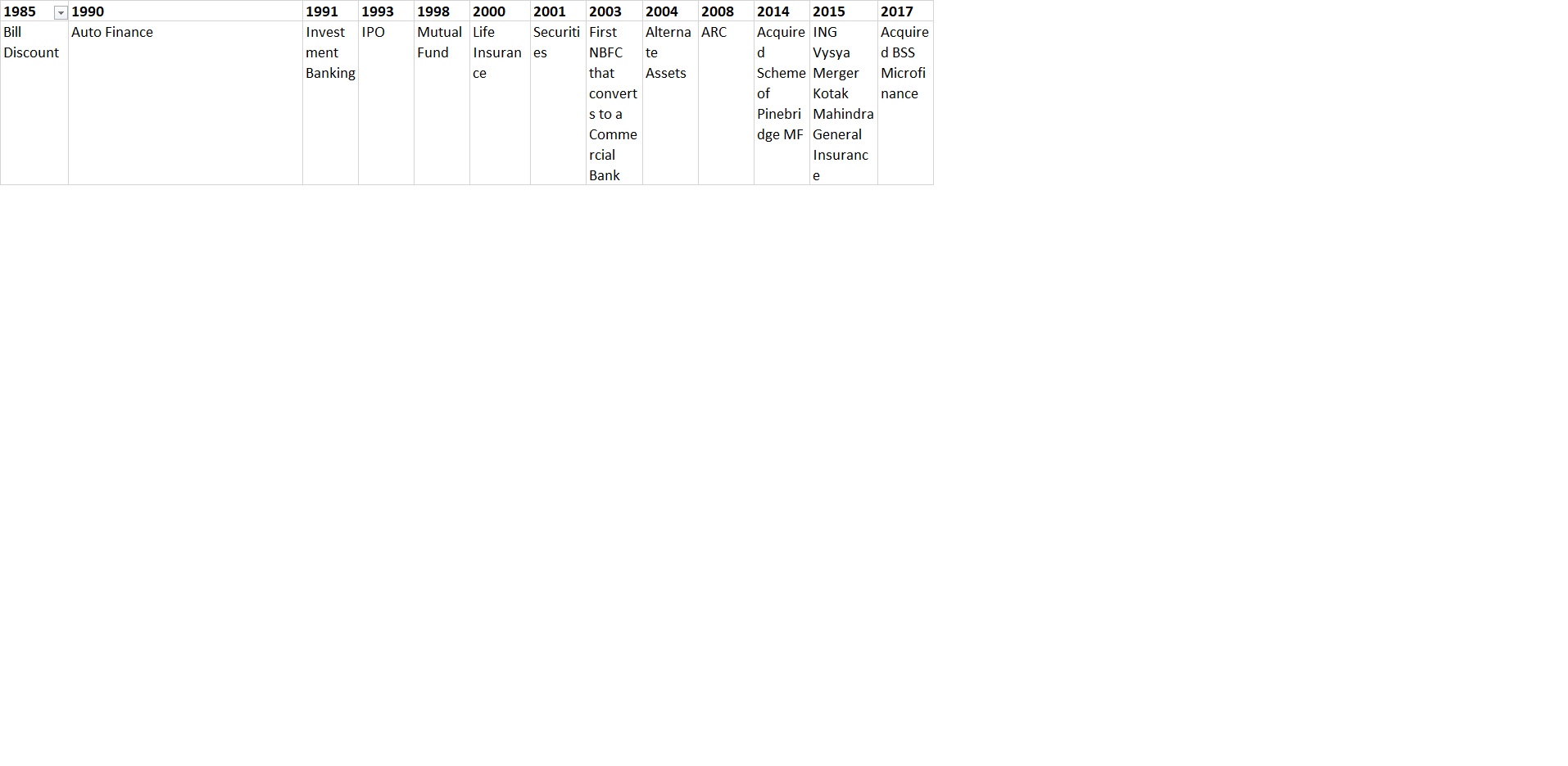

Kotak is a well known bank across the country. Since there is no existing thread, I would like to take the opportunity to create one.

Key banking numbers in FY19:

PAT Margins: 17%

RoA: 1.7%

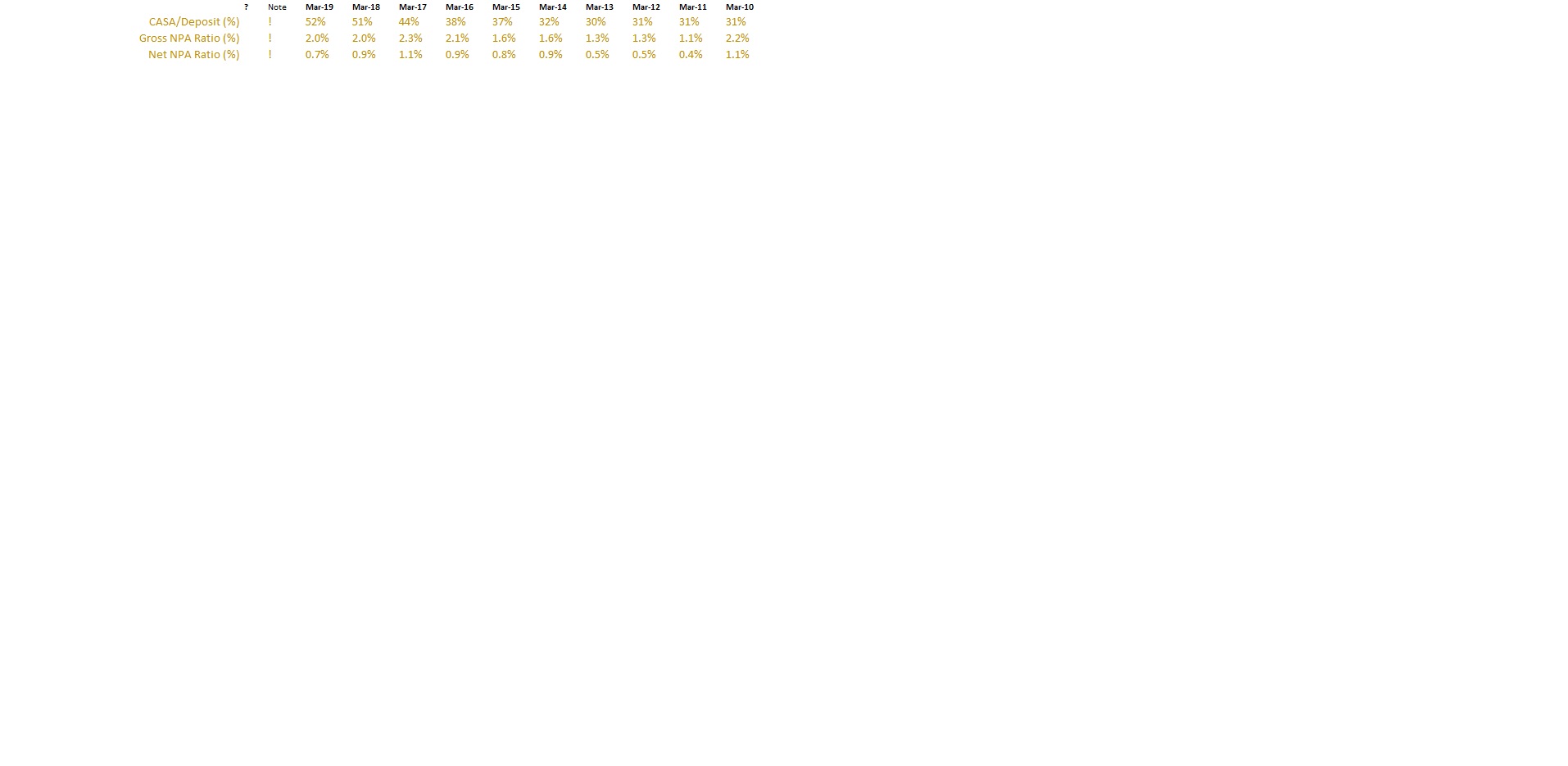

CASA Deposits Ratio: 52.4%

Govt Securities in Investments: 81.6%

Unsecured Loans: 23.8%

Priority Sector Loans: 35.1%

NIM: 4.48%

GNPA: 2.14%

NNPA: 0.75%

For more numbers, please allow me to quote screener: Kotak Mahindra Bank Ltd financial results and price chart - Screener

Management:

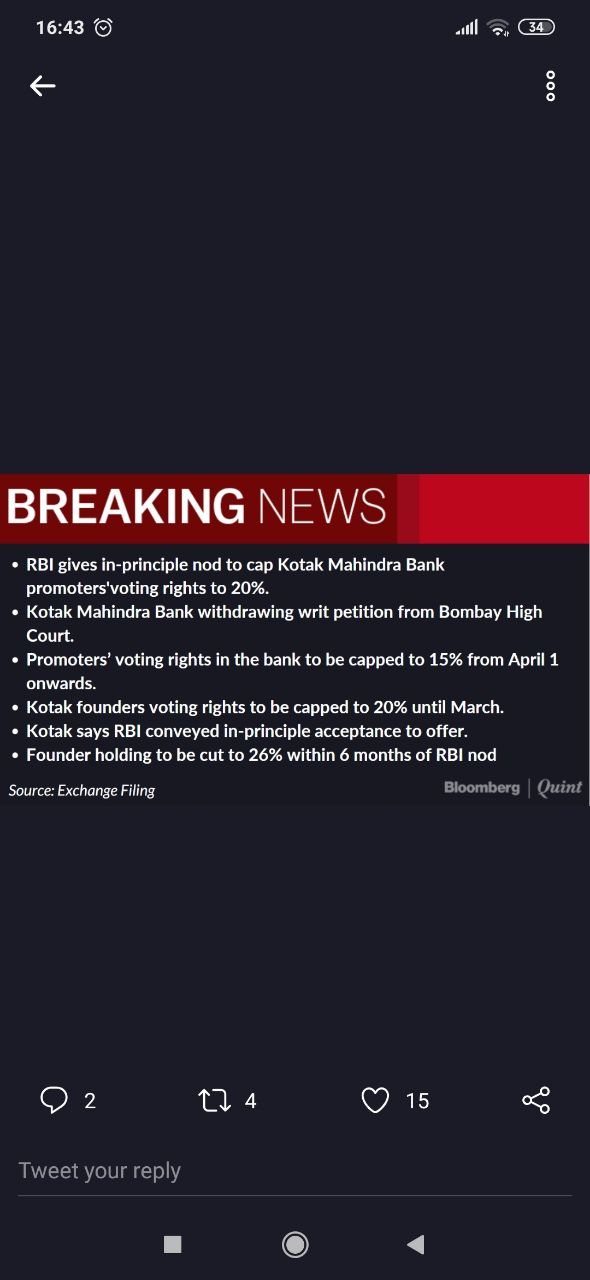

Uday Kotak who owns about 30% of the bank is leading the bank full on. His wording in ARs and Conf calls suggest he is fully committed to its long-term prosperity. A step further is to notice that he bought out the minority shareholders in Life Insurance business and all the non-banking subsidiaries are now 100% owned by the bank. He is also fighting with RBI in court to retain his ownership in the bank. If one goes through the conf calls, it is easy to observe that Uday Kotak is quite cautious in nature, going slowly when trying out something new (like ARC, Consumer durable) and slowly increasing their growth in that as they learn that segment.

Another important point to notice is most of the senior management professionals have been with the bank since 1990s which demonstrates their commitment to the bank, its leader, culture and prosperity.

Liabilities:

Regular customers - These customers typically belong to mass affluent segment and have high balances and most of them were acquired during the pre-demonetisation era.

811 customers - 811 campaign was launched after the demonetisation incident to acquire customers digitally. After launching the campaign the company set itself a target to double its customer franchise from 8 million to 16 million in 18 months (from March17 to September18) which it did achieve successfully.

Kotak’s CASA Deposit ratio is industry best at 52.5% and they don’t have a number in mind and would like to achieve as best as possible for that. Important to remember that Kotak also offered higher interest rate for savings deposits till FY19 which is hitting the bottomline by 1000 crores. Uday Kotak says this is the cost they would like to take for building long-term stable liability franchise. Starting FY20, they seem to be decreasing the interest rate here. In Q1FY20, they decreased for savings accounts with balance less than 1 lakh.

According to Uday Kotak, building a stable low cost franchise is the toughest part of building a financial services firm. He clearly stated that this is his top priority over everything else and his team is fully committed to go as far as possible in this aspect.

| Deposits | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|

| Demand Deposits - From Banks | 3685.3 | 4031.4 | 3839.9 | 3951.4 | 2551.4 | 1710 | |

| Demand Deposits - From Others | 385324.3 | 318426.2 | 273768 | 228865.3 | 129262 | 85698.2 | |

| Demand Deposits - Total | 389009.6 | 322457.6 | 277607.9 | 232816.7 | 131813.4 | 87408.2 | |

| Savings Bank Deposits | 796847.1 | 655292 | 415039.3 | 294947.2 | 140361.1 | 100870.5 | |

| Term Deposits - From Banks | 630.8 | 13446.9 | 5776.8 | 7476.2 | 10575.5 | 6103.6 | |

| Term Deposits - From Others | 1072316.1 | 935236 | 875834.7 | 851190 | 465853.1 | 396341.1 | |

| Term Deposits - Total | 1072946.9 | 948682.9 | 881611.5 | 858666.2 | 476428.6 | 402444.7 | |

| Total Deposits | 2258803.6 | 1926432.5 | 1574258.7 | 1386430.1 | 748603.1 | 590723.4 | |

| CASA Deposits Ratio | 0.5249 | 0.5075 | 0.4399 | 0.3806 | 0.3635 | 0.3187 |

Assets:

Corporate Banking - 30% of Assets (stable across years)

Kotak is growing at 20% in this area and would like to keep it that way. Based on management commentary, it sounds like they can grow at faster rate than this if they want to but however would like to limit themselves to 20%. Important to remember that banks with heavy exposure to corporate / wholesale banking are those with highest NPAs. There is a study by PwC on this area. Please find that attached here: banking_profitability.pdf (629.6 KB)

Corporate loan book contains about 60% working capital, 40% term out of which around 25% will be what we call the long term about 3 year plus loans. So it is largely medium term and short term oriented book.

Home Loans and LAP - 20% of Assets (used to be ~25% few years back)

Though home loans is considered to be one of the safest loan asset, there are some evil practices going on in the LAP area. The collateral valuers of LAP (or any other collateral) are not regulated / monitored and typically quoting very high value of what they actually should. The bank is cautious in this area and has developed relying on internal mechanisms to judge about the same.

Agriculture Division - 13% of Assets (used to be ~20% few years back)

The bank slowed down in this area too and again due to some bad practices. Apparently farmers don’t have to pay any amount to the bank for the first year after they receive a crop loan. Lots of people, especially in Punjab, are exploiting this law by just taking loan on land by claiming it as crop loan. And that too in big ticket size. Essentially, it is LAP disguised as crop loans to avail its benefits. So the bank has slowed down quite a bit here too and decreased its exposure. Actually, most of the existing exposure has come from ING Vysya bank when they were merged.

Another thing the bank has done is to increase its market share in tractor financing. Kotak bank is the best in tractor financing and have been increasing their share significantly to meet the Agri target.

CVs & CEs - 10% of Assets (stable across years)

This was slowed down during the period of 2011-12 due to some bad practices which were openly called out by the management. Once it is resolved after the slowdown in 2013-14, the company seems to be growing this portfolio at 20%

Business Banking - 10% of Assets (used to be ~20% few years back)

This portfolio is also slowed down due to bad practices. Again the same story of collateral valuation mismanagement. The NPA probability of SMEs is a bit higher as compared to other loans. But when the bankers go to collect the collateral, it is typically observed that the defaulter is vanished, his equipment also sometimes and the value of the factory is a fraction of what the independent collateral valuer valued it for. So this portfolio is also intentionally slowed down by the management.

Small Business, Personal Loans & CCs - 16% of Assets (used to be almost 0% few years back)

This is fast increasing as this segment is highly underpenetrated. Analysts did ask that the income levels of people is not growing at this rate and how are we comfortable growing this segment at such rates and the answer was underpenetration.

Other Loans - 2% of Assets

| Advances | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|

| Corporate Banking | 618887 | 521333 | 417031 | 346965 | 202995 | 143773 | |

| Home Loans and LAP | 407216 | 324294 | 261209 | 230094 | 147087 | 120994 | |

| Agriculture Division | 269915 | 229156 | 189687 | 179929 | 121058 | 104681 | |

| CVs & CEs | 197058 | 152017 | 108270 | 74633 | 52040 | 54412 | |

| Business Banking | 182154 | 182690 | 178841 | 233181 | 64216 | 53879 | |

| Small Business, Personal loans & CCs | 331642 | 251292 | 173865 | 96268 | 62628 | 4320 | |

| Other Loans | 50076 | 36397 | 31918 | 22853 | 11583 | 6217 | |

| Total Advances | 2056948 | 1697179 | 1360821 | 1183923 | 661607 | 488276 |

Asset Liability Mismatch:

Reasonable amount of mismatch during the periods of 3 months to 6 months; 6 months to 1 year and 1 year to 3 years. I’m not sure if this is a big concern. Request experienced people to guide on that.

| ALM (crores) | |||||

|---|---|---|---|---|---|

| 2019 | 2018 | 2017 | 2016 | ||

| 1 day - Assets | 11561.86 | 14093.59 | 17535.32 | 13314.5 | |

| 1 day - Liabilities | 6604.18 | 5795.79 | 4993.39 | 1478.91 | |

| Cum Diff | 4957.68 | 8297.8 | 12541.93 | 11835.59 | |

| 2 to 7 days - Assets | 15393.87 | 9484.21 | 6052.64 | 8249.24 | |

| 2 to 7 days - Liabilities | 17712.73 | 11501.91 | 13218.02 | 11403.61 | |

| Cum Diff | 2638.82 | 6280.1 | 5376.55 | 8681.22 | |

| 8 to 14 days - Assets | 3766.22 | 4630.57 | 4128.86 | 4840.51 | |

| 8 to 14 days - Liabilities | 4743.57 | 4526.37 | 3296.55 | 10007.56 | |

| Cum Diff | 1661.47 | 6384.3 | 6208.86 | 3514.17 | |

| 15 to 28 days - Assets | 8113.85 | 8402.84 | 5310.05 | 6778.39 | |

| 15 to 28 days - Liabilities | 4551.87 | 6914.95 | 6017.64 | 5480.13 | |

| Cum Diff | 5223.45 | 7872.19 | 5501.27 | 4812.43 | |

| 29 days to 3 months - Assets | 27451.79 | 23450.52 | 20518.54 | 21089.26 | |

| 29 days to 3 months - Liabilities | 35230.54 | 32005.44 | 26403.64 | 30254.4 | |

| Cum Diff | -2555.3 | -682.73 | -383.83 | -4352.71 | |

| 3 to 6 months - Assets | 23774.75 | 17740.54 | 15457.5 | 13501.25 | |

| 3 to 6 months - Liabilities | 38008.35 | 33584.26 | 30937.76 | 30338.5 | |

| Cum Diff | -16788.9 | -16526.45 | -15864.09 | -21189.96 | |

| 6 months to 1 year - Assets | 22997.73 | 20459.17 | 12472.42 | 15893.62 | |

| 6 months to 1 year - Liabilities | 38483.56 | 29938.59 | 22618.66 | 25229.8 | |

| Cum Diff | -32274.73 | -26005.87 | -26010.33 | -30526.14 | |

| 1 year to 3 years - Assets | 118425.33 | 98397.76 | 73888.59 | 61929.7 | |

| 1 year to 3 years - Liabilities | 127012.12 | 101434.67 | 77771.76 | 47126.85 | |

| Cum Diff | -40861.52 | -29042.78 | -29893.5 | -15723.29 | |

| 3 years to 5 years - Assets | 27546.99 | 23668.19 | 14736.43 | 14084.42 | |

| 3 years to 5 years - Liabilities | 4073.05 | 4430.1 | 2577.12 | 9705.03 | |

| Cum Diff | -17387.58 | -9804.69 | -17734.19 | -11343.9 | |

| > 5 years - Assets | 33786.81 | 25527.66 | 19921.14 | 18858.86 | |

| > 5 years - Liabilities | 480.56 | 378.83 | 971.77 | 2739.47 | |

| Cum Diff | 15918.67 | 15344.14 | 1215.18 | 4775.49 |

Kotak Mahindra Asset Management Company:

KMAMC is the asset management arm of the bank. It is well acknowledged that the asset management industry is highly underpenetrated. I think one can go through HDFC AMC thread to find out more details about this industry. I’m putting down some numbers for people to quickly get to speed.

| KMAMC Financials | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|

| Income (crores) | 655 | 518.9 | 291.2 | 240 | 125.4 | 166.1 | |

| PBT (crores) | 337.1 | 124.5 | 58.6 | 71.9 | -35.9 | 49.6 | |

| PAT (crores) | 218.1 | 81.2 | 38.2 | 59.3 | -36.2 | 33.4 |

| KMAMC Other Numbers | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|

| Equity AUM (crores) | 54830 | 44475 | 19922 | 13666 | 6450 | 3107 | |

| Debt AUM (crores) | 83385 | 70924 | 57169 | 41079 | 32137 | 32582 | |

| Total AUM (crores) | 138215 | 115399 | 77091 | 54745 | 38587 | 35689 | |

| Market share (Net Equity Inflows) | 5.20% | 5% | |||||

| Market share (Total Equity) | 3.70% | 2.40% | 1.80% | 1.30% |

Kotak Life Insurance:

This is the Life Insurance arm of the bank. Again, I would not like to clutter the first post with too much info on subsidiaries. So just putting some numbers and will come back on details of the subsidiary in later posts.

| KLI Numbers (crores) | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|

| Gross Premium Income | 8168.3 | 6598.7 | 5139.5 | 3971.7 | 3038.1 | 2700.8 | |

| First-year premium | 3977.1 | 3404.2 | 2849.7 | 2209.7 | 1540.2 | 1271.8 | |

| PBT - Shareholders’ account | 590.8 | 471.2 | 342.7 | 281.9 | 261.2 | 261.2 | |

| PAT - Shareholders’ account | 507.2 | 413.4 | 303.3 | 250.7 | 228.9 | 239.1 |

| KLI Premium Mix | 2019 | 2018 | 2017 | 2016 | 2015 | |

|---|---|---|---|---|---|---|

| Individual regular premium | 1616.2 | 1530.4 | 1176.2 | 925 | 602.3 | |

| Individual single premium | 515.4 | 441.5 | 260.4 | 138.8 | 147.1 | |

| Group regular premium | 1845.5 | 1432.4 | 1413.1 | 721.7 | 459.1 | |

| Group single premium | 0 | 0 | 0 | 424.2 | 331.7 | |

| Total new business premium | 3977.1 | 3404.3 | 2849.7 | 2209.7 | 1540.2 | |

| Renewal premium | 4191.2 | 3194.5 | 2289.8 | 1762 | 1497.9 | |

| Gross premium | 8168.3 | 6598.8 | 5139.5 | 3971.7 | 3038.1 | |

| New Business Premium Growth % | 0.16825 | 0.19461 | 0.28963 | 0.43468 | 0.21103 | |

| Renewal Premium Growth % | 0.31200 | 0.39510 | 0.29954 | 0.17631 | 0.04821 |

| KLI Other Numbers | 2019 | 2018 | 2017 | 2016 | 2015 | |

|---|---|---|---|---|---|---|

| Cost Analysis | 16.30% | 16.80% | 18.10% | 20% | 22% | |

| AUM (crores) | 30310 | 25133 | 20940 | 16936 | 15219 | |

| Claims Settlement Ratio | 99% | 99.30% | 99.50% | 98.80% | 98.30% | |

| Market Share (of Private) | 5.80% | 6.20% | 5.97% | 4.40% | ||

| Solvency Ratio | 3.02 | 3.05 | 3 | 3.11 | 3.13 | |

| AUM Growth Rate | 0.2059 | 0.2002 | 0.2364 | 0.1128 | 0.2573 |

There are other subsidiaries which are owned by the bank too which are quite small. Kotak Mahindra Prime is a reasonably sized one which gives Auto loans and recently starting consumer durable loans. I will write follow up posts on the subsidiaries in the following months to come.

Investment Case:

- PSU Banks and NBFCs are struggling and this is to benefit well-run private banks. This will also help bring back appropriate pricing into the industry increasing the margins. High CASA deposit ratio of Kotak is going to help them give industry leading margins

- Kotak has more than doubled its customer base over the past two years after demonetisation using 811 initiative. However, the new customers are of low balances. The management is now looking to cross-sell products to these customers and increase their revenues

- Kotak’s savings deposits used to offer higher interest compared to other banks. This has helped them increase their CASA deposits by mind-boggling growth rates. Kotak is now decreasing this interest rate which is helping them increase their margins and this is coming while maintaining (in-fact increasing) their CASA deposit ratio. You can observe that PBT margins have improved in H2FY20

- Non-banking financial businesses like Life Insurance and AMCs are doing very well. I believe the under-penetration of these industries well discussed across various threads now. No plans for management to spin them off and list them but still should help contribute to bottom-line of the consolidated company

Risks / Concerns / Questions:

- Asset Liability Mismatch during the periods of 3 months to 6 months; 6 months to 1 year; and 1 year to 3 years. Bank might be borrowing some funds when those periods occur during the year and using those to clear the liabilities. But is this sustainable?

- Very low (though increasing) penetration in credit cards. HDFC is bang-on in this area. People typically maintain higher balance in the bank of which you own the credit card. So wondering if that will hit the CASA deposit ratio of Kotak going forward

- Why did the bank merge itself with ING Vysya Bank?

- Tail risk, like for any financial company. You lend today but realize only few years later that it is a bad loan

- High valuation

Discl: No holdings. Recently started looking up. Planning to follow the company closely. This is not a buy / sell recommendation. Investors are required to do their own due diligence before taking any decision. All of the above information is public and available on Kotak Mahindra Bank website.