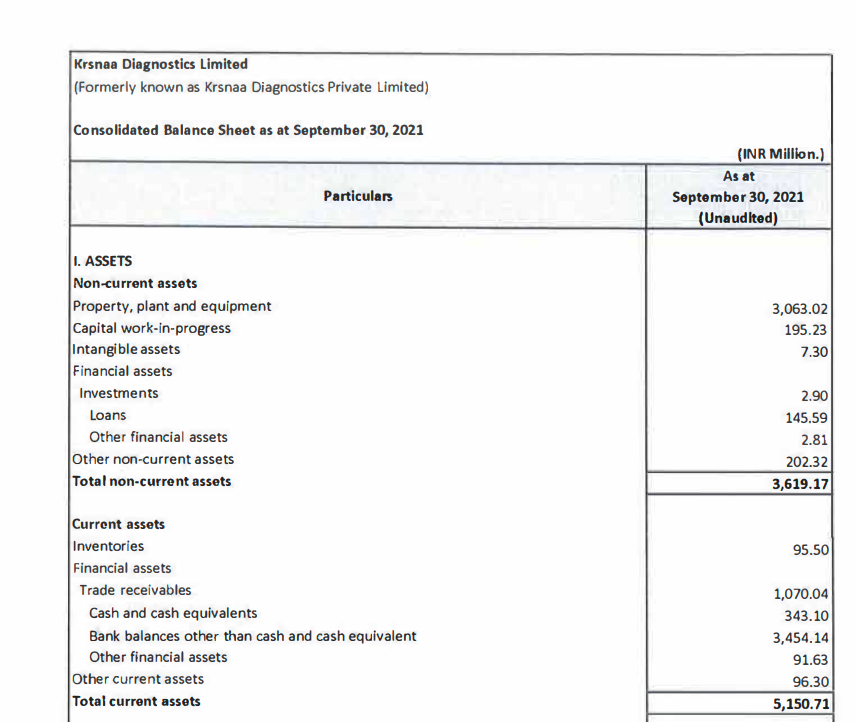

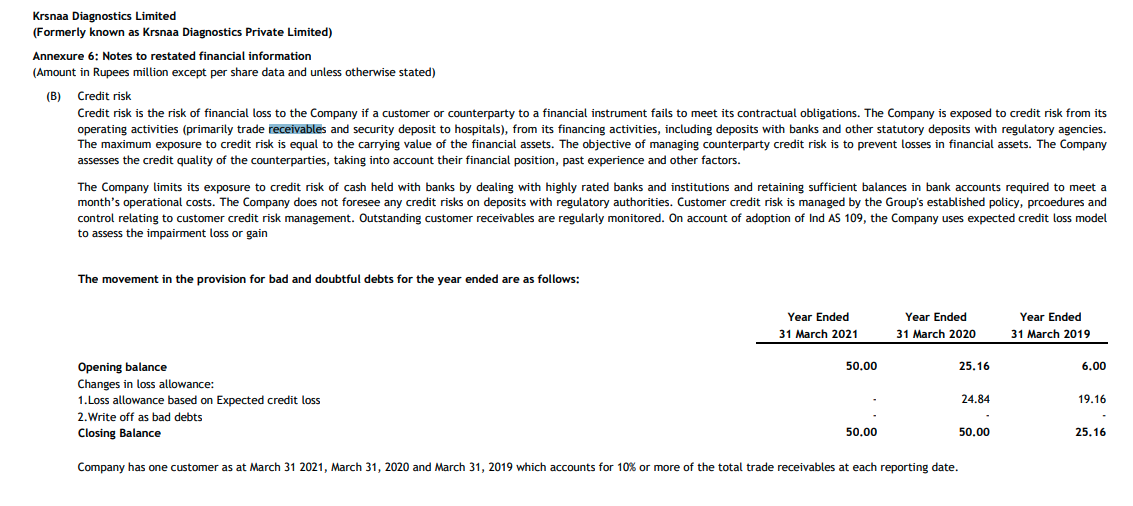

Let us analyse some more data from their DRHP this time around receivables.

Receivables from last 3 years.

Receivables in latest Sep-21 balance sheet:

While they have handled receivables rather well between 2019 & 2021. Going from 56cr to 72 cr while revenue base scaled from 209 cr to 396 cr. Receivables as a % of scales scaled down from 26.7% in FY19 to 18% in FY21.

However, situation has deteriorated back to FY19 levels in Sep-21 Q. 107 cr receivables for TTM sales of around 450 cr. Works out to around 23.6% of sales being stuck in receivables.

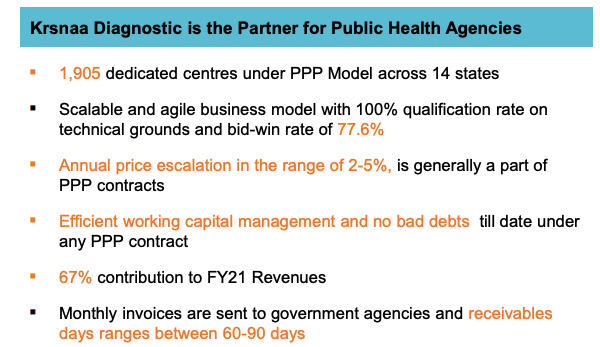

This works out to receivable days of around 86. THis is average over entire business. They claim in preso to have receivable days of 60-90 for PPP:

However, the data does not back this up. Average for entire business itself is around 86 days. private is most likely better in receivables than government. It would not be unreasonable to conclude that PPP biz receivables are > 90 days.

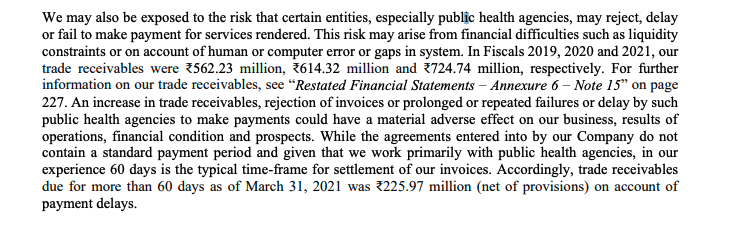

Here is another para from DRHP on risk wrt receivables:

The receivables > 60 days was around 31% of the receivables. I would be very interested in figure out same number for > 90 days & > 180 days receivables & how this deteriorated in sep-21 balance sheet & how this evolves in mar-21 balance sheet. I am surprised we did not see enough probing around receivable deterioration in Q2 Q3 concall.

One good thing is that they havent written off any receivables at least between mar-19 & mar-21. Should ask management whether they have in FY22 better know now rather than when annual report comes in Jun-22.

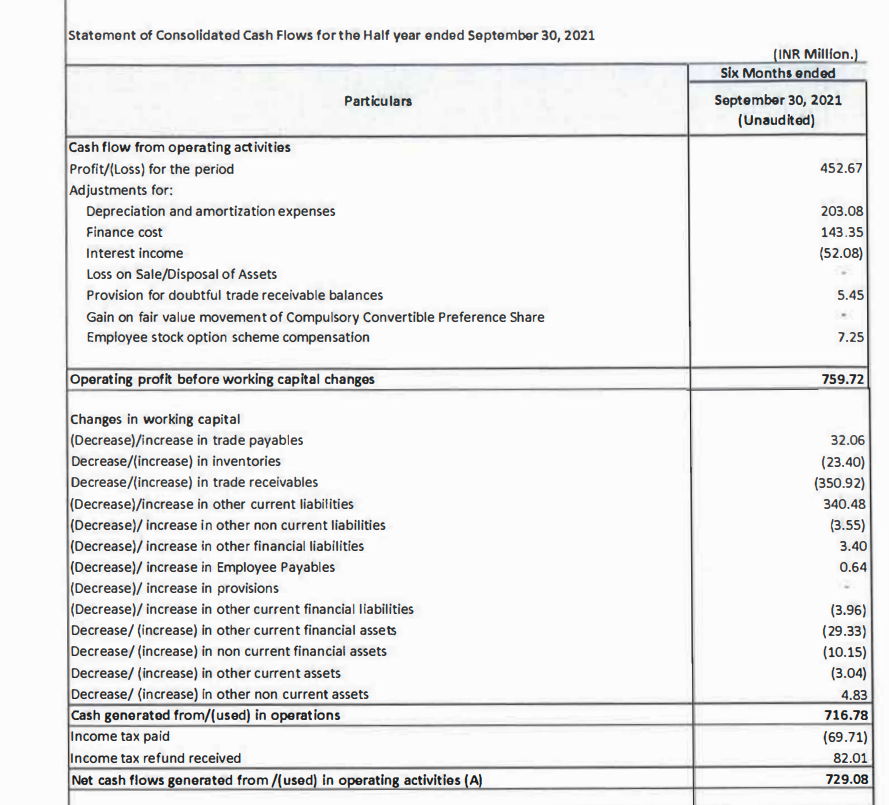

One interesting thing is that this deterioration of receivables HAS NOT impacted cashflows yet. Why?

Their “Other current liabilities” has also gone up by 35cr or so which has totally offset the deterioration in receivables. Note that the payables has not gone up that much (only 3 cr). So i would also want to dig deeper into this “other current liabilities”

And their “other current liabilities” have always been fairly low at around 3cr or lower earlier. For this to blow up by almost same amount as receivables going up is definitely extremely convenient (not alleging any wrong doing here, only pointing out the coincidence/facts).

If you go into the breakup of the other current liabilities in DRHP you see that these do seem to be somewhat similar to payables.

- statutory dues payables

- advances from customer

- deferred revenue

i dont think #1 would go up since revenue base has not exploded.

I dont think #2 would go up coz they are having difficulties collecting billed revenues. Advances from customers going up by 30cr is somewhat unreasonable imo.

I dont think they have deferred revenue because they recognize revenue at the time of their test. that is their revenue recognition policy. So, how did other current liabilities go up almost the right amount to compensate the deterioration in receivables? It remains a mystery to, me, but definitely worth solving.

Possible solutions:

- balance sheet/p&l/cash flow statement jugglery that i dont understand

- Advances from punjab government contracts. Is that how these tenders work? I dont think so

- Some new line item coming in other current liabilities which I have not anticipated.

Definitely will ask in next concall if we cant figure out before then.

Disc: Have a small position, understanding the company.

25 Likes

Sorry but my question is on a slightly different aspect here.

How do you perceive the competition coming up from from private players (Like the photo of lupin diagnostic going around). When i say competition, i mean to say for the whole diagnostic industry.

I see competition as good, if it brings growth from new customers (i.e. Brings more people in the basket)

The shift from private to branded diagnostic is happening for sure (Personal Experience), but i am not sure about the growth prospects giving current valuations are still not cheap.

1 Like

Hey, sorry I’m very new to investing. But how did you find out that PE value in screener.in is wrong. I have checked other websites too but they have mentioned the same number. Could you explain how is the adjusted PE is around 100?

Thank you

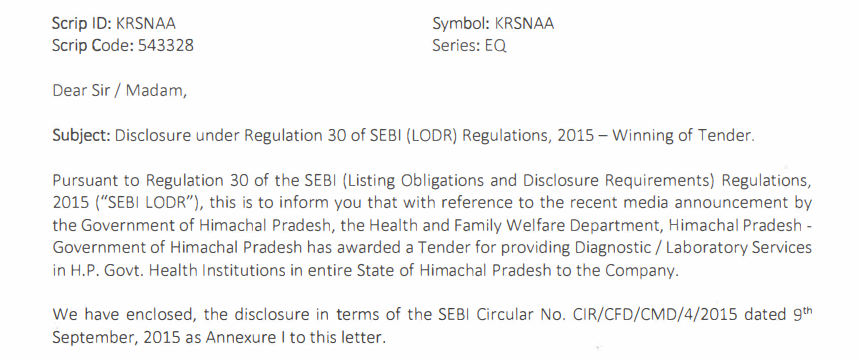

Sharing some reading I’ve done on recent news.

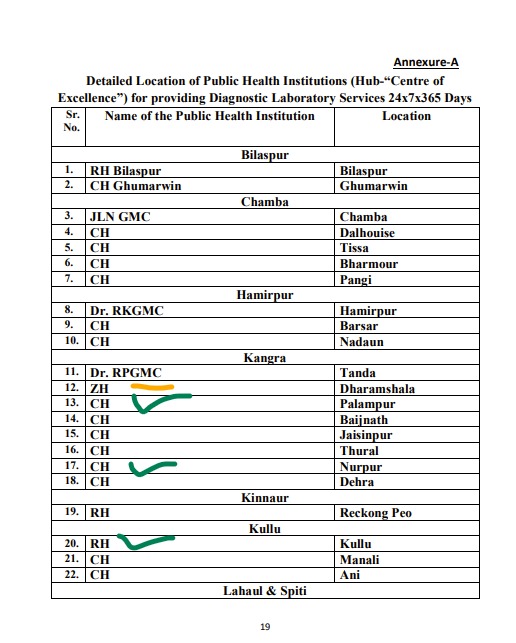

Krsnaa won a tender in Himachal Pradesh:

Notice the wording of the release, it’s for diagnostic/laboratory services, with no mention of radiology. I found this tender from a few years ago that I believe is the same one as the wording and tenure matches with the exchange filing:

Details:

- Contract has been won for 5 years.

- Tender requires setting up pathology clinics in 50+ government hospitals based on hub and spoke.

- There are no price hikes in this specific contract.

- Contract stipulates receivables will be settled monthly.

- Details of path works are mentioned in the tender.

If this is the same tender mentioned in the exchange filing, it becomes very interesting as Krsnaa already has a presence in some of these hospitals for radiology work.

Krsnaa has a radiology center set up in the centers marked green. Yellow indicates that they have a presence in the same district, but at a different hospital. (Edit - they’ve also just inaugurated a center at Bilaspur, #1 on this list.)

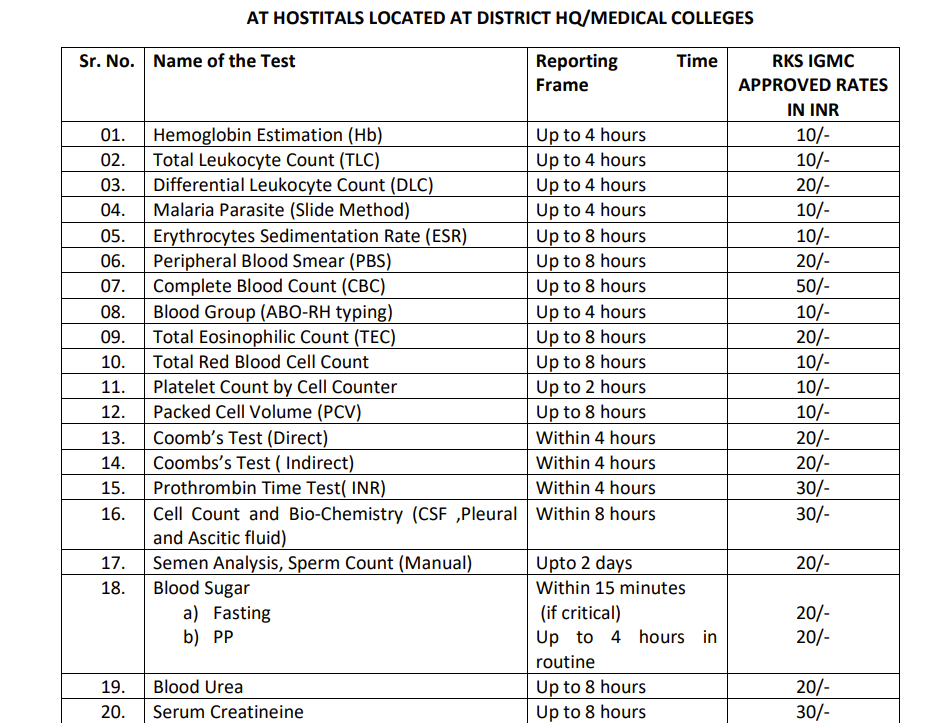

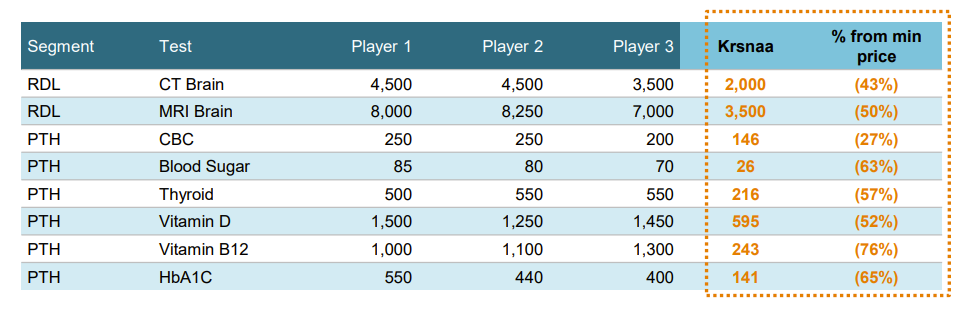

Now, radiology tests have lower volume but high realisation per test, while pathology tests have high volumes and low realisation. Here are the benchmarked prices that Krsnaa had to discount in order to win the tender:

These prices are lower than what Krsnaa has offered in Pune:

Note that the price for a CBC in Krsnaa’s presentation is Rs. 146 (Pune), while the IGMC benchmark in Himachal Pradesh is Rs. 50. IGMC benchmark price for a CT scan is 1500, so one would need roughly 30 CBC tests to offer the same revenue as a CT scan, before considering operating costs. I also believe that path works are bundled together, and often patients don’t undergo one singular test, but 2-3 to make a diagnosis.

Thanks to @Dev_S and @sahil_vi for adding so much value to this thread and more exposition on thesis/anti-thesis pointers.

Screener’s PE calculations for Krsnaa are currently based on FY21 numbers, not trailing twelve months. Note how there was a huge loss in FY20 followed by a significant entry in the other income for FY21. These were due to a one off (two off?) issue compulsory convertible preference shares, and won’t be seen again.

Due to the extra 265 Cr. of income in FY21, the PE looks like it’s in single digits. In reality, if we ignore the other income entry, we’ll have a realistic picture of what we’re paying. FY21 without the other income would have a PAT of ~20 Cr. Against a market cap of 1868, this is an FY21 adjusted PE of 93.4

Now, Q3FY22’s PAT was 17 Cr. This is a steady state quarter since we don’t have covid revenues, and we don’t have interest payments. Annualising this through FY23 gives us an FY23E PAT of 68 Cr., against a market cap of 1868 Cr., or a PE of 27.5. If we think Q4 and Q1 will offer better realisations than Q3FY22, (or in other words management delivers 600-650 Cr. topline) PAT can be significantly higher than 68 Cr. in FY23…

PS: I believe they’ll do around 68 Cr. of PAT in FY22 itself, so FY23 should have 68 Cr. as a base, and we can consider FY22E PE to be 27.5…

20 Likes

Did some scuttlebutt around the contract procedures. Talked to 3 different doctors in 3 different states about how it works in their states. The feedback i received was not specific to krsnaa but rather about how tendering works in general in government hospitals.

The feedback received was quite negative for 2 of the states. The entire process is driven by comissions & payoffs. Politician involvement.

Feedback i received from 1 state was positive with most of the tendering happening above the table fashion.

All in all, at best (if krsnaa does not indulge in such payoffs) it reduces the TAM to states where the process is mostly above the table/board. At worst it puts cashflows & revenue streams at risk of political & bureaucratic interventions. I will put this on on the back burner until i am able to gather even deeper scuttlebutt & understand as clearly as possible what I am dealing with. Able to find equally good “simpler” opportunities.

In short what one of the doctors told me is : “avoid being in business with the government”. And as they say discretion is the better part of valor.

20 Likes

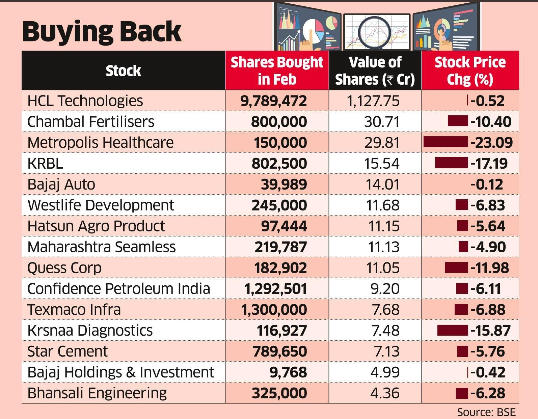

Again Promoter is buying

6 Likes

COO hiring, Ex Lalpath/metropolis/HUL - interesting as he is not from Govt business background. Also has a New biz dev/growth exp. Imp as mgmt bandwidth will be limited with high growth and hiring professionals to run ops is a good sign.

7 Likes

Another feedback from pune .

Health activists thumb down PMC’s PPP models in public health care services - Hindustan Times

6 Likes