@RajeevJ the most important factor for investment in Kopran is management focus or change in intentions i.e. what has changed in past 2-3 quarters that they were not able to implement in past so many years?

Have u got a chance to interact with the management and get some insights on this?

I had mentioned while initiating the thread that the Co. / Promoters had not done anything worthwhile over the last many years as a “concern”. In such cases, rather than stay on the sidelines with suspicion, it is perhaps better to take a small initial position. With skin in the game, one tends to track the investment more meaningfully.

The Kopran growth story has only just began, & is giving enough opportunity to investors to come on board at every level. Expecting an even better Q3 shortly. At some point next year, the new plant as also the expanded capacity would go on stream taking care of further growth. For me its a three year story.

The Kopran Q3 numbers were more or less in line with expectations. The important feature is that the operating margins continue to inch higher in each subsequent qtr. Sales growth is expected starting next year 2021-22 after the effects of the ongoing expansion come into play.

Increased sales with constantly increasing operating margins is in short the main investment thesis in Kopran. These increased margins are a result of both backward integration as well as increased sales to the developed markets where margins are higher. The Co.'s focus continues to be towards increasing approvals for new molecules in the US & Europe. Hopefully the Co. would give an update / presentation as it did after Q2 numbers.

The next 12-18 months could potentially take this Co. into a different league.

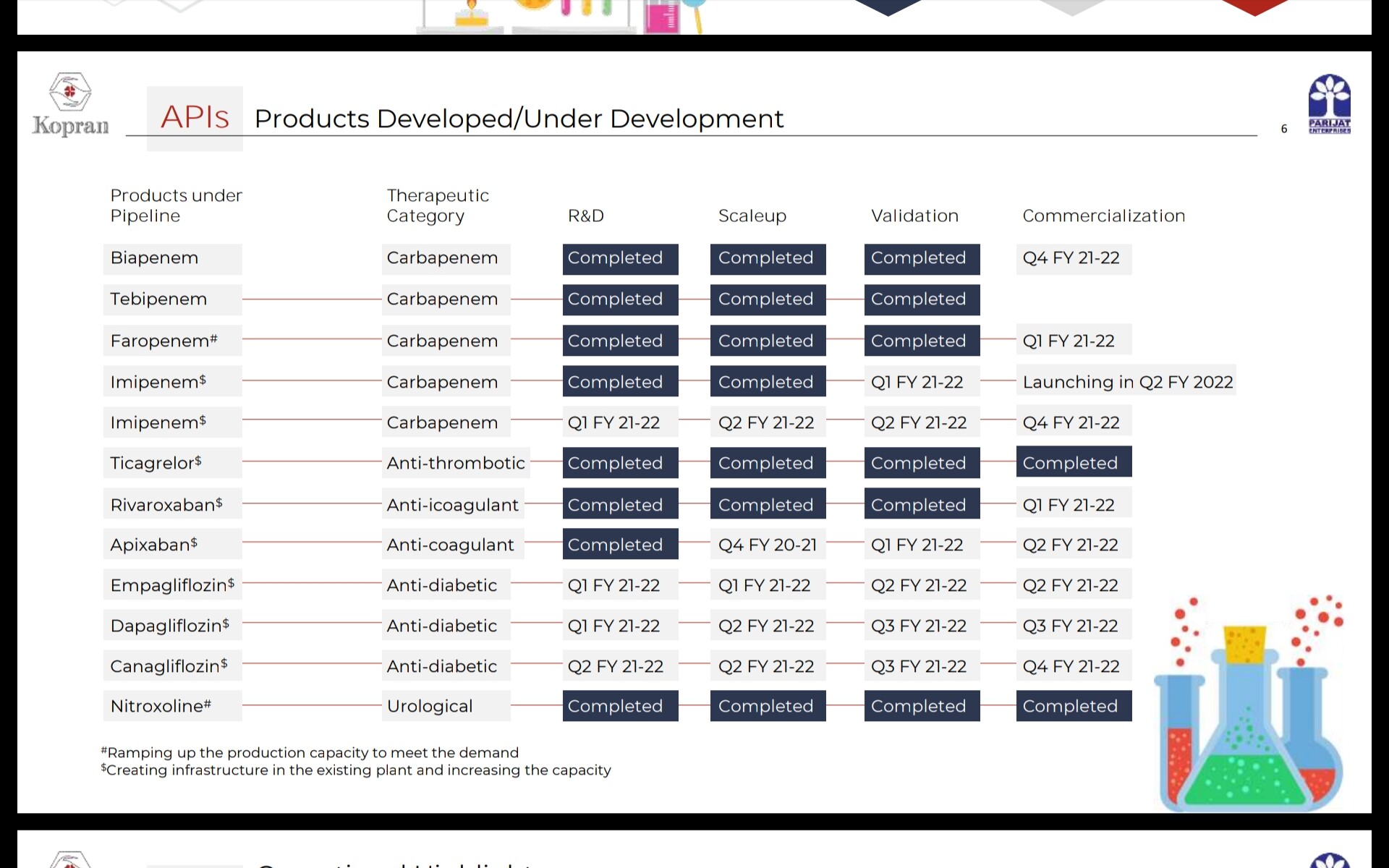

Q3 deck - quite elaborate and like the fact that they are highlighting QoQ and acknowledged misses( could have easily done YoY and show a rosy picture)

API QoQ performance- sterile carbepems were called out for reason for drop on revenue,

anti hyperintensive - alenotol is where they are aggressive in US mkt, QoQ growth 40%

Export grew QoQ from 46 to 49cr, higher margin mix

API vs Formulations 68 cr to 45 cr

for API focus is developed geographies ( alenotol called out) - higher margin front

Formulations- focus seems to be non regulated countries( except UK) with 90% of dossiers filed there, primarily Africa and LatAm- which is tender dominant market( likely using API infra in regulated market to extend to Formulations and thus cost advantages and synergy with decent margins)

Formulations flat QoQ at 45 cr- Africa is 80% of revenue

Valuations- at current qtr runrate they will end up with EPS around 14-15 range, sales in vicinity of 500 cr. DEBT/ equity have come down to 0.29. Market cap is still 550 cr type. Ratios look respectable( RoCE etc). Re rating is imminent with sector tailwind and industry peer average valuations.

to watch out for - Regulated mkt growth, any lumpiness in revenues( both broader geographies and product basket base , this will not be likely case), continued momentum in Atenol - anti hypertension, tender success in non regulated market

Thanks to @RajeevJ for bringing this to the group.

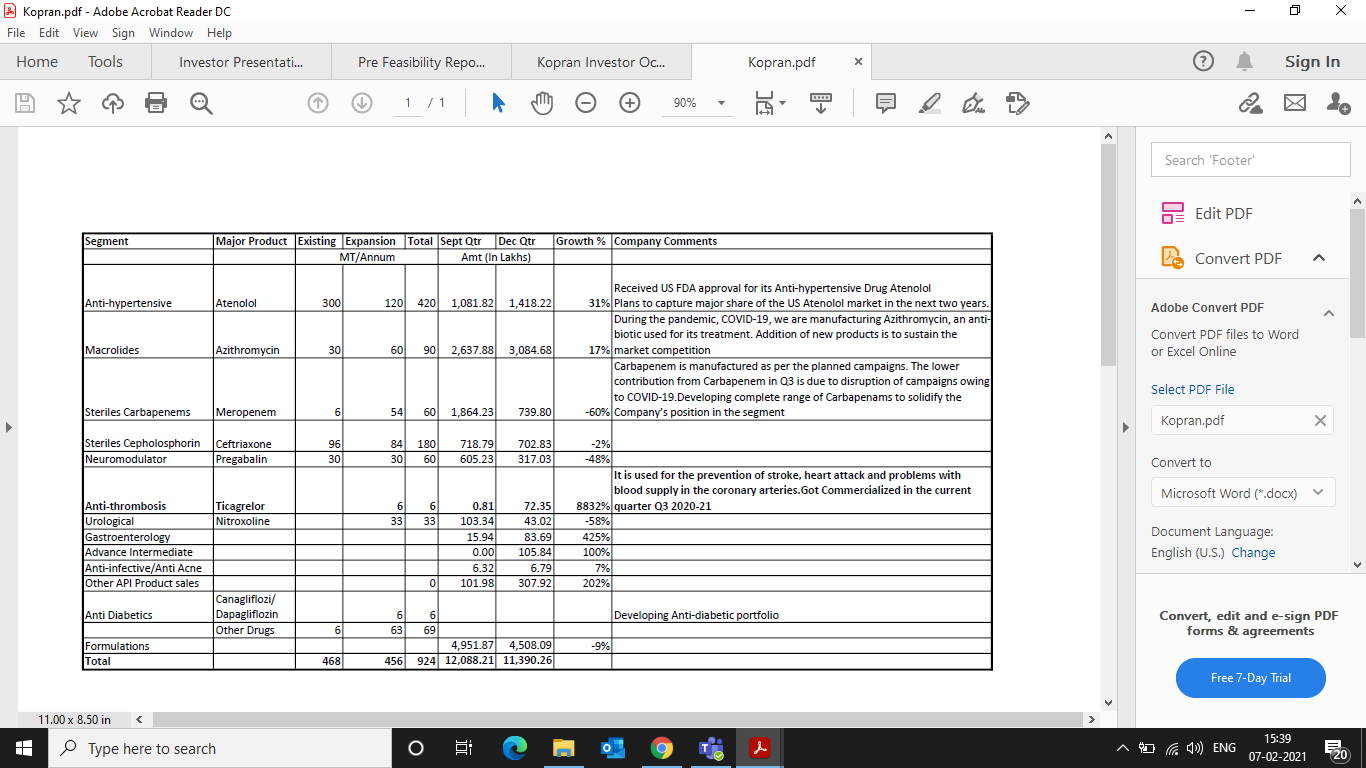

Key Triggers Ticagrelor, sold under the brand name Brilinta among others, is a medication used for the prevention of stroke, heart attack and other events in people with acute coronary syndrome, meaning problems with blood supply in the coronary arteries. (Source : Wikipedia)

Company has commercialized the Sales in the quarter Q3 2020-21 which is visible from

investor presentation . Athenolol - It is shown growth of 31% from the previous quarter which means it is getting very good response from US Markets .It substantives from increase in Export Sales . Kopran.pdf (441.1 KB)

Mar 2020 PAT was 28 cr

Trailing 12 months PAT is 70 cr

Source: screener.in

Profit growth is 117% for the past year, something definitely is up. I believe their formulation and API business in Africa is picking up. With multiple new molecule launches coming PAT and sales should increase.

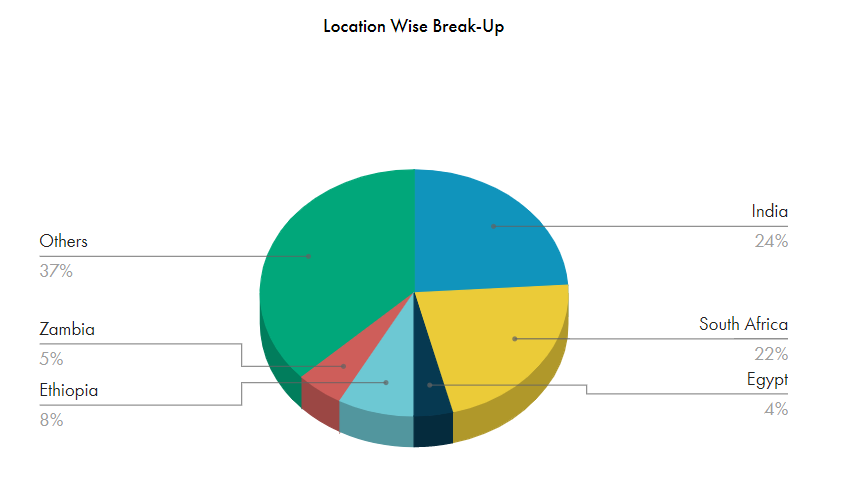

The closest comparison for Kopran I can make is Granules. Both are generic formulations and API businesses but catering to different markets. Kopran is more into Africa and EMEA while Granules is US heavy.

Disc: have a tracking position, accumulating a small position

Kopran’s main market is Africa with 39% share as per last earnings.

Since Kopran doesn’t deal with USFDA and African countries drug agencies are not as uptight as USFDA can I assume the regulatory risk to Kopran’s business is very low compared to other bulk drug and formulation manufacturers?

Lot of these API companies are going through a cyclical upturn given the challenges around China - that is why the margins are up across the sector whether the companies do specialty products or not. Anyone’s guess how long this lasts. Only the very good cos will be able to maintain the profitability growth after the tailwinds are gone. See what happened in the paper sector a couple of years ago. So bear that in mind while you are looking at the current margins.

Kopran’s Investor presentation given after the Q3 numbers is pretty detailed. This is the second successive presentation after quarterly numbers. The mgt. is now willing to share its future plans / targets with specific timelines. This is certainly a big positive. Not sure how many Co.'s of Kopran’s size are doing this. The other important benefit of these presentations is that we investors get a definite idea if the mgt. is indeed walking the talk. If indeed they are then it exudes confidence in the Co. / its mgt. We will know better as the next few quarters unfold.

The presentation mentions about the plant shut down in the current qtr (Q4), but also mentions that Sales will not be impacted. I understand that its expansions (other than Panoli) over the next couple of years will be brownfield in nature as it has sufficient land for the same, so the expansion will be faster with the basic infrastructure in place leading to higher asset turns & faster/ better returns. The Panoli plant too will become operational in the coming year (2021-22). It will be interesting to note if the increased sales are accompanied by increasing margins as well. Investing after all is all about growing with the growth of the Co. that we invest in. If growth seems sustainable, it will make sense to scale up our bet as well. On the other hand if growth falters, we have the option to take the call to exit.

To me the story looks sustainable, but only time will tell!

Sorry, I have not tracked this business in detail to be able to answer this. my comment was a general statement rather than a comment on Kopran margins though my view is that current margins of almost all API cos. have some element of tailwinds and most of them are likely to see some compression going forward - degree will vary depending on specialization in product portfolio and end markets (regulated vs unregulated). If you find Kopran margins are lower than peers, most likely it is because the specialty portfolio may be smaller. BTW, given Kopran caters to unregulated markets, especially Africa than the risk in those markets is higher and hence Ideally margins should be higher and not low. Just to give you an anecdote to give you an indication on the tailwinds in the API businesses - a few years back no pharma company wanted to even consider backward integrating by getting into API. If an API business was put up for sale, there would typically be no acquirer. But currently the scenario is reverse. Macros have changed because of geopolitical and other reasons not purely because of sustained demand increase. So need a better handle on that situation to judge API businesses at the moment. I am not an expert on pharma businesses - so dont go by my views - but sharing the facts am aware of. But do more work on the overall macros driving the API market and its sustainability.

Yes and when the GOI encourages you to set up anything Pharma under the PLI scheme, everyone will rush to buy an existing plant first and then try greenfield one(this takes time).

If the China + 1 is really sustainable(i believe it is) and the GOI doesnt go back on its word on PLI, then it is at least a good place to be stock wise. The USA FDA raids on Indian pharma(i paraphase) on the quality front may prove to be a blessing because when the pandemic struck, most plants were fixing their hygiene and FDA observations and buyers were at least comforted knowing that plants were inspected.

Bulk low end API is good overall from a country standpoint from a diversification and self sufficiency view; on a investing metric,not so much, especially multibagger ideas and visions of making it big.

net, net, as long as China virus is kept in the news and China continues to make itself the enemy of the world, the odds are in Indian Pharma favour

India azithromycin market is expected to grow at a steady rate during the forecast period. The India azithromycin market is driven by the supportive government policies and schemes that are promoting the manufacturing and development of drugs, intermediates and active pharmaceutical ingredients in the country. This will not only improve the status of local manufacturers but also help India in becoming self-sufficient. Additionally, the widespread use of the drug in various conditions such as middle ear infections, sexually transmitted infections, pneumonia, Lyme disease, skin disorders and a range of respiratory infections & diseases is further expected to boost the demand through FY2026.

Azithromycin contributes 27% of revenue of Kopran for quarter ended 31st December 2020.They are tripling the capacity of Azithromycin from 30 MT/annum to 90 MT/annum.