Given the massive market going forward there is enough room for both the companies.

1.It will take about 4-5 years for Polycab to be able to make sales in EHV as the all the orders require long prequalification.

2. Agreeing with @ishu the market is growing rapidly and in India there are only two players KEI and Universal cables.

1 Like

8 Likes

Polycab is doing EHV with the help of JV with Brugg Kable. Earlier till Nov’22 Brugg Kable had JV with KEI. So, KEI has already taken the juice for what Polycab is at the starting point.

2 Likes

I am studying KEI at the moment. Anyone concerned how the promoter and key managerial people are slowly but surely reducing their stake in the stock, specially in the recent 5 months, when the stock has been doing well. This also happens to be a concern raised repeatedly. Today the promoter has disposed off 200000 shares.

8 Likes

Yes the same concern I have too, 2 lakh shares is not a small number. Any reason behind this

1 Like

I am invested in KEI since last 6 years . Promoters have been selling their stake since at least 2014 . Promoter selling by itself doesn’t mean much ,unless it is accompanied by other doubtful activities.

2 Likes

Here’s the video that will clear many of the questions some of you have asked including those relating to promoter selling.

The following is the summary (any omissions and errors are mine ![]() )

)

- Order inflow - Infra pipeline, industrial expansion in line. All round growth projected in these areas for the next few years.

- Infra, real estate, solar sectors will be growth drivers.

- 10L crores allocation by govt. in infra, metros, railways will benefit the industry

- Growth can be better than earlier guidance.

- Promoters selling is very small quantity sales due to personal needs. 2L shars sold amount to 0.1% of the entire holding.

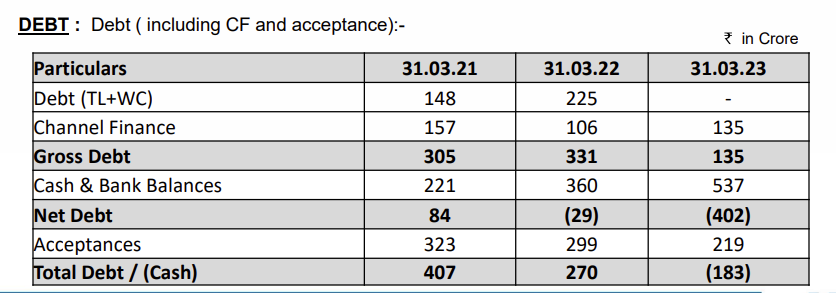

- CAPEX - 250-300 cr. for 2023; 1000 cr. for the next 3 years. .

- Capacity utilization in cables 90%, company working on brownfield expansion through which they will expand capacity by 15%

- Utilization in wires is 65%

- The EHV segment will grow.

- EPC will degrow as guided…will remain about 500-600 cr.

- EBITA Margins - may improve.

- Contribution from dealer distribution 45%. Next one year it will go to 50%

- Regional sales - All regions are strong, some in cables, some in wires. But focus is on all regions.

Disc: invested

10 Likes

In case of key risks involved for KEI business, many research reports talk about Policy risks. In case of EPC business, KEI is consciously reducing its share in sales…but in Institutional cables, how much impact business can have due to change in Government policies , legislations, regulations? Will this have major impact on overall revenue of the company and if yes then how much position sizing we should do on portfolio level, to reduce the impact of such adverse conditions?

1 Like

KEI has guided for robust 16-17% revenue growth in FY24 primarily based on the

capacity addition at its Silvassa plant and other greenfield expansion projects.

Management’s strategy of expanding its retail business also augurs well for the

company. It is difficult to say how much impact it can have due to changes in Government policies since they are focusing on diversification of product portfolio and de-risking business (retail accounts for ~44% with the target to reach 48-50%

in FY24). Further, KEI Industries has obtained UL approval for specified products to sell in the US market and has already commenced sales from January '23 onwards.

As far as the guidance given by KEI and the focus on more retail accounts, I do not see a major impact on overall revenue at this point.

The allocation depends on your risk tolerance vs the growth of the KEI. If you really want to play safe keep just 10-20% of the allocation. Again it depends on your risk tolerance and exit strategy (when to exit). Please keep an eye on EPS CAGR vs PE CAGR as well. The valuation must be considered.

6 Likes

@Mayank_Bajpai Ji,

Please don’t just post link to a blog or twitter page, unless it shows preview that contains the relevant points. Placing link to BSE or company website is fine though.

I am adding the content for others benefit.

KEI’s management Interview - (Key Outcomes)

.

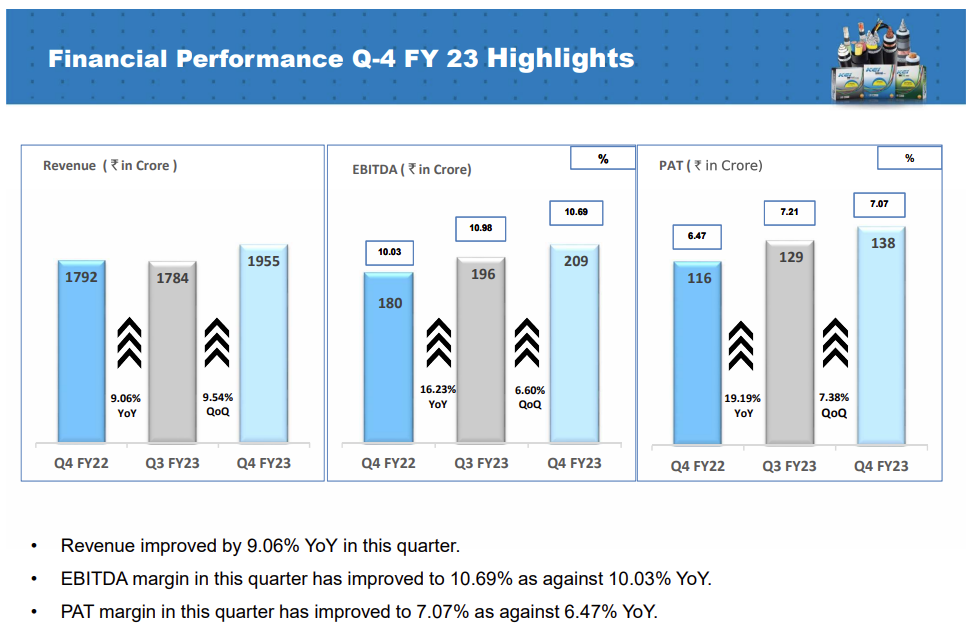

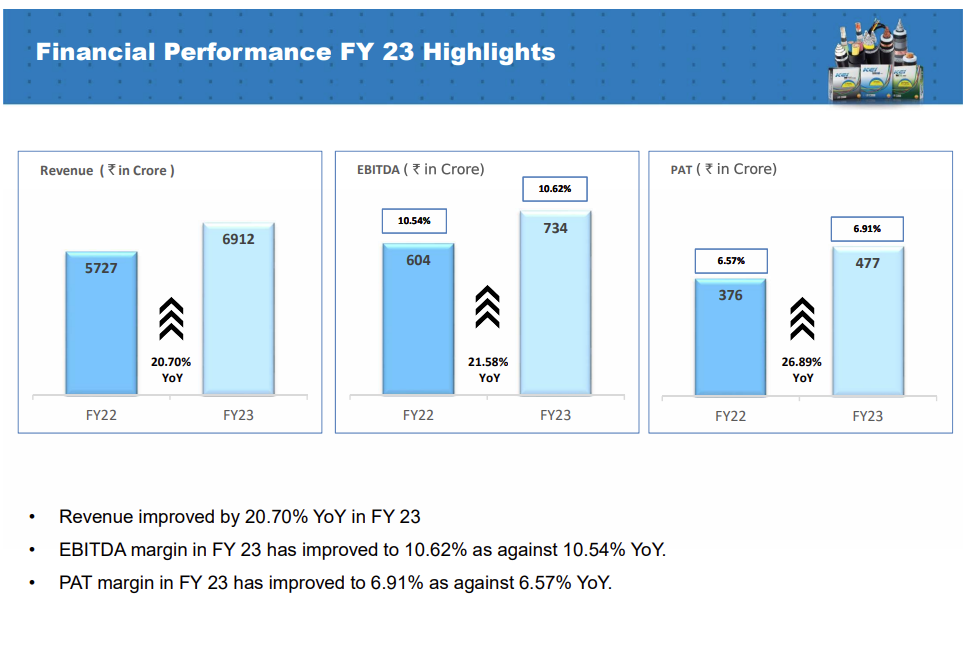

-Revenue growth in the cables business was 30.5%, with volume growth of 22% due to lower raw material prices.

.

-Market share concerns were raised, comparing Kei Industries’ 22% volume growth to competitors’ 30-50% growth.

.

-Margins dipped due to capacity constraints and higher expenditure on IPL and advertisements.

.

-The company is building up capacities to meet strong market demand and achieve targeted volume growth of 16-17%.

.

-Large capex planned for the room factory with an investment of around 1000 crore over three years.

.

-EHv business on track to cross 600 crore, despite Q1 dip due to clearance delays from utilities.

.

-Export contribution is expected to increase, and margins in exports are slightly better than domestic sales.

.

-Retail business to be ramped up to 46-47% of sales this year, with similar margins to B2B business.

.

-First-quarter margin dip due to higher expenditure on IPL and advertisements, overall margin expected to be close to 11% for the full year.

.

-Market share movement in Q1 lower than peers due to capacity constraints.

.

-The company maintains its guidance for the year despite market expectations.

13 Likes

Sujay ji, thank you so much for the candid feedback and I will keep this in mind in the future. I am sorry for any inconvenience.

1 Like

KEI has corrected as they had capacity constraint and couldn’t fulfil the orders. Still grew Volumes in cables at 30%. Peers grew 40%+ due to excess capacities.

2 Likes

Basis q1 FY24 concall, KEI now seems on the right path as expected by me in Jan 2022 - refer above post.

5 Likes

Kei ind update

(From credit rating ,concall)

KEI

1…Capex

A… Company plans to invest ~1,000 Cr over next 3 to 4 years to setup a manufacturing facility in Gujarat. It has bought property, and the first stage of the plant is projected to be operational within 18 months from beginning of construction.

…Gujarat project to start sales in Q4 FY '25.

B… Company plans to invest Rs.50 Cr in expanding its Chinchpada unit. This project is scheduled to be finished in September 2023

C… Plans for a brownfield capex of Rs. 45 Cr in Silvassa plant to be completed by September, brownfield expansion by Q1 FY '25,

=KEI has lined up a significant capex of ~Rs. 800-1000 crore over the next

three years, likely to be funded by internernal accurals

2…Order Book

Company has a order book of Rs.3,567 Cr, including EPC projects, extra high voltage power cables, and domestic and export cables

3…Segmental

Retail ~ 44%,

Institutional ~ 46%,

Export ~10%

4…U.S. market is a key focus for export growth.

…KEI received clearance for its LT cables, HT cables and solar cables for the US market. It will begin sales in the US market in the 4th quarter of FY 2022-23 to power, gas and petroleum sectors

5…End industries

=Favourable demand drivers in various end user industries such as power generation, transmission and distribution, railways, real estate, among others while maintaining its

profit margin profile.

=ICRA notes that the company’s products are witnessing robust demand from various end-user industries

that are benefitting from government infrastructure development activities, including urban and rural electrification, solar

power projects, tunneling and ventilation projects on highways as well as railway and metro rail projects.

=Additionally, private

capex is currently at healthy levels across sectors such as renewable energy, steel, cement and real estate, including housing

demand, under the GoI’s initiative of ‘Housing for All’

6…To boost its retail sales, KEI has increased its distribution

network to over 1,925 dealers pan India as on June 30, 2023 (Mar 31, 2022: ~1,800), in addition to increasing its employee strength.

7…Despite the commodity headwinds in FY2022, KEI’s margins remained protected on account of

a partial natural hedge as the company maintains an inventory for 2-2.5 months and passes on majority of the raw material

price hikes to customers.

8…NEGATIVES

=KEI’s moderate profit margin profile due to the adverse movements in raw

material prices and foreign currency fluctuation and intense competition in the wires and cable industry, which limits its pricing

power to an extent.

=The cable industry is inherently competitive with the presence of multiple large established

players such as Havells India Limited, Polycab India Limited, Finolex Cables Limited, V Guard Industries Limited, RR Kabel

Limited, etc., in addition to some competition from the unorganised sector. This limits KEI’s pricing power, to an extent,

especially in the retail segment, which is expected to drive its revenue growth over the medium term.

Disc…invested from lower level

5 Likes

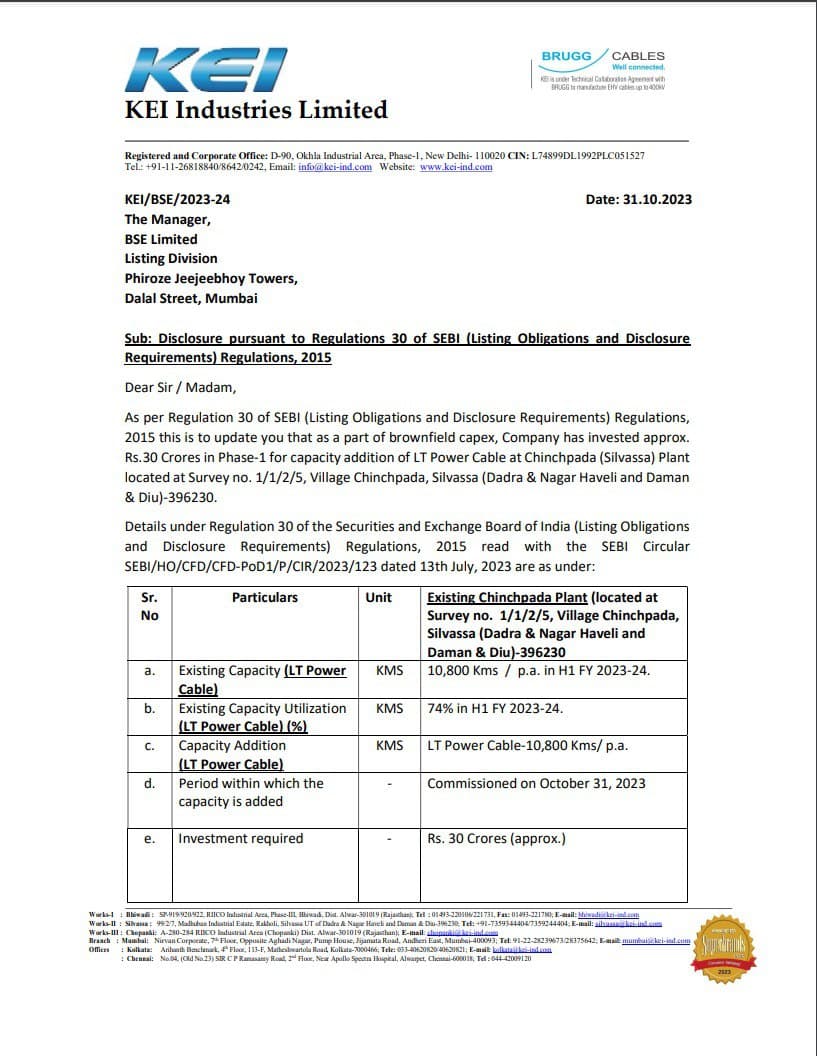

KEI Industries Limited, has made an investment of approximately Rs. 30 Crores in Phase-1 for increasing the capacity of LT Power Cable production at their Chinchpada (Silvassa) Plant. This plant is located in Silvassa, Dadra & Nagar Haveli, and Daman & Diu.

Here are the key details about this investment:

- Existing Capacity (LT Power Cable): 10,800 Kms per year in H1 FY 2023-24.

- Existing Capacity Utilization (LT Power Cable): 74% in H1 FY 2023-24.

- Capacity Addition (LT Power Cable): 10,800 Kms per year.

- The capacity was commissioned on October 31, 2023.

- Investment required: Approximately Rs. 30 Crores.

The financing for this expansion is from internal accruals. This investment has expanded the LT Power Cable production capacity to approximately Rs. 240 Crore per year.

8 Likes

The Management has repeatedly mentioned that they target 16%-17% revenue growth annually and during this quarter’s Concall they categorically said “we do not target to grow 30%”. Now Polycab is also growing in the range of 15-20% annually.

Does this commentary from Management indicate industry specific realistic growth or are they less-ambitious or is it a capacity-debt related constraint? Any insights would be helpful here!

2 Likes