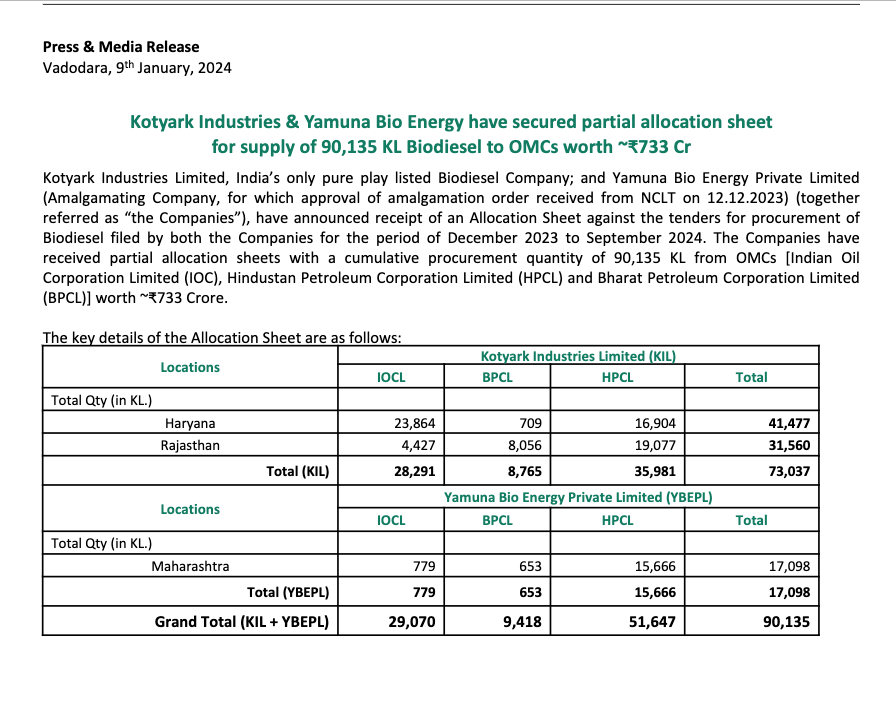

They have received an order of 733 Crore and might receive one more similar order. We should be able to see their execution skills in coming quarters. I am tracking it and took an initial position.

Disclaimer: Invested

They have received an order of 733 Crore and might receive one more similar order. We should be able to see their execution skills in coming quarters. I am tracking it and took an initial position.

Disclaimer: Invested

They have also incorporated a new wholly owned subsidiary called Kotyark Bio Specialty Ltd.

The only description provided about the business of this company, is that it will deal in advance Glycerin.

This information can be found here

Company seems to have great potential to create wealth for the share holders. The only concern for me is governance and execution and they seem to lack in both as pointed in this discussion.

i don’t understand why they are raising capital through preferential issue(of 55 Cr). they seem to have great order pipeline of worth more than 1500 Cr. they could easily make this money and pay within a year.

I would appreciate if someone can shed more light on these issues.

Disclaimer: Invested

Company has allocated 6.35 lacs shares to promoters/non-Promoters/public aggregating to 49.5 cr on preferential basic at 780 rupees share.

Seems like a good news. We should wait and see who has bought these shares.

corp filing

Disclaimer: Invested

Was interested by the numbers so went through the filings and annual report. Found some points which were a bit intriguing/strange. If anyone has any counter-points on the same; would be extremely helpful since the order book is growing at a rapid pace and it seems like a structurally growing business:

There are many points which don’t get answered to reflect the tremendous growth which is about to be there in next 1 year.

Can Anyone answer the above points to throw light on it?

Disclosure - Invested and could be biased

Hi experts,

Press :- https://nsearchives.nseindia.com/corporate/KOTYARK_17052024221745_Press.pdf

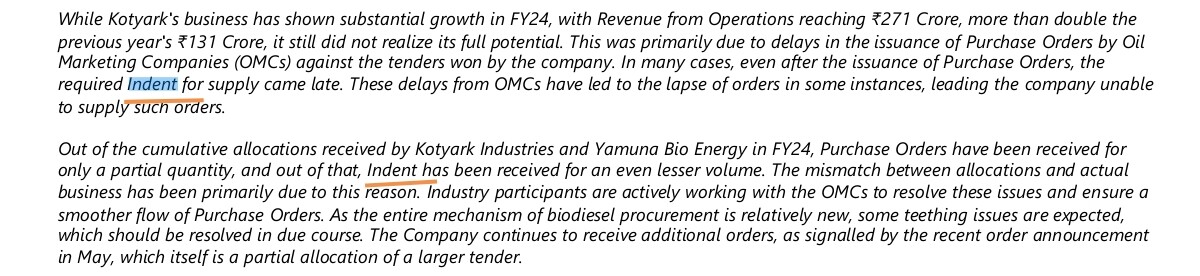

In the above mentioned press release i see some surprise and cautions points which looks very strange.

ex:- it still did not realize its full potential. This was primarily due to delays in the issuance of Purchase Orders by Oil Marketing Companies (OMCs) against the tenders won by the company. In many cases, even after the issuance of Purchase Orders, the required Indent for supply came late. These delays from OMCs have led to the lapse of orders in some instances, leading the company unable to supply such orders

can any give some comments on the same?

@srt @yrm91 @Chirayu26 @Vivek_Chadha @Dhvanit_Merchant17

Right

So OMC releases the tender → Purchase Order → Letter of intent

Since the bio diesel theme is new there is gap in the procurement of bio-diesel from OMC side. Also the raw material prices are high.

Post elections we should see some improvement in the procurement process and more and more tender will be released

Please see the ppt released by company. It was able to fully execute the quantity received in LOI. Its the OMC’s which are delaying plus govt extended the penalty imposition by 1 year and hence a delay in procurement as per my analysis

Disclaimer - Invested and biased

In my line of business I deal with a lot of government owned oil and gas entities and delays in procurement are norm here. Small companies who don’t have leverage, bargaining power and dedicated sales presence struggle with their collection. The smaller the vendor, the more delay they are likely to face with collection.

Its not about collection, its about Letter of intent for supply of bio-diesel

That was my point. Company executed an order against letter of intent and not an actual purchase order. If they don’t have purchase order they won’t get paid as it’s not in the system, which will impact collection.

It’s not an intent it’s called INDENT.

The company clearly states that they have POs but subsequently those POs were not converted to indents.

Google meaning of indent,

Disc: invested

I’m in sales and I have seen usage of letter of intents (spelled on customer-issued letter as “intent”). LOIs are generally used in the cases where there is time-pressure for business to recognize booking in a given period (month or quarter) and there is a delay in issuing POs (purchase order) due to several factors (approvals, system breakdown etc).

The company issued statement says indent, and specified what order the system follows,

What you have seen may be different.

Disc: invested

Vikas is right. Indent is different from. (Letter of) Intent.

LOI is a mere wish to do (procure)…indent is request to supply against issued purchase orders.

Regards

Disc. Tracking not yet invested

Indent and intent shouldn’t be mixed up. Indent here is a kind of call-off or request for services/supply against an agreed scope of work which is included in the purchase order. And which is what you see here.

Letter of intent is basically an unofficial agreement between seller and buyer to have a transaction without a legally binding purchase order in place.

So in case of Kotyark it seems they started the work not based on letter of intent but actual purchase order. But their problem as per the excerpt produced by you is delays in getting purchase order and not being committed the full scope of supply, as stipulated in POs, by their buyers. This leads to mismatch in booking and actual revenue of the company that eventually shows up in P&L.

Let’s hope they can resolve this with their buyers although I would say this is a very common with large government buyers.

Company website is down from weeks. No filings in long time.

Multiple queries sent on compensation of Gaurang bhai, Dhruti and Bhavini Shah is still unanswered.

Salaries for the current Fy shall be as follows:

Gaurang Bhai: 17 lacs per month

Dhruti Shah: 4 lacs per month (previous CFO has a salary of 25 thousand per month)

Bhavini Shah: 7 lacs per month

Combined annual salary of the family: 3.36 cr for a comapny with PAT of 22cr (15% of PAT)

Why does the promoter family deserve such a high salary for a company of this scale?

There is AGM on 27th Sept. You can sent questions as shareholder to CS and they shall be obligated to answer.

Queries were sent to CS post release of AR. 2 reminders have been added on top of it. No response.