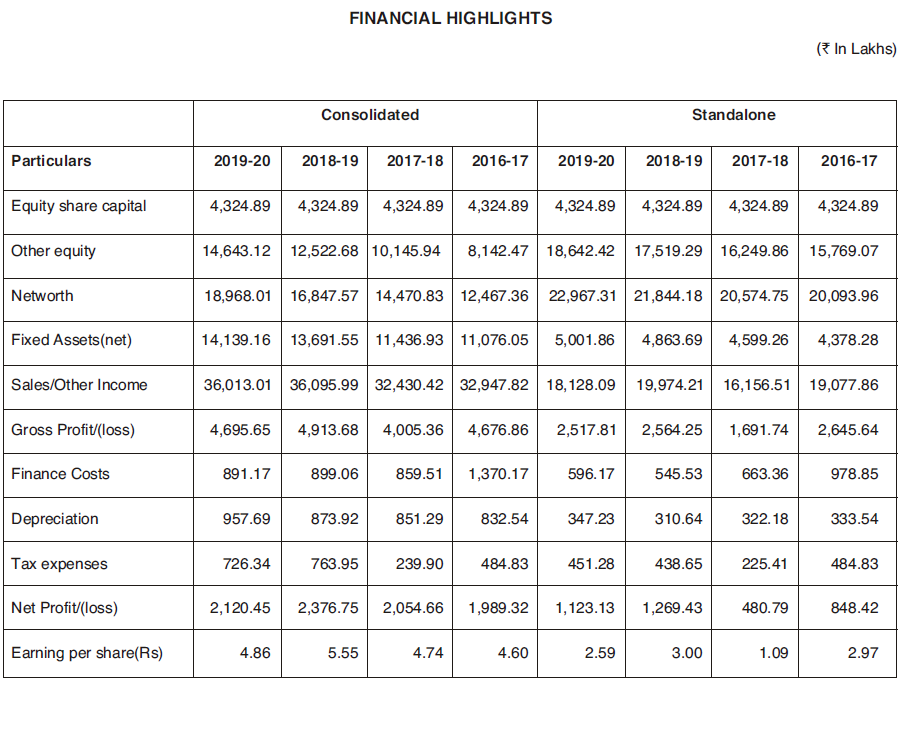

Kopran Ltd. is a pharmaceutical company operating both in Formulations as well as API’s. The formulations are manufactured at its plant in Khapoli & API’s are manufactured under its subsidiary Kopran Research Laboratories Ltd at its plant in Mahad. Together on a consolidated basis the Co. has been doing Sales of about 300-400 crs over the last 4-5 years with Profits of around 20 crs in the same period.

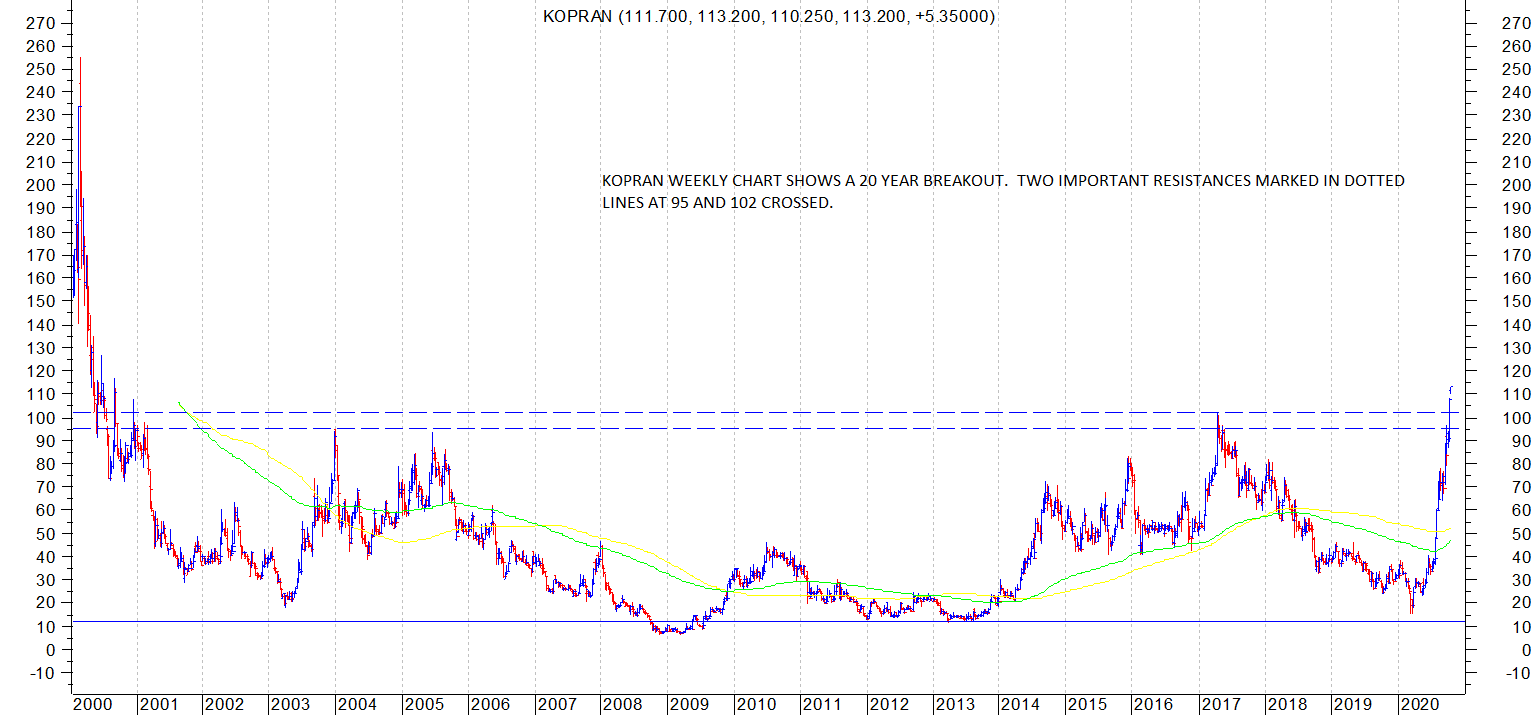

On the face of it, nothing very exciting, but taking a closer look at the numbers over the last few quarters suggest that things may be changing here.

The June quarter results brought the Co. into the limelight with a jump in both Sales & profitability at 120.88 Crs & 14.23 Crs. respectively.

The March qtr numbers were pretty good too, if one factored in the notional forex loss of 5.5 Crs in the qtr. The Co. could easily do a PAT of about 45 Crs, net of forex gains / loss with cash profits of about 55 Crs. for the year. The current market cap of the Co. is about 392 Crs.

Numbers aside, with recent tensions with China, the Govt. has decided to give a huge thrust to the pharma sector to reduce our dependence from Chinese imports of APIs. It has announced investments of Rs. 10,000 Crs to incentivize the production of APIs in India. Discussions are on about making this even more attractive to encourage pharma companies looking to relocate from China to set up shop in India.

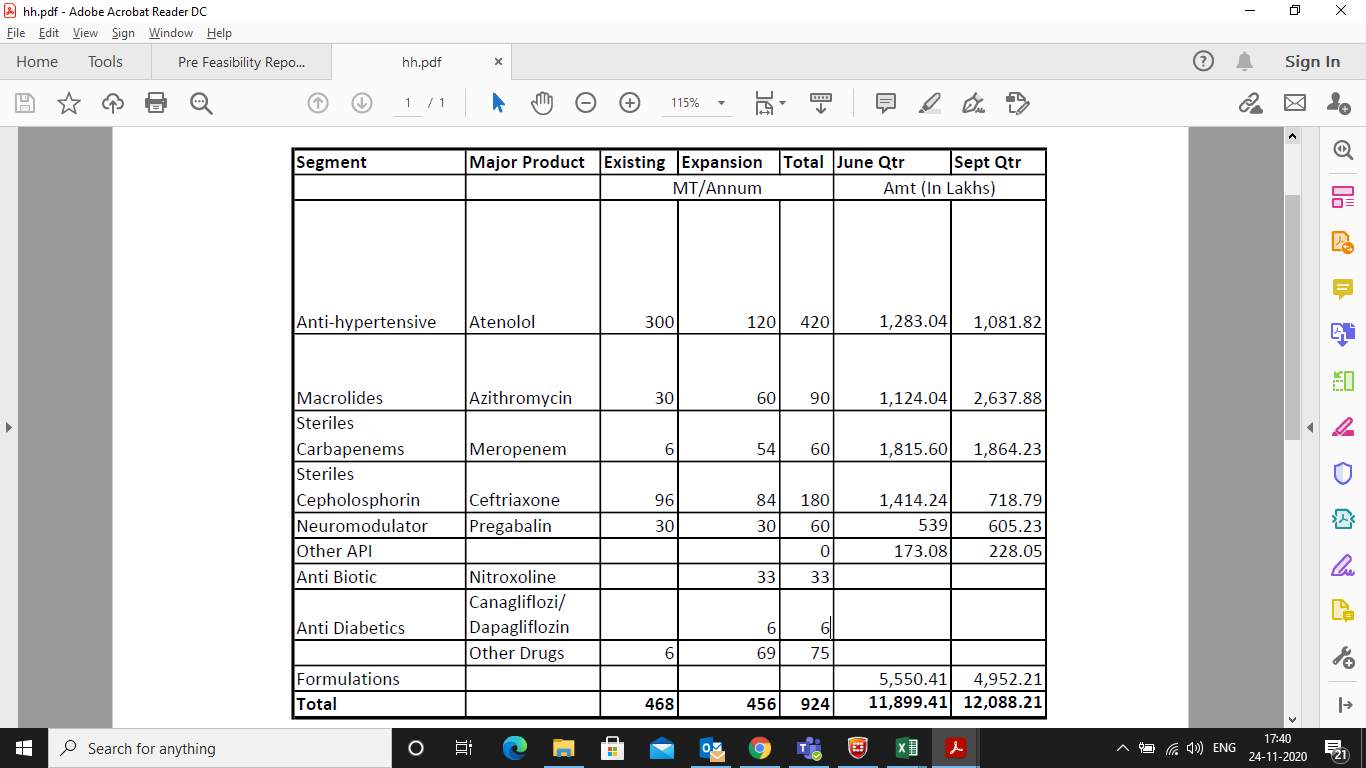

There has been a lot happening within the Co. over the last few quarters. The Co.’s API facility at Mahad was inspected by USFDA in January 2019 without any observation under Para 483. The Co. had filed the DMF of Atenolol which has been approved by USFDA & the Co. is in the process of commencing supplies of the API Atenolol to the US in the current year.

The Co. has also received the approval of Pragabalin from EU-GMP & will be able to market the API in Europe. Further it has filed for USFDA approval for Pregabalin & Azithromycin.

New products like Nitroxiline & Ticagrelor have been commercialized.

The Co. is gearing up production of both APIs & formulations & expanding its portfolio. The API plant in Panoli in Gujarat which the Co. was trying to acquire got delayed by a year, has finally come about & will give a further fillip to the scaling up of API business.

It is also reliably learnt that the Co. is in advanced stage of closing a couple of deals for contract manufacturing. Mgt has been paring down debt (about 77 Crs as on March 31, 2020) over the last few months. This will further improve the ROCE which based on the current year’s performance would be in the range of about 24% for 20-21.

Concerns: Kopran has been around for as long as I can remember, & has not done anything to write home about in all these years, so could this be a false alarm? Though in all fairness, the Somani family which are the promoters, have been having their own family restructuring & with the ownership issues now settled, the focus can shift back to the business of running the Co.!

Disc: Invested