Hi All,

I have been following this company for sometime and it looks to be good turnaround story. Established in 1986 Kamat Hotels India Ltd. has an illustrious past, troubled present and a probable bright future in its hospitality ventures. The Group is headed by Dr. Vithal Venkatesh Kamat and is joined by the next generation, Mr. Vishal Kamat and the host of Professional team members.

THE ORCHID, a 5 star Ecotel Hotel in Mumbai is their flagship hotel and currently the backbone holding them together in the financial mess. Alongside this, they have another hotel under the brand name VITS in mumbai which is also doing fairly well. Both these hotels are located in close proximity to Mumbai Airport. Unfortunately, the other hotels of the group aren’t performing as per the plan and have dragged them under debt burden.

Kamat had built a 5-Star hotel under the Orhcid brand name in Pune to serve the demands of Common Wealth Games but the venture didn’t take off. Consequently, with increased debt on books and a slowdown in the hospitality industry (falling ARR & Occupancy rates) left them with losses and surrounded by CDR Issues. Later, the PE firm Clearwater Capital (which had invested $18 million in Kamat’s FCCB) also exited their investment in the group by taking a huge write-off.

However, in FY17 Kamat has again turned profitable and has pared its loan to Rs.410 Cr from Rs. 570 Cr. and is looking to bring it further down to a more comfortable level. Group has several properties which can go on block and raise the funds required to repay the lenders. Management has shown its intent of restoring the lost financial prosperity.

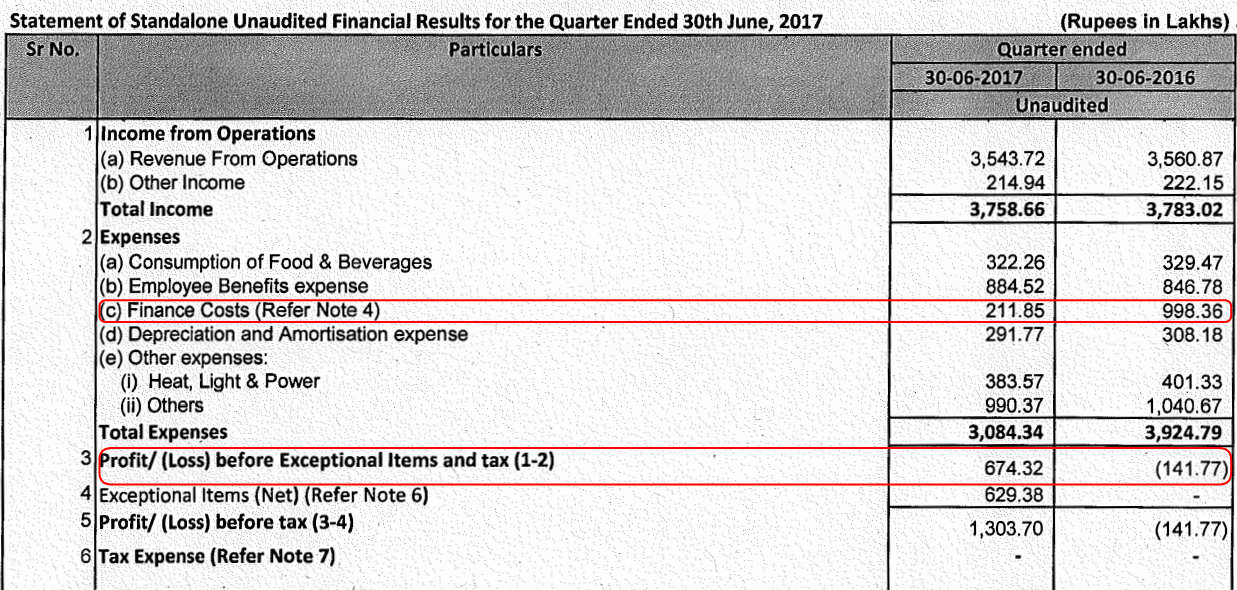

With improvement in occupancy rate, ARR (see tables below)- EBITDA levels and gradual reduction of debt makes Kamat a potential candidate for a turnaround story.

You can read few news articles using the link below to get a better sense of the story.

http://www.thehindubusinessline.com/companies/kamat-hotels/article9627792.ece

Management Interview: Expect To Be Profitable In FY18: Kamat Hotels - YouTube

To summarize, the story has 2 key pillars- improving EBITDA levels and reduction of debt, currently both of these are complimenting each other. If the company is able to continue on its streak of reducing debt with internal accruals and a better deal from its lenders the results will be quite favorable. On the other hand, the exact same thing when looked from different vantage point will serve as the risk highlight.

Hence, this aspect of the story will serve both as an opportunity as well as the risk and I therefore request the forum members to share their thoughts and valuable insights to take the discussion forward.

Regards,

Yogansh Jeswani

Disclosure: Invested.