The Company is not drowning,It is cheapest on Net Worth basis in its history. The same stocks are held by PPFAS mutual fund and nobody is complaining. The only bad remark on this company is the CBI investigation which seems to stem out of some personal issue with the promoter rather than actual finanial wrongdoing. Disc- Biased

8 Likes

A good analysis of KRBL and interview with the CFO - https://www.youtube.com/watch?v=n2NFyXXXg4c

2 Likes

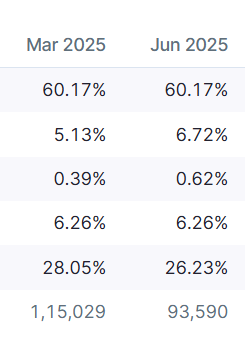

Interesting change in the June 2025, shareholding pattern. FIIs have added almost 1.75% sold by the retail investors. Infact almost 20k people have given up on the stock making it owned by less than 100k people.

12 Likes

They are entering some real estate value unlocking.

How much was the land worth they said.

Was it 7000 crores?

1 Like

Concall excerpt:

Q: My first question is I think in the results release you also talked about your foray into real estate. So if you could just kindly tell us what are the plants there?

A: As far as real estate is concerned, let me tell you, we have around 150 acre land in our Ghaziabad plant, which is valued today around 4,000 crore rupees. And we intend to shift this plant about 50 or 80 km away from Ghaziabad, somewhere near Meerut, And that land, by the time we shift to Meerut, by that time it will become about 7,500 crores. We want to monetize on that land and shift our plant to Meerut side. That is all.

Q: So what are the timelines here?

A: It might take two years, two and a half years.

It seems they value land at 4,000 crores right now, which they expect it to be values at 7,500 when they start to develop. Apparently they are going to develop with some minor developer partner.

10 Likes

This needs clarification

Land appreciation from current value of 4000 to 7500 in 2.5 years !?

That’s a CAGR of 29%.

2 Likes

As per the management, the land is presently valued at 4k. They intend to develop it with a partner developer and fetch gross 7.5K from the sale of the township.

3 Likes

How Punjab floods going to affect the overall Basmati production scenario in india?

I expect lower than expected production of Basmati rice in india which can lead to increase cost of Basmati. Anything other than this is not coming in my mind. All counter views are welcomed.

1 Like

Prima facie, assuming lower basmati yields due to floods on India and other side, you would assume the prices for next year should be high.

Assuming KRBL is aging its own inventory ( as per my understanding KRBL buys paddy ages and then sells aged rice) but I am not sure what percentage of the revenue are from aged inventory, at least KRBL shouldn’t have problem with volume, and in the best case benefits from price bump, if shortage of Basmati crop also gives a bump to aged rice. I would assume worst case business as usual, best case may be above trend margins.

All these are conjectures at this point though.

2 Likes

After following this industry for 5 years, I think it goes on like this -

- If basmati crop is increased, then paddy prices decrease, leading to higher gross margins for KRBL (As was the case this year)

- And vice-verse, If crop is lower (as might be because of floods), then paddy prices become higher, and thus gross margins are reduced.

As KRBL is mostly in branded space, They can’t adjust prices too much (both on the upside or downside), so movement in basmati rice price (If rice price goes higher due to lower crops in both India and Pakistan) will only be captured in the bulk exports segment. Even here, the delta between rice and paddy price movements will decide if its positive or negative for KRBL

About ageing rice-

From what i have observed in operational performance or krbl in 5 years, ageing rice doesn’t much matter in terms of margins. It’s mostly direct correlation of paddy prices movement.

(Learned this the hard way, when two years ago paddy prices rose, and management was confident of maintaining margins, but it didn’t happen)

3 Likes

They did mention in the recent con call , Q1 FY26 ended with lower inventory because of volatile prices and cautious stocking. But from October 2025, if new paddy prices open slightly lower, they intend to build up large inventory.

So if the flooding influences the paddy price on higher side , they preferred to keep limited stock rather than build large inventory

Independent director resigned citing corporate governance issues

5 Likes

From Annual Report:

The AGM Notice contains a resolution (Item No. 7) to alter the Memorandum of Association, adding “real-estate development and allied activities” to the Object Clause.[1] The notice states that this was approved by the Board on August 07, 2025.

The independent director’s resignation letter is also dated August 07, 2025. The company’s action (altering the MOA for real estate) is the exact action the director is complaining about, and the director’s departure is timed to coincide with this decision. This is a very strong signal that the director’s professional judgment on this matter was dismissed by the board, leading to their immediate resignation.

4 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive/6336da2e-eb42-4fa9-8753-2e0af471c649.pdf

Is this just optics, to do damage control? or Genuine efforts to improve corporate governance?

2 Likes

Recent developments, notably the resignation of the independent director citing “suppressed dissent, questionable write-offs, and withheld information” the decision to bring in a third-party audit seems warranted but also signals deeper issues. Over the next 30 days, the company’s actions, especially what comes out of the review, amendments to its MoA (real-estate investment plans), changes in board minutes and disclosures — need close monitoring.

The risk is that KRBL is moving away from being a pure FMCG / rice business toward more speculative or risk-laden sectors. For investors who bought in under the assumption of a governance-sound, focused business, these shifts may undermine expectations and expose one to unexpected risks. Expecting more downside moves connecting all the dots and news we have already in the open.

Discl: Invested and Biased. No investment actions in last 30 days.

1 Like

a0d29c3c-d40e-4e71-bf61-b9a65ad400bf.pdf (388.0 KB)

KRBL has successfully bid for PACL properties in Sonipat. It seems they were well prepared to venture into realestate. The belt in which the said land is situated has seen tremendous progress over last decade and KRBL has done a very good work in identifying the fit in the current business. They could shift their legacy plants from erstwhile places to this new land and make commercial devlopments at old places. If you check on youtube they are already willing to lease out office space at their current Corporate office.

Youtube link:https://www.youtube.com/watch?v=-X8DYWzFrgo

All said and done,the resignation of Independent director with a rather inflamatory letter has hurt the reputaion of the company very badly. It seems to be a hit job rather than actual events. I am surprised that people believe an ex-govt babu but think of all businessmen as thieves(the drop of 40% in stock price would have hurt them the most). After the ED fiasco they were treading very carefully but this has really finished any hope for stock price recovery for them. Bad loans and write-offs are part of every business and promoter’s don’t gain much from that. It is better to have a good valuation rather than siphoning off few rupees.

5 Likes

KRBL is interesting:

The existing thread already covers issues related to its Director and an understanding of the business model.

Recent news around KRBL:

- Unlocking value of land assets

- A Director resigned with some allegations against the management

- Acquiring real estate

Company numbers show:

- Approximately 5,000 Cr in reserves

- Approximately 8,000 Cr Market Cap

- Generating 500 Cr profit year over year

- Trading at 14 PE

- Plus, value unlocking through land assets

It has not touched its 2017 high, but what baffles me is that while the overall market is expensive, KRBL has become cheaper over the years, and it is a consumer-facing company.

However, no Mutual Fund is interested in taking any position. They might take a 1-2% position in some other counters as a bet, but they are not touching KRBL at all.

6 Likes

We are posting this analysis as part of the discussion on KRBL- The King of Basmati rice, solely for knowledge and learning purposes. This is not an investment suggestion; it is for discussion only.

KRBL Limited, with 130+ years of history, is India’s first vertically integrated rice company and a world leader in basmati rice. Its India Gate brand boasts robust domestic leadership and distribution in 90+ nations. Spanning the whole value chain from seed to marketing, KRBL applies cutting-edge technology, extensive product coverage, and robust brand equity to drive growth and pursue new markets and categories.

In Q1 FY26, KRBL Limited posted a solid set of numbers, both indicative of financial robustness and operational resilience. The company’s total income stood at ₹1,617 crore, up 32% YoY, spearheaded by strong export growth of 98% YoY at ₹489 crore. The domestic business was also healthy at a growth of 15% YoY to ₹1,063 crore. Margins improved significantly, with EBITDA growing 62% YoY at ₹225 crore, representing a margin of 13.9%, and PAT growing 74% YoY at ₹151 crore. The balance sheet also improved with significant deterioration in net cash position to -₹1,281 crore and inventory reduction to ₹2,953 crore. Market leadership was maintained with India Gate holding No. 1 rank for both General Trade (37.9%) and Modern Trade (38.6%).

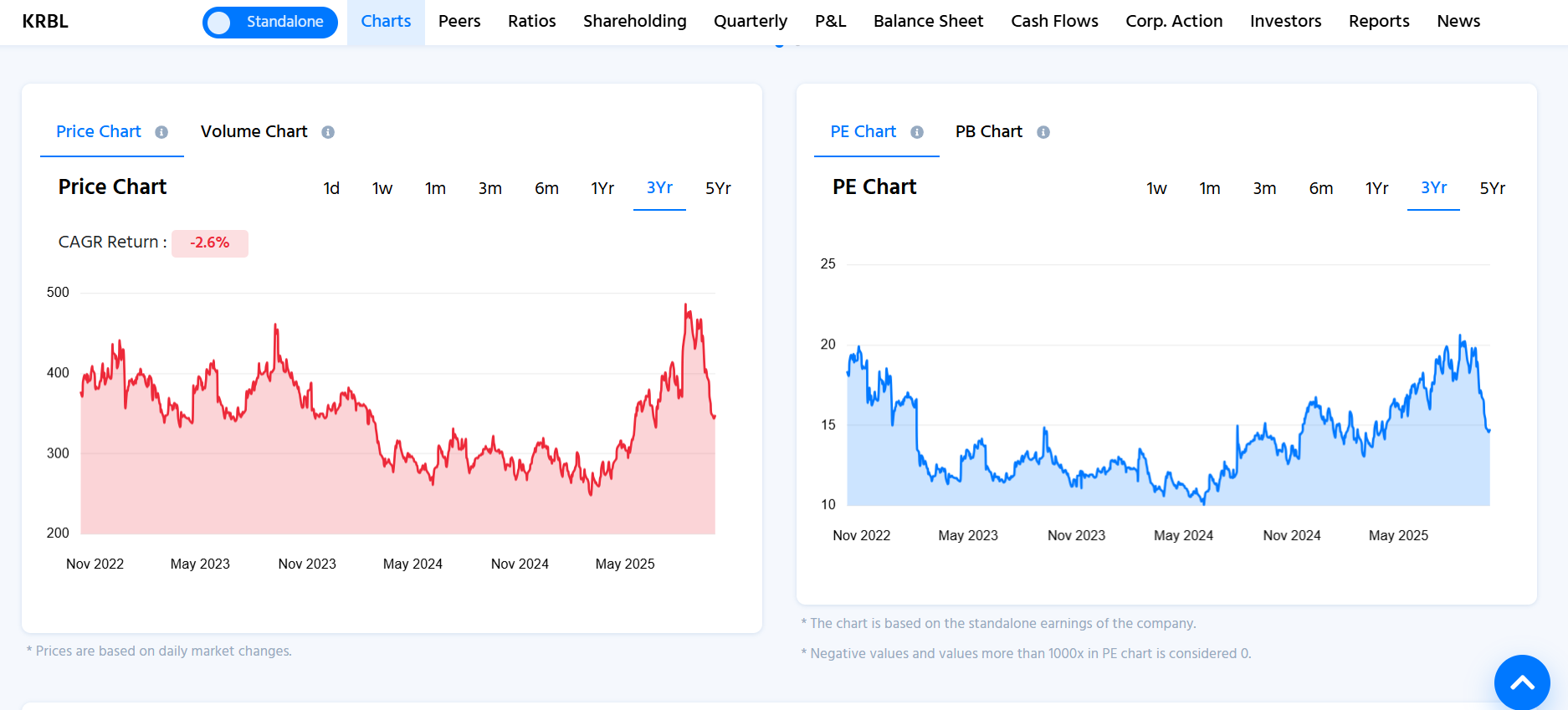

KRBL Ltd. returns present a sharp divergence over periods. The stock has risen vigorously in the past year with a CAGR of 18.8%, depicting good momentum. But looking at three-year averages, the CAGR is only 0.2%, indicating that profits have been virtually flat due to volatility. Over five years, the CAGR is 4.9%, which means only moderate wealth creation despite violent price fluctuations over the period.

Valuations too witness a change, with the P/E decreasing to approximately 10x in 2023 before re-rating to close to 20x by mid-2025. The stock has picked up speed recently, but long-term performance is still mediocre.

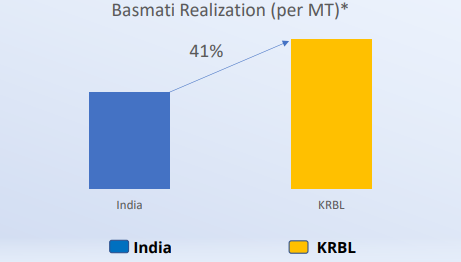

KRBL’s pricing strength in the world basmati market, wherein its realisation per metric tonne through exports is 41% more than India’s average. Such premium is high and indicates the popularity of its market leader brand India Gate and the success of the company in differentiating on the back of its better product quality, brand reputation, and consistent premium positioning, thus allowing KRBL to charge better margins than peers.

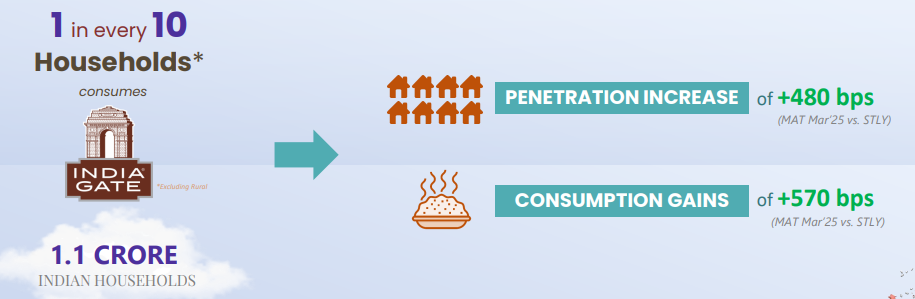

India Gate has consolidated its position in Indian homes. Now 1 out of 10 urban homes (approximately 1.1 crore families) uses India Gate rice. In the last year (MAT Mar '25 vs. previous year), the brand recorded a penetration gain of +480 bps, i.e., more households began purchasing it, and consumption gains of +570 bps, i.e., increased purchase frequency or quantity among the existing consumers. Cumulatively, both represent broader adoption and greater consumption, further establishing India Gate’s robust market presence.

On the strategies side, KRBL continues to build its brand by investing in high-impact campaigns such as those with Amitabh Bachchan with a reach of more than 65% pan-India. KRBL has also ventured into multi-source edible oils under the India Gate UPLIFE brand, which has already registered a market share of approximately 5% in major modern trade platforms. In addition, KRBL is also approaching shareholders for approval to modify its Memorandum of Association in order to facilitate land monetisation and real estate business, which management considers as a possible vehicle to unlock shareholder value.

Eager to hear fellow members’ opinions on KRBL’s performance and future prospects.

-

With exports up 98% YoY in Q1 FY26, will international markets remain the main growth driver, or is domestic penetration more critical?

-

India Gate’s pricing premium is 41% above the national average. How sustainable is this in the long term amid competition?

-

KRBL is diversifying into edible oils and considering land monetisation. Could these initiatives meaningfully boost revenue and shareholder value?

-

Despite strong one-year returns, the three-year CAGR is almost flat. What factors could explain this volatility in performance?

7 Likes

Corporate governance issues. Please go through the thread for more information.

I tend to agree. Company was taking the right steps to regain market share over the last few years. However, recent developments unlikely to be well-received by investors seeking a pure-play FMCG opportunity. I have fully exited this counter for now and am monitoring the developments. Given the excellent business fundamentals and brand recall, it’s worth keeping a close watch for a better window to re-enter the position.

Disclaimer: On Watchlist. Not a buy/sell recommendation. Consult a qualified advisor before any investment decisions.

3 Likes