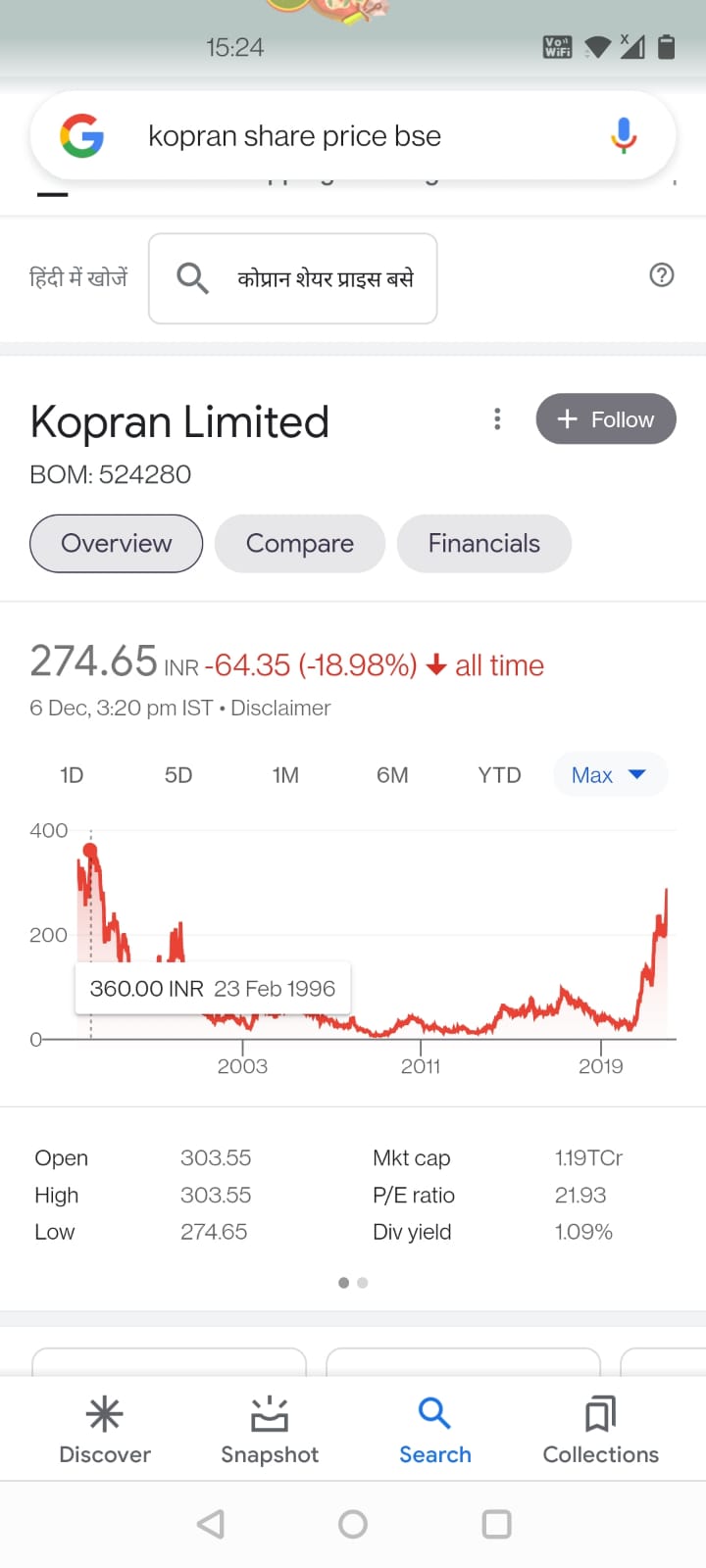

small correction here.Ath is around 370 that the stock hit in 1996.

3 Likes

Most of these sites/apps usually don’t have data from BSE,maybe Kopran listed on NSE around the year 2000 hence a different chart.There you go:

3 Likes

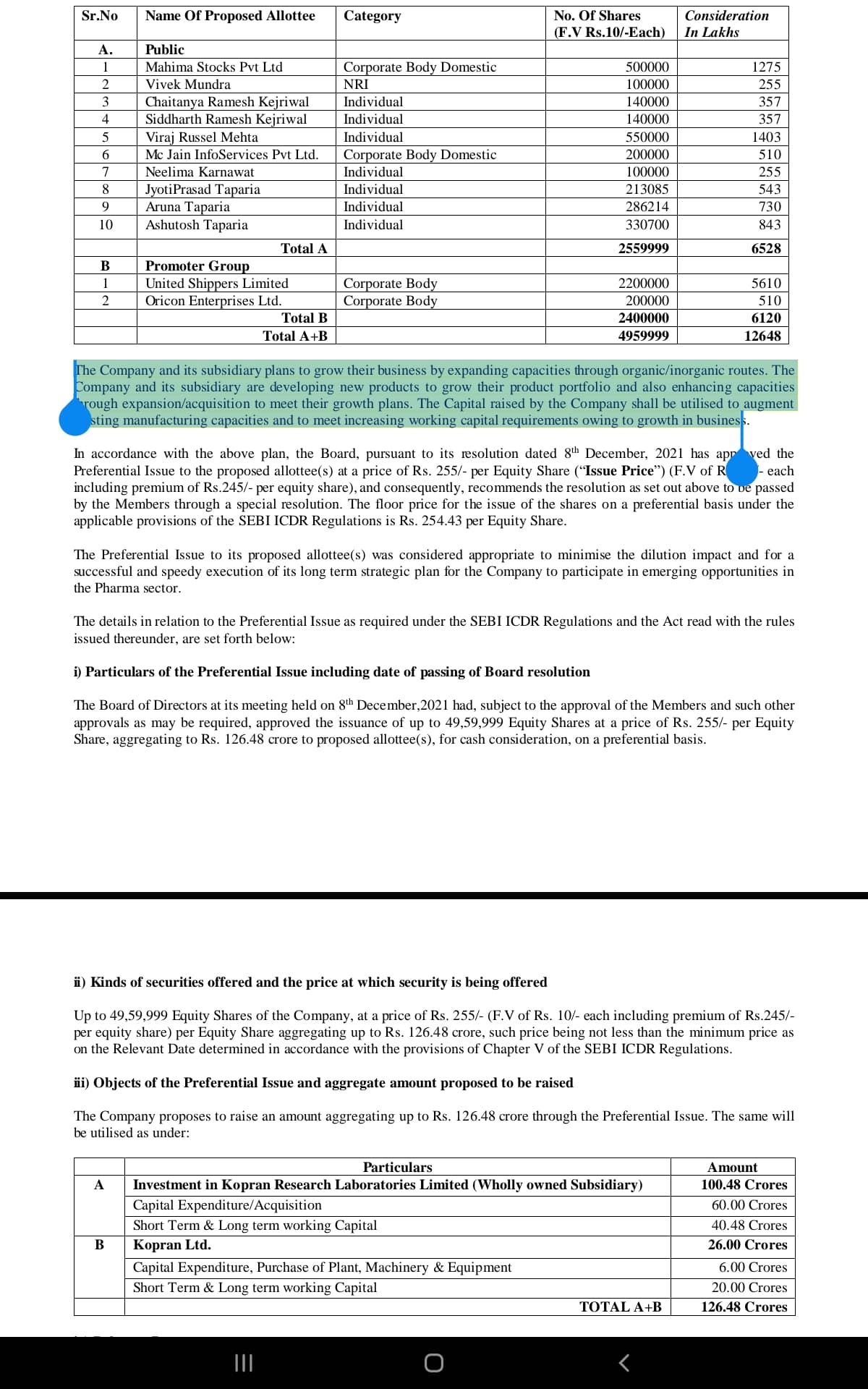

Promoters have increased the stake at Rs.255/share through Private placement.

| Total Shareholding | Promoter Sharholding | % Promoters | |

|---|---|---|---|

| Existing | 4,32,50,000.00 | 1,89,34,203.00 | 43.78% |

| Private Placement | 49,59,999.00 | 24,00,000.00 | 48.39% |

| Total | 4,82,09,999.00 | 2,13,34,203.00 | 44.25% |

7 Likes

Further to what @Pranshinv has posted above, amongst the non promoter allottees, are some interesting names. The Taparia family is the same one that sold contraceptive maker Famy Care to Mylan for $800 million, a few years ago. Infact, Ashutosh Taparia was India’s highest individual tax payer that year.

Another name, Viraj Russell Mehta is the brother of Mukesh Ambani’s daughter in law.

Some of the other names appear to be PMS clients of big known names. So all in all, a positive development considering the promoters themselves are investing another 61.2 crs at Rs. 255 a share to maintain their share holding in the Co.

19 Likes

Press Release

The Indian Patent office has granted Process Patent No. IN384085 for 20 years to Kopran Research Laboratories Limited, Wholly owned Subsidiary of the Company for the Active Pharmaceutical Ingredient (API) product NITROXOLINE, for the invention titled “IMPROVED, COST EFFECTIVE PROCESS FOR PRODUCING NITROXOLINE “

7 Likes

Question to fellow members:-

Does the Q2 revenue numbers reported by Kopran for Carbapenems i.e. 30crs - whether that is on 6MT annual capacity or 60MT annual capacity? I am struggling to understand whether the 900+MT per annum capacity has come on steam or the expanded capacity is yet to kick in?

EDIT ::

So going by this press release, the expanded capacity in APIs has kicked in but the API revenue in Q2FY22 vs Q4FY21 is flat. Can anyone explain this? Or the expanded capacities are not yet functioning to optimal level?

If they are not functioning at optimal level - is it due to the fact that product approvals for much of the sterile penems are currently under process and hence products are yet to go commercial?

3 Likes

Mahad Plant

Expansion in manufacturing capacity of API products from 474 MT/Annum to 924 MT/Annum at Plot No. K-4/4, MIDC Mahad, Tal.- Mahad, District - Raigad, Maharashtra has been completed as mentioned in Investor Presentation - Page No.8

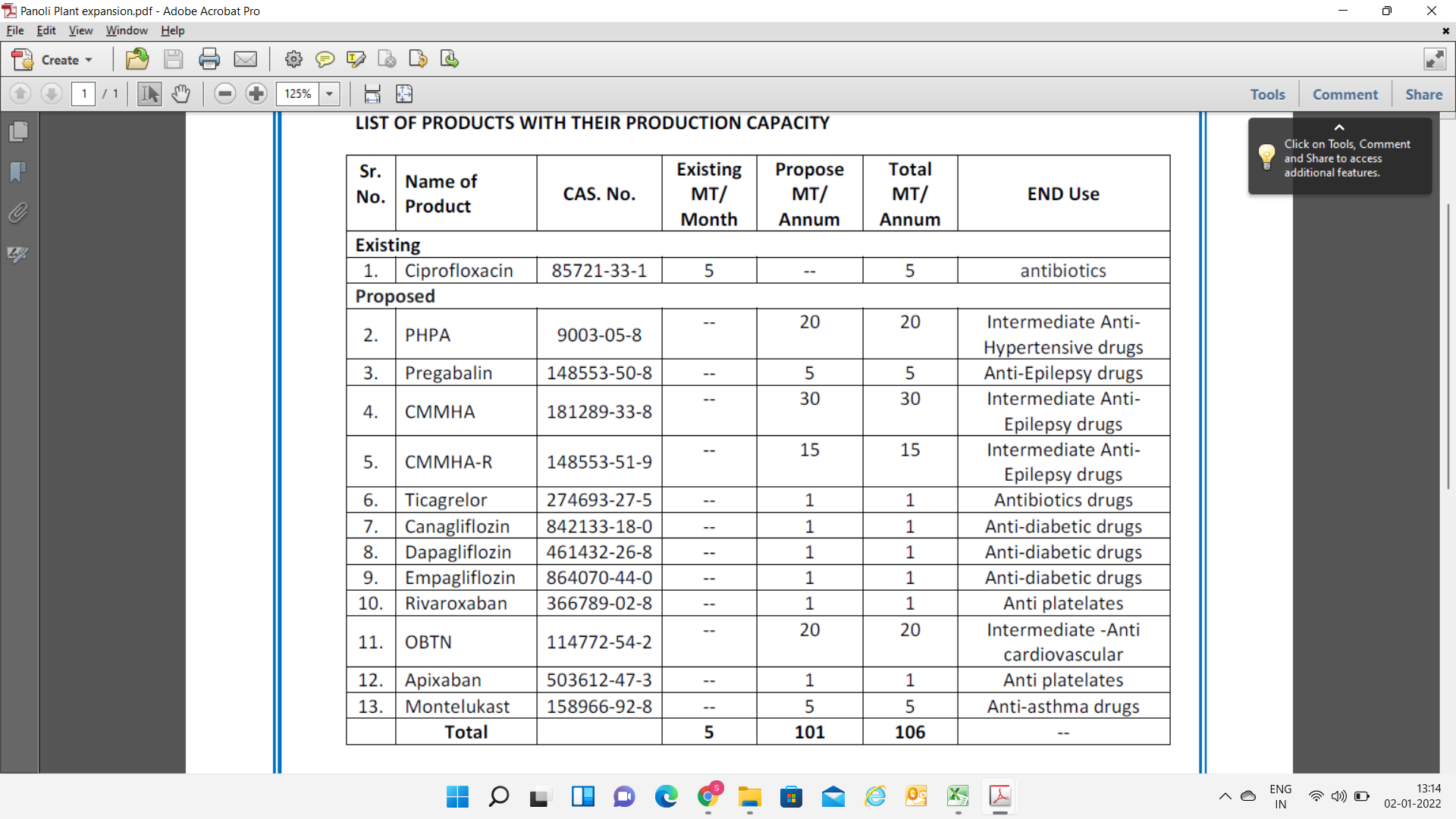

Panoli Plant

PROPOSED EXPANSION OF BULK DRUG & BULK DRUG INTERMEDIATE (5 MT/MONTH TO 106 MT/MONTH) IN EXISTING MANUFACTURING UNIT OF M/S. KOPRAN RESEARCH LABORATORIES LIMITED AT PLOT NO. 663, GIDC PANOLI, TALUKA ANKLESHWAR, DIST: BHARUCH – 394116, GUJARAT.

Expansion is commenced and expected to be completed by April 2022

Panoli Plant expansion.pdf (72.6 KB)

Once the plants run at their Optimal capacity , the impact will be seen in the revenue numbers

9 Likes

Hi @Pranshinv

- Could you tell us the date of Investor presentation which has the expanded mahad capacity details?

- Any idea how much additional revenue one can expect at full utilization of new capacity which has come online and panoli capacity expansion which will come online in Apr22.

Imvestor Presentation of Sept 2021 mentioned the fact that Mahad plant had completed expansion and updation .Panoli plant expansion will be completed in April 2022

1 Like

Kopran came out with December qtr results with its already high operating margins getting a further fillip, coming in at almost 21% (net of forex gains), perhaps an all time high. This high operating margin is perhaps what is steadily re-rating the stock.

The effects of the expansion are still to show in the numbers, but it is not unusual for expanded capacities to take some time to stabilize. The recent fund raise of 126 odd crs has changed the game somewhat. It will be interesting to know how the mgt. intends to deploy these funds, given the mgt.'s fixation on margins. The Panoli plant should be going on stream in the coming 3 to 6 months. Its quite likely that the Co. may be looking at some inorganic growth as well. It appears to be on track to do between 650 to 750 crs in sales in the coming year 2022-23. Hopefully, the investor presentation that follows the results would shed more light on this.

All in all, results in line with better times ahead going forward!

30 Likes

Notes from AR - FY 2021-22 and half yearly results for FY 21-22 iro Kopran Ltd -

- An integrated Pharma company committed to supply best in class Formulations and APIs. Formulations plant is located at Khopoli ( Maharashtra ). API plant is located at Mahad ( Maharashtra ). Company caters to over 50 regulated and un-regulated markets.

- Formulations - Mainly into oral solids and dry powder formulations for both penicillin ( anti biotic ) and non-penicillin based drugs.

Penicillin based finished drugs made by the company- Anti-infectives, Amoxycillin, Ampicillin, Cloxacillin, Amoxy Clauv

Non Penicillin based FDFs made by the company - Macrolides ( erythromycin, azithromycin etc ), Anti - Hypertensives, cardiovascular, Anti- helmentics ( anti worms… basically ), Anti-histamines ( anti allergy…basically ), EDS ( exceptional drug status… like tricyclic anti depressants ), Anti diabetic, CNS, Pain management and GI drugs. - APIs - company has dedicated and versatile facilities for manufacturing of - Atenolol ( beta blockers ), pregabalin ( anti epileptic ), various sterile and non sterile Cephalosporins ( non - penicillin based antibiotics ) and various Sterile Carbapenems ( beta lactic antibiotics ) , Macrolides and Urological APIs. Company is one of the leaders in Atenolol and Sterile Carbapenems.

New APIs under development / commercialised in FY 21-22-

Biapenem, Tabipenem, Faropenem, Imipenem, Ertapenem, Ticagrelor ( Anti-thrombotic ), Rivoraxaban ( anti-coagulant ), Apixaban ( anti-coagulant ), Empagliflozin, Dapagliflozin, Canagliflozin ( all three anti-diabetics )

- Last 5 yrs data starting FY 2016-17-

Sales - 318cr, 314 cr, 357 cr, 359 cr, 491 cr

PAT - 19 cr, 20 cr, 24 cr, 21 cr, 61 cr

Finance cost - 13 cr, 8 cr, 9 cr, 9 cr, 6 cr

Depreciation - 8 cr, 8 cr, 9 cr, 10 cr, 10 cr

- Last 6 months, segment wise API sales breakdown -

18 cr - anti hypertensives

19 cr- Macrolides

7 cr- neuromodulators

48 cr- carbapenems

9 cr- cephalosporins

14 cr - urológicals

Total 121 cr

- Geography wise formulation sales -

Africa - 30 cr

RSA - 38 cr

SE Asia - 9 cr

Others - 7 cr

Total - 84 cr

- PLI scheme commitment made by the company - 80 cr vs the current Gross block of 132 cr

- Other highlights -

Completed upgradation and expansion of Mahad facility undertaken during the last fiscal

Completed upgradation and expansion of solvent recovery plant

Expansion of non sterile plant undertaken by the company will be completed by Jan-Feb 22

Development of Panoli site expected to be completed by Apr 22

Disc : holding, tracking position, biased

14 Likes

2 Likes

Indirect proxy to KOPRAN… ORICON is increasing stake since now 18% from 13% in December quarter

It’s holding value comes to 250 crore at current KOPRAN’s price of 300

And promoters are increasing stake in ORICON too

7 Likes

Hoping something good we will be able to see in near future.

As per 19th March disclosure:

“The Company had raised funds amounting to Rs.126.48 Crore through Issue of Equity Shares on Preferential basis in the Month of January, 2022. As stated in the objects of the said issue the Company has made investment aggregating to Rs.100 Crore in the Equity Share Capital of Kopran Research Laboratories Limited (KRLL), by way of subscription to the Rights issue and accordingly, has been allotted 2500000 Equity Shares of Face Value Rs.10/- each at a premium of Rs.390 per share of KRLL on 19th March, 2022.”

Promotors has good faith in the company which gives confidence to us as well.

3 Likes

Lackluster Q4 by Kopran.

For FY22, slight de-growth in revenue and profits compared to FY21.

Decent Rs.3 dividend

Out of the net proceeds of preferential issue, the Company and its subsidiary Kopran Research Laboratories Limited had utilised Rs. 7521.59 Lakhs upto March 31, 2022 towards

purposes specified in the private placement offer letter. The balance amount of proceeds of preferential issue as on March 31, 2022 remains in fixed deposits/balance with scheduled commercial banks as interim use

of funds

@RajeevJ, Do you expect a turnaround in FY23?

https://archives.nseindia.com/corporate/KOPRAN_27052022153057_bmoutcome27052022.pdf

2 Likes

Some questions of my own.

Actually these questions are more to understand the balance sheet and cash flow situation better vs previous year.

I am a newbie as far as balance / cash analysis is concerned , so apologies for any stupid questions !

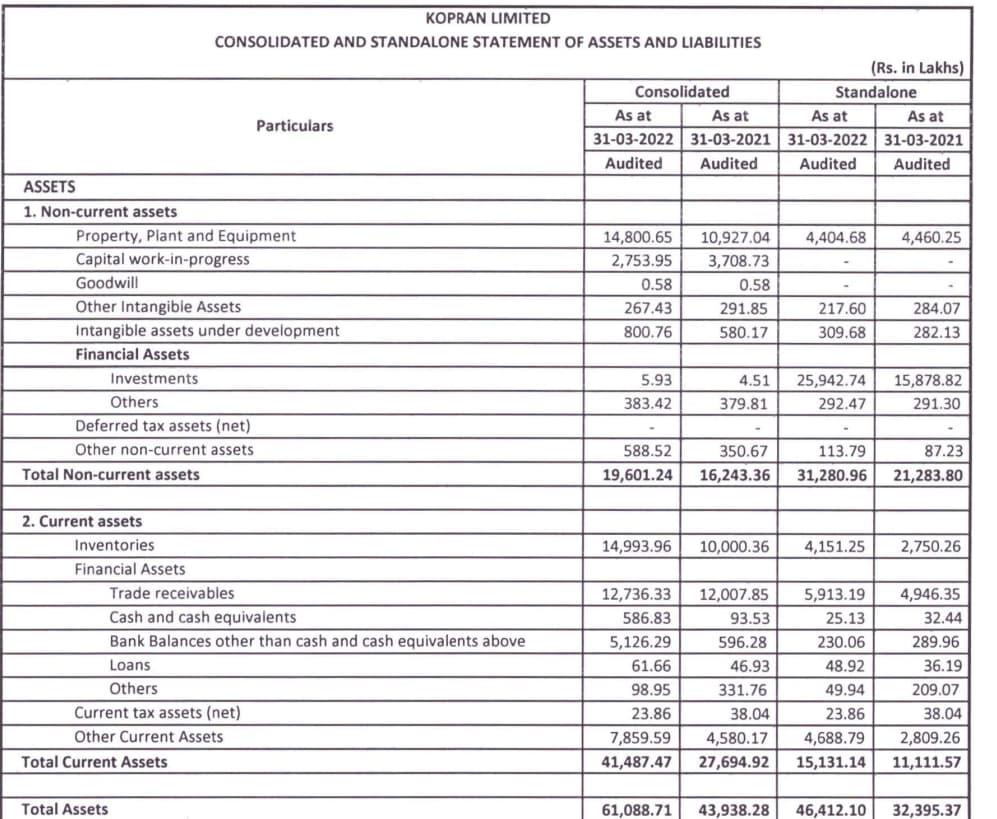

[Balance sheet]

- CWIP was 27.5 crs for FY21. Can we infer that it will be around 40 crs this FY ( I am referring to cash flow section - 'Purchase of fixed assets, including CWIP) ?

- ‘Intanglible assets under development’ has increased this year to 8 cr from 5.8 cr last year.

Can we infer this refers to IPR development? What would be the revenue impact of this item ? Does this give a new direction to the company’s efforts in coming year ? - Current assets have jumped to 149 crs vs 100 crs last year.

What can we assume from this huge inventory jump ? Is the company experiencing demand issues or is this just a fluctuating figure every year.

[Cash flow ]

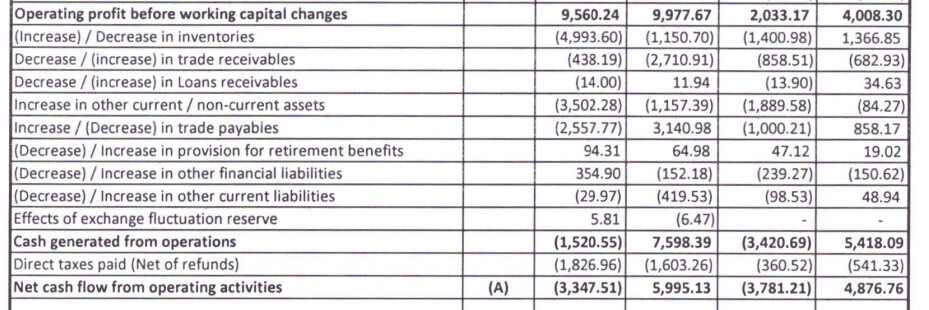

- Very large increases in inventory (basically quadrupling ) impacted cash flow negatively

- Net cash flow has drastically worsened to (844) cr this year from (252)cr year.

Should one not read too much into this or is this a worrying sign ( maybe this is fine in the context of the future expansion plans perhaps)? Maybe this is intentionally done for stocking purposes ?

Employee benefits have increased by 2 crs compared to previous year to 11 crs ( but this has probably increased last quarter itself, flat this quarter). Maybe this points to hiring rampup for the proposed expansion perhaps?

[Disc: Invested ]

Regards,

Abhijit.

3 Likes

Keeping in mind that Kopran is under sizable capacity expansion stage, Q4 to Q1 may throw better view, presentation will have finer insights but till then , here are some trends

-

Standalone performance QoQ ( formulations?)

Revenue up from 54 cr to 64 cr, GM shrank from 38% to 36%, despite that margins have gone up from 6.4 to 10.6% - indicates better utilization, better realization, something they are doing right. However this beinb low margins biz going high in mix is pulling down the xonsol margins. -

Consol - standalone (API and others) = Revenue flat QoQ 78cr to 79 cr , GM maintained above 50% in both Qtrs - OPM 29% to 27% - indictes holding GM and decent margins, Concern is flat Revenue QoQ - however if this is seen in sector performance view where many have reported degrowth in QoQ and margin erosion- this seems resilient.

Valuations when sector is kind of under stress( with narrative being generics pricing pressure in most con calls) is tricky affair in short term, however if Q1 was normal ( plant shutdown) PAT for year FY 22 would have been 70-72cr. Gives 15 PE at current mkt cap of 1050 cr- neither cheap nor expensive.

We will know further when presentation comes out. Pl note calcs above are approx.

Some other things worth keeping in mind is

- Fixed asset FY 22 is 150 cr+( 30 cr CWIP) , company asset turns has ranged between 3-4X. Capacities for 700 cr+ revenues are in place, including Mahad expanded facilities due in Apr 22 commission.

- Sizable cash raised in recent fund raise is deployed partly, near half is yet to be deployed.

- Current price is in discount to recent fund raise at 255.

- YoY looks flat but if one were to normalize Q1 22, 130-145 cr revenue and 17-20 cr profits has been a new base for qtrly run rate thus 10% topline and 15% profits growth FY 21 to FY 22 , with improving product mix, steonger balancesheet, new capex ready to contribute.

- Near 270 cr in Inventory( 150cr) and trade receivables( 120 cr)- ( last year 220cr) - inline with operations expansion and sizable inventory given supply chain issues.

- Dividend payout healthy- some may like it and some may not - reflects sound business ops from mgmt point of giew.

- Fund raise opportunistically during healthy matket times - different aspect of short term prices being down.

Mgmt commentary on growth outlook is key.

Invested

7 Likes

Wouldn’t it be cheap given the capex in place as you also have indicated in your post?