Kamat Hotels -

Q2 results and concall highlights -

Revenues - 85 vs 64 cr, up 33 pc

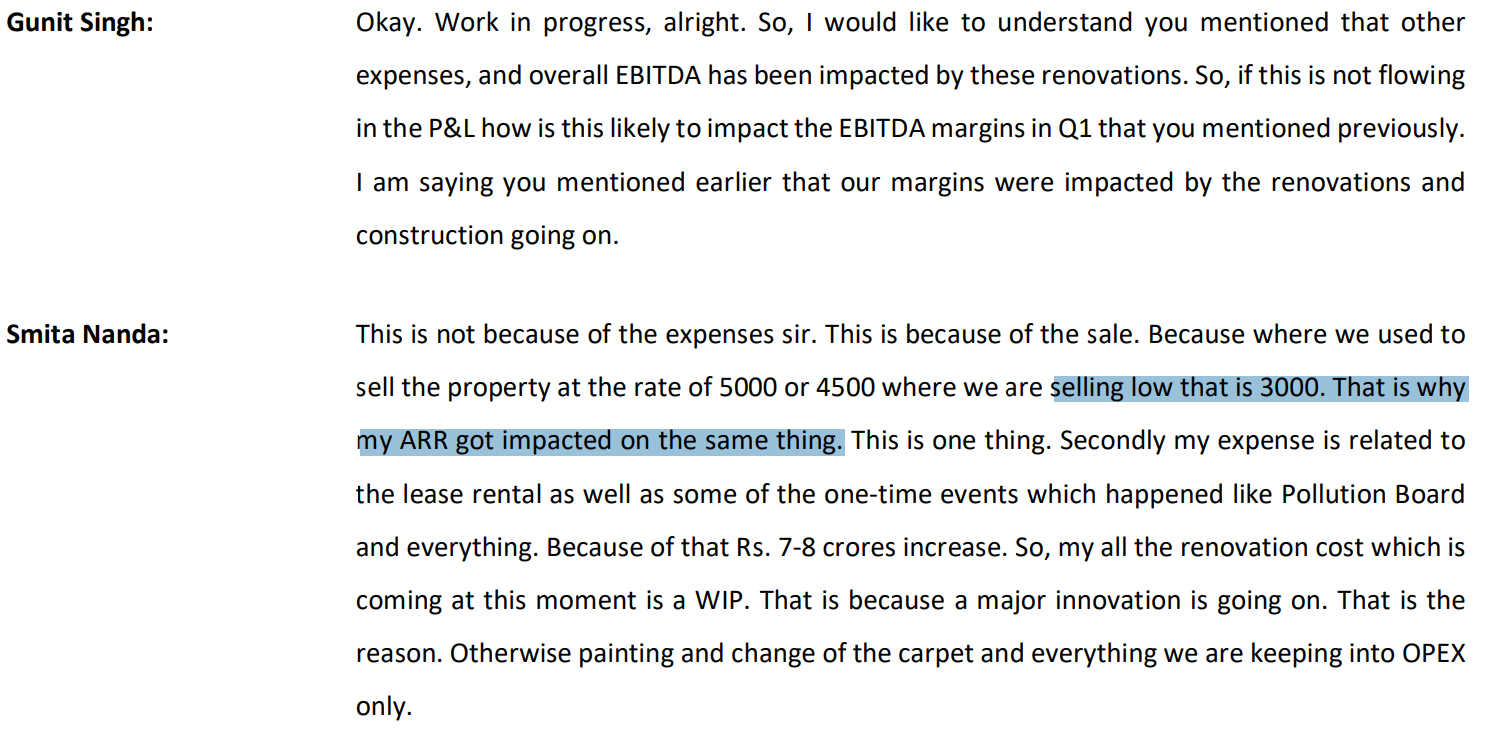

EBITDA - 22.5 vs 18.7 cr, up 20 pc ( margins @ 27 vs 29 pc )

PAT - 8.3 vs 0.03 cr ( due to sharp fall in interest costs - due repayment of loans )

Current portfolio of Hotels ( all hotels are leased except 02 which are owned and 01 on management contract ) -

Under Orchid brand -

Pune - 410 rooms

Mumbai - 372 rooms ( Owned )

Shimla - 96 rooms

Manali - 47 rooms

Goa - 48 rooms ( Owned )

Lonavala - 36 rooms ( management contract )

Jamnagar - 45 rooms

Toyam ( Pune ) - 21 rooms

Under IRA brand -

Mumbai - 195 rooms

Bhuvneshwar - 111 rooms

Nahsik - 31 rooms

Sambhaji Nagar - 33 rooms

Ayodhya - 49 rooms

Lotus Resort Murund - 40 rooms

Fort Jadhavgarh Pune - 58 rooms

Madhodhani Palace Puri - 33 rooms

At present - capex ( addition of rooms / facilities ) and renovation work is on at Orchid - Pune and Goa

Upcoming properties -

Under Orchid brand @ Chandigarh, Dehradun, Gwalior and Puri

Under IRA brand @ Bhavnagar, Hyderabad and Noida

Most of these properties are likely to open up in calendar year 2025

Aim to keep upgrading / renovating 2 properties each year

Current debt on books @ 120 cr with RoI of 10.5 pc

Expecting to maintain EBITDA margins in H2 - at levels similar to Q2 - due increased manpower and energy costs

Expecting to clock revenues of around 350 cr for FY 25 with full FY 25 EBITDA > 90 cr

37 pc of company’s business comes from repeat customers ( which is a very healthy number ). As the company expands its number of properties, this percentage should increase going forward

IRA Noida is opening on 07 Nov 24

Company expects their finance cost to be between 6-7 cr for Q2 - this should be a key positive and bump up the PAT in Q2

Revenue target for FY 26 stands at 400 cr

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation