Wish it was a simple answer, believe valuations are a function of broader market sentiments, growth (current+ ahead), sector dynamics etc. Not looking healthy in current state but mkt being forward looking would have factored them

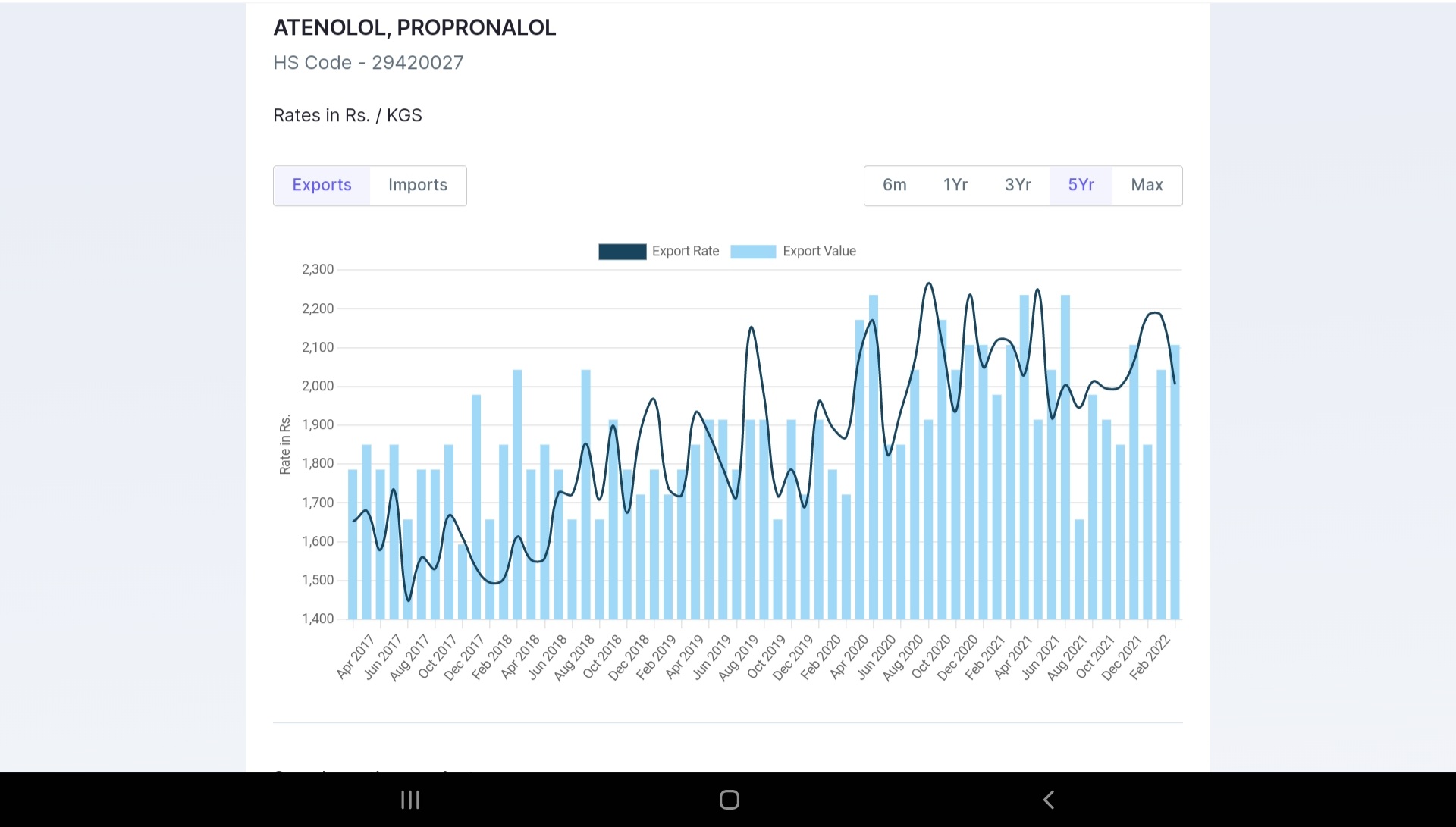

APIs seem to be coming off a high base of last year and have price correction across the board, in Kopran case here are few prominent one’s ( there seems volume growth but price trend is downward and on positive side at bottom of longer range ), good thing though is Atenolol- key bet that Kopran calls out in presentations, seem to be bucking trend and holding quite well

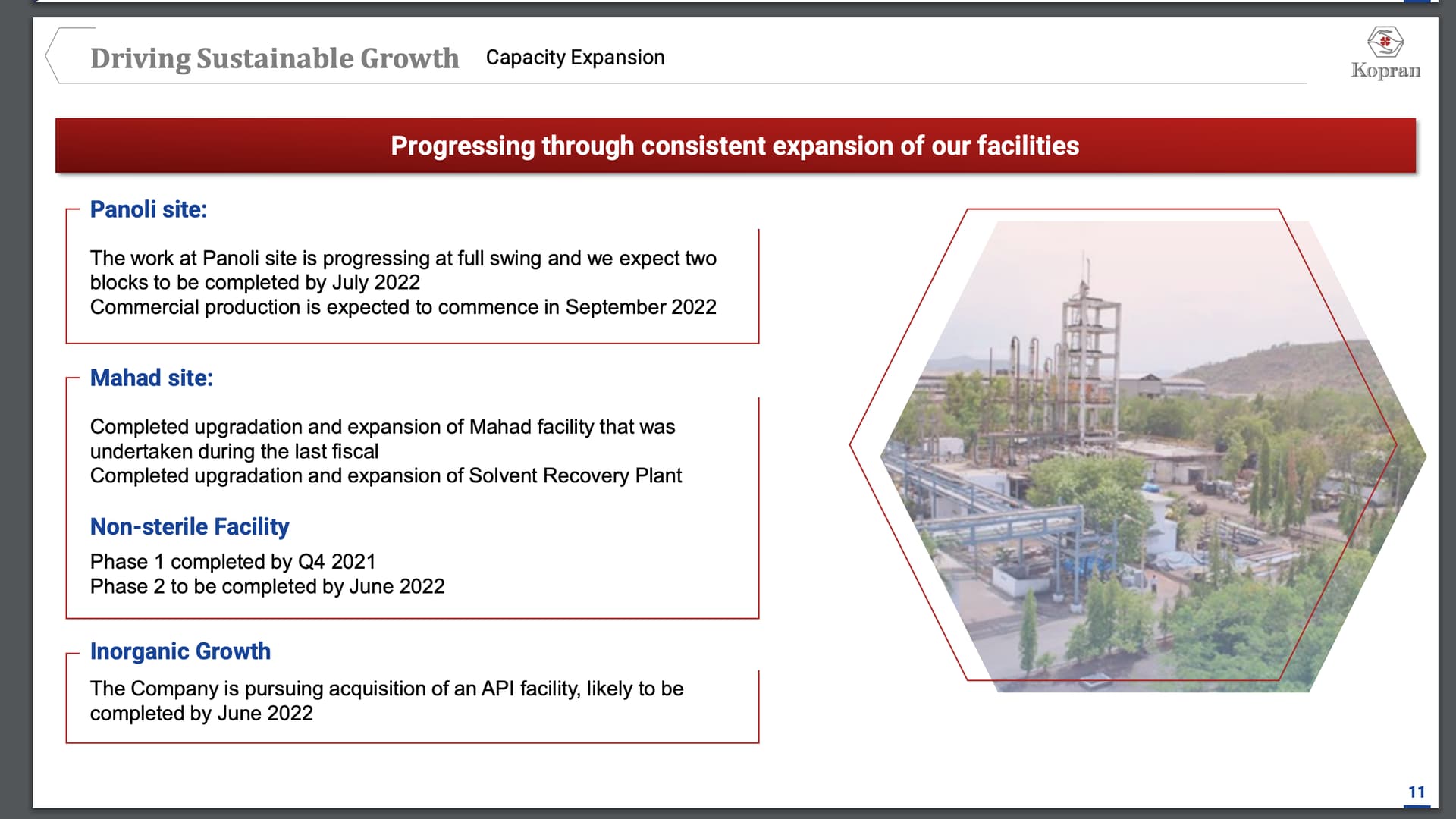

The Investor presentation mentions about inorganic growth through the acquisition of an API facility which should be ready by end June itself. This materially alters the situation as it hastens the Sales growth & will give the much needed boost to the operations. This plant apparently was a sick unit & has been picked quite cheap by the Co. The Panoli plant too should be operational by September end. This is in addition to the expansion being carried out at the Mahad facility.

The second half of the current year should see the results of the current expansion start playing out with Sales for current year expected to be in the vicinity of 700 crs though the next year (2023-24) should see the full impact of the current expansion with sales in the vicinity of 800-1000 crs. This could potentially take Kopran into a different league with operating profits in the range of about 180-200 crs & Pat of about 115-125 crs. The current correction has brought the market cap down to about 1050 crs & this presents a very interesting opportunity indeed!

Hope many members have already seen this. But anyway sharing here.

Please watch from 27 Minutes for more details on Kopran.

Actually you can start watching from 22 minutes on the timeline,

Special thanks to Sujal sir for sharing this on Youtube.

Disc- Invested & Biased.

Can someone throw some light on the line item - " purchase of stock in trade ". It has gone up from 1.2 cr to 16.4 cr YoY and from 1.0 cr QoQ. What could be the reason???

I am just wondering why Kopran does not do ConCall.

Doing ConCall increase faith of investor. It gives a platform to ask questions to management and also shows management capability to handle questions regarding their company. It increase transparency.

After a long time some developments on acquisition as Investor Presentation is not released yet.

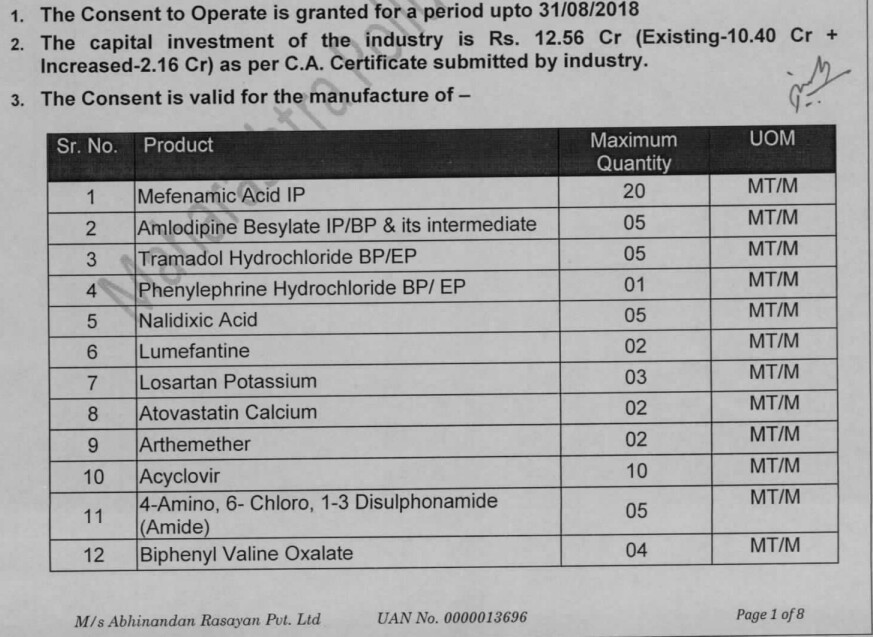

Sub: Acquisition of Assets

This is to inform you that pursuant to an agreement entered into by Kopran Research Laboratories Limited, the wholly owned subsidiary of Kopran Limited, it has acquired the assets of an API manufacturing Unit of Abhinandan Rasayan Private Limited located at MIDC – Ambernath, subject to certain terms and conditions as mentioned in the said agreement. Pursuant to the said acquisition, once the unit is made fully functional, it will help the Company in increasing its API and intermediate production capacity.

Abhinandan Rasayan Private Limited (ARPL)

Lasa Supergenerics Ltd has acquired the assets (which includes land and building with entire plant and Machinery) of ARPL for a total consideration of Rs.15 crore via memorandum of understanding dated March 18, 2018.

The Said acquisition was under dispute due to alleged collusion between lender and Abhinandan Rasayan Pvt. Ltd. to save Abhinandan Rasayan Pvt. Ltd. account turn bad in Lenders Books.

Due to the alleged foul play by other parties the deal stood cancelled as transaction did not succeed within stipulated period.

I was trying to understand Kopran’s installed and potential upcoming API capacities.

Mahad - 474 MTPA API (expanding to 924MTPA as per Aug 2020 EC application)

Panoli (2019 acquired) with 60MTPA capacities (expanding to 1212 MTPA - API + intermediates) as per 2020 EC application.

Abhinandan Rasayan - 828 MTPA (ref @Pranshinv post above)

So effectively existing API capacities could increase from about 534 MTPA to approx 2500 MTPA over the next 3-5 years.

Also, the Kopran presentations keep referring to Expansions being commissioned and in process of being commissioned - I am presuming that this is within their sanctioned 474 MTPA and not beyond since EC clearance perhaps was pending as late as Aug / Sep 2022.

Expansion is huge (>6X)

Approvals have also been received

Funds is lying in Bank acct (Private Placement)

Waiting for expansion to be converted into Sales and then Cash Profits !

(MT/A)

API/Intermediates

Plants

Existing

Proposed

Total

Panoli

60

1152

1212

Mahad

468

456

924

Ambernath

768

768

528

2376

2904

Savroli Plant (Formulation) expansion has also get approval.

why are these improvements not showing up in results? In the absence of conference calls, information is not easy to find out. What are the reasons for the slide in results.

Yes. I also noticed this. But the quantity is just TOO SMALL and its first time new purchase for H. Somani. So am not fully convinced about this. Have to track for few mare days and then decide.

dr.vikas

")