I was recently on a webinar where the head of one of India’s prominent Asset Mgmt cos said that real estate as an investment is pretty much dead…

2 Likes

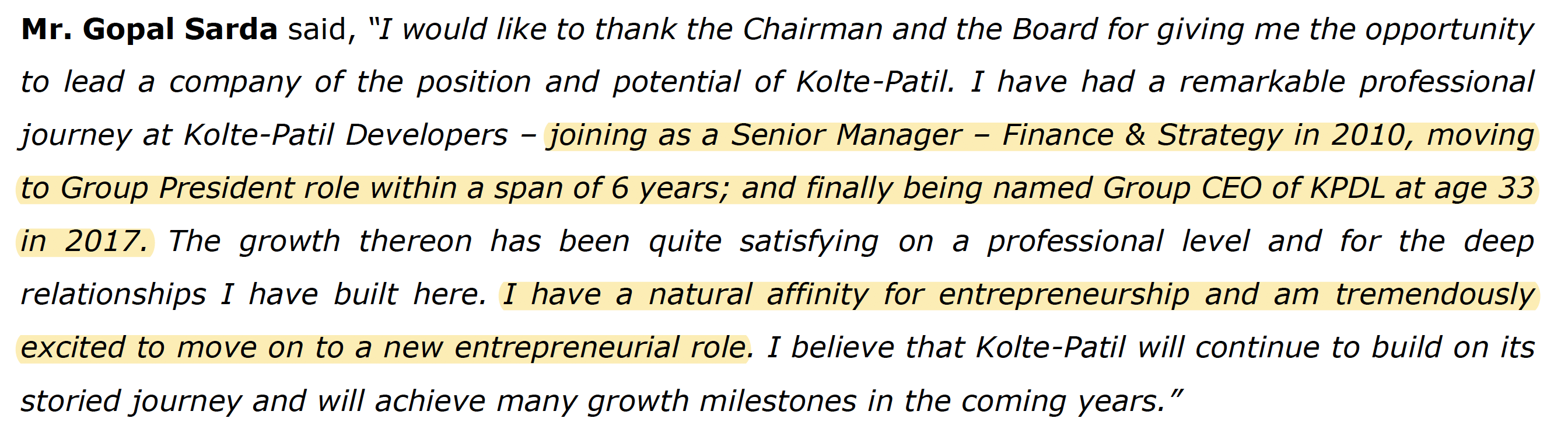

Gopal Sarda has resigned as the Group CEO of the company.

He was a good capital allocator in kolte-patil. Hope company gets a good candidate!

Not a good exit per se.

Do you see any red-flag?

D: invested

1 Like

A few observations:

- Gopal Sarda seems to be starting his own venture

- The new CEO (Yashvardhan Patil) is young (30 years) and is the son of Rajesh Patil (Chairman & MD of Kolte Patil). He has been involved in company operations since 2012.

- Kolte Patil as a company likes to bet on fresh blood, Gopal Sarda was made CEO at 33 years, now Yashvardhan Patil has been made CEO at 30 years.

Disclosure: Invested

5 Likes

Note he is son of Rajesh Patil (promoter founder of Kolte Patil)

One more theory that i can think of is:

Yashvardhan Patil finished his studies and got experience and maybe he was getting prepared for this role all these years. As he was being groomed, Promoters for CEO’s from outside and now that Yashvarshan maybe able to handle the role of CEO. Promoter group may not need any outside CEO.

Again, note that its just a abstract theory in my mind. Happy to discuss!

1 Like

Thanks a lot Harsh for highlighting. The worrying part is not Mr Sarda resigning but this disposal. I bought it a few days ago only. Might have to re evaluate the decision

What were the reason / assumptions / outcomes that you had in mind when you bought the stock

How that has changed … that should decide whether to own or sell any stocks??

If CEO was the whole and sole reason for owning the stock then you should sell it right way … If not then it is better to wait and watch and check development that are taking place …

Kolte Patil stock price is less than what is was in April 2015 & Jan 2008 … This is probably true for many Real estate stocks

CEO changes have hardly made any difference as sector was under stress .

Last decade would have been wrong time to make Promoter Kid CEO … but now just when sector seems to take off - they have made him CEO … so that he can take credit for turnaround …

Disc : I am invested in Kolte Patil … effective cost price is ( -53 ) . This is part of my non core opportunistic portfolio - hence negative cost because of trading in and out of stock over last 5 years

Gopal Sarda took over the co as the CEO in feb’18 - earlier he was mumbai CEO. If you look at the sales performance (in volume msf) it has been more or less flat barring some minor peaks here and there. In fact in fy21 they clocked their lowest sales volume in the last 10 years.

| fy12 | fy13 | fy14 | fy15 | fy16 | fy17 | fy18 | fy19 | fy20 | fy21 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Sales vol (in msf) | 2.84 | 2.64 | 2.13 | 2.86 | 2.04 | 2.1 | 2.1 | 2.7 | 2.5 | 2.08 |

If you listen to Mr Sarda speak on con calls - he has been saying the “next level of performance” for years now which hasnt quite materialized so far with sales volume in Fy18 (when he took over) at 2.1 msf and in fy21 - 2.08 msf. One could argue that he took over when the cycle was not favourable and that would be a fair argument but that speaks more about the cyclical nature of real estate than CEO prowess.

Having said that, the yearly run rate is not bad ( Godrej is similar but its a relatively new entrant in the Pune scene comapred to KPDL), but there seems to be less visibility on the growth levers - perhaps with the appointment of the new CEO from the family , there will be more focus on increasing sales volume to finally cross the 3 msf barrier.

Best

Bheeshma

5 Likes

And if you compare Mcap/(total area under construction*sales realization per sq ft)

Kolte Patil currently working on=2922.144 Cr worth of project (0.4885988)

Mcap-1800 Cr

Mcap / (total area under constructionsales realization per sq ft) = 0.61.

Godrej working on (63019.4) = 59229.4 Cr

Mcap -39,520

Mcap / (total area under constructionsales realization per sq ft) = 0.66.

There has to be a good reason to say yes i’ll buy Kolte Vs Godrej.

I can’t find any.

Roce and roe would be in favour for kolte plus land value : life republic remaining land value is around 1500-2200 cr with EV of 2200 cr of Kolte

1 Like

@kb_snn

Judging by your comment, apologies to say this but isn’t it more like a confirmation bias? Obviously I agree CEO’s come and go. Given the nascent knowledge I have, 2 points I want to make to you:

- CEO opting out and even selling his stake indicates that my better bargain would have been less than 250. CEO was never the whole and sole reason. All I said was that I need to watch it more carefully. A young CEO of 35 years resigning as CEO makes me wary. Ofcourse I have never questioned the company. Their AR’s are clean which is a rarity

- Regarding the below comment of flattish sales performance which is there in the below comment, please note that the industry was facing headwinds and the capital allocation skills of Mr. Sarda were phenomenal. All I wanted to say was company has lost one precious resource.

I want to rest my case here.

1 Like

Pabrai sold off around 2% and now owns ~5%

2 Likes

yeah. looks like his conviction is going down or he is finding something else interesting

1 Like

@nikunj_patel @sangam_khandelwal @harsh.beria93 Did you guys try to get in touch with Mr Sarda. I had mailed to KPD investor relations about the explanation. As usual, it was a bland reply.

This is abstract theory but makes sense. @nikunj_patel Thanks for highlighting

Planet Smart City and Kolte Patil : 15000 houses across Pune / Mumbai and Bangalore

If one looks at design and amenities @ price they are planning to offer seems very good . Not sure of how attractive will be margins

For people who want to understand what Planet smart city does …

And Kolte has launched a project with them couple of years back - Universe at Life Republic

Any Puneites can give their feedback on this project - Is it what it promises to be … @ 35 odd lacs

This differentiation is relevant in context when DLF management said for Indian listed companies > 75 lacs is viable product and they focus more on the same …

Another change in CEO, now Rahul Talele has been made group CEO and Yashvardhan Patil has been made joint MD.

2 Likes

AR21 notes

- Has ~9.13 mn sq.ft under execution (sold and unsold), 170 cr. of RTM inventory

- Realizations increased by 9% to 5’785 due to increased contribution from Mumbai

- Digital capabilities: 180 homes were sold during March 15 - April 30, 2020

- Mumbai + Bangalore sales contribution increased to 300 cr. (~25% of FY21 sales)

-

Pune:

o Launched Universe at Life Republic and sold substantial volumes at a higher realization compared to the other sectors within the project

o Completed final tranche payment of 81cr. for buyout of ICICI Venture’s 50% stake in Life Republic (first tranche of 70cr. was paid in March 2019 and the second tranche of 70cr. was paid in November 2019). Company’s economic interest in its entire portfolio grew from ~60% to ~90%.

o Signed 3 projects with a combined saleable area of ~2.2 msf in Pune under capital-light models; (Projected topline of 1500 cr., projected KPDL PBT ~220cr.) -

Mumbai:

o Mumbai portfolio reported sales value of 180cr. (vs 19.8cr. in FY20)

o Launched Evara at Q3 end (the first new launch in Mumbai in 4 years) and sold 54 units (75% of inventory)

o Launches of Verve (Goregaon) and Vaayu (Dahisar) in Q1FY22 should increase Mumbai sales proportion to ~25% in foreseeable future

o Redevelopment projects: Evara, Verve and Vaayu (expected topline of 1000 cr.)

o Will focus on large redevelopment properties that present possibility of generating at least 50 cr. in profit before tax. - Net debt declined by 124 cr. to 310 cr.

- Availed 3-month debt repayment and interest servicing moratorium

- Reduced marketing from a peak of 3.7% of sales in last few years to 2.6% in FY21

-

Partnerships:

o KKR committed 193cr. in R1 sector of Life Republic

o Entered into 120cr. agreement with an affiliate of J.P. Morgan Asset Management for its Mumbai redevelopment project Jay-Vijay Society in Vile Parle (E)

o Planet Smart City bought 10.4 acres of land at Sector R10 at Life Republic for 172 cr. and partnered KPDL to launch the project at Sector R10 in a profit-sharing agreement (1.42 mn sq.ft)

o The real estate investment firm ASK is a profit-sharing (70%) partner in the Three Jewels project -

Brands:

o Kolte-Patil (addressing the mid-priced and affordable residential segment)

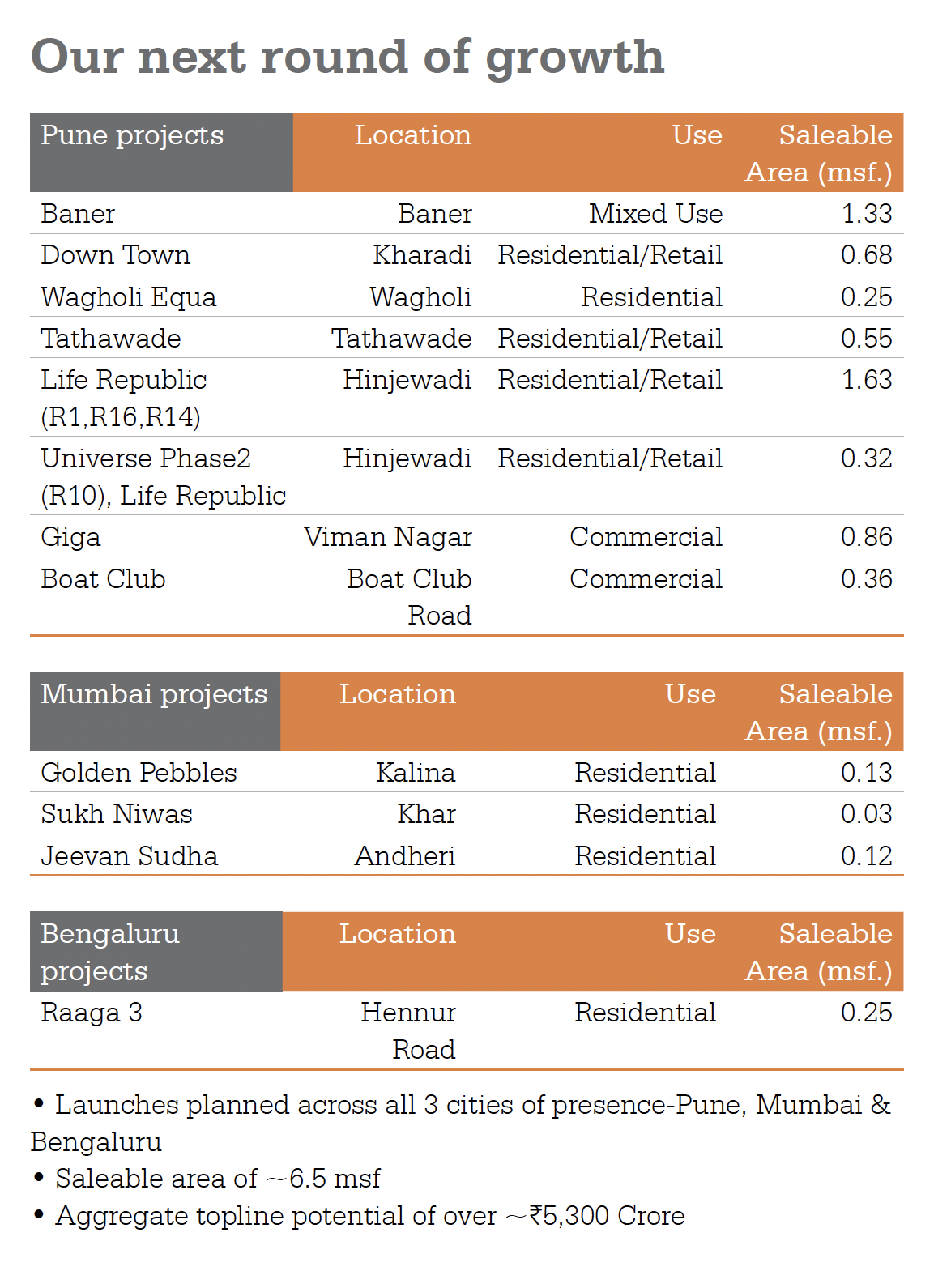

o 24K (addressing the premium luxury segment). - Planned launches: 8 in Pune, 3 in Mumbai, 1 in Bangalore. Total saleable area ~ 6.5 mn sq.ft, revenue potential: 5300 cr.

- Shareholder: 37’665, Share price: low (110), high (281.95)

- Number of employees: 558

- Aim: To reach 5mn sq.ft annual pre-sales run-rate in 3 years

- FY22: Signed 2 new projects with a combined saleable area of ~1.3 msf in Pune (Hinjewadi and Tathawade) under the DM model. Expected DM fees of ~80 cr.

Disclosure: Invested (position size here)

7 Likes