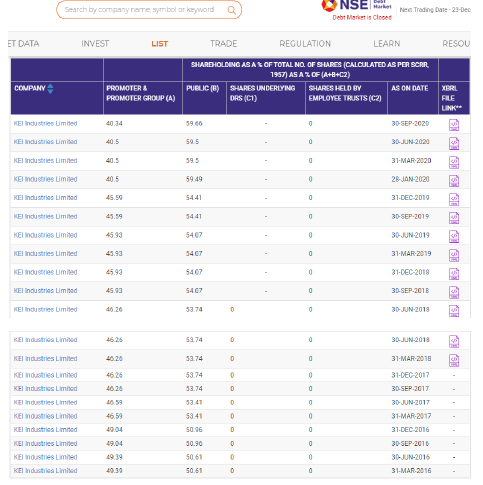

From the begining the promoters constantly decreasing their holding. Any reason for this. 49 to 40% in 4 years time frame.

below are the reasons for change in share holding

- ESOP — to Employee minor

- increase in share capital due to allotment of equity shares to Qualified Institutional

Buyers under QIP - -2.80% or 1900000 shares decrease in FY 2016-17 due to sale by Promoter Mr. Anil Gupta

number of shares held by Promoters 3,62,48,466 did not change over the period from March 2018 (both in March 2018 and Sep 2020)

3 Likes

I think, increasing demand of renewable energy like solar will have positive impact on kei industry.

Anyone from cable,solar or related industry can provide valuable inputs

Thanks.

Disc…invested.

1 Like

stocks strength is its product portfolio which is wide spread,however the charts are not comfortable also increasing copper prices will be a dampener.

1 Like

Q4 FY21 Updates:

- [Order book]

- Order book as on 25.05.21 is 2561 Cr. Of which EPC is 806Cr (Export order 316 Cr), EHV is 506Cr, Cables is 1249Cr (Domestic 1198Cr , Export 51Cr)

- [Growth Guidance-Attractive]

- Revenue Growth for FY22 - 25% in Domestic Institutional sale and more than 35% in retail space. (Volume growth is 24%)

- Revenue target for FY22- 5000Cr

- Overall revenue Growth of 17-18% in FY22

- To focus on retail growth recruited more than 100 employees in last four months

- [Does current capacity support growth-Yes]

- Current capacity utilization

- Cable division - 59%

- House Wire division - 61%

- Stainless steel division - 85%

- Capacity of EHV is maxed out, so additional business is not possible

- with current capacity, they can do revenue of 6500Cr.

- Current capacity utilization

- [Future Capex - Yes]

- Targeted to spend 600-700Cr in next 4 years through internal accruals to maintain CAGR of 17-18%

- Company has sufficient capacity for 2 years or growth and new capacity will be available by same period

- A new green field plant is planned to start in Gujarat with capex of 150Cr. Work will start by Q2 FY22

- [Current Debt - Reduced]

- Net Debt details - Overall reduced - 407Cr vs 923Cr yoy

- Cash stable - 221Cr vs 214Cr yoy

- Acceptance reduced - 323Cr vs 770Cr yoy

- TL+WC loans - 148Cr vs 230Cr yoy

- Channel finance - 157Cr vs 137Cr yoy

- Net Debt details - Overall reduced - 407Cr vs 923Cr yoy

- [New debt - No]

- Retention money of 150Cr will be released from EPC in FY22, which will take care of Capex requirements and working capital.

- Future capex of 600-700Cr in next 4 years through internal accruals

4 Likes

- KEI has done 20% sales CAGR over last 5 years v/s 14% for the industry. Management expects a 17-20% topline CAGR over next 3 to 5 years

- KEI expects revenues of Rs 50bn in FY22E and Rs100bn in FY26E.

- If copper remains at current levels, management expects FY22 revenues at Rs 55bn.

- Utilization: 59% in cables, 61% in house wires and 85% in stainless steel wires.

- Cash profit of Rs 3.5bn in the coming years, of which Rs 1.5bn-1.7bn will be used for capex requirements each year for the next 4-5 years.

- Used Rs 5bn QIP issue to reduce debt, thus saving Rs 750mn in finance costs.

- After strengthening retail chain, will get into switchgears, RCB, MCB, fans and pumps.

Disclosure: Invested

4 Likes

KEI IND

MOATS

Disc…invested

2 Likes

• Revenues at Rs10.2bn +36% YoY

• EBITDA at Rs1.16bn up 37% YoY

• EBITDA margin improved to 11.45% as against 11.39% last year

• PAT at Rs671mn + 71% YoY

• Total Institutional cable sale (HT& LT) up 9% YoY

• Cable sales through Dealer/ Distribution market increased 108 % YoY

• EPC Sale (apart from Cable) increased by 10% YoY

Disclosure: Invested

3 Likes

Here’s my take on KEI Industries

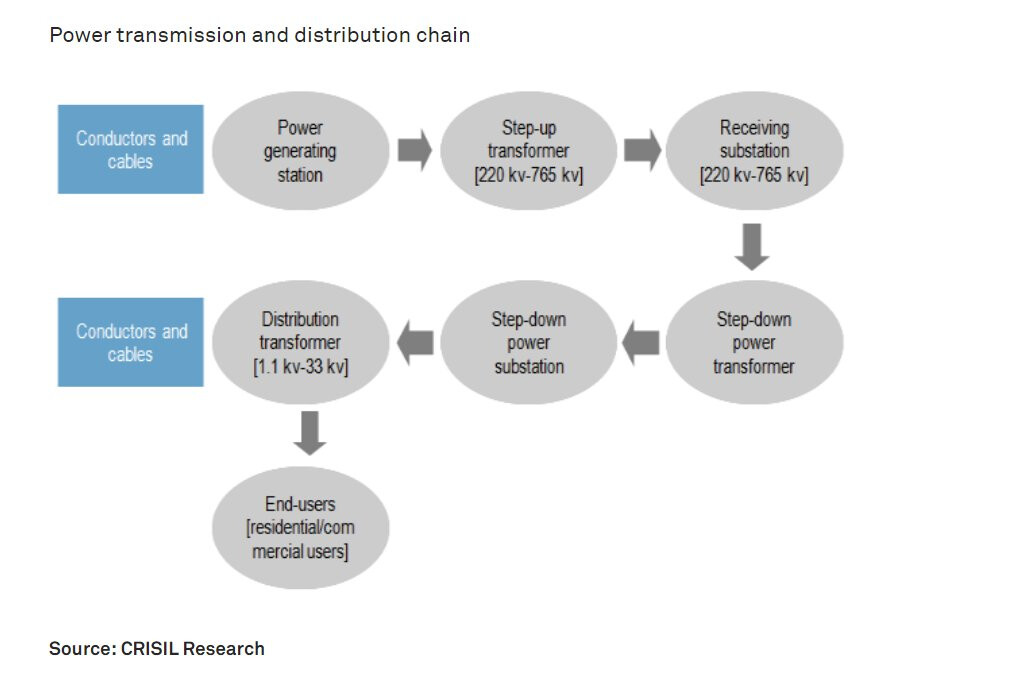

Industry Overview:

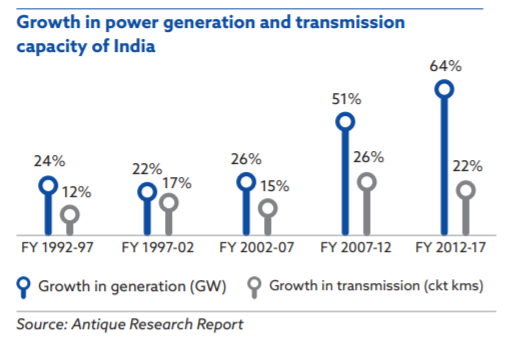

Power Industry T&D Chain:

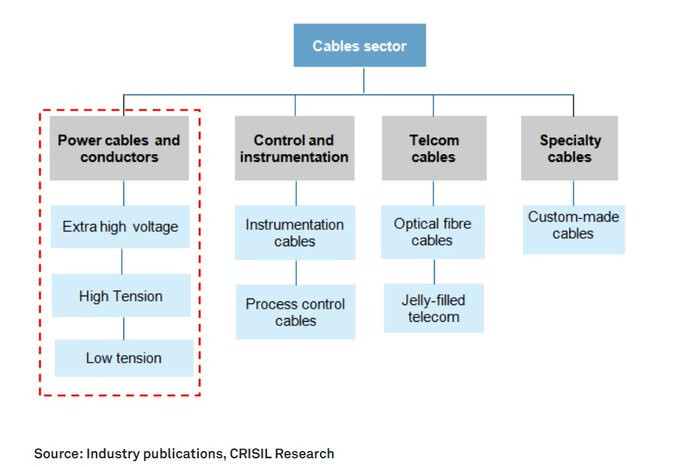

KEI Industries mainly operates in the Wires and Cables Segment.

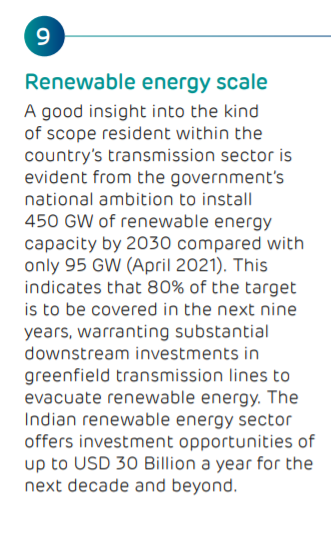

The domestic Wires and Cables industry is set to expand by 20-22% CAGR to reach Rs 245-255 billion over fiscals 2021-24 compared to the ~3% CAGR over fiscals 2017 to 2020. This will be mainly supported by demand from IPDS, DDUGJY & Green Energy Corridor along with transmission-led investments along with the low base of fiscal 2021. However, the demand is expected to moderate, owing to the completion of the Saubhagya scheme. Over the same period, exports are expected to grow at a CAGR of 10-12% majorly to the African and SAARC region. ----- ( Source: Crisil Research)

If this sounds very optimistic, Please look at this snippet from KEI Aug 2021 concall:

Crisil research suggests that In the long term, power demand is expected to be supported by economic growth recovery, expansion in reach via strengthening of transmission and distribution (T&D) infrastructure, and improved power quality, thereby registering a 5-6% CAGR over the next 5 years.

The long-term growth story for the power demand is intact and it could be well pushed further by EV adoption. The faster the EV adoption, the faster the growth in Power demand.

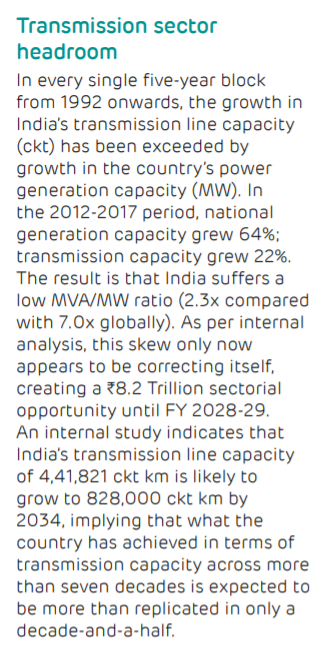

The Transmission and Distribution industry will see significant investments in the next 5 years led by robust investments in inter-regional and inter-state grid networks, increased private sector participation, and focus on Green energy corridors.

The T&D sector is facing tailwinds and The Power cables and wires sector is the direct beneficiary of this.

Few snippets to support my statements:

Source: (Adani transmission Annual report)

KEI Industries:

Highlights from the 2021 annual report

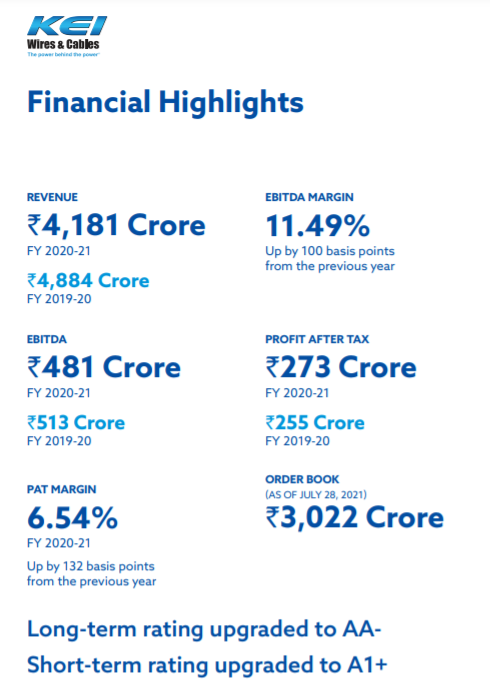

Financial Highlights:

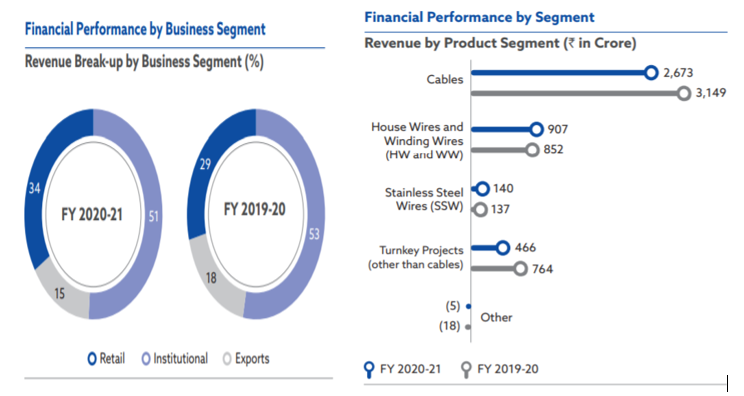

Currently, KEI has a 7% market share in India’s organized wires and cables segment & a 12% market share in the institutional segment.

Growth strategies:

- Expanding capacities in product portfolio

- Focus on increasing retail share

- Increase in exports

- Expanding distribution network

- FMEG launch in the next 2-4 years

Focus on Retail: Currently at 34% of sales, aim to achieve 40-50% of revenues from Retail, because retail has better growth prospects, better margins, and lower WC requirements as realizations are faster. EPC is being deliberately reduced due to the elongated WC cycle and low margins.

The current capacity utilization gives a lot of headroom for boosting sales.

In the Institutional segment, the company has strong MOAT’s as there are strong entry barriers like stringent compliance requirements, product approvals.

The company bagged an order from Tamilnadu Transmission corp ltd for 400Kv EHV cables which could be the first of many. EHV cables also face significant tailwinds as many cities are pushing for underground cable networks and the development of smart cities will further push the demand for EHV cables upwards and KEI is one of the very few companies which produce 400Kv EHV cables.

Investment Thesis:

- KEI Industries is one of the largest players in the Institutional Power cables and Wires segment and this segment has high entry barriers which would help KEI to grow with the demand and there would be less stress on pricing from the competition.

- KEI has hired consultants and is constantly engaged in increasing sales through the Retail segment which has better margins and lower WC requirements and also they said that they would be reducing the share from EPC due to longer WC cycles.

- Huge sectoral tailwinds for the T&D industry as mentioned above

- Housing also continues its growth which would aid KEI retail segment further

- Far fetched but foray into the FMEG segment like Finolex and Polycab would help the company scale up its revenue significantly

- Company trades at half the valuations as Polycab ( Polycab has a fast-growing FMEG segment)

Disclaimer: Invested, views could be biased

15 Likes

Follow up on the Previous post:

The Prev post did not cover the risks associated with the wires & cables industry, I will try to cover them here.

Key Risks:

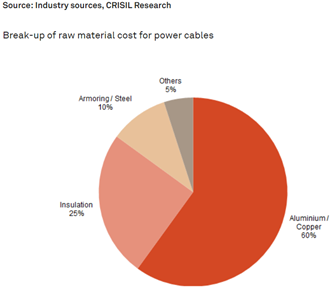

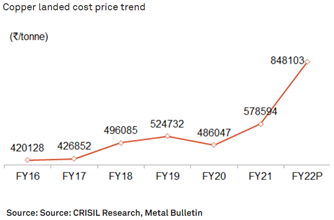

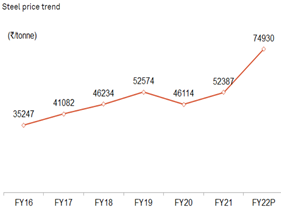

Raw material Price inflation: (Not a big one in my opinion)

Raw material costs make up a significant portion of the expenses. RM constitutes up to ~80% of the operating expenses for cables.

Ever since the pandemic stuck, RM prices are going only one way. Please see the trend in prices for Aluminum, copper, and Steel which are the main raw materials.

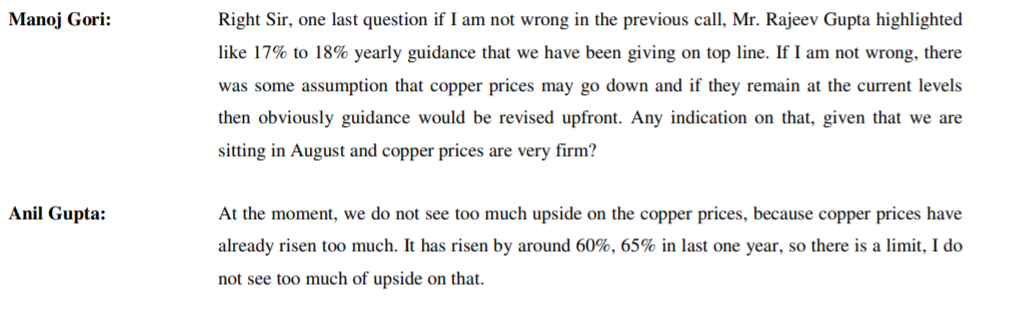

Management sounds confident that there won’t be a further rally in copper prices as they have risen too much already. Snippet from Con-call

over that management says that no competitor can absorb copper prices and there is a pass-through mechanism and prices are revised once/twice a month based on copper price movement and for institutional orders, they always have 2-3 months of inventory which acts as a natural hedge. For PVC company has backward integration and manufacturing its own PVC for cables.

Would appreciate more views on Key risks for the company. Thanks for Reading

Bonus: If you haven’t already read it Please go through the below

Here’s an extensive report from Prabhudas Lilladher on KEI

5 Likes

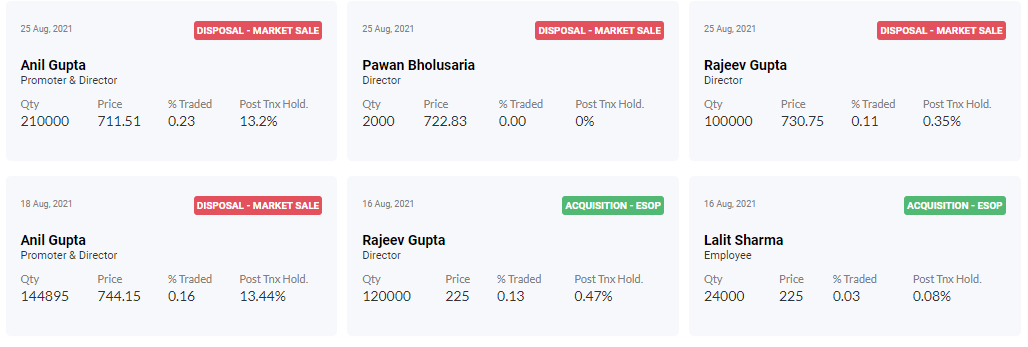

Even though small but promoter selling slowly seems a concern, any idea why?

Mr .Rajeev Gupta acquiring shares as ESOP and selling and Mr. Anil Gupta also selling.

1 Like

As per peter lynch "Promoter selling has not much significance if it is not huge as promoter may have cash requirement or he/she want to diversify his investment.

1 Like

One Question after the new Elecertricty Amendment Bill, will KEI also be ancillary to play this theme since the company is a major EPC supplier with ties to Tata power , ABB Power Products, and also other private players in the space, also the infra boom theme

What will be the key areas KEI lags behind Polycab and Havells in its retail segment of Cables?

1 Like

KEI is shrinking their EPC business because its a rubbish business with competitive bidding, lower margins and long working capital. Based on this the stock is rerating. And you want to buy KEI for EPC…

BTW there is no Infra boom theme. Infra boom happens when capex grows at 30% plus per year…which has not happened post 2009-10 and unlikely to happen soon

4 Likes

Buying a Rs140crs house for his son in Delhi

1 Like

2 Likes

KEI Industries results were much better than the cable and wires business of leader Polycab and no. 2 Havells

• Revenue up 30.5% YoY to Rs13.5bn

• EBITDA yp 28% YoY to Rs 1.49bn up 28% YoY

• EBITDA margin at 11.00% down 74bps YoY

• PAT up 37% YoY to Rs917mn

• Sales through dealer/ distribution market +67% YoY in 2Q and was 43% of sales in 2Q

• Active working dealer of the company as on Sep 30, 2021 was ~1700 Nos.

Disclosure: Invested

5 Likes

Good - comparison is must between these mentioned competitors

2 Likes