In your Inventory Days Outstanding, your numerator is your present inventory but your denominator COGS is of 1.5-2 years old. Inventory value has been steadily moving up, but COGS will be volatile given lower procurement cost in some years compared to higher procurement cost in other years. Hence the output of this ratio is not very helpful to me if I look at it alone.

I suggest you to not look at inventory alone. Dive little deeper. Track volume and cost of inventory that is being procured to get complete picture. 1000kg of inventory procured at Rs. 10 makes Rs. 10,000 worth of inventory. But 769kg procured at Rs. 13 also makes inventory worth Rs. 10,000. They have always procured more volume of paddy at lower prices and have been very aggressive when prices are lower.

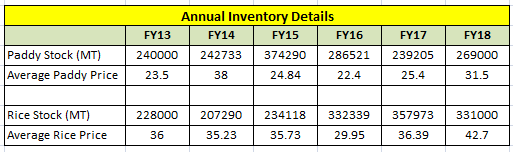

From below screenshot you can see that they aggressively procured paddy in FY15 and rice in FY16 when prices were lower. So my point is tracking only change in inventory without looking at ongoing paddy prices, volume procured, etc is not of much use (at least to me). Looking at everything together should give you a better view.

Same as above for inventory turnover. If they were not making necessary sale to efficiently manage their inventory, they would not have funded 1008cr worth of WC through internal accruals in last 8 years. Their inventory levels have gone up 4x but Net Debt level has gone up only 2x. Look at slide #12 of my deck to better get what I am trying to say.

At 7000cr worth of inventory in my view they would do top-line of ~14000cr in bad year and ~18000cr in a good year. This is longgggg-way away for now.

I don’t look at FCF for “equity owner” for valuation but I look at “owner earnings”. For example - if KRBL is generating 500cr worth of OCF and 400cr goes towards funding inventory (assuming zero CAPEX), your FCF is 100cr. So you will value the business based of 100cr. But your business has made 500cr and out of which 400cr is ploughed back, earning good ROIC, which is going to increase your business’ intrinsic value. So why should I use only 100cr as my FCF? I am going to value the business based on it’s “owner earnings”. If tomorrow, KRBL management is happy with the scale that they have reached or there is no incremental growth opportunity left, with current inventory levels KRBL on average will keep throwing 500cr cash at you annually. So why should we ignore 400cr worth of earnings for valuation purposes that is ploughed back for future growth. Another example - Tasty Bite Eatable has generated ~155cr worth of OCF in last 10 years and ~135cr of CAPEX. That leaves only 20cr of FCF in last 10 years. It has every year ploughed back money back in business for future growth leaving almost nothing as FCF. Look at the wealth that this business has generated and one would have not valued it properly if one only looked at FCF for valuation purposes.

My central point which I know you have read it before (from Mr. Buffett’s Owner Earnings concept) here is that its safe to treat incremental CAPEX and WC used to generate the growth in business as Owner Earnings/FCFE - as long as you understand the business, trust management, and you have good confidence in its future prospects. Cash spent on CAPEX and WC to grow the business is ultimately going to bring more cash which will be again deployed to grow the business and the cycle will continue forever until management sees growth prospect. It will be good if these investments are funded from internally generated funds or minimal debt. If funded full with debt, then one should be very cautious and skeptical. IMHO - one needs to treat this cash portion differently which is spent towards growth of the business.

One shouldn’t need cash in their hand from a business that is generating >25-30% ROIC. KRBL’s agri business is generating excellent ROIC. Let them plough back OCF to agri business and grow the intrinsic value of the business. Monitor their capital allocation. If they put money in activities which are not ROE accretive, one should pull out. Else, one should happily ride until captital allocation is appropriate and future growth story is in-tact.

Someone asked Buffett how does he value a business. Buffett replied that the value of a business is the present value of all CFs that it will generate from now until the eternity. Munger was in the same room and he tried to pull Buffett’s leg by saying that he has never seen Buffett do DCF. Buffett wittingly replied that there are some things that one should do only privately and DCF happens to be one of those things. ![]() This I heard in one of the CFA India webinars by Rajeev Thakkar and I believe this is a true story.

This I heard in one of the CFA India webinars by Rajeev Thakkar and I believe this is a true story.

So instead of doing DCF by using my assumptions, I try to do reverse DCF using today’s stock price to see what is that market is implying at current stock price. I highly recommend you to read Expectation Investing by Micheal Mauboussin to get a new valuation weapon.

Due to tax and ED issues overhang in last 1-1.5 years, KRBL stock price has been languishing such that I didn’t need to pull out my excel spreadsheet for it’s valuation. Just with simple back of envelope calculation, one could had figured out that one was not paying anything for growth for all this time, in my view. And with it dropping to 92 levels, it’s market cap was ~2200cr and it had ~2000cr worth of inventory in hand. One was getting the entire existing KRBL branded business for almost free and future growth also for free , even after resolving 2000cr tax issue.

Disc: invested and my views will be biased. I’ve added in last 2 weeks.