Recently started studying Kopran, Comparing the last 3 Quarter Presentations (Slide 7 - Product Pipeline):

1 . Faropenem Commercialization is completed as shown in Q2 but in Q3, it is showing that it will be commercialized in Q1 FY22.

2. Ticagrelor Commercialization is completed as shown in Q2 but in Q4, it is showing that it will be commercialized in Q2 FY22.

Not sure if this is supposed to be this way for some reason, if someone can enlighten me on this, that will be really helpful.

Update from company on state of expansion ( and covid impact):

“Kopran Research Laboratories Ltd., a wholly owned subsidiary has undertaken expansion and upgradation of various Plants at its Active Pharmaceutical Ingredients facility at Mahad since March 2021. Due to the onset of the second wave of the Pandemic, the expansion work was delayed, especially because of non-availability of Workers and Industrial Oxygen. The expansions of two Plants were completed by April 2021 end and resumed operations. The expansion and upgradation of the Sterile Plant was completed and operations resumed by June 2021 end. Due to the above, there would be an impact on the results of Quarter 1 of FY 2021-22.”

So there should be a positive impact ( correct me if my interpretation is wrong here ! )

[Disc: Invested ]

Yes, in both the cases, the word “resumed operation” is there, which means operation was suspended. But for how many days operation was affected, was conveniently not mentioned. So do expect some hit on profit for QTR 1, but how much, is a matter of one’s own conjecture.

The Company has announced that the expansion / upgradation of various plants at its API Unit at Mahad have been carried out & completed in June, so Q2 should see the full impact of the expansion. Markets are forward looking & do not like uncertainty & with the mgt. clarifying that the expansion having been completed, any fall in Q1 Sales will be taken as expected.

The Kopran mgt. keeping investors updated with the developments is a refreshing change from the past. Expect incremental growth in Sales & Profits in both the current year 2021-22 as well as the next 2022-23 with operating margins better than many of its illustrious peers. Something that has gone relatively unnoticed is that Kopran has given a payout of 28% of profits as dividends for the year 20-21, despite ongoing expansion.

All the boxes are gradually being ticked & it is only a matter of time that the Co. gets its due on the bourses.

I have ben an employee of Kopran two decades back (during their hey days)

The company at onetime was the second largest exporter of pharma from India

It was also amongst the first or second to have approvals in UK, and South Africa. Considered one of the difficult markets in the 90’s (from entry perspective)

In OTC they had a very successful entry with the SMYLE range of products

However one of the main issue was financial / governance

They were rumoured to have dealing with Ketan Parekh and leading to quite some MTM losses in the " investments"

Corporate governance needs to improve for long term investors feel confident

They had warned of bad results with those notifications of delays in expansion and upgradation, leading to plants resuming operations later than expected.

Unfortunately there are no notes given here so we don’t know if the impact was only because of those delays, or other factors that have been affecting many pharma players in the last quarter like increasing shipping costs, destocking by customers and dumping of excess supply from competition.

I sold out at about 250 a couple of days before the result. Will likely buy back on Monday if there is more fall.

Kopran came out with June qtr numbers which were impacted due to plant shut down as intimated by the Co. in advance. The June qtr in any case is always the weakest qtr, except for last year, when I gather that some of the previous Q4 sales had been carried over to Q1.

With the expansion having been completed, the Co. is in line to do average quarterly Sales of about 150 crs. which should give a PAT of about 22 crs for the quarter & a yearly profit of about 90 crs. Not to say that profits for 21-22 will be 90 crs, due to a weak Q1 as mentioned above, but markets are forward looking.

With the new plant at Panoli expected to go on stream by the end of March 2022, the Co. is expected to do average quarterly sales & PAT of about 200 crs & 31 crs respectively. For the year 22-23 the Company is likely to generate sales & profits to the tune of 800 crs & 125 crs.

The market cap after the recent correction is about 926 crs. While a further correction in the short run cannot be ruled out altogether, the stock appears to be reasonably valued at current levels & perhaps presents another opportunity to enter for those who missed out earlier. The mgt. has been particular about not diluting margins for the sale of growth.

Hi @RajeevJ

How did you arrive at these sales and PAT numbers for FY22 and FY23. Has the co. given any given any idea about how much capacity they have added recently and how much it will be adding with Panoli? Dont find it in AR or result updates.

I had done some deep dive scuttlebutt from distributor of generic pharma agency, first told me who is making real kopran dont know, i asked why ? they told me first antex pharma pvt ltd is third party makrketing than after some time raja antibiotics also doing same thing , it doesnt so much concern frequent change might be questionable .

now from other distributors i make question , they told we dealing in kopran

2 years ago and not doing now , distributors answer frequent change in CNDF and not proper distribution delay in transportation .

now last but not least in generic kopran had no any brand power.

this my two cent , its only opinion , happy investing.

disc.not sebi register, not a any position in this stock.

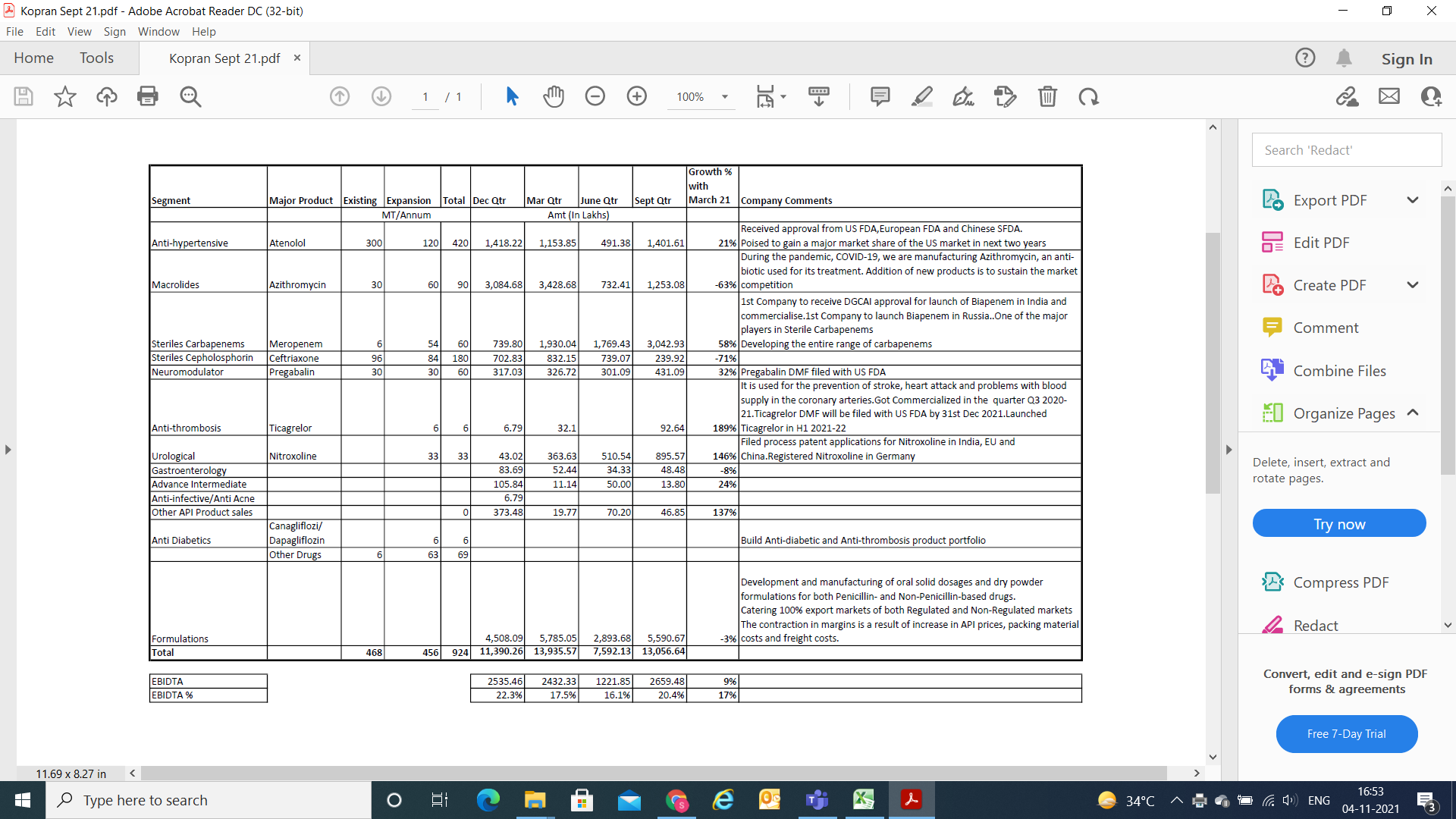

EBIDTA margins have improved in current quarter which should be mostly due to new products (i.e. Carbopenems). Expansion is converting into numbers and Atenolol (Anti -Hypertensive) is ready to fly in the near future.

Steriles Carbapenems and Atenolol increase in sales has absorbed decrease in sales of Azithromycin (Covid 19 drug) which indicates that from here onwards the investment in Capex is ready to give results.

PLI Scheme - Capex Commitment of 80Cr

The expansion of Non-Sterile plant undertaken by the Company will be completed by end of January 2022.

The development of Panoli site has commenced and is expected to be completed by end of April 2022

Possible triggers on timing as new regime may come in soon ( given that a sizable expansion has been recently completed).

Last month turbulence in broader market didn’t affect it much and has been on tear after taking out life time high with good volumes. Took out 20+ years all time high of 250+ recently. Stands out in pharma pack both in improving fundamentals and technical on charts.