Hi @Deepesh_Punetha with reference to your questions i have read the annual reports and will try to address your queries as per my understanding. Obviously management will be in a better position to address the queries

1)The hotel land for orchid mumbai is owned by promoter entity (Plaza hotels) and is given on long term lease to kamat hotels. It is mentioned as owned as technically it is owned by group company but actually it is a leased hotel. Kamat hotels pays royalty charges to promoter entity.

2)Even though agreement will end in 2024 this agreement is extendable for another 30 years so it will be extended.

3)The royalty payable is basically for orchid vile parle mumbai which is based on the percentage of sales as decided by the board. It is basically lease expenses but it is paid as royalty so it would be accounted in other expenses and not as lease as per ind as.For FY23 it was 3 percentage of sales and for FY24 it was increased to 5 percent of sales. Going forward not sure what will this be. Maybe management can provide clarity.

4)Loan was given by kamat hotels to promoter entity (plaza hotels) at 20 percent which was the same rate at which the company had raised ncd’s. The loan was given to enable promoter entity to clear outstanding dues with prudent arc which was taken for construction of a hotel project in nagpur which the promoter entity was undertaking and which was to be handed to listed entity but this project was shelved.

5)The contingent liabilities are mainly income tax issues due to misreporting by the banks of loan settlement as the loans were assigned to arc’s and arc’s also subsequently reported it so as per the company it led to double counting of income by the it department. The company believes these dues are not payable and should be set aside by the courts so hence it has not provided for them. Also some expense disallowances were not admitted by the it department which the management feels is admissible and it is under appeal

In case you received any further update from the company kindly let us know

Overall i feel valuations are attractive and the legacy issues of debt have been resolved. Now the company is on a strong growth trajectory which would kick in from Q1FY25. Moreover expansion would mainly be through the lease route rather than management contract so this would significantly contribute to topline. FY24 was more of a restructuring year for the company so growth will start to kick in from this quarter.

As per the Q3 concall, Vishal Kamat ji was quite confident of achieving INR 100 crores of EBITDA, but there’s a miss by 10%.

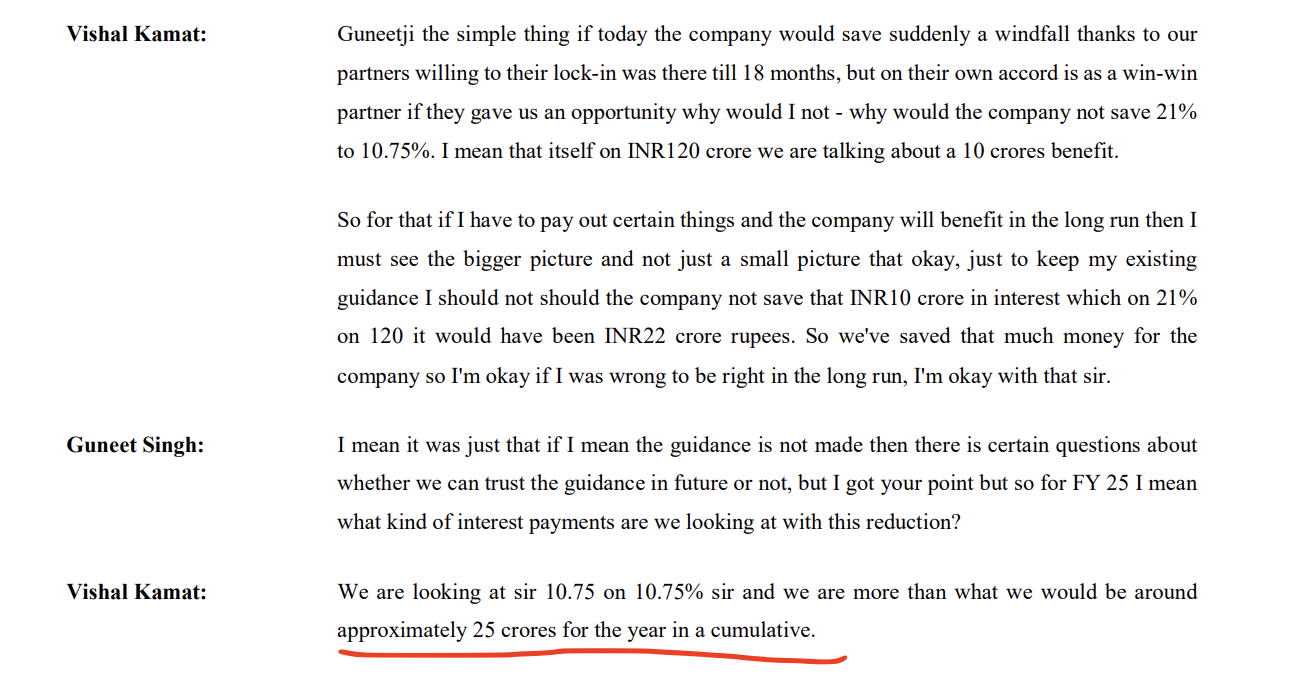

Although, on the other hand they also said that the debt will remain at the same rates till June or July but they’ve managed to bring it down to lower rater.

It was a bit disappointing that the management didn’t take the one off costs ( finance restructuring / statutory payments etc) in their calculations while giving the confident 100 Cr EBITDA guidance in the last concall held in Feb 2024.

This episode raises concerns on their guidance of 400Cr/140cr ebitda target for FY25. There will be one off costs in FY25 too considering the plans to add ~600 keys / ramp up of new properties, so will have to wait & watch.

While upfront investments in manpower/opex for upcoming properties is understandable, calling out the total one off expenses in Fy24 might have been prudent in their investor communication so investors have an idea of the normalized EBITDA.

Finance Restructuring cost will come under Finance costs and won’t be a part of EBITDA calculation. And I think it is good news that they’ve restructured the debt earlier then what they’ve mentioned.

Next year, bottom line should get better, even if everything remains same due to debt reduction and restructuring.

Couple of hotels were partially operational during last year and should be fully operational during this year + Multiple hotels have come online during Dec-23 to Apr-24 period which should contribute to topline. Even if they achieve 15-20% growth from here without messing things up, I’ll be very happy because it is cheaply available as of now.

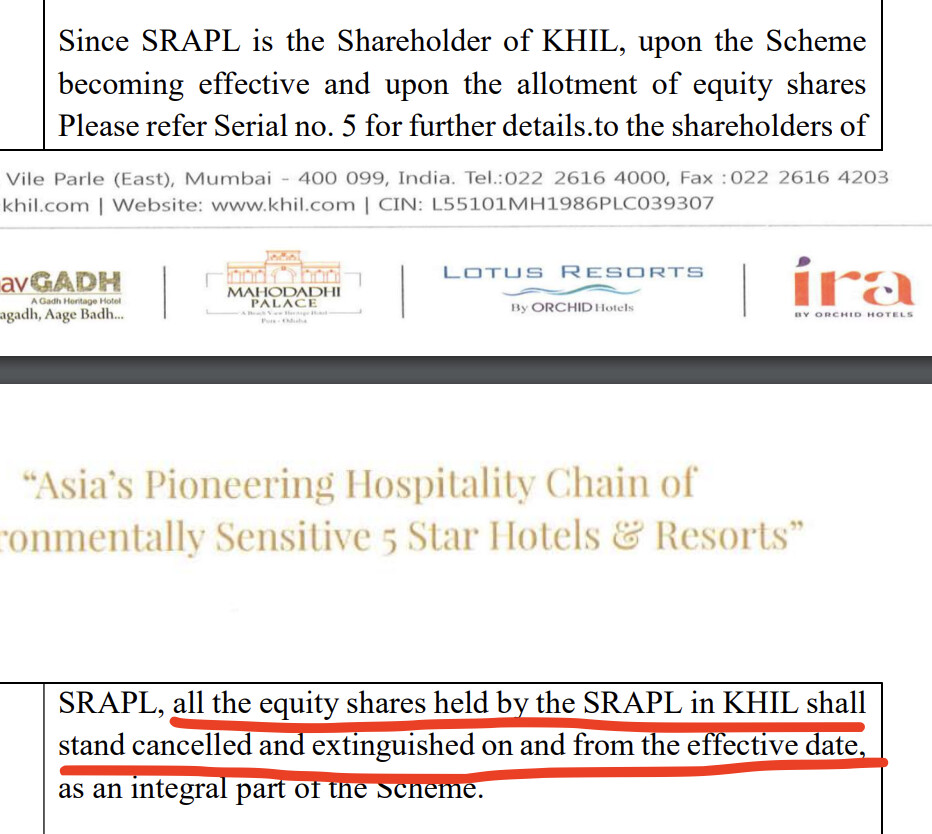

As per the filing today for the merger (link) nearly 44 lakhs new shares to be issued to the promoter group . As per the closing price of 260 /- today, the ascribed value of new shares issued is nearly 114 Cr.

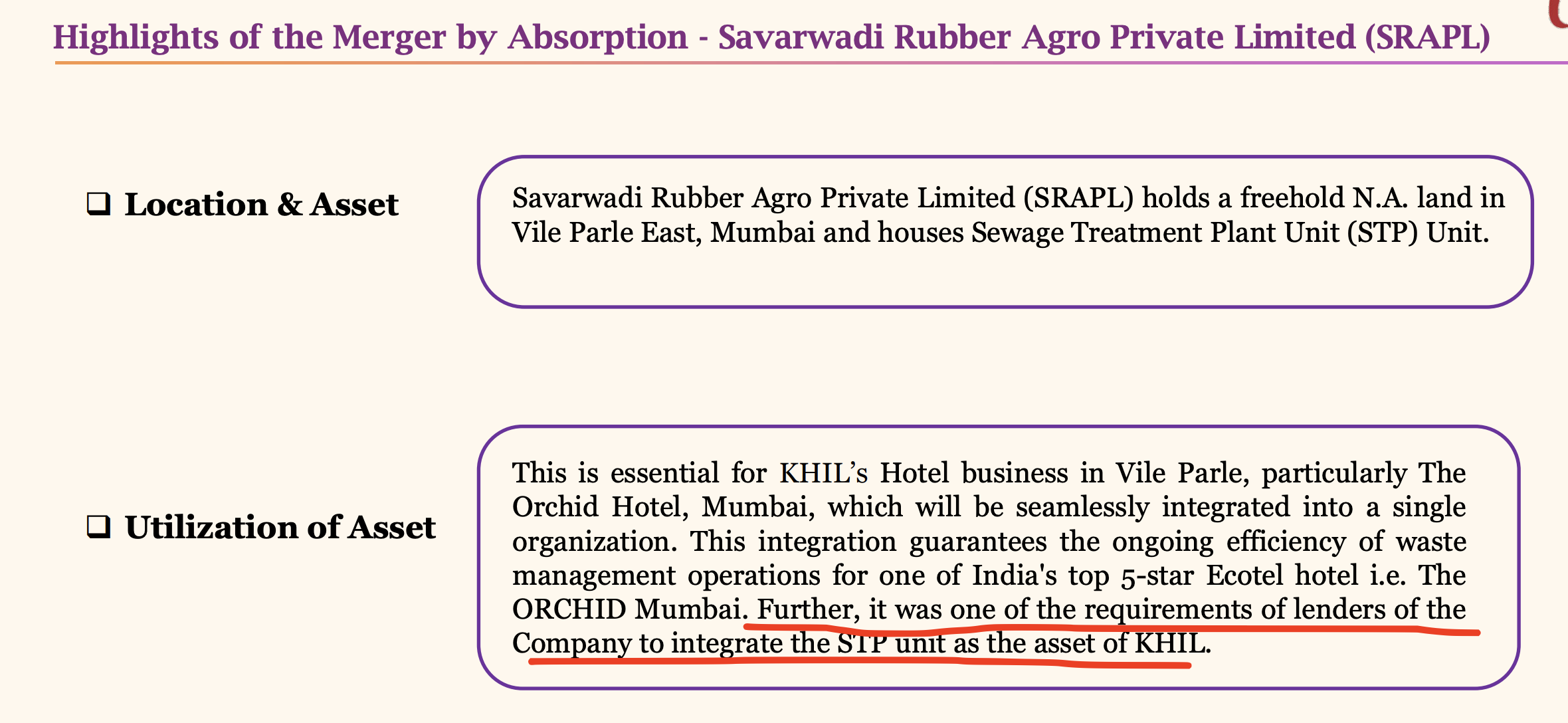

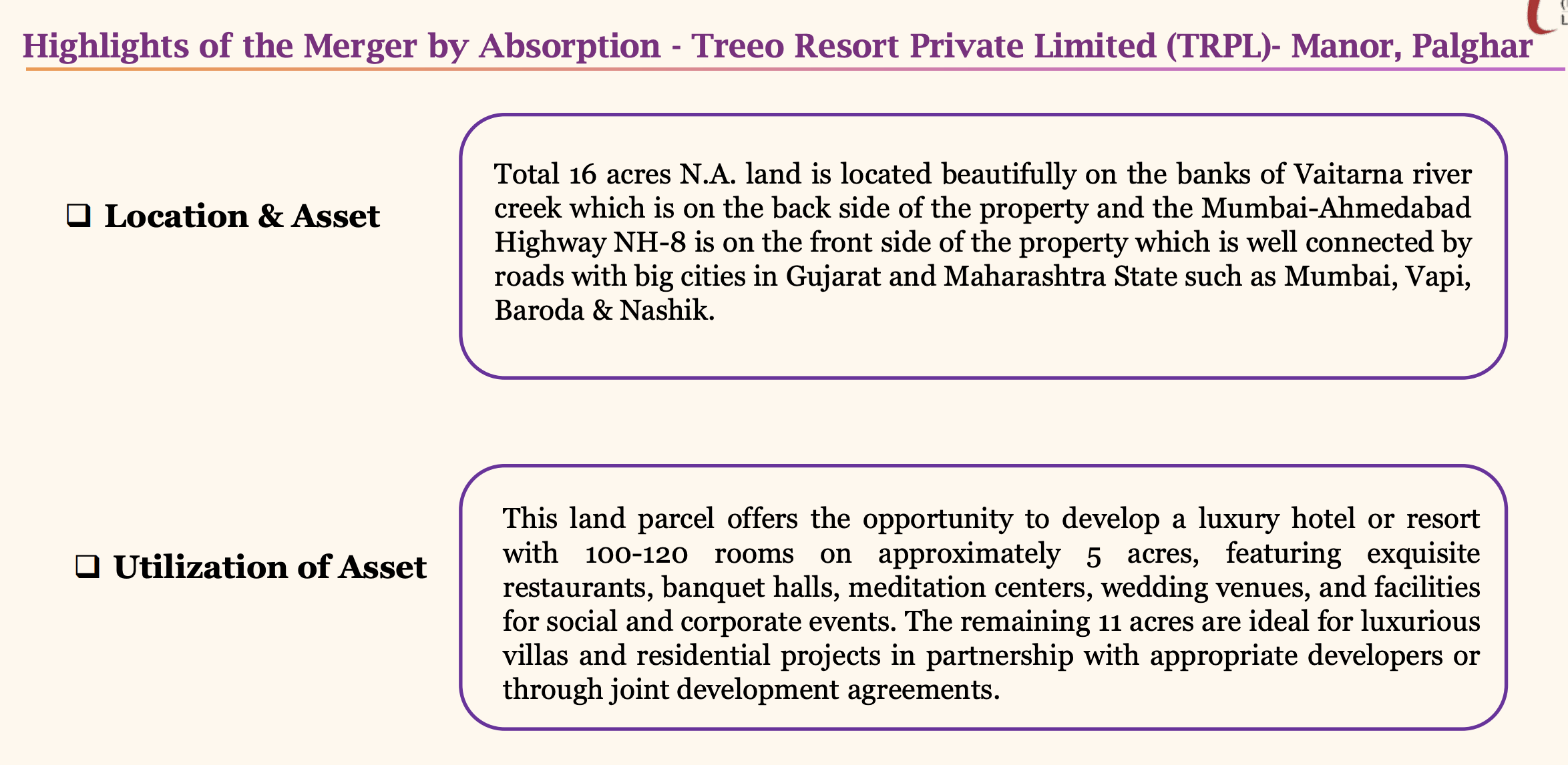

The last annual report mentions about the same that the STP was set up on the land of SRAPL in Vile Parle. The Orchid Vile parle hotel itself was inagurated in 1997 so its been nearly 27 years . Not sure if KHIL paid any amount earlier for the use of this land.

This is a 16 acre land parcel for which 75,000 x 20 (ratio) x 256 current share price = 38 Cr approx value , so approx cost of 2.4 cr/acre. This allows them to develop hotel on 5 acre and 11 acres can be for other real estate users

They probably want to use the 5 acre plot for themselves either for a hotel resort and maybe lease out/JV the remaining land to real estate developers.

FY25 profitability will be a turnaround for the company , 61 Cr odd finance costs will come down to 25 Cr odd → so minimum 25-30 Cr flow through to the bottom line . FY24 PBT was 24 cr odd, so just savings on interest cost could double the PBT. Now if the company does the growth as given in the guidance earlier, the jump would be even higher.

Now its a wait and watch if market rerates the business or not.

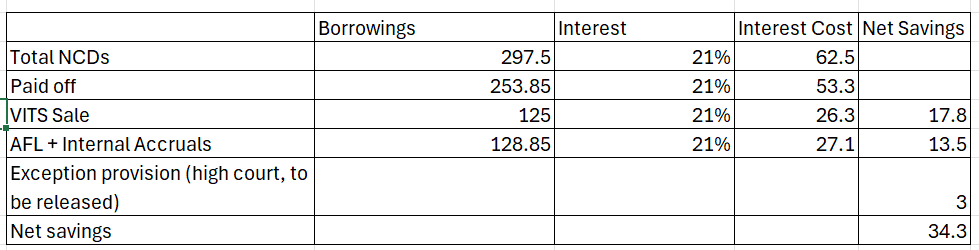

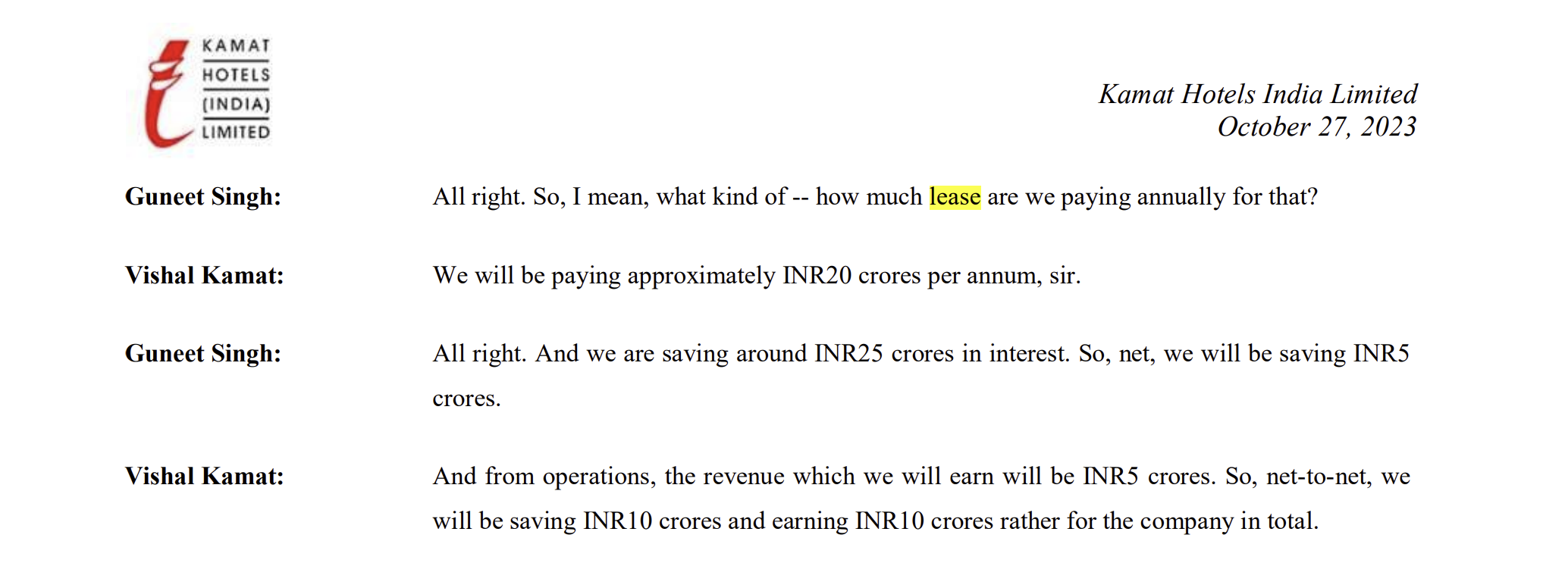

I think while focusing only on interest cost reduction, we are missing one thing. They have sold VITS Andheri for 125 cr which helped repay debt at 20% interest cost or around Rs 25 cr per year. But at the same time they have leased the hotel back from the new owners under a management contract and the lease cost is Rs 20 crs per annum. So on the Andheri hotel sale, the flow through to PBT is only Rs 5 crs and not Rs 25 crs.

So, assuming a base case of 30% turnover growth as guided and translating the same to PAT growth @ 30% (Management has actually guided an EBITDA growth of 50%+ which is not far-off, assuming 7% ARR increase, 10-15% occupancy increase but let’s be conservative)

I have a few queries - does anyone have any ideas on the same?

The remaining 58 Cr NCD were supposed to be redeemed with the warrant money and internal accruals over July /Aug - any idea when?

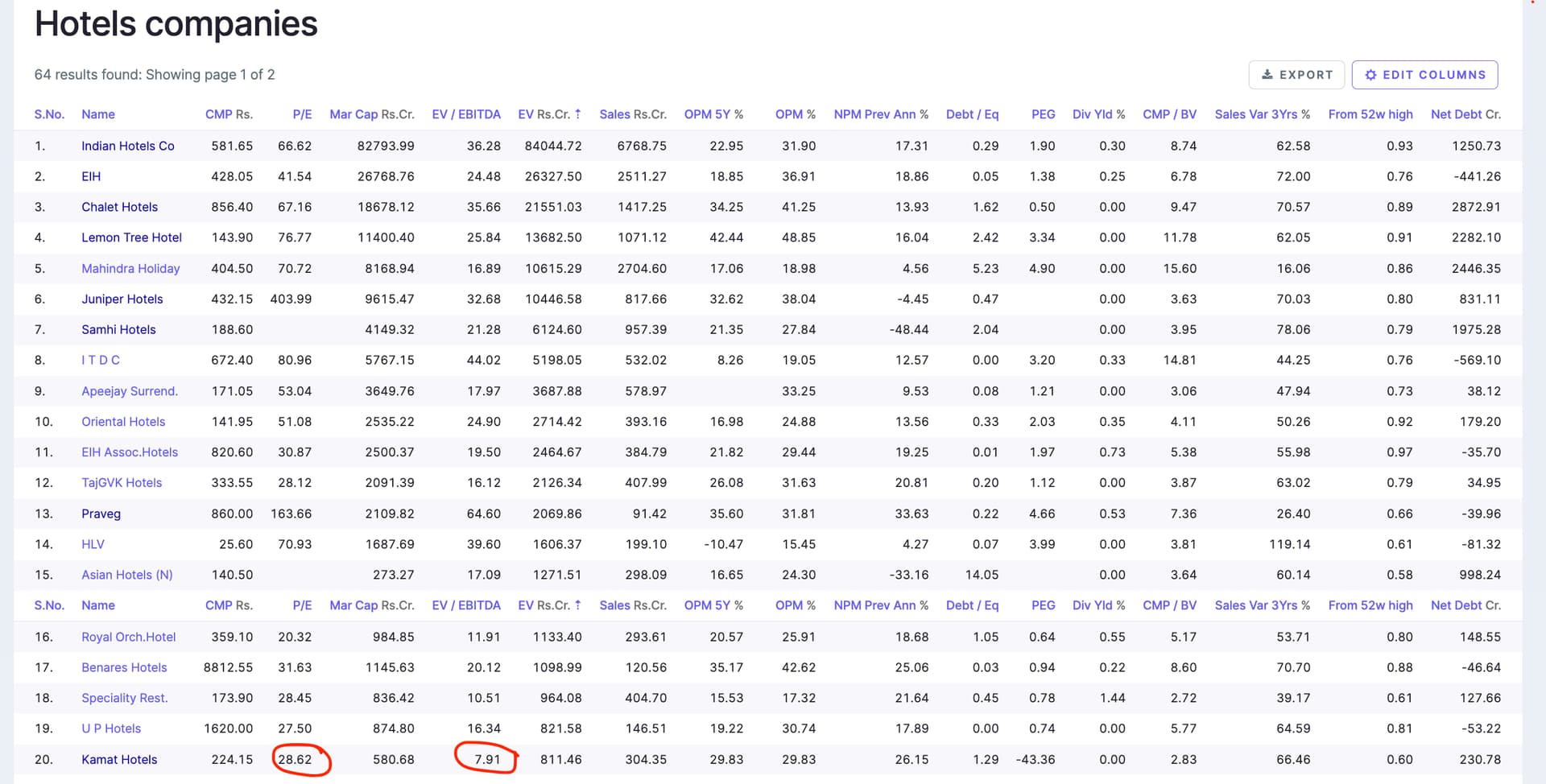

Management claimed that they are targeting 140 Cr ebitda in Fy25 → even if they achieve 120-130 Cr EBITDA, its available currently at <7x EVebitda for FY25. There is an overhang on the valuation multiple given by market currently , given the past issues on leveraged expansion etc. If they execute on their guidance and deliver, there might be a rerating?

Any idea of the depledging of promoter shares, given NCD’s to be repaid in full soon?

They might generate 40-50 cr surplus cash post repayment of NCD’s (one participant was mentioning total inflow of 120 Cr types in last concall), so has management indicated any dividend/buyback etc?

Disc: Invested and biased .

I was meaning to post a detailed analysis of this company for sometime now. Let me know in case of any feedback or something I can add to my analysis

What does the company do?

Company has 5 decades of experience in hotels, first hotel started in Mumbai

Headed by Vishal Kamat (3rd generation) since 27th May ‘23

Hotels:

16 in 4 and 5-star categories

1637 keys

372 owned, 36 on mgmt. contract and 48 in Goa is free holding meaning the company owns the hotel, land (currently used as collateral for loan)

Rest 72% are leased; model is asset light similar to LemonTree which has ~60% owned or leased hotels and similarly Indian Hotels also has 60% leased or managed

ARR: 6,500

Owns 5 brands:

Orchid: 6 hotels (5 upcoming). Ecotel 5-star hotel chain

– FY24 Occupancy is 55% from 75% in FY19, occupancy of other hotels in the 5-star segment is much higher – 72% for Lemontree and 80% for Taj. As per Kamat’s management, this is because a lot of their properties are small which doesn’t allow them to host large events

– ARR in this segment is expected to increase by 5-12% as per industry estimates. Kamat management has guided for 15% increase which seems aggressive

Ira (4-star): 5 hotels. New branding from July-23, earlier it was VITS

Lotus resorts (4-star): 3 hotels. Occupancy at 54% in FY24 from 50% in FY19

Fort Jadhavgarh (5-star)

– FY24 Occupancy is 40% from 55% in FY23: Larger hotels have an advantage of being flexible and being able to take more kind of functions so occupancy is a challenge here

– ARR is 8,364 increasing at 6% CAGR

Mahodadhi Palace (5-star): JV with 51% stake. 33 rooms currently, which will be expanded to 120

Why is Kamat Hotels a good investment?

This is a classic turn-around story with PAT to increase due to decrease in debt along with potential PE re-rating when compared to its peers in the hospitality sector.

Company took on huge debt for its Pune hotel and was unable to service it in 2014 due to slowdown in Indian economy, especially the hospitality sector

Debt reduction from 664 Cr in FY16 to 265 Cr in FY24

What will it turnaround or increase its earnings?

– Guidance of hotel sales and operating profit growth

1. Revenue: 315 Cr to 400 Cr in FY25 (27% increment)

2. EBITDA: Between 30-35% -> 130 Cr in FY25

Savings from balance sheet and other items

Levers for hotel sales growth

1. ARR and Occupancy increase

* ARR: FY25 company is guiding for 15% ARR increase (looks unlikely)

* Occupancy: Existing main hotels are already at their peak performance in terms of 85% for the year. Rest of the hotels are smaller and their occupancy seems unlikely to increase

2. New launches

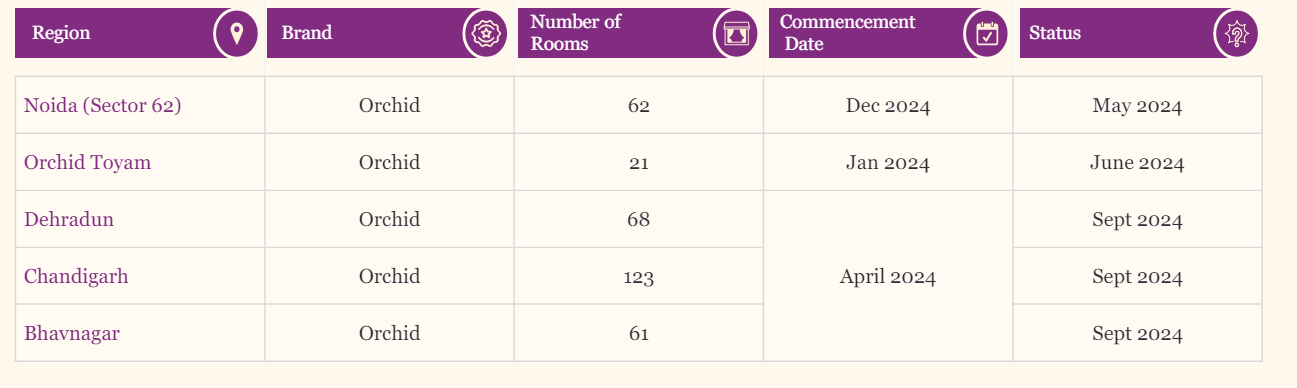

* Planned: 335 keys (20% increase) in 5 locations till Dec 24

Not yet announced: 300+ additional keys (addn. 20%+, so overall 40% increase) in 4 new locations (no launch date). 87 rooms to come from Mahodadhi Place in FY26

Adding new keys is easy because company only needs to invest in lighter material (linen, crockery) which is 0.3 to 0.7 Cr per hotel and other additional costs are manpower related

– F&B: Contributes 37% to sales

Financials

Debt: Interest expenses expected to decline by 53%

FY24

FY25

Interest rate

NCD-1 borrowing

297.5

43.65

21%

Interest on NCD-1 (till mid-Oct when VITS was sold)

44.3

9.2

Remaining Interest on NCD-1 (mid-Oct to Mar)

10.6

0

NCD-2 borrowing

27.5

27.5

21%

Interest on NCD-2

5.8

5.8

Alternate financing

0

128.85

11%

Interest on alternate financing

0

13.9

Total debt

325

200

Total interest

60.6

28.8

-53%

Company is paying lease of 20 Cr for VITS hotel

Warrants are due in July 24. So EPS will come down and PE will go up

5. Valuation:

FY24

FY25 (E)

YoY

Sales (as per guidance)

304

400

32%

EBITDA

91

120

EBITDA (%) – conservative est. considering lease and new keys

30%

30%

Other Income

12

16

Dep

18

18

Interest

60.6

28.8

PBT

24.4

88.7

264%

Tax

17%

17%

PAT (excl. exceptional items)

20.3

73.6

264%

PAT (%)

6.7%

6.7%

PAT + exceptional items + savings

45

73.6

64%

No. of shares (post warrant dilution in July-24)

2.95

2.95

EPS (excl exceptional items and incl. savings)

6.9

25.0

CMP

227

227

PE (current)

33.1

9.1

Exit PE (assumed)

30

Price (est)

749

Upside

+230%

Competitive analysis and industry benchmarking

Lemon Tree:

The number of people who use branded hotel rooms will grow 3-5x in the next five years. In China and Indonesia, around 2006-07, when they were at this point in their economy, hotel room demand grew over 22% every year

13% ARR increase in FY24

Management: “My forward view is, now I think the whole industry will wait for the upcycle, which is imminent in my opinion. At which point, you will see further significant hikes. Otherwise, typically, the hikes you will see will be depending on the market and depending on the quality of hotel, it could be anywhere from 5% to 12%.”

The first point is that the segment that took off first, because it had the lowest base, was luxury and 2 years lag, then mid-market took off. I think we are seeing the same thing in India. You will notice luxury operators are showing a much higher growth in ARR than the mid-market

What I can say is for Lemon Tree certainly, we will see at least a 15% increase in revenue every year for the next 3 years. And this will partly be led by ARR increase, partly by occupancy and partly by management contract business increasing. The minimum we expect is 15% increase.”

Company wants to be debt free in 4 years

In 2006, 2007, 2008 and 2009 until the global financial crisis, the average rate of Lemon Tree which did not have a Lemon Tree Premier, it only had Lemon Trees and Red Foxes, the ARR was Rs. 9,000. Actually, we are below what was there 15-18 years ago. And that is true, by the way, for every hotel company that had hotels there. There is an ability to reprice.

I do not see much competition very frankly because of a very basic reason, it is that demand is growing. When demand grows, then everybody runs like horses. It does not matter what you were in your previous avatar, but everybody becomes a racehorse. Obviously, there is competition in terms of similar hotels going after similar accounts and retail customers. I can sense the early tide of a rising wave of demand. And I think that’s going to quite distinctly get demonstrated in the next 15 months.

Mumbai, Delhi are large markets where demand will always outpace supply

IHL:

Experts like Horwath HTL have predicted that demand will grow at a rate of over 10-11% annually for the next 3 to 4 years. while the supply will continue to lack demand. Most of the future supply is expected to come outside of the key markets for non tier-1 cities

The ARR is really all about the part of the business, 47% of our business is room revenue. There’s everything else in terms of F&B, in terms of the asset light businesses, the banqueting, the chambers and a whole bunch of other things actually

CareEdge ratings:

It’s not just leisure hotels and resorts that are driving up and sustaining room rates—there is sustained demand for city hotels from the domestic business traveller, as well.

Amid all this, supply is estimated to record a compound annual growth rate of 4% to 5% over the next four-five years, said the CareEdge Ratings report, adding just 50,000 rooms to the country’s current inventory of approximately 160,000 branded rooms

With the above, at least the overhang of high promoter pledge/ balance sheet cleanup issues will be sorted. The only missing aspect is the revenue/ebitda growth , if the company delivers, might be rerated soon. Q1 results will set the baseline for Fy25 , historically the last couple of years has been sub 70 Cr, lets see what they deliver.

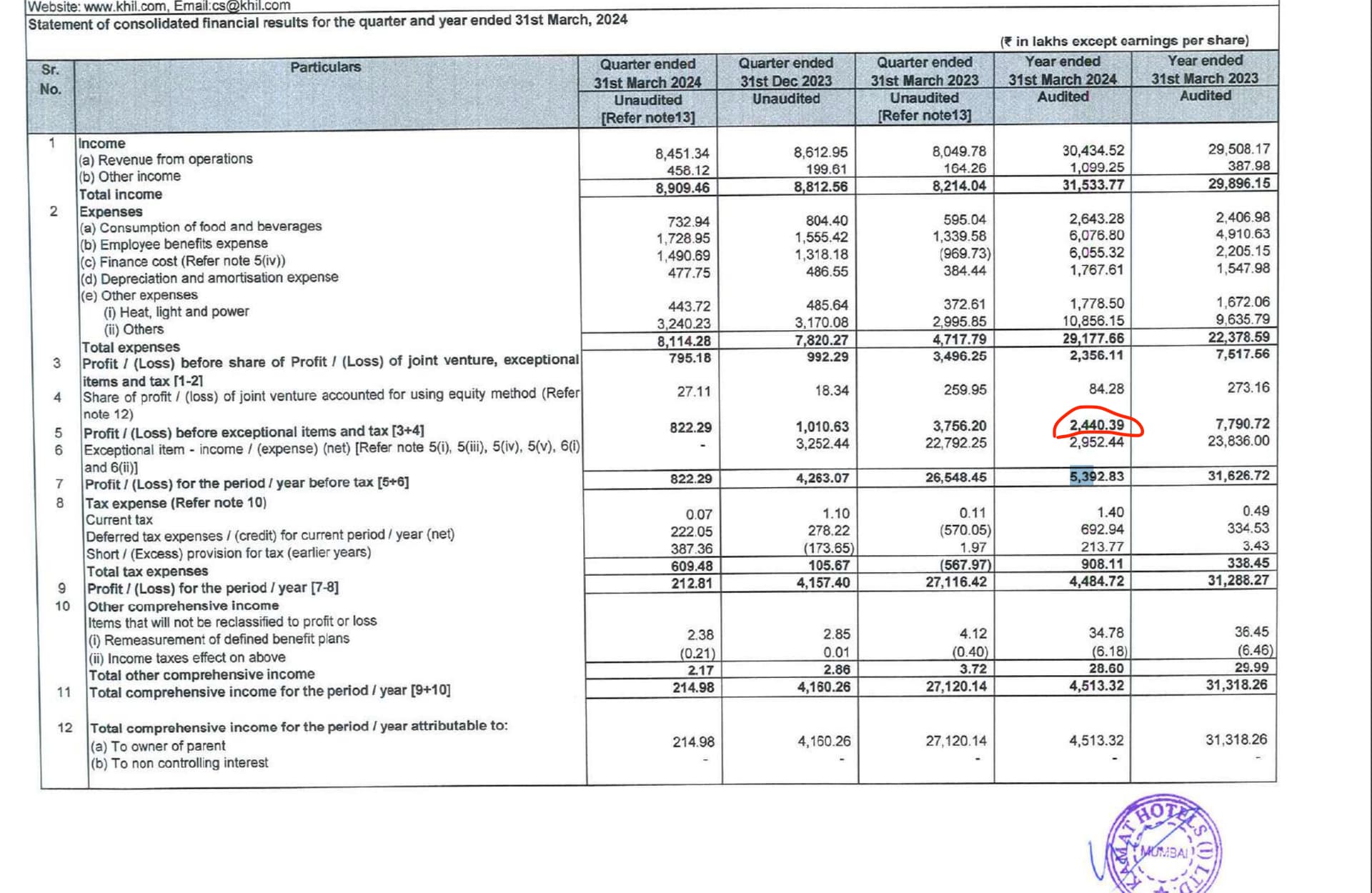

I am a little confused here. As per my understanding 71.15 Cr of NCDs (43.65 from NCD-1 and 27.5 Cr from NCD-2) was left. This clearance should only be a part of the NCD clearance or are they saying both the NCDs are cleared?

Company has certainly delivered on their promise of NCD clearance by July / Aug and their pledge has also cleared. Re-rating seems likely in the near future