Learning about this company and trying to understand what about the business model is causing inventory days to be so so high. Is it because sowing happens only for a limited window every year?

Kaveri seeds

Highlights from the management interaction

-

Guidance: Overall growth is expected to be in the 10-15% range, majorly driven by the non-Cotton segment, which is expected to record 15-20% growth in FY22, supported by growth in volumes and realizations.

-

The Cotton segment is expected to grow at 5-7% in FY22 as acreages are expected to remain stable. Realization is expected to rise by 4-5% in FY22.

-

Market share: Other than Telangana and Andhra Pradesh, KSCL gained market share in the Cotton segment across all states. The company managed to gain 0.5% market share, taking its overall share to 17%. Market share in rice increased to 10% as the company managed to gain share in FY21, whereas the same in maize is currently close to 10-11%. The size of the domestic maize market is currently pegged at 85,000-95,000MT.

Kaveri seed consider buyback and board meeting aug 25

Kaveri Seeds Analyst Analyst call key point discussed Q1 FY22

- Revenue – 629.77crs A degrowth of 12.5%. EBITA 34.09%

- Contribution of new products have gone up from 6.98% to 17.88%.

- The current year has been one of the worst in last two decades for cotton and hybrid seed market because of illegal and HTBT seeds. Second wave of pandemic impacted the sale with supply chain issues. Farmers could not travel to near by places to buy branded cotton.

- Difference between branded and unbranded or illegal cotton seeds is only 100 rupees.

- Hybrid rice will contribute significantly in sales going forward.

- Growth of vegetables segment is also very strong and will add few more crops to the list.

- Sales return 35%, as most of the stock will remain in market and take time to come back to the company.

- Write off are high on non-cotton crops – 22crs

- Transportation during lock down was difficult and effected the bottom line.

- Dependence on cotton must reduce and the company is concentrating on that.

- Gross margin is going down because sales have been impacted and employee cost is increasing because the industry as a whole is increasing.

- The company does not operate or plan on organic farming.Not looking for any parallel business.

- 850-900 crs in last 15 years . This year is a little different because of pandemic, or the cash wont be held back.

3 Likes

Let’s hope it is via open offer and not tender route! Recently another company decided to issue a tender offer for Rs 3200 when the trading price was around 2200. Company is rewarding exiting shareholders and diluting existing shareholders. Hope Kaveri Seeds does it the right way this time.

2 Likes

company purposely crashed their price from 770 to 578, when analyst asked about buyback in that analyst call, they said that no idea at present. After two days they have considered buyback. i feel they will not give more than Rs 800.

In last Concall company said they are yet to allocate cash. This Q’s Concall also they dint come back with cash allocation strategy.

I have serious doubts about it now. First, I dont see reasonable growth and no capex plans in place for exapansion. Second, I dont understand the management stance on many issues like exports, cash allocation, etc.

disc - invested

1 Like

Berkshire tries to buyback at cheaper stock prices. Hopefully some of our companies start to do the same. Selan Exploration did an open offer buyback and that signals that the company is doing the buyback benefiting the existing shareholders like they should.

It would be a good thing if share prices come down and the company does an open offer buyback at the lower market prices than buying at higher prices to “reward” exiting shareholders. Instead the companies should give a dividend which would benefit all shareholders rather than just those participating in a buyback. However, it is understandable the promoters prefer tender offer rather than dividends because of the dividend tax (upto 42%?) vs buyback tax calculation (22% of [buyback price - issue price]). Better yet, why don’t the companies start investing in securities by hiring a portfolio manager.

Whenever a company in my portfolio does a tender offer buyback where the offer price is much higher than the prevailing share price, I think it makes sense for me to surrender the entitled number of shares rather than hold on to them.

1 Like

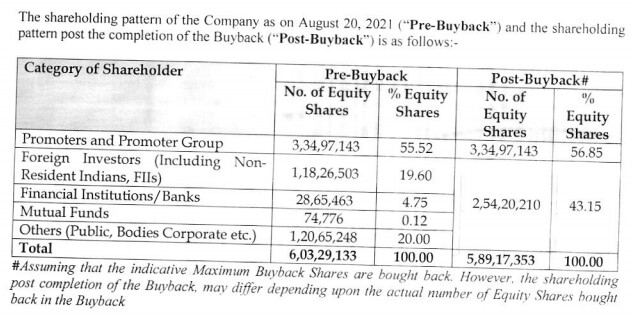

Buyback size of Rs 120cr announced, representing 2.34% of paid up shares.

Price no exceeding 850rs

Promoter not participating in the buyback

Discl: Not invested

1 Like

Finally, looks like this buyback is via open offer (Companies like Eclerx Services should take a cue). Also, the promoter holding will go up and they are signalling that this buyback is value accretive to the existing shareholders.

2 Likes

Cotton revenue for Kaveri drops to 30% of total revenue in FY22E from 57% in FY16. Is the pain in the stock over due to dropping cotton sales with this big drop? Lot’s of opportunity in paddy, vegetables and maize.

Source: Traits which matter...

5 Likes

As per new law ,now we don’t have to pay any tax on profit on shares tendered in buyback. The tax is being collected from company by tax dept.

Thank you for pointing this out. Is this below section what you are referring to:

Shareholder

Buy Back Tax is levied at the level of the company, the consequential income arising in the hands of shareholders is exempt from tax, as per Section 10(34A) of the ITA.

Just occurred to me that they went the opposite way with regards to Dividend Distribution Tax. It would have been better if they kept the DDT!

Many of these companies who go the tender route are offering significant premium to the current market price. For example, a company’s shares ended at 2353 today. Their buyback price is Rs 3200 (Update on 19 Sep: The buyback price is now set to 2850 which is not as bad. ) provided the shareholders approve. That’s a 36% premium. To pay this 36% premium for an exiting shareholder they have to pay 20% buyback tax. So for every Rs 100 of value they are acquiring for existing shareholders, they pay extra 36% premium + 20% on buyback price - issue price. Is this the most efficient way to reward shareholders? Paying a premium mostly benefits participating shareholders and not those who want to stay shareholders long term. I won’t participate in Kaveri seeds buyback but I am incentivised to participate in the other company’s buyback. It would be value eroding for me to not participate.

I am hoping more companies change from tender route to open offer route to add value to its existing shareholders.

1 Like

As per new law ,now we don’t have to pay any tax on profit on shares tendered in buyback. The tax is being collected from company by tax dept. If we have higher purchase price then buy back price, we can’t claim loss also.

2 Likes

"Cotton volumes decreased by 24.29% and revenue decreased by around 23.04%. Expecting cotton volume to take a lead from this year and the demand would increase during the financial year. Hybrid rice volumes increased by 19.2% in FY22 and revenue by close to 30%. The new contribution of hybrid rice was up from 68% to 75%.

During FY22, hybrid rice sales were not encouraging, in spite of that the company has grown its hybrid rice revenue by more than 40% and had gained the market share. The prospects for hybrid rice growth during FY23 is better than FY22. Selection rice volume grew by 6.26% in FY22. Maize volumes decreased by 16% and revenue by 7.69% in FY22."

- Earning Call Transcript (Q4 FY22)

2 Likes

Earning Call Transcript (Q4 FY22)

“Any major shift in adoption of hybrid rice, maize and vegetables and increase in volumes for the cotton seed are going to drive the growth of the company.”

3 Likes

Hello Amit,

Are you tracking or looked into it lately? Do you still hold similar views CG issues?

@varadharajanr Are you still tracking Kaveri?

Looked into Kaveri recently and it seems to be at a turning point this year onwards. 70% of profit now from non cotton.

Thanks,

Ayush

1 Like

Look like no one wants to touch this…despite the possibility of good Q, given almost all agro commodity prices are up and farmers might be willing to pay up for good seeds…

Disclaimer: invested in last few weeks… 8% of portfolio…

3 Likes

This result marks the end of sowing season. Historically, the stock stops performing from this quarter on until next year. Even with the changing story and encouraging transformation in company, the cynical nature ensures no sales (vegetables are too small to contribute meaningfully and sowing of rice has already happened). Questions:

Knowing this, wouldn’t it be better to come back to this stock next year?

Why is the growth of Hybrid rice still so little at 6%, despite it’s advantages?

1 Like