Basically , i am medico person, though i will try my best to explain you

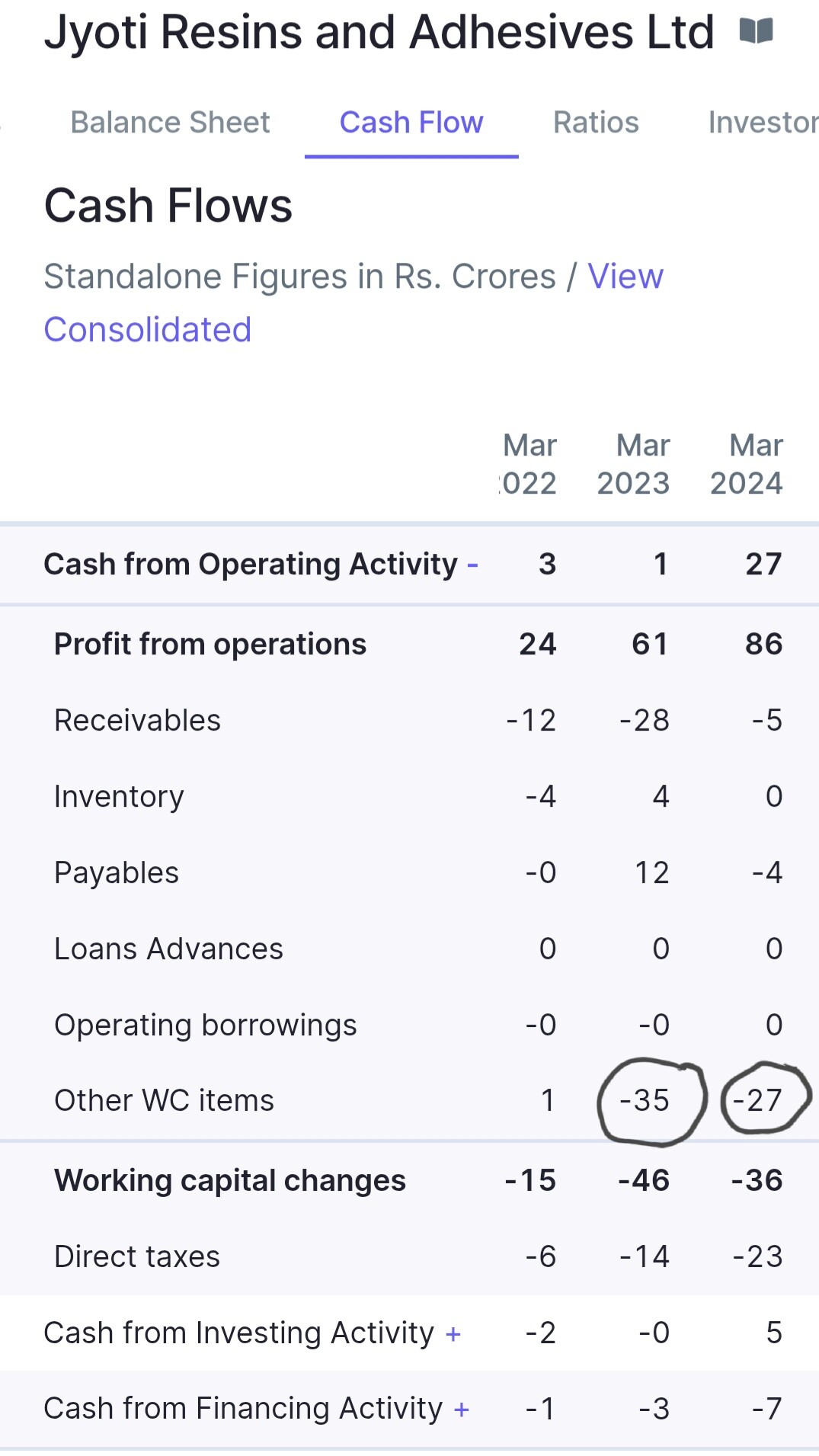

1…Depreciation

=When we calculate net profit ,we deduct depreciation from revenue .However actually we are not losing any cash(non cash expense). So depreciation is added back for calculation of operating cash flow.

2…Receivables ,inventories

=While calculation of net profit, these are not considered. However, they affect actual cadh flow from operation.

=Lets take an example.

Suppose,

A …We have revenue of Rs 10,000 for selling some goods. Cost of goods is Rs7000

B…We have receivables of Rs 1000

C…We have unsold invenoties of Rs 1000

So

A…We have net profit Rs 3000(10000-7000)

B…But we dont have actual 3000 cash

Actual cash flow from operation will be Net profit-receivables-inventories=1000

3…Payables

=Sameway payables will be added to profit for calculation of operating cash flow.

In short, depreciation will affect net profit

While working capital(receivable, payables, inventories) will affect OCF(Operating cash flow)

And for calculation of OCF, receivables and inventories are substracted form operating profit

While payables and depreciation will be added.

Hope ,this will help you