Kotak bank Q3 concall highlights -

Segment wise loan growth -

Home Loans, LAP - 92 vs 76k cr, up 22 pc

Consumer bank (WC) - 30 vs 26k cr, up 15 pc

PL,BL,CDs - 15.7 vs 10k cr, up 56 !!!

Credit Cards- 10 vs 5.5k cr, up 81 pc !!!

Agri- 27.5 vs 26k cr, up 9 pc

Tractor Fin - 14 vs 10.7 k cr, up 29 pc

Micro Fin - 6.2 vs 3k cr, up 103 pc

Corporate bank - 70 vs 69k cr, up 1 pc

SME - 24 vs 20.4k cr, up 18 pc

Others - 6.5 vs 4.5 k cr, up 48 pc

Overall - 3.25 vs 2.75 lakh cr, up 19 pc

Deposits -

CASA at 52.8 vs 60.7 pc

A lot of SA deposits moved to Term Depositss

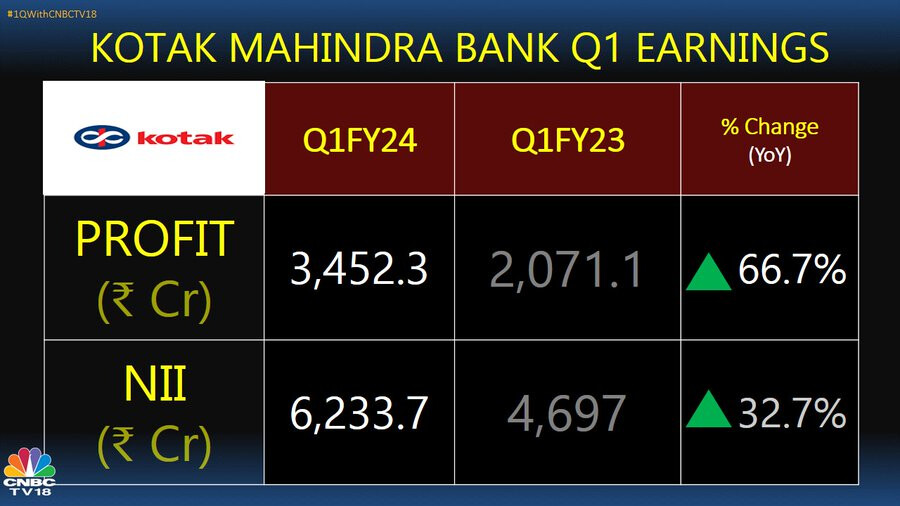

Consol PAT contributions-

Bank-3496 vs 2767 cr

Prime (car fin)-224 vs 313 cr

Investments-100 vs 101 cr

Microfinance-89 vs 43 cr

Securities-182 vs 252 cr

Kot Mah Capital-48 vs 42 cr

Life Ins-205 vs 267 cr

Gen Ins-(55) vs (46) cr

AMC - 192 vs 102 cr

Consol PAT at 4566 vs 3892 cr

Consol RoA at 3.06 vs 2.94 pc

Consol RoE - 16.9 vs 16.6 pc

Despite Capital Adequacy > 23 pc

Total branches at 1780

Management commentary -

Sustainable growth tgt for next few yrs at 17-22 pc

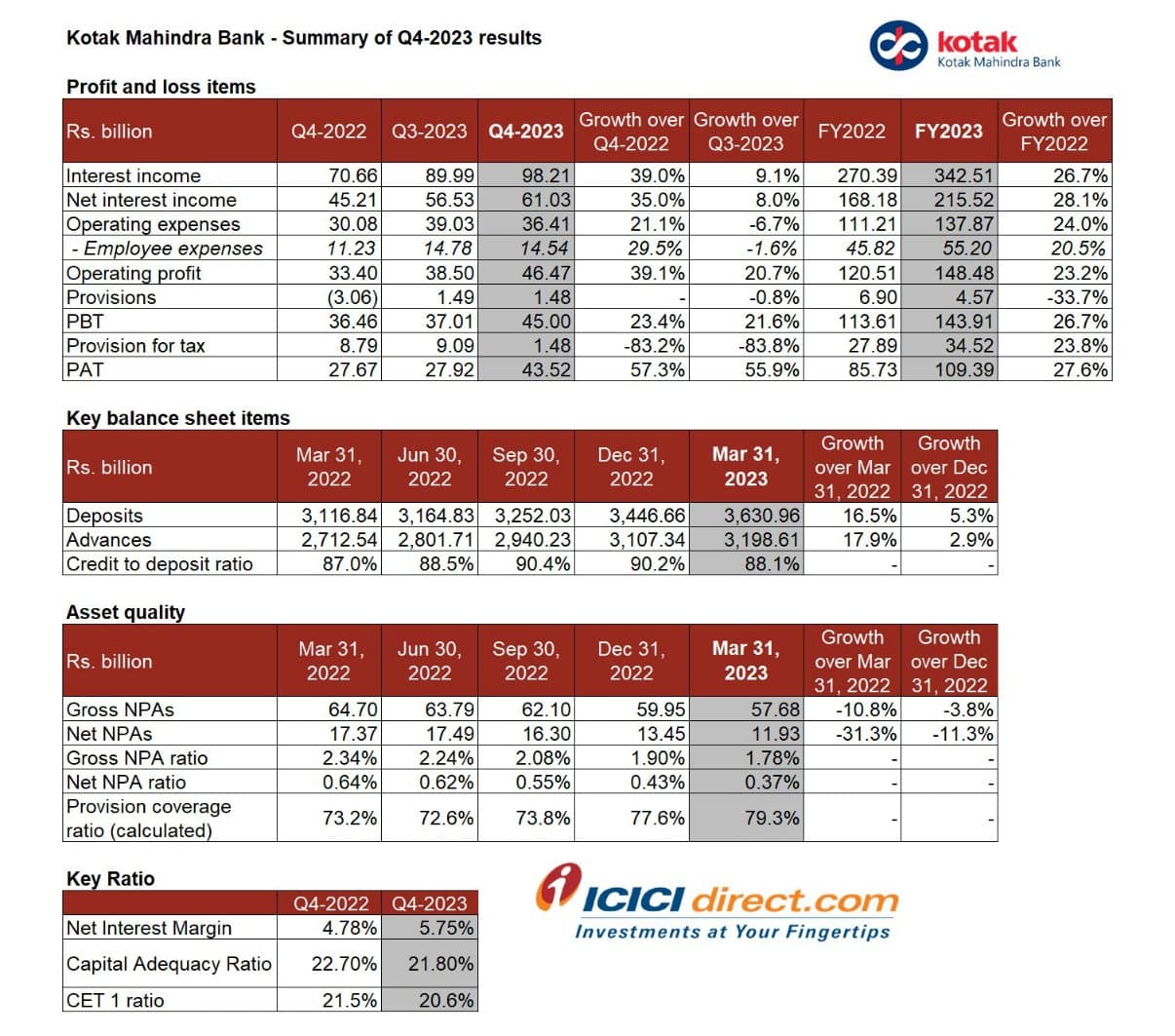

Q4 NIMs at 5.75 pc !!!

Bank’s standalone Q4 operating profits at 4647 cr, up 39 pc

GNPAs at 1.78 vs 2.34

NNPAs at 0.37 pc, PCR of 80 pc

Slippages - 823 cr ( @ 0.92 pc of advances on an annualised basis - well within control )

Restructured assets at - 0.22 pc ( very healthy )

Tractor Fin Mkt share at 11 pc

Term deposits grew by 40 pc yoy due increasing rates

Seeing slowdown in Kotak Prime’s business in FY 24

Kotak Life’s VNB margins are now best in the industry

Kotak Securities cash Mkt share at 10.5 vs 10.6 pc, Options mkt share at 5.6 vs 3 pc

Fall in Kotak Sec profits due to sharp fall in daily cash mkt turnover by aprox 30 pc

Kotak AMC AUM up 5 pc, reached 2.87 lakh cr. Equity AUM at 1.53 lakh cr, up 17.6 pc. Equity AUM mkt share at 6.5 pc. SIP book at 870 cr/month. Retail AUMs at 55 pc

NIMs should sustain above 5 pc for FY 24 as well

Witnessed repayments in the corporate book. Seeing high competition in this segment

Added aprox 100 branches last FY. Aim to add 150 branches this year

Clearly, Bank’s focus is more on digital 811 accounts vs physical branches

However, a healthy mix of physical branches shall also be maintained

Going to invest heavily in technology in next 12 months to improve per branch productivity vs peers. Likely to see significant gains going fwd

Disc: holding, biased