Kopran is beginning to come on the radar and is being covered by a few brokerages now. The note/ update below is from one of them- Sunidhi.

Kopran Ltd (CMP ₹189, M. Cap ₹8bn): - Expanding wings

Company Update

Kopran is a Mumbai-based integrated Pharma company that generates ~ 58% of revenue from APIs and 42% from the formulation business (9mFY21). The exports of APIs and formulation together contribute ~80% of its revenue. Its formulation business is operated through Kopran Ltd and APIs vertical is run by a WoS- Kopran Research Laboratories Ltd (KRLL). The company has shown strong performance during recent quarters on the back of a larger products portfolio, focus on niche segments and geographical expansions. It has built dedicated and versatile facilities for Atenolol, Pregabalin, Cephalosporins (non-sterile & sterile), Macrolides, Sterile Carbapenems, which are witnessing healthy growth worldwide. The strong performance of company may sustain going forward on the back of an attractive products pipeline backed by up-gradation of facilities and a larger presence in the US and Europe. An improved business outlook (focus niche products and regulated markets) augur well for growth of the company over near to medium term. The stock is currently trading at 12.5x/10x FY22E/FY23E EPS.

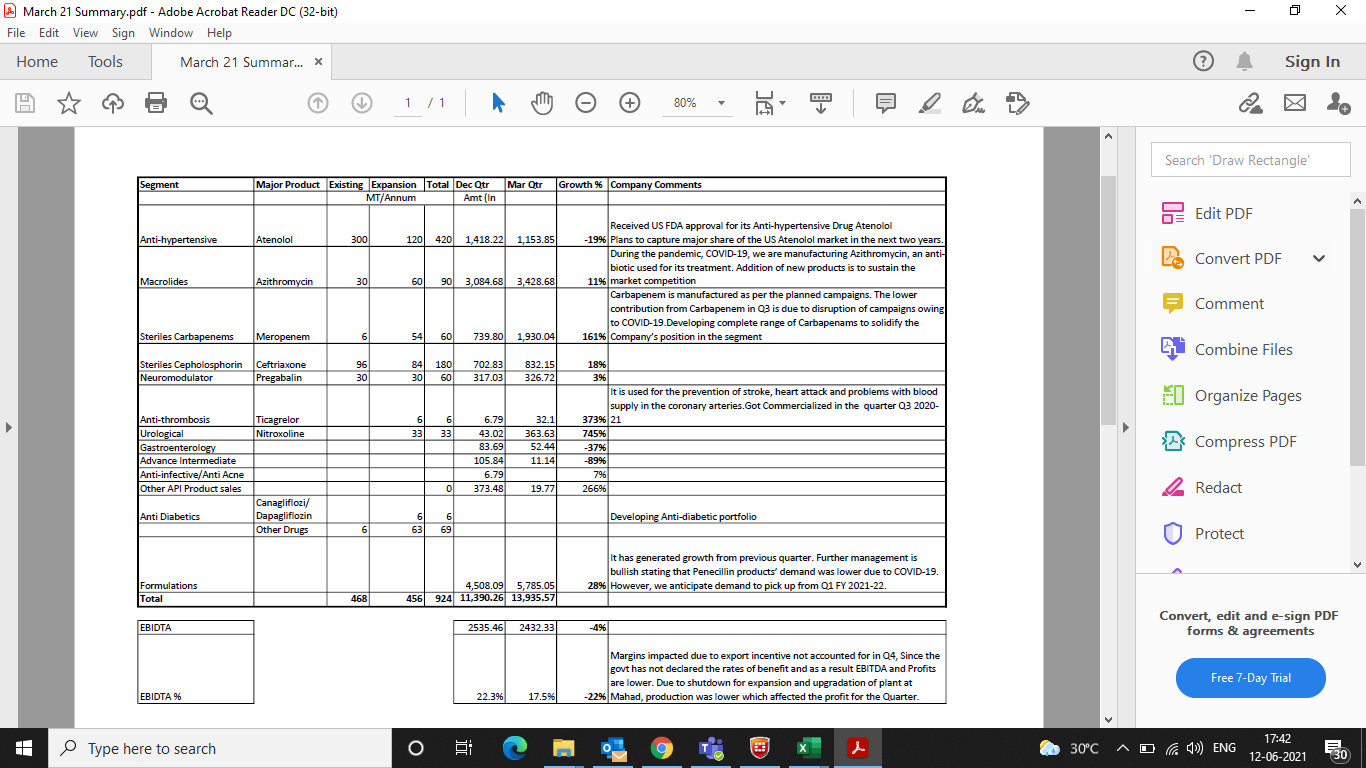

Strong pipeline in API vertical to drive revenue and margins: Kopran’s API business grew at a CAGR of 25% during FY19-21 on the back of new products, geographical expansions, and focus on niche segments. It has fast expanded its products portfolio (4 DMF filed in FY21 itself out of a total 9 US-DMF) for bigger markets like the US and Europe. The company got a strong fillip in the US after a recent launch of Atenolol and it aims to gain market share in the next two years. Besides, it holds 4 CEPs for the European market, 2 product filings in China, and multiple registrations in emerging markets. However, its pipeline in Carbapenems (5 new products to be rolled out during FY22 & FY23) and foray into next-generation anti-diabetic drugs also provide strong growth visibility going ahead. The company also built a pipeline in anti-coagulants and anti-thrombosis. Koprans’s API business is expected to reach Rs3.87bn in FY23 from Rs2.87bn in FY21 (CAGR of 16%), even after building lower sales in Azithro.

Expansion in key API facilities: The Company has been expanding and upgrading its facilities in a calibrated manner over the past couple of years and currently it is undertaking the up-gradation and expansion of 3 blocks at the Mahad facility to cater to the increasing demand of existing and new products. Besides, it is also developing the Panoli site as an intermediate facility, which is expected to be operational by Q3FY22.

Formulation business to see faster growth post normalization on COVID-pandemic Kopran has dedicated facilities for penicillin and non- penicillin-based formulations which mainly caters to the African continent (~80% of formulation business), wherein it participate in local tenders. Its current basket includes 20 dossiers in Africa & French West Africa, 11 dossiers filed in South East Asia, 25 dossiers filed in Latin America. The performance of this vertical is expected to improve after the normalization of the pandemic. The company is eying to expand business in UK and Canada through contract manufacturing opportunities.

Focus on a niche and larger products basket to help improve EBIDTA margin

Kopran reported an EBIDTA margin of 16.6% in FY21 from 11.6% in FY20, thanks to favorable pricing in some of the products like azithromycin and higher offtake. Although the pricing in some of APIs may see softening going forward, niche products- especially carbapenem and anti-coagulants and next-generation anti-diabetic drugs may help sustain EBIDTA margin in FY22 (16.6%) and FY23 (~17%).

Multiple triggers for growth and improved financial performance

A strong products pipeline in API space focus on better margin products and expansion in regulated markets are some of the elements which should lead to the improved financial performance of the company in the next 2-3 years. Its sterile API facility is currently approved mainly for RoW markets, though the company aspires to get into regulated markets. The regulatory approvals of its sterile facility by the US regulator would be a key milestone for the company for future growth opportunities. The stock is currently trading at 12.5x/10x FY22E/FY23E EPS.