First of all, it’s good to see a lot of people with skeptical lenses with all good questions probing for critical thinking. Sharing my opinions below. Sorry for long post but its long since I had to share my take on so many issues that have been raised. Thank you for sharing these issues.

KRBL has appointed Walker Chandiok &Co. as statutory auditor from July 24, 2018. If Bindal Brothers and KRBL management jointly cooked books, then that is a big problem. I didn’t find anything specifically to KRBL. If you find anything specifically that they did while being auditors at KRBL, please share it here with everyone.

Nothing wrong with what you are saying. We all have to protect our capital in the best possible manner. We all have different styles of investment and we need to invest in a way that allows us to sleep peacefully in the night. I call it sleep-adjusted-returns.

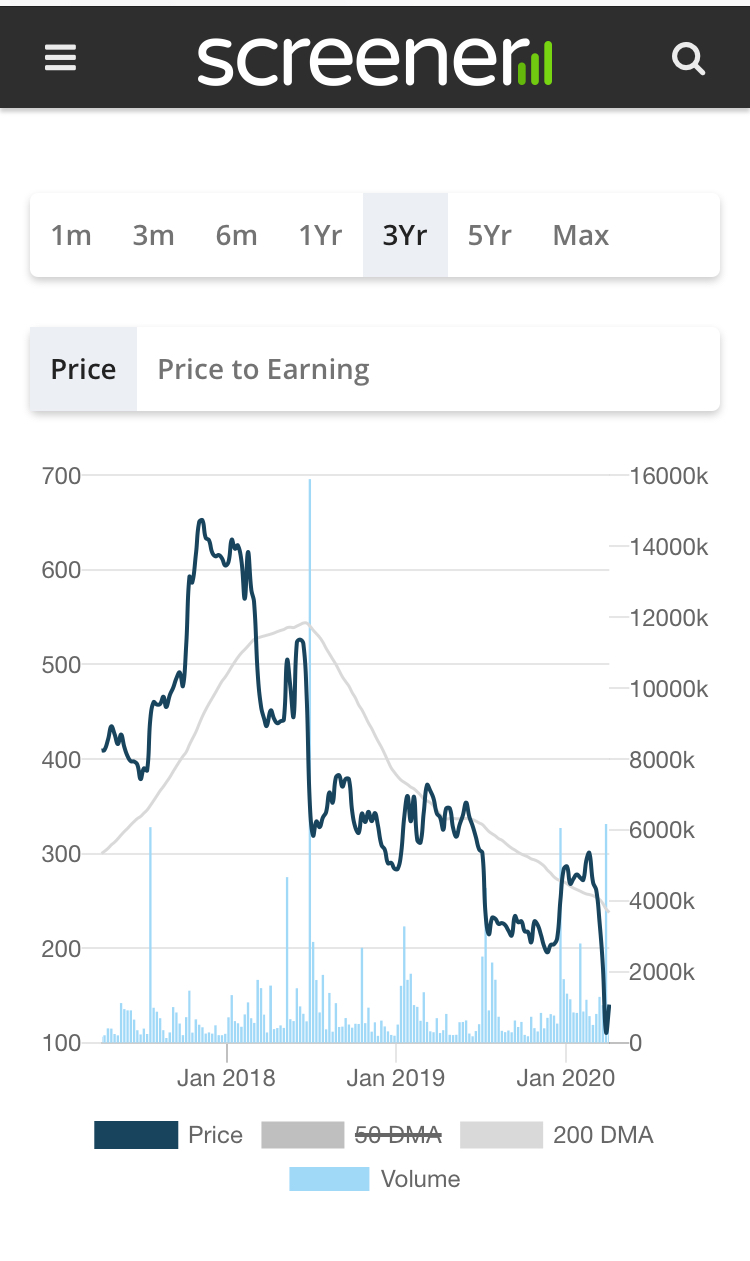

If you were just going to go by price action, you would have sold off most of your mid-cap & small-cap holdings post carnage in them after Jan 2018 since most were down > 50%. Market painted most small and mid cap businesses with same brush, but not all businesses had inherent ethical issues. Avanti fell 75% and BRL fell 55% from their 2018 peak. But Avanti Feeds jumped 3x to 777 from lows of 250 levels. Bharat Rasayan jumed 2.5 times from lows of 3500. Avanti & BRL are not fraud companies but you may stamp them as suspect managements by the type of price action that happened. You may also stamp Piramal Enterprise as fraud by the way their prices have fallen from 3000 to current levels. I can give you many such examples where a lot of good quality small and mid caps rallied and gave handsome return from Oct-Jan time period. But I hope you get my point. In stock markets, narratives change swiftly with falling and rising prices.

Bottom-line: I just don’t look at price action to make my judgement. And I don’t completely ignore it either. During extreme reactions on either side of the pendulum - nothing matters but the sentiment and emotions of the market participants. I have come to realize that it’s best to combine both fundamental and technical knowledge to act rationally in any market situation.

On 17th Jan 2020, the Appellate Tribunal has restored the possession in favor of the campnay, however, such attachment will continue till the conclusion of the matter. Matter at stake is 15cr. For me restoration of possession to the company is big victory. Rest you can make your judgements.

I have covered this above.

They won the case and big contingent liability of ~2000cr is behind them. I don’t understand what your point of concern is.

Kotak, Reliance, Anil Kumar Goel, were invested till end of Dec 2019. I know Vallum Capital was also invested and regularly attends earnings con-calls. We will see if that changes with Mar 2020 shareholding pattern. But I don’t take comfort by who is holding and who is not holding. I’d do my homework and have enough conviction in the business that I have bought that other’s actions don’t bother me at all.

I don’t think anyone else other than Mr. Goel can provide an answer to your question. If anyone else give you an answer that would be nothing but speculation.

Re: receivables management has shared in con-calls that for domestic 80% of payments come in 4 days (after cutting 1.5% cash discount). And then distributors pay in 30 days if they don’t pay in 4 days. Anything over 30 days, they have to pay 18% interest. They have not had any bad debts so far. Exports is done only against LCs. No credit in exports. For me receivables is not a point of concern.

Disc: invested and my views will be biased.