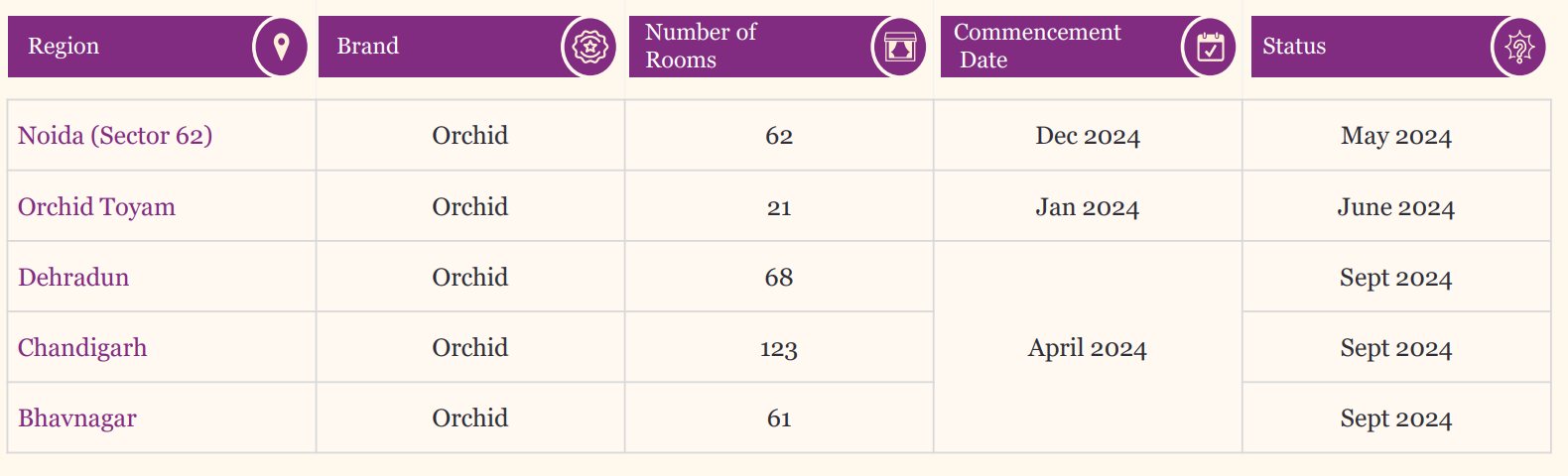

I was going through the list of hotels that the company had declared that they’ll open in 2024 along with the commencement date. We can see that there are 2 hotels that are still not opened. They’re supposed to share the status by Sep-24 which will probably be the next concall.

Meh results. It seems like there’s some delay in opening or ramping up the hotels that the management has expected to open given the 400 Cr Sales guidance.

Do keep in mind that Q1Fy25 was expected to be poor due to elections, heat wave and this was communicated by other hospitality companies. Edit: Looks like Kamat management wasn’t expecting it

Costs have risen, probably because lease costs, hotel cutlery, linen, etc. costs have increased to acquire new properties. This has hit the EBITDA margin hard whereas sales haven’t increased on par.

Finance costs should have reduced more, was expecting around ~7.2 Cr interest costs instead of the current 11.4 Cr. Not sure why the interest payment is higher.

Still bullish but this will add more lead time for any possible re-rating of the stock.

Also, the company has merged with other promoter companies which own some land in Ville Parle. Will need to check whether the valuation and shares issue to the company is at fair price. Promoter equity has increased considerably post this merger, hope the dilution is fair for minority holders.

Company has also released their Q1FY25 presentation. Some interesting snippets:

Occupancy rates were lower across properties due to General Election period resulting in Y-o-Y decline in revenues

This was expected but no new keys additions is brutal.

Lower Occupancy rates combined with ongoing Capex at Lotus Goa and Orchid Hotel Pune resulted in decline in EBITDA

This is the first time that the company has mentioned this capex. So far it doesn’t look like the company is any closer to achieving its guided EBTIDA. Last time as well, they didn’t reach their guidance except that time they had a solid reason of buying back NCDs

Doesn’t look like they have added any new keys so far in this quarter, not sure how they’re going to achieve their revenue growth

Haven’t reduced their guidance as well in the ppt.

Have some question on the merger scheme. I am wondering if the swap deal is at a good price:

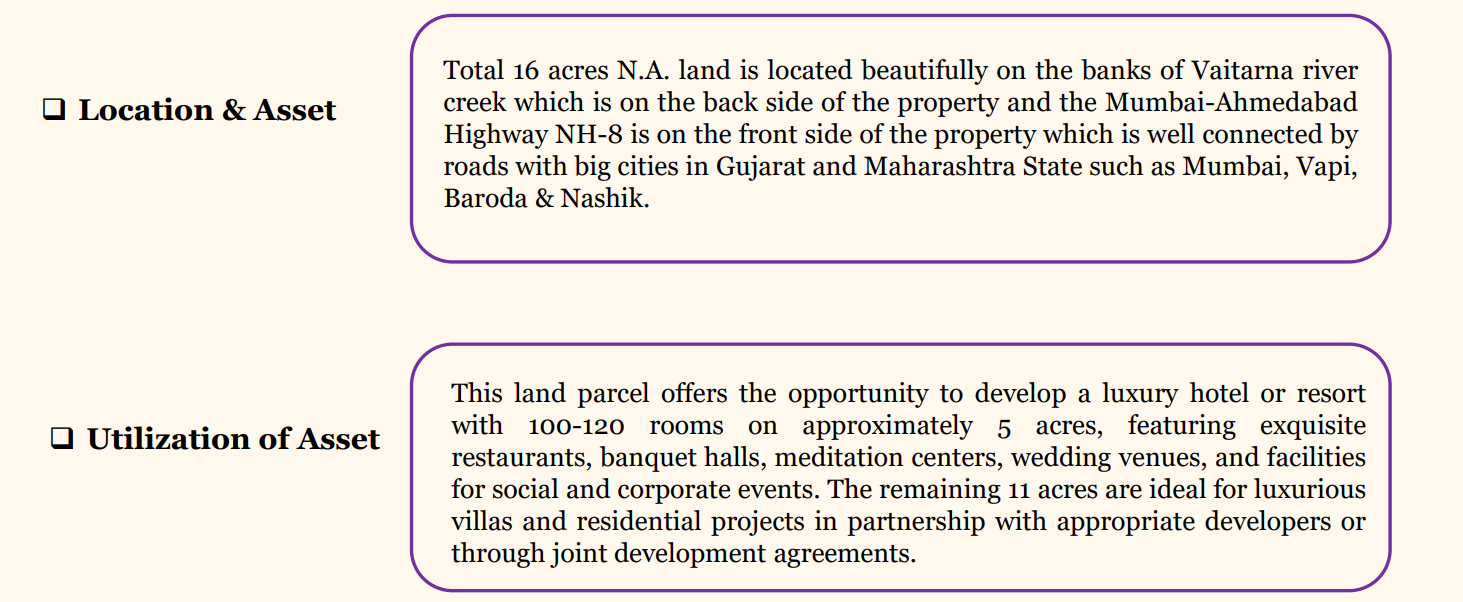

What is the size of the land parcel in Vile Parle that was with SRAPL, removing 0.77% stake in Kamat, it’s estimated cost at 231 CMP is ~65 Cr? Is this txn done at a fair price, isn’t 65 Cr a lot for a sewage treatment plant?

Is the Manor, Palgar land on a good location and is 2.2 Cr per acre a fair price for the land?

Edit: As per the concall the fair price was around 20-25 Cr and company wanted to derive more value by holding and developing the land parcel

Good things - Debt has come down by 172cr to 130 cr, Left with approximately INR 130 crores from Axis Finance Limited at the rate of 10.75% and as per mgmt will result in significant reduction in finance costs from ensuing quarters. I am expecting 4 cr int cost and 5 cr depreciation going forward.

Another positive news from this results, All pledged shares of promoter group would also be released with immediate effect. Hence forth investors dont see threating message while buying Kamat.

Negatives- Yes dilution to an extent of 5%, glad this is limited to 5% which happen in most cases where promoters see huge value. Even if the value is there in acquired companies, that will be loss for minority share holders as we dont see any value in the next 3 yrs. By this promoters kept their holdings intact as theirs will be diluted to pref allotment. Hope they buy another 5% by yr end and allow share rerating.

We can expect good results in q3 and q4 and q1fy26 and I think those results only help the stock in rerating. For now just accumulate if it falls below 200.

Next FY probably we can expect 30 EPS considering 3.3 cr equity shares.

Did they give any reason for promoter not being present in the call?

This looks bad. Still, there’s sufficient margin of safety considering the stock price and company’s debt is sustainable and the business is cash accretive so no need to panic just yet.

Did they mention anything about addition of new keys, given the 2,200+ target that they had for FY25? Owner being sick is not a good enough reason, why are they not approaching other owners.

How come they didn’t anticipate drop from election when everyone else was expecting it, are they living with their head in the sand?

I have been tracking this company for past 2-3 quarters. After every quarter, I see people on the forum discussing the promises the management has not kept. And I get the feeling that the management breaks more promises than they keep.

Market has many other opportunities. In such a scenario, it is better to deploy your hard earned money in a company where you can trust the management’s guidance than go bottom fishing.

Cheap stocks are cheap for a reason, especially in these bull markets

Management is doing well in running business and they did very well in reducing debt. Offcourse they are over optimistic in giving guidance, they are ahead of 3 to 6 months actual results. This qtr the shock is merger, its a 15% dilution without accretive EPS in the near future. One should be ready to see these bouncers in investing journey. If not for these, why else stock trades in discount?

What a shitshow of a concall. Promoter throwing the CFO under the bus by making an excuse to not attend. Removed earlier guidance of revenue and ebitda from PPT and then saying that it is premature to say after just q1. Yet it was completely fine 3 months earlier to speculate.

What kind of a cfo was this? First she said 12-13 cr interest cost then 7-8. Then someone again asked her and she said 5-6. Then another analyst present her the math and she agreed to even 3.6-3.7 per quarter. Oh. My. God.

Seems like they were not paying fees to Maharashtra pollution control board. She mentioned paying one time fee of 1 cr. And then said it will be yearly. Wow

Disappointing results and concall . Management doesn’t seem to understand the importance of guidance and associated perception of not meeting their own guidance repeatedly despite full confidence in earlier concalls. E.g. crossing 100 Cr ebitda in FY24, on/off frequent one off expenses , massive confusion on the interest costs . If they were expecting a tepid Q1/Q2, they should have laid out that upfront instead of being 100% confident of crossing 400 Cr in Fy25. Market will neither reward nor rerate this stock if these things keep happening. They should have expected questions from investors and analysts (e.g. jump in other expenses QoQ/YoY, interest costs ) and should have laid out the explanation in the ppt itself instead of getting repeated questions on con call and wasting time. Unfortunately the con call became a clarification exercise instead of being forward looking , frustrating for everyone!

IMHO, investor communication should be made more precise and clear and avoid multiple confusion . They can spell out all the basics in the Investor presentation which should clarify all questions which will limit follow up questions on call.

Q2 results will set the tone for FY25, but the 400 cr FY25 guidance seems too far fetched, and the actions of the management doesn’t inspire confidence yet.

Really a tamasha is going on at Kamat Hotels. Worst kind of management I have ever seen. They are making caricature of themselves. Repeatedly they have failed miserably to give guidance. But still they are going ahead to give it and having muck in their faces. Is it a management or sham ? Any one could foresee bad numbers for Q1 and Q2 just by looking at history of all hotel stocks. But this management could not see. Rather I will say they are having last laugh. Actually they don’t care. Because they know that public memory is very short. And don’t blame the CFO. They are green horns. They don’t know anything. They are being paid to say what management wants.

Small investors should avoid such management. And remember big equity dilution. We should dump the stock and move on. And to punish the management, let us spread words to avoid their hotels by all means. This management deserves a kick where it hurts and that can only be their finances. Once hotels run dry they will come to their senses.

Debt down to 130 crores with 10.75% interest rates

No Pledge

Negatives:

Poor execution. Even though Q1 is lowest checkout Indian Hotels, Samhi Hotels, they’ve posted amazing results considering Q1 and elections. Comparing with them because Kamat’s major keys are in Mumbai, Pune

Issue with clarification on NCD redemption timelines

Capex delays

Don’t know what was going on there but even an 8th grader can calculate 10.75% interest on 130 crores would be around 14 crores annually and 3.25 crores quarterly whereas the CFO never reached there and someone guided her there.

CEO hiding away

Exited as soon as results were out. Will wait for execution to pickup as it is still available at cheap valuations

On one hand I want to book my loss on this one, at the same time, the stock is at low valuations, more so after the recent fall. Technically also there is strong support at the current level. It might be worth waiting for the next quarter results but ofcourse these kind of shenanigans will limit any rerating potential even in case of good results.

please check praveg also, its better than kamat hotels.

its better in team, capex, margins and also in mcap 2000cr

kamat hotels has 500cr mcap only. it look risky and small, whereas praveg is bigger then kamat and in better condition rn.

They said owner was unavailable during concall but I can see constant posts since 12th Aug on his Instagram handle (which is public). My guy was posting pictures with parrots and doing Marathi podcasts and ducked the tough call. Also, did anyone actually email the CS (cs@khil.com) on any of the tough questions which the CFO passed? She sounded very frazzled and not confident at all.

So many tailwinds in hospitality sector that they need to try really hard to mess this up. Hoping that this was intentional to get favourable merger valuations and they would ramp-up the execution from Q2 onwards. Can’t see any other reason for the sudden capex on their Pune and Goa properties or maybe management hasn’t been completely honest on state of these properties.

Also, risk is that they will definitely not add 600+ keys in this year, more likely 300 which should boost revenues a bit with most of the profit margin coming from interest reduction so even with no re-rating, there can be decent upside. I have stopped calculating their interest costs as they make no sense to me and looks like even the CFO is clueless.

Still plenty of safety margin at this valuation that I’m not super concerned yet, waiting till Q2 results. The company has delivered on debt reduction and demand still outpacing supply + good weather + pickup of domestic travel.

CFO mentioned that their ARR almost halved due to low demand. This basically implies a severe lack of pricing and consequently brand power. Not good to hold in a downturn.

Key questions:

EBITDA margins: Basically impacted due to lower ARR.

23 Cr of capex is still left from 25 Cr so doubtful margins go back to previous levels.

How much lease expense that they’re going to incur?

Additionally, the issue is their ARR and keys growth

My old post deleted as I thought I can post my 4th reply by deleting my 3rd -

(Debt 57.00 cr redemption, so 14% int cost and 6% redemption premium amounts to 20% which amounts to 11.40 cr int cost which is what they considered and shown in the results.

Remaining debt of 130cr with 10.75% int amount to 13.98cr which which will be adjusted in the next 3 qtrs.

Basically she is not prepared for this basic maths or fumbled in the concall as she could not or cant justify merger. Looking from mgmts eyes., no mgmt will post rosy results when they want to do the merger in their favour, nor they want share price sky high which will make difficult for them to justify current merger ratio. So lets merger be approved at the earliest and I think mgmt becomes more transparent from then.

They posted 110cr ebita in fy23 itself, so posting 140cr ebita is not big issue with 2000+ keys which is 100% possible by yr end. So just we need to keep in mind that new equity is 3.3cr than 2.9cr}

So now my new comments on Kamat:

Kamat had 1510 rooms as of Apr 2023 and 1658 as of Apr 2023, an extra of 150 keys and revenue increased by 4 cr, so no question of ARR halving. Its more like less occupancy or a discount of max 10%.

Kamat had 53% occupancy as per q4fy24 inv presentation. By Jan 2025, 250 keys may be added and another 70 by Apr 2025. So extra revenue by extra keys only for fy26. But there is good scope to increase in occupancy and ARR if the demand is strong in q3 and q4.

Extra capex will be taken care of by another 21cr outstanding warrants amount, so this yr too they will be having other income not normal of around 25 to 30cr. Going forward, extra lease expense and slight increase in depreciation need to be considered. I think 400cr is possible in fy26 and if they get extra 200 keys, then mgmt can look for 430 cr to 450 revenue.