What is Biodiesel ?

Biodiesel is a liquid fuel, technically known as a mono-alkyl ester, made from oils and alcohols. Biodiesel is a renewable fuel that can be produced in any climate using already developed agricultural practices. Biodiesel is made from renewable resources such as vegetable oils, or other types of biomass. B100 is 100% biodiesel. Biodiesel is widely available in both its neat form (B100) and in blends with petroleum diesel (for example B2, B5, B20)

About Kotyark

Kotyark Industries Limited (Kotyark) is revolutionising the fuel industry by providing sustainable alternatives to fossil fuels. Incorporated in 2016, Kotyark is the only listed Indian Company that exclusively manufactures biodiesel and its by-products. The Company focuses on green energy and sustainable development of renewable resources (biofuel) through the adoption of environment-friendly technology, which is ultimately aimed at facilitating a net reduction of greenhouse gas emissions.

With its manufacturing unit at Swaroopgunj, District Sirohi, RICCO, Rajasthan, Kotyark is one of the key players in the state of Rajasthan in India. Its manufactured products find application in any and all industries that use diesel, primarily commercial vehicles and diesel generators. At present, the Company is capable of producing 500KL of biodiesel per day from multi feedstock.

Total Annual Production - 182500 KL

Capacity Utilisation in :

2019 - 3%

2020 - 5%

2021 - 12%

Raw Materials

- Non edible vegetable oil (which are all procured from Rajasthan & Gujarat) & Used cooking oil & kitchen waste

- Alcohol : Such as Ethanol, Methanol, Isopropyl or Butanol

- Catalysts : To initiate reaction Sodium Hydroxide and Potassium Hydroxide are used

End Products

- Biodiesel : Any vehicle that has a diesel engine can be powered by biodiesel easily, without any modifications. It is just like petroleum diesel, which can be used to fuel compression-ignition engines. Apart from transportation, it can also be used to power diesel-run generators.

- Crude Glycerin : For every 100 litres of biodiesel produced, approximately 14 litres of crude glycerin is produced as a by-product on average. Kotyark’s crude glycerol is sold to large refineries that upgrade and supply the refined rendition to other end-use sectors

Kotyark Industries has added 8 more mobile retail outlets (MRO) of biodiesel under its brand ‘Green N Green’, which puts the total to 25 such operational MRO’s. Further, in line with its strategy of expanding Retail Outlets’ revenue stream, the Company plans to apply for 50 more licenses.

At present, the Company is envisaging a potential ~4 lakh units of carbon credit, given its current scale of operations

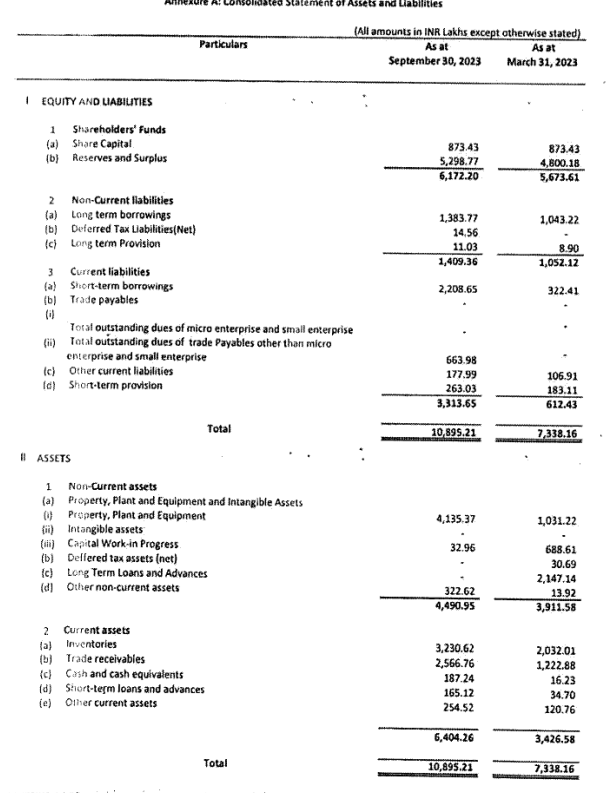

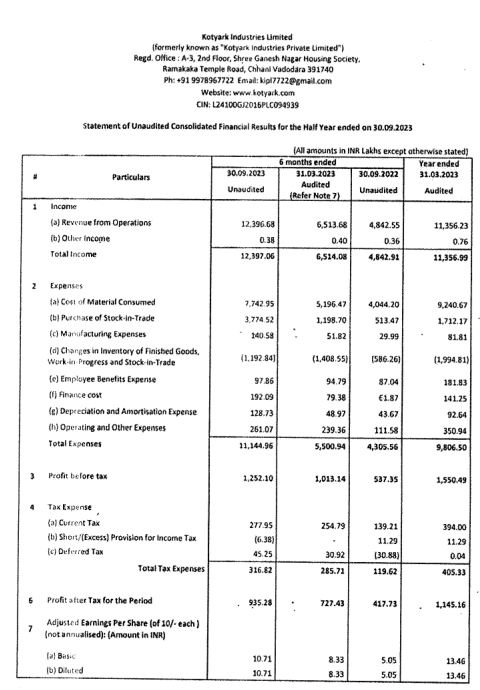

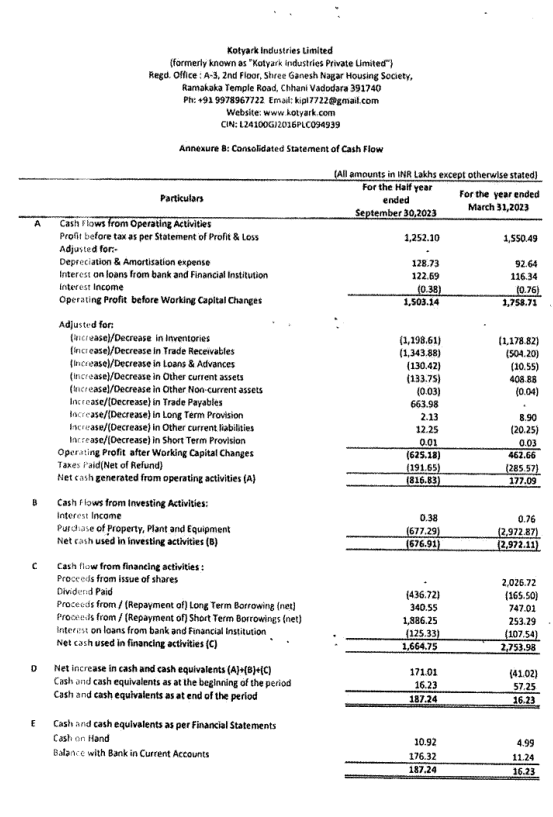

Financial Highlights for the year ended March 31st, 2022 :

• Revenue from Operations stood at ₹ 15,604.59 Lakhs in FY22 compared to ₹ 6,520.61 Lakhs in FY21, an increase of 139% YoY

• EBITDA (excluding Other Income) stood at ₹ 1,272.32 Lakhs in FY22, an increase of 338% YoY

• EBITDA margins stood at 8.2% in FY22, an increase of 370 bps YoY

• PAT stood at ₹ 864.04 Lakhs in FY22 compared to ₹ 104.44 Lakhs in FY21, an increase of 727% YoY

Recent Updates

- Amalgamation / Merger of Yamuna Bio Energy

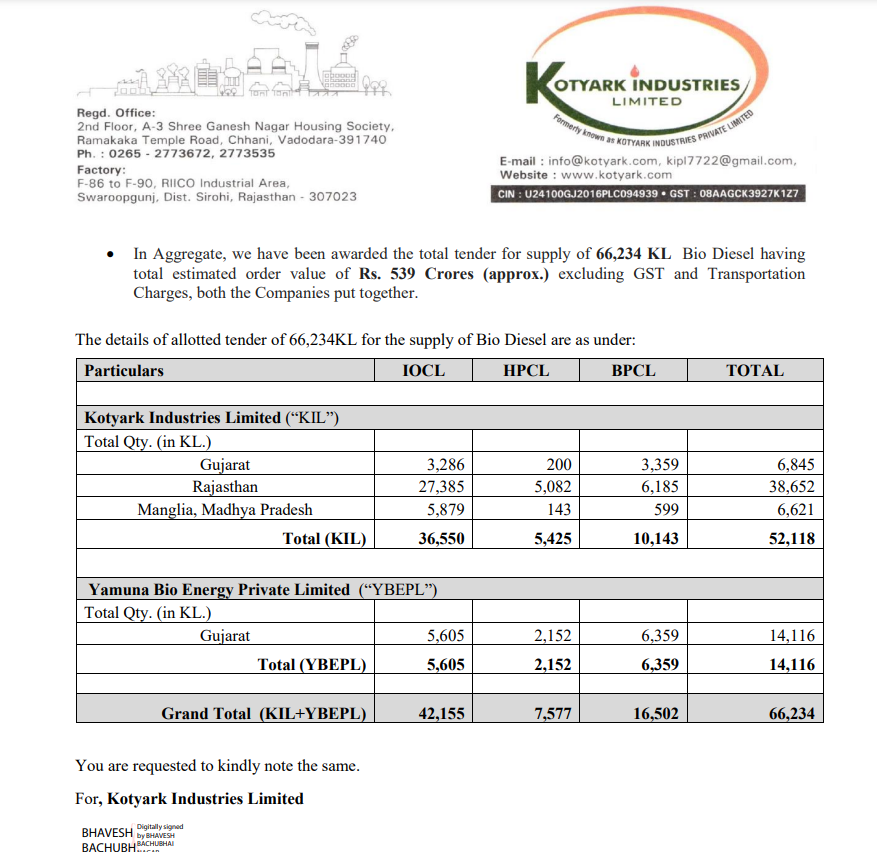

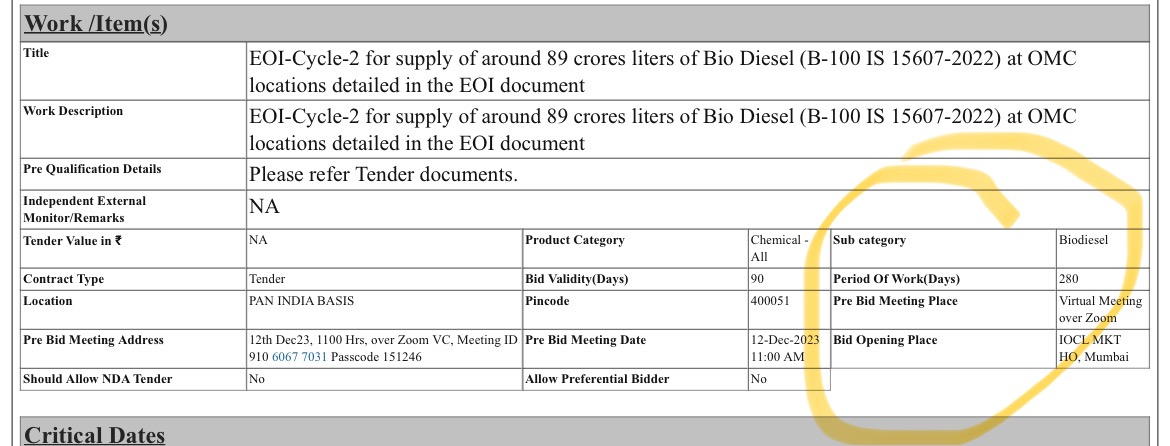

- Kotyark Industries & Yamuna Bio Energy win tender to supply Biodiesel worth ~₹25 Cr from IOCL

(this order-win is part of a joint tender of 3 OMCs in which both Companies participated, and so far, we have heard back from only one of the OMCs, i.e., Indian Oil Corporation Limited. More news on the same will be shared as we receive updates from other two OMCs.)

The future of biodiesel in India

- India’s Biodiesel Production is growing @8.6% CAGR till FY30

- The Indian government has proposed a target of 20% blending of ethanol in petrol and 5% blending of biodiesel in diesel by 2030

Risk

- Inherent Risk being a SME

- No Entry barrier to competitors in Biofuel (But opportunity & sectoral tailwind looks huge)

- Execution capability of Promotor

- Already a huge move in stock price from IPO

→ Anyone who has done scuttlebutt of the plant or personally met the promotors can share their experience (vision of promotor, their order book etc.) as its a SME very less information available.

Disc : Invested