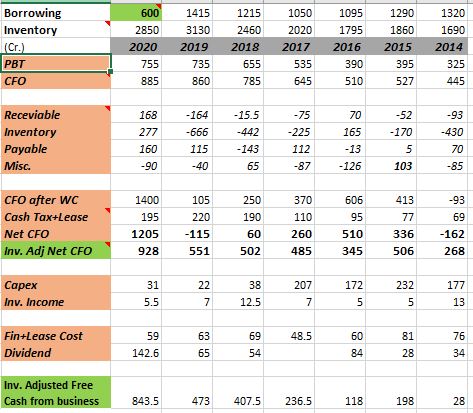

This is how the cash looks like for the past few years.

Let me know your thoughts, sometimes zooming out from quarter to quarter clutter helps.

Disc: Invested

Edited for slight mistake in copying the excel sheet.

This is how the cash looks like for the past few years.

Let me know your thoughts, sometimes zooming out from quarter to quarter clutter helps.

Disc: Invested

Edited for slight mistake in copying the excel sheet.

Any insights on the management bandwidth and succession ? is it a one man show ? how competent is the next gen ?

i request you to look at the investor presentation… they have the succession plan in the final slides.

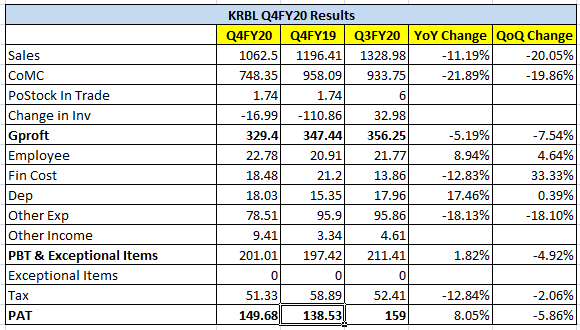

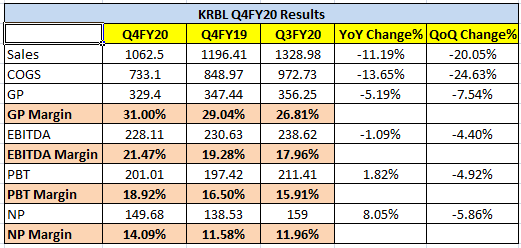

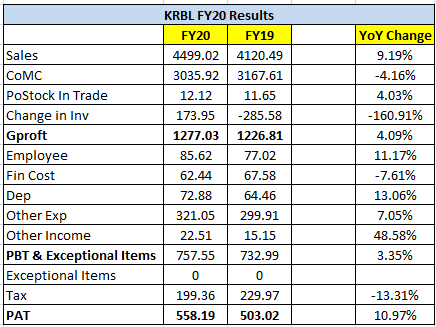

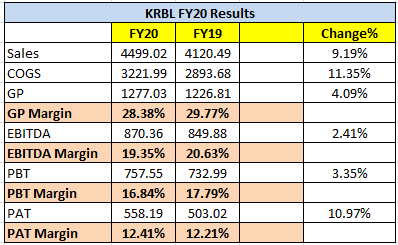

Q4FY20 results give enough indication that KRBL as a business has tremendous longevity. Even COVID-19 couldn’t break the momentum that KRBL’s business has been having for last many years. Management confirmed on the con-call that they have 5 months worth export orders in-hand for next 3 months and it should keep them super busy. Goes onto show the resilience of the business. In a period where there will be significant de-growth in most businesses, KRBL’s management guided for 10% volume growth in FY21 which is quite outstanding. In my view, market is not giving enough terminal value to KRBL that it deserves. KRBL’s consistent results being in a commodity product business is quite remarkable.

Below please find my take on Q4FY20 results.

Earnings Con-call Notes:

EXPORTS

• Orders are very good. Order book is full. Couldn’t ship out orders due to issues at the port.

• Pre-covid port was able to load 5000MT per day, but now it has come down to 800-900MT per day. Now to load a 25,000MT vessel it takes 20-25 days which was taking 4-5 days earlier. There is long waiting period to fill the vessel. Labor at Kandla port was at 20% of precovid conditions

• For last 2.5 months (from 24th March) – there was labor shortage at various ports. Now most labor force has come back. Packing materials is available now without any issues. Next 3 months have orders equivalent of 5 months. Now things will come in strong momentum. Exports orders are better compared to last year.

• Basmati rice of more than 40k MT lying on Kandla port valued at 470-480cr. Most should ship out in June and some in July. By 30th June things should stabilize.

• Saudi and other ME countries age rice themselves. Generally they have stock of 1 year.

• US market share would be 10%. Do only branded business in the US.

• Except Iraq and Iran we don’t do private label anywhere else.

• Don’t expect ban of importing rice from Iran this year due to Covid-19 issues.

DOMESTIC

GENERAL BUSINESS

Disc: invested with no transaction in last 60 days.

On valuations - If we take a 4-5 year view, Sales growing to 8k crore and profits doubling & ROE moving to 25%.

Can KRBL be valued at 20PE? if this happens KRBL can provide 4x kind of returns

In these 4 years:ED issues should be sorted

Tile companies are valued at 20PE, KRBL can get atleast get that.

If ROEs move up(30% kinds) with separate energy business that would be a bonus

Future lower interest rates should anyways move PEs slightly higher for all companies.

Any views?

Do you think the downfall in crude prices will have an impact on it’s exports of expensive quality to gulf countries and domestically , the people remaining away from restaurants and lavish marriages/gatherings not being there is also going to impact sales.

In my limited experience I have seen that once a company is caught in an legal issue like the one with KRBL, it’s return to name and fame becomes difficult.

Have you considered the above factors in your thought process?

Think about it, even in such an environment management is guiding 8-10% growth in topline.

Yes legal issue remains a risk, enough has been said about it already in this thread.

My only concern was inconsistency in promoter actions and commentary related to buying shares in open market in personal capacity. Earlier guidance of increasing stake has now been refused. Also not a satisfactory explanation for not buying shares during pledged sale issue in mar19.

KRBL has been an interesting developing story. I think that concerns related to promoters and management are overdone especially when compared against the valuations which the market is ascribing given:

a) 10+ year track record of excellent numbers in terms of RoE, Debt control and reduction, margins and most importantly in the stock price itself

b) nature of the business wherein the domestic branded revenues numbers are corroborated with impartial and creditable agencies such as Nielsen as well as in terms of reputation among the competitors (basis primary research) as well as fair visibility of products across channels.

c) strength shown in cash flows as exhibited in cash tax outgo, continuously increasing dividends and most importantly debt reduction through the years. Perhaps the best example of the same was set in FY20 itself wherein company generated a mind-boggling ~1000+cr of free cash flows and used it to pay down debt by ~1000 cr resulting in lowest ever debt to equity ratio along with paying decent dividend

d) some other soft factors which I found comforting is that way the company has never lost a single rupee in bad debt (as per consistent commentary of the management in concalls) as well as the way capex and aquisitions (where there is a lot of possibility of cash siphoning) have been kept at a very low levels.

Once the income tax case which was a major overhang on the stock price was also announced in company’s favour, still this stock which generated ~1000+ cr of free cash flows in FY20 was available at a paltry valuation of ~2500 odd cr few weeks back. I think it was a screaming buy at those unbelievable levels as the fall was caused more due to technical levels (one of the major shareholders’ stocks were sold by the brokers in the market indiscriminately for lack of margin) than any promoter related or fundamental reasons.

Even now while the stock is trading at 5000 odd crore market cap with almost zero debt and a trailing P/E of less than 10 times, I think it can be a attractive long term bet. But of course, this is not a HUL, so it requires active monitoring and smart position sizing given that the volatility in the stock price as well as any positive/negative news flow which can give multiple opportunities to buy and sell at attractive levels thereby giving an opportunity to earn returns far exceeding the long term returns of the stock which by the way are also very impressive at over 10 times in the last 10 years.

The other very attractive proposition for the sector is the size of opportunity itself. When I look at it, a similar example I can think about is 5 star hotels. If one goes 15-20 years back, 5 star hotels in India were almost fully positioned and built for foreigner clientele (for instance, you would hardly find water jets in the washrooms of 5 star hotels back then ;-)). Now if one visits any 5 star hotel in India, almost 80% plus customers are Indians - be it for leisure or business (and waterjets are also omnipresent ;-)). The same I feel can happen for Basmati (and few more premium category) Rice market, which is considered a pricey delicacy in India. As incomes grow, in a decade or two we will find that a significant % of Indian population are able to afford Basmati rice. Currently almost half of the current opportunity for these companies are in exports but India by itself can be a much larger producer and consumer of such and other pricey branded rice. A significant part of that as well as adjacent market opportunities are available in the hands of just few companies which have a potential to grow at high rates for a long time. This means a high terminal value and hence a much higher Price to earning ratio for such companies. Hence there seems to be a potential for both multiple re-rating and earnings growth which is the requisite condition for spotting a multi-bagger.

Regards,

Sarvesh Gupta

PS - I run a SEBI registered investment advisory firm and I have bought the stock for myself and clients right from levels of 110 and upwards in the recent fall. I am an active investor and may add more or exit depending on how the opportunity unfolds.

A comparison of different Indian consumer brands performance with ROE in 20s & PE ratios

High ROE FMCG players are intentionally left out for reasonable comparison. (Discl - Invested)

Disc.Invested

The Auditor remuneration seems so be on the lower side, almost @ Rs. 8/Lac. I’m taking this from Annual Report of '18-19.

Isn’t this a matter of concern?

Disc. Not invested. Analysis in progress

i can see the remuneration as 36 lacs. Auditor- M/s Walker Chandiok (auditing firm under Grant Thornton). Dont see an issue here…

Not going into environmental and political issue but this practice actually make no sense. they can just mix the residue into soil while they are preparing soil for sowing, burning soil actually reduces moisture and nutrients from soil. so my point is even if the govt tries to stop this practice it is not going to cause any harm to the farmland or product.

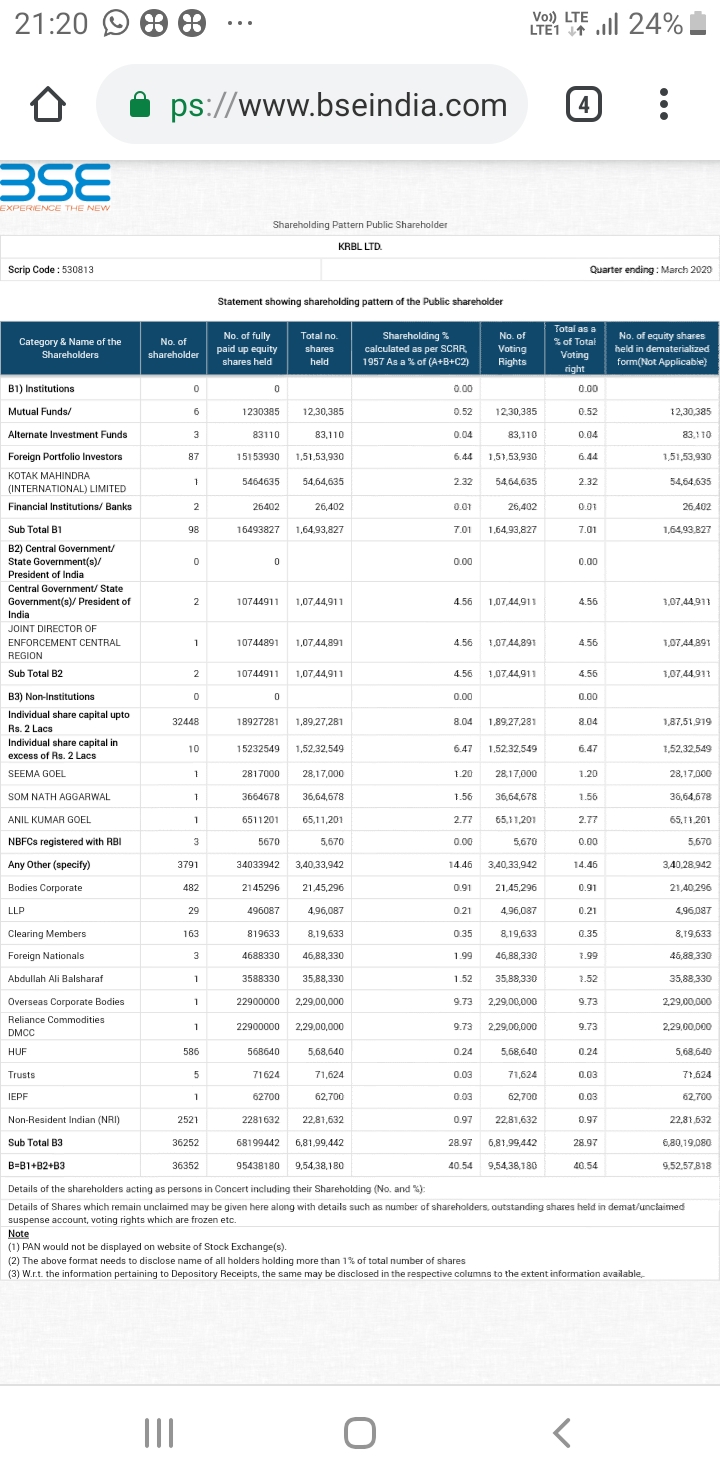

The DMCC is “Dubai Multi Commodities Centre”, so RI is having something there in Dubai and they are holding KRBL from that subsidiary(?) may be… the KRBL is anyway having Dubai connection.

Reliance Commodities dmcc is ADAG undertaking. Wanted to clarify this so that people don’t confuse it as Reliance Industries subsidy and tie KRBL story with Reliance Retail opportunity.

Thanks, actually i don’t know anything about this, I did a google search and come up with this DMCC thing, that’s why I put a ? there. ![]()

Every year we see part of company’s WC borrowings are from interest-free loans from promoters. What is the reason for this??

Not sure if this has been discussed above in the thread or not, but if the bank loans are available, then why the indulge in such related party transactions. Hope @rupaniamit, others can throw light on this.