what about kamat result

Disc:- invested

what about kamat result

Disc:- invested

Hi yogansh,

It looks difficult to repay debt of 174cr in 2 years…

do you have some calculations of how much they can pay back and expected earnings of next 2/3 years…i think maximum they can pay 35cr say this year and if very good 40cr next year so still they will have lot of burden

A recent interview of Mr. Vishal Kamat.

http://www.fnbnews.com/Interview/in-kitchen-it-is-ultimately-chefs-skill-41826

Regards

Krishna

Some interesting insights on the current uptrend in hotel industry

Regards

Krishna

To better understand the hotel industry and its capital cycle one should go through this. Very well writen by @rohithpotti

Latest interview of management on Bloomberg.

Follow the tweet - https://twitter.com/BloombergQuint/status/975650665954361344?ref_src=twcamp^copy|twsrc^android|twgr^copy|twcon^7090|twterm^3

Latest management interview on the hotel industry trend and what we can expect on occupany front.

Though, Vishal didn’t comment on how they are planning to reduce cost, improve margins and reduce debt. The commentary overall for the hotel industry was upbeat.

Q4 Fy18 results

https://www.bseindia.com/xml-data/corpfiling/AttachLive/451aab9e-9560-47d9-a7ce-987dcc7f021e.pdf

Standalone results look good but didn’t understand the loss due to impairment at consolidated levels.

If someone could throw some light on the same.

Regards

Krishna

Looks like ICICI Bank had sold the loan to ARC and the ARC wants the company to sell of ORCHID Pune and during this the assets were noted to have recoverable value lesser than the previously mentioned book value due to which the impairment.

Step in that direction.

Kamat Pune Property Transfer.pdf (44.5 KB)

Decent nos from the company - https://www.bseindia.com/xml-data/corpfiling/AttachLive/367911db-621c-44c0-b8bf-e8bb7387f732.pdf

Anyone has any update on their plan to sell Pune property?

any update in kamat hotel

disc-invested 80% of portfolio

It can be a good buy above 55.3

CUP and HANDLE Breakout might take place.

And current market cap is Rs.75 Crs.

PRASHANT

Kamat hotels came up with very good numbers in Q1FY23 (EPS of 5 Rs) in line with all the hotel companies. Can this be a turnaround candidate? Haven’t been able to find much on the company in recent times.

Hello everyone,

The thread has been inactive since a long time now but I have been tracking the company and there is a recent development which might get interesting if it works out.

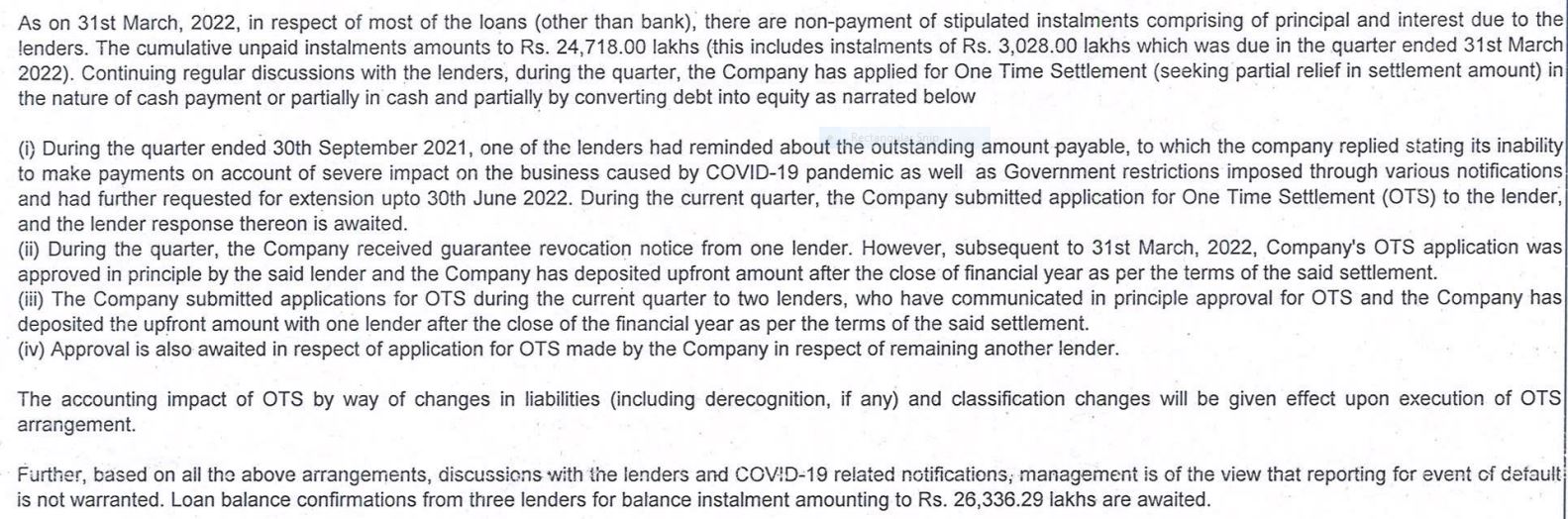

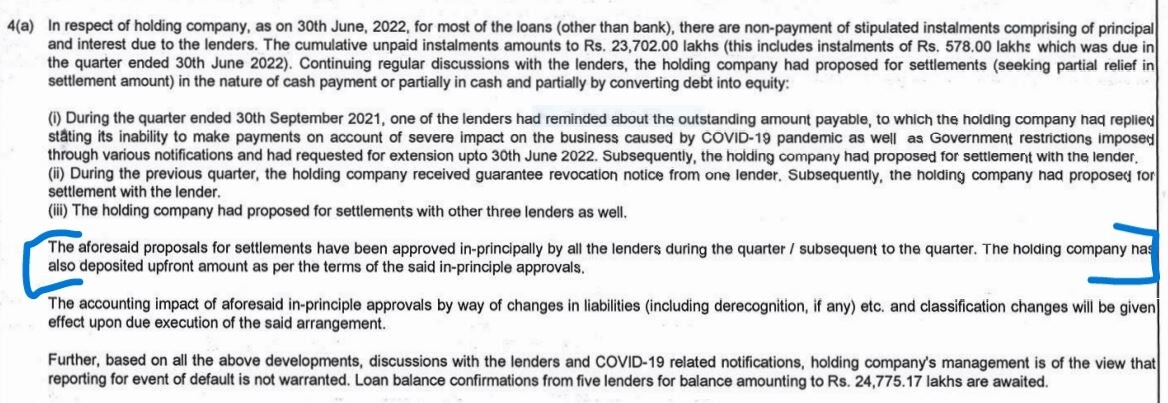

We all know co. got into unsustainable leverage situation due to their Pune property- OHPPL. That one bad capital allocation decision undertaken by the management caused stress on balance sheet of standalone entity which otherwise was a stable 180 Cr annual topline business with average EBITDA and CFO of 60 Cr.

While these OHPPL loan which was bought by IARC(blackstone funded ARC) from ARCIL for Rs.135 Cr in 2018 but still remain unresolved and is a significant monitorable for the company going forward.

However, a new development was mentioned in March’22 quarterly results wherein co. applied for OTS on standalone entity for the first time and in June’22 quarterly result they got in principal approval from all the lenders involved in standalone debt. This debt is around 300 Cr and any haircut here would help the co. to bring down the debt to much more servicable level (given 60 Cr annual EBITDA and CFO)

I am attaching snippets from the quarterly results for further clarification.

While timeline for the OTS needs to be closely monitored in my opinion. I am looking forward to feedback of other members tracking the stock and how do they perceive this development.

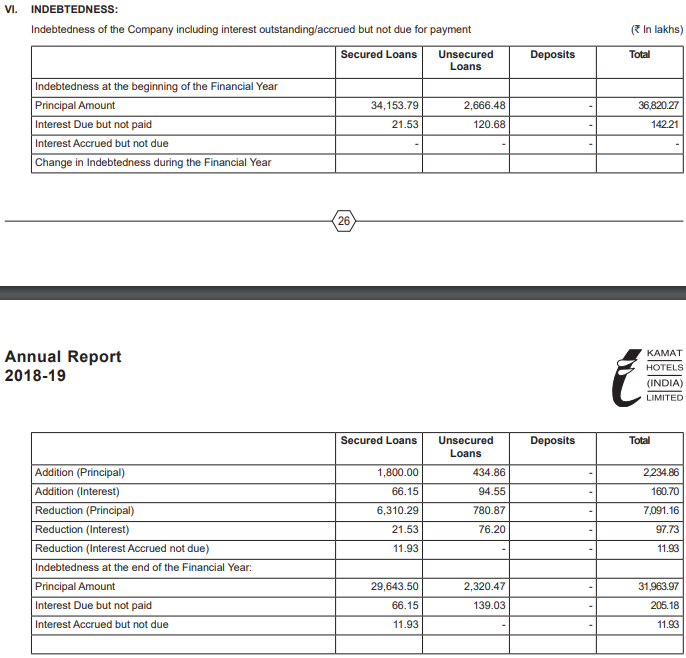

Snippet from notes to accounts of Q4FY21 quarterly results:

Q1FY22 wherein they mentioned of approvals from all lenders for OTS:

Disclosure- Invested.