Thanks  also what about the diketene ?

also what about the diketene ?

1 Like

Hello Value Pickrs

i have made a video on Jubilant Ingrevia. Do watch and share your views

Jubilant Ingrevia detailed Analysis

Thanks

6 Likes

HDFC Securities initiates buy…

Disc. INVESTED

3 Likes

Hi all,

Jubilant Ingrevia recently met twice with a state commission regarding capex plans for their dyes / intermediates. This proposed expansion is at Gajraula.

If you remember my posts from a few months ago, I had two broad concerns:

- Is Jubilant Ingrevia complying with environmental clearance norms?

- Is there a risk from pollution control boards for any breaches?

Their letters to the state authorities have some really positive information regarding compliance.

In 2019, the NGT had called out Ingrevia for violating air pollution norms at Gajraula. Here’s a sample

As per the analysis result of ambient air quality monitoring […], PM10was found to be 132.1 pg/m3 against notified standard limit of 100 pg/m3.

Ingrevia is carrying out tests every six months, and this is the most recent quality assessment carried out a few months ago:

All the emissions are currently well within the allowed ranges. Particulate matter emissions are down 43% since the notification. This means in the last two years, they have listened to the NGT and have really improved quality standards.

The second data point that is important is that the testing was carried out by an independent group that has several large clients such as Coca Cola, ITC, Tata Steel, Teva, Ultratech, etc.

All this points to a significant improvement in environmental compliance, and a reduction in probability that pending environmental clearances will face impediments. The proposed expansion relates to doubling formaldehyde, pyridine and picoline capacity. The diketene value chain is also produced at the plant.

I’ve been following the story at Nira too, since their EC is due for renewal in a few months. They were given a show cause in June by the board, but got the consent to operate towards the end of August.

Cheers ![]()

34 Likes

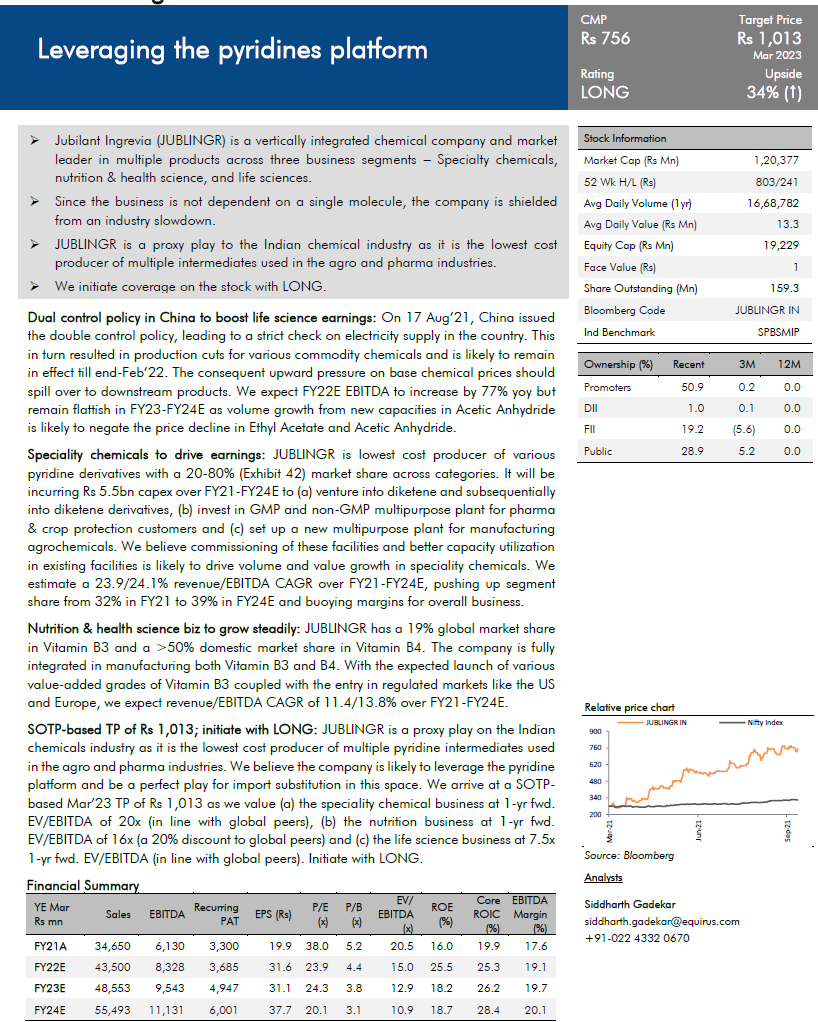

There was a detailed research report (>50 Pages) released with good outlook and insights on all the products of Ingrevia on 30th. Attaching the summary page of the same below for reference.

10 Likes

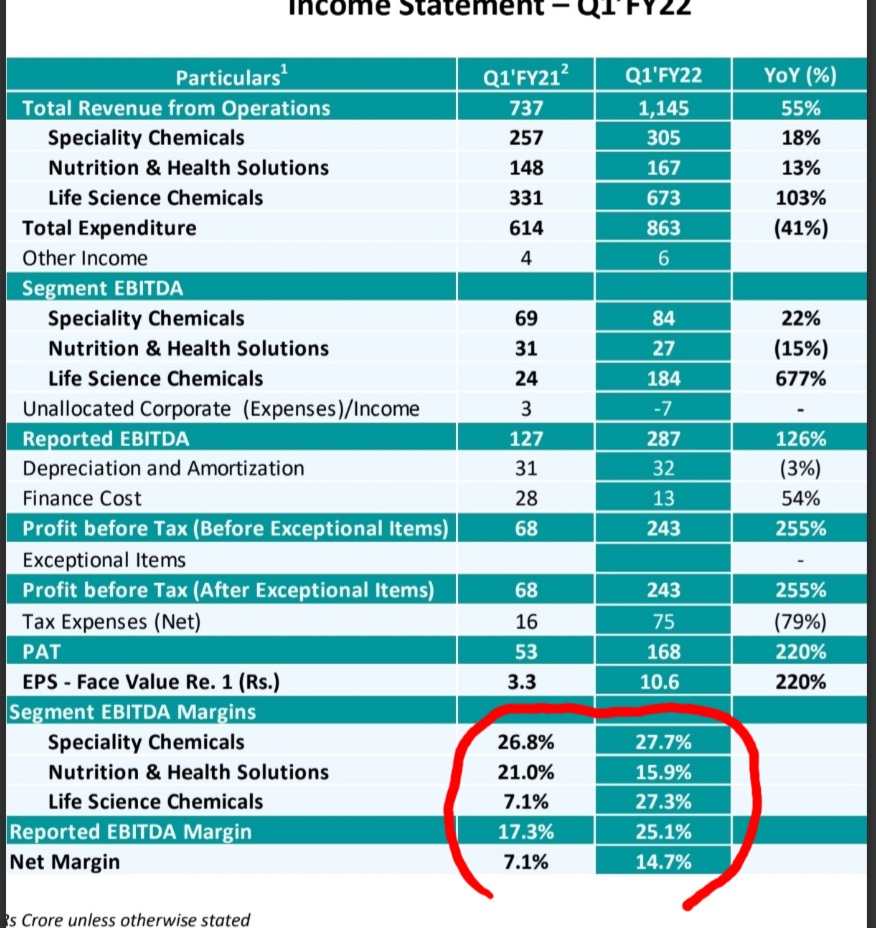

As per the report, why is the EPS figure for FY 23 the same as FY 22 even though the estimated PAT is much higher?

As I understand, this is bcos they are getting one time profit due to disinvestment of 10% of their holding in “Safe Food Corporation” for 132 crores

2 Likes

Chemical Manufacturers in China have been impacted by Power Disruptions

BY LUCIE BENN ON OCTOBER 2, 2021

China’s Chemical sector is seeing a profit rise, but the country’s sustained success is jeopardized by widespread power outages and the country’s efforts to reduce carbon emissions.Earnings in the chemical sector increased by 145% in the first eight months of the year, nearly doubling the average industrial profit gain- says China’s National Bureau of Statistics.

However, the run may be coming to an end. At least a dozen Chinese Chemical businesses, ranging from fertilizer makers to polyester fiber firms, have declared production curtailments owing to a scarcity of energy in recent days.Furthermore, on September 23, the US Company Celanese announced force majeure for numerous polymers after being compelled to close acetic anhydride and vinyl acetate plants in Nanjing, Jiangsu Province, to comply with government directives.

!(data:image/svg+xml;base64,PHN2ZyBoZWlnaHQ9IjIwMCIgd2lkdGg9IjMwMCIgeG1sbnM9Imh0dHA6Ly93d3cudzMub3JnLzIwMDAvc3ZnIiB2ZXJzaW9uPSIxLjEiLz4=) According to China PetroNews, power outages might affect hundreds of Chemical plants across the country.According to the magazine, executives from numerous chemical businesses in Jiangsu Province, Inner Mongolia, and Ningxia are complaining that the inconsistent electrical supply is affecting maintenance, feedstock loading, and production safety.

According to China PetroNews, power outages might affect hundreds of Chemical plants across the country.According to the magazine, executives from numerous chemical businesses in Jiangsu Province, Inner Mongolia, and Ningxia are complaining that the inconsistent electrical supply is affecting maintenance, feedstock loading, and production safety.

Firms in the eastern provinces of Jiangsu and Guangdong, which are home to many of China’s Chemical manufacturers, are suffering the most, as these provinces have failed to meet the central government’s dual targets of reducing energy use per capita by 3% per year and controlling total energy consumption growth.The energy reduction objective, which is linked to China’s overall carbon emission reduction goals, is merely one of the causes of power outages. Furthermore, with coal costs soaring and government-capped energy rates, China’s power firms are hesitant to produce additional electricity at a loss.

Published in News and Power & Energy

THIS COULD HAVE A POSITIVE IMPACT ON JUBILANT INGREVIA

9 Likes

Its for Captive use and to meet the green energy needs and optimize energy cost and to comply with the regulatory requirement for captive power consumption under the electricity laws.

3 Likes

On the contrary is it also not that the raw materials/KSMs dependent on china has also become expensive and therefore, leading to margin contractions

1 Like

Looks like nobody is talking about the coal. Apart from the high input costs (Acetic Acid), logistics issues, there is steep rise in international coal prices.

This is what management has mentioned in the latest AR about the impact of the coal supply and prices:

The coal supply from Coal India as well as international markets were adequate and prices were soft. This helped us contain our steam and power cost. However, in Q4 FY 2021, imported coal prices have gone up significantly, thus, impacting couple of our plants.

Since then the situation is aggravated and now there is coal shortage in India if the media reports are to be believed.

So in my view there may be multiple headwinds for Jubilant Ingrevia to take advantage of Chinese power crisis (at least for the short term). We may need to wait for the management commentary to get some clarity. However I am super bullish on long term prospects of the company

Disc: Invested and biased. Not a SEBI registered advisor. Do your own due-diligence before investing.

13 Likes

Good result:

Raw materials impacted margins slightly. Expected to be passed on as per info provided

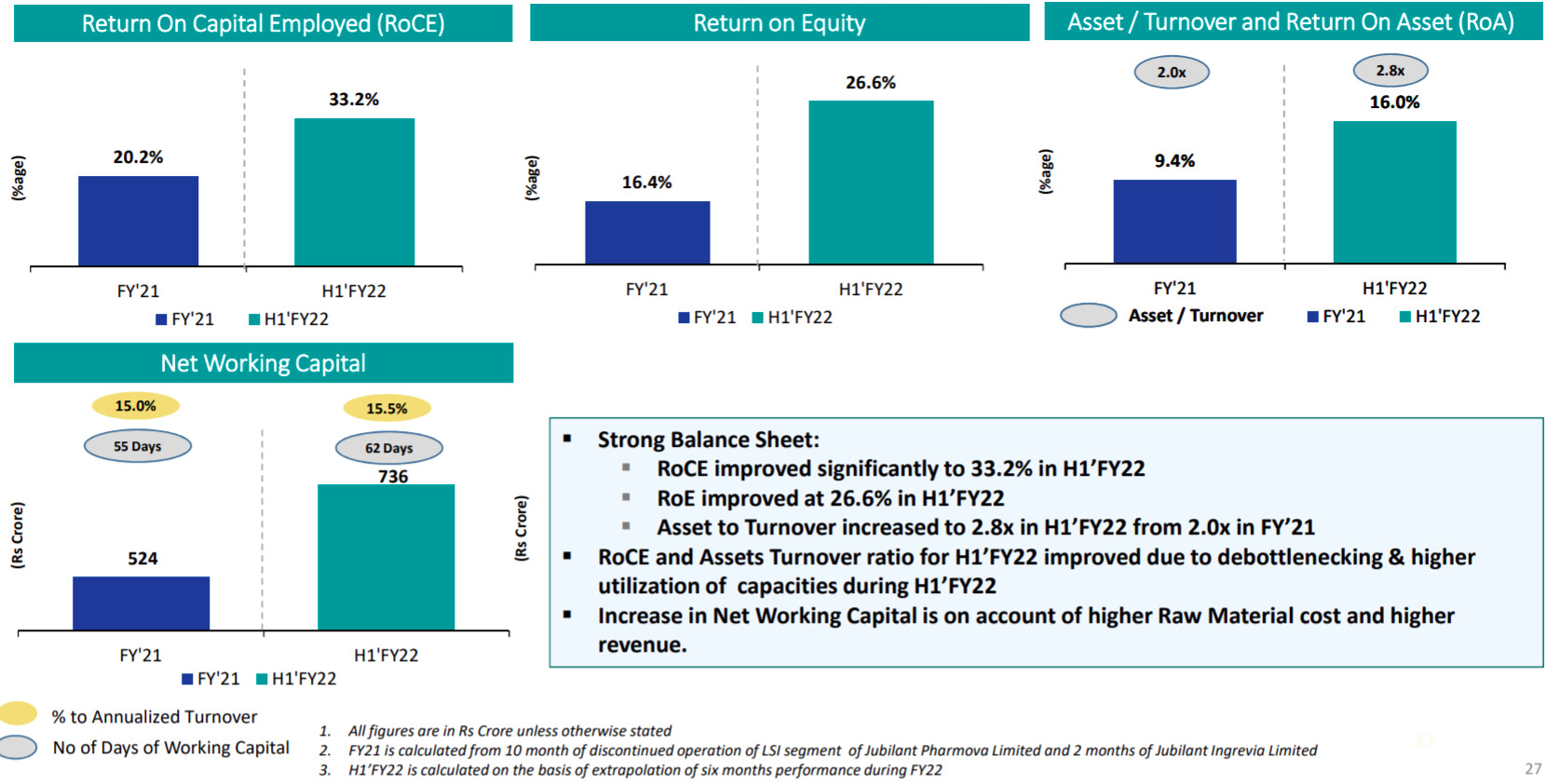

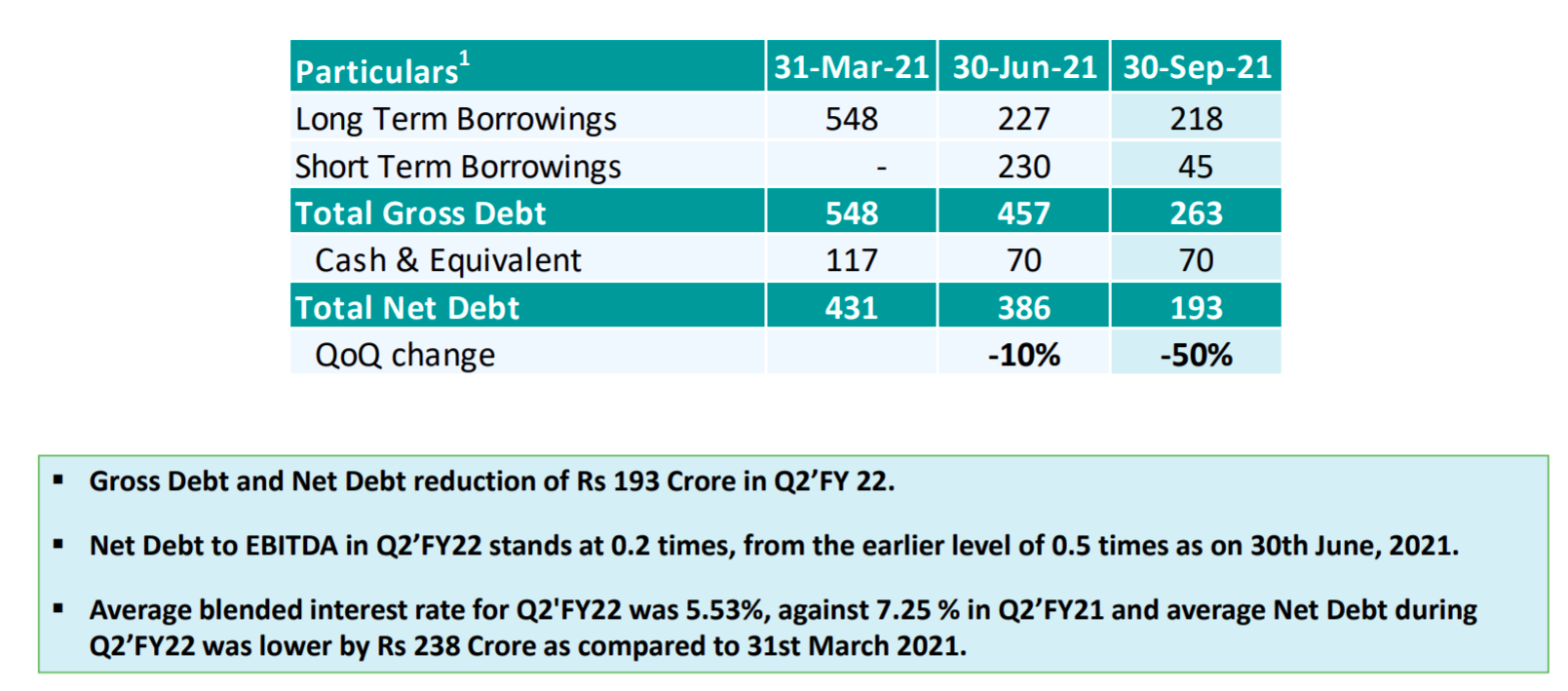

Decent Improvement in Balance sheet metrics ROCE & ROE & Debt levels

13 Likes

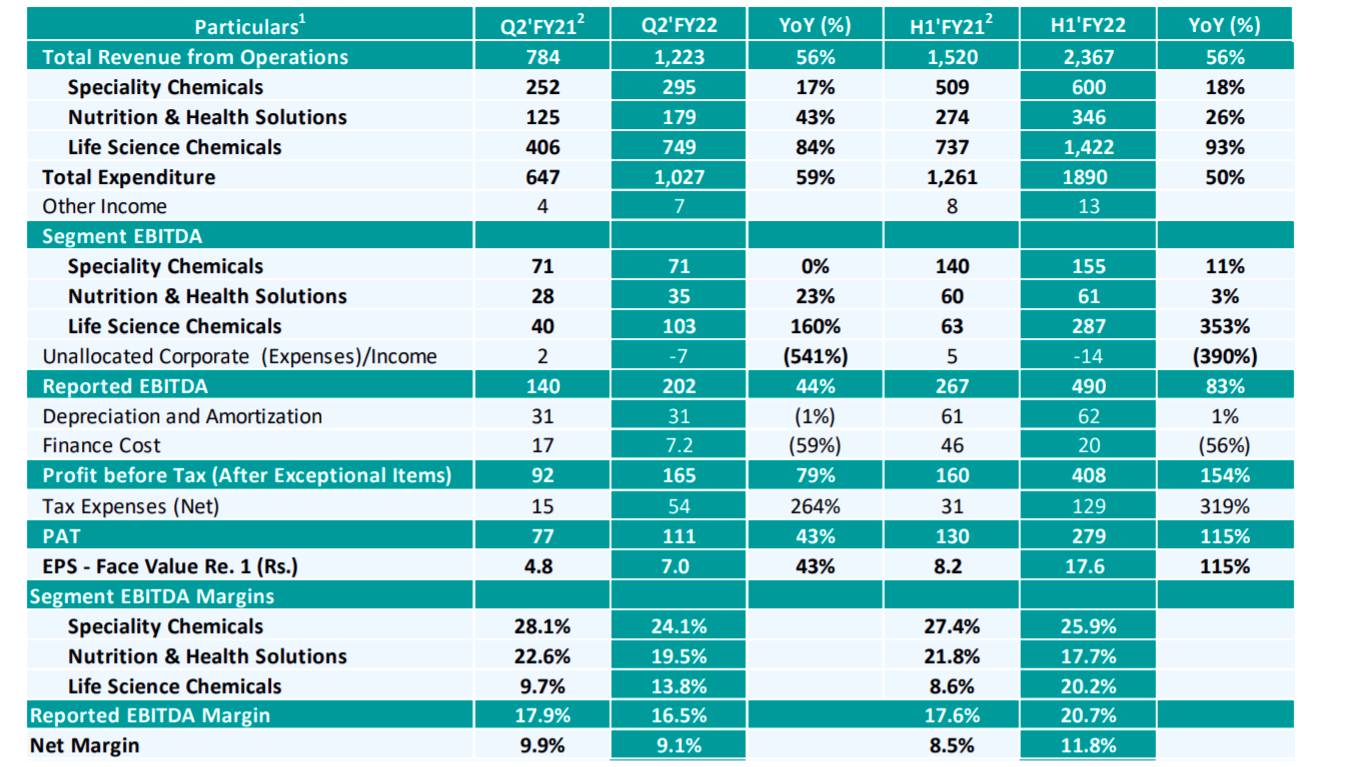

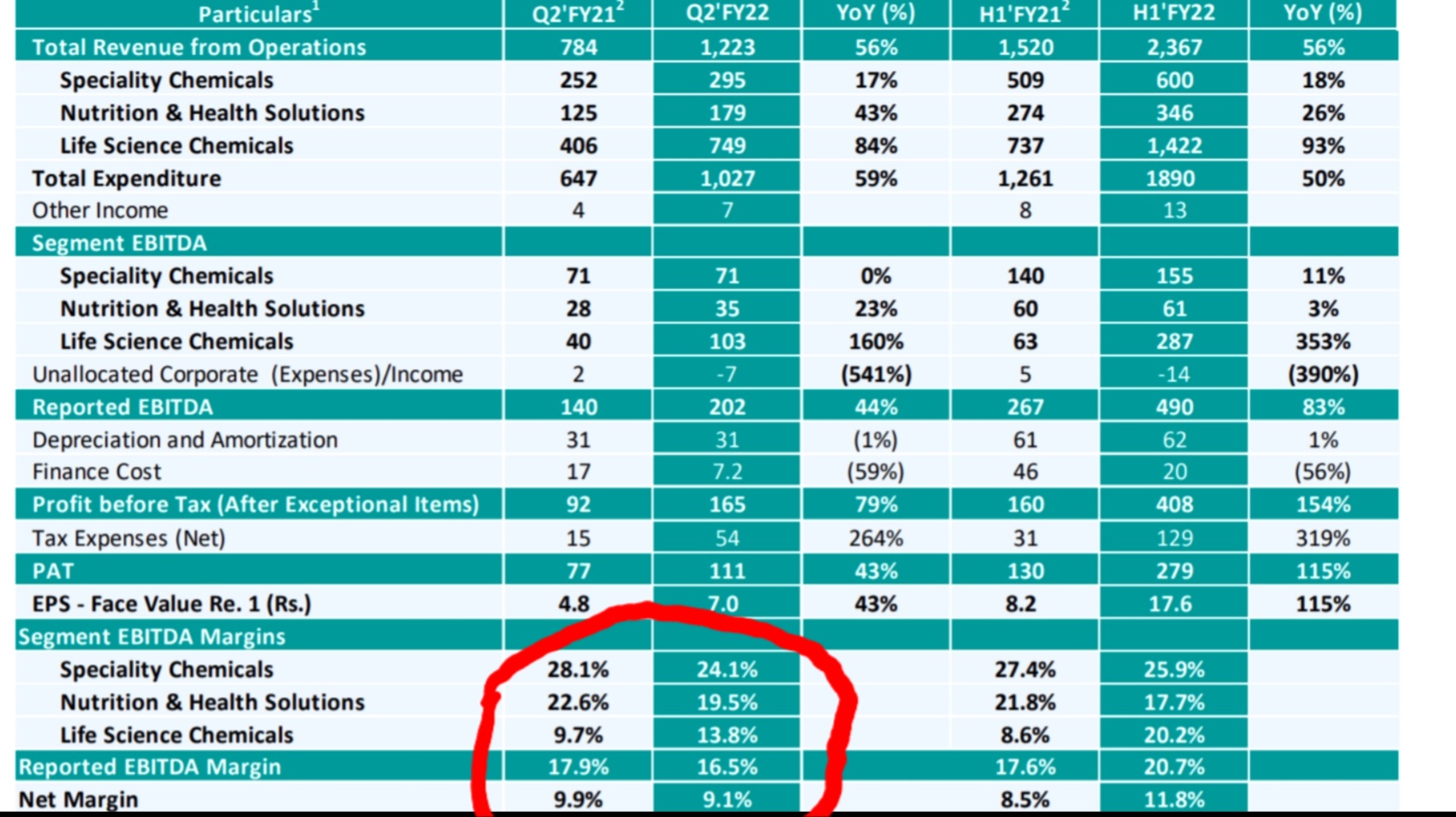

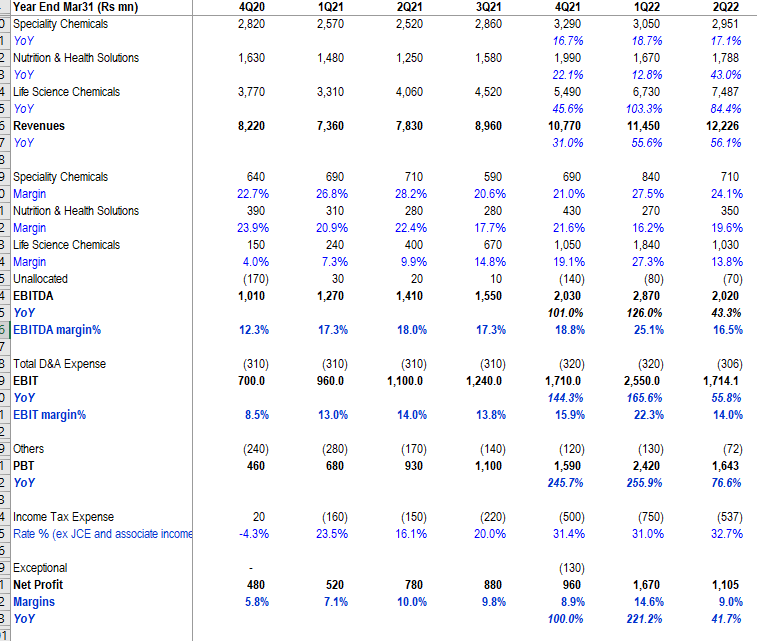

Jubilant Ingrevia Q2FY22 Results

As expected, the results are affected by fuel, logistics and higher raw material costs. The management is confident to pass on the incremental costs. There are many positives in the management commentary which are worth noting:

- The company is witnessing strong demand in most of its products due to Supply disruptions from China.

- The company has limited dependency on China for raw materials.

- The net debt is reduced further by Rs 193 Crore during Q2FY22.

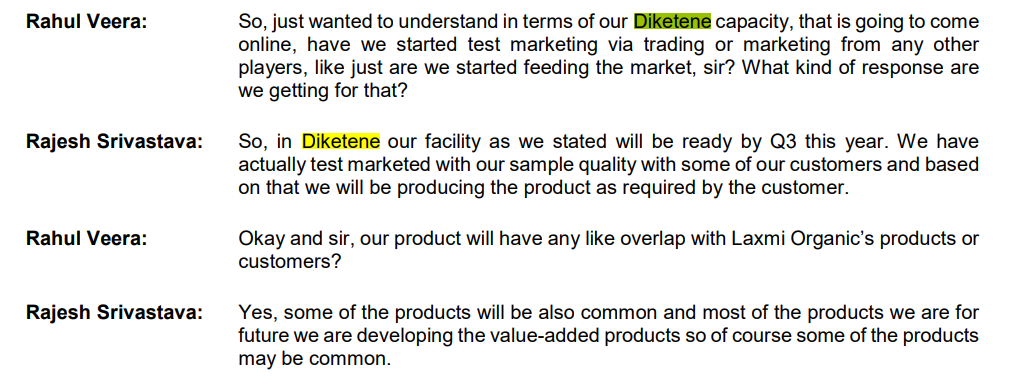

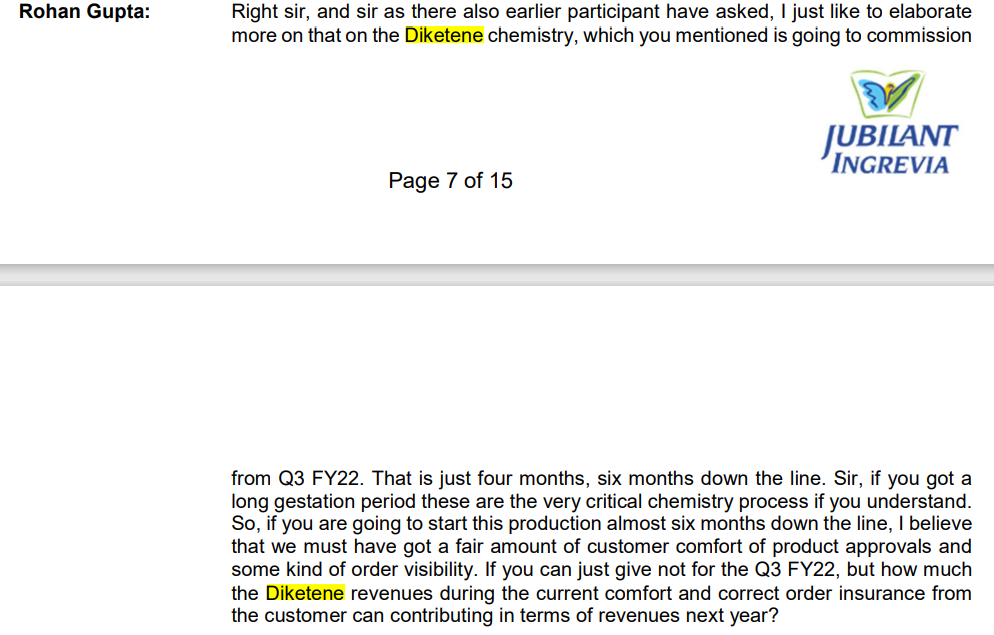

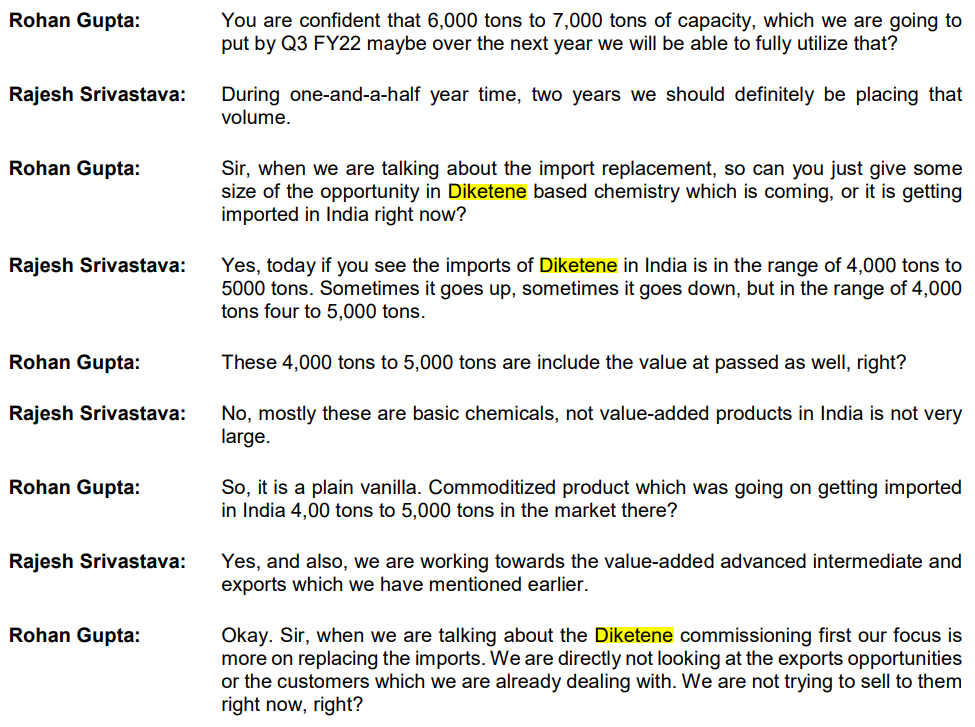

- Progress of ongoing Diketene Capex is as per schedule, and is expected to be commissioned during the Quarter Jan to March 2022.

- Further during the year the company committed investment worth Rs. 450 Crore for growth capex. At peak capacity these investments are expected to generate additional annual revenue of Rs. 900-1,000 Crore at prevailing prices.

Today’s knee jerk reaction post results was expected considering the hype and the fanfare built around Jubilant Ingrevia of late. The excess froth had to be removed at some point in time and I guess today was that moment. In my opinion long term story is intact and the company may do very well in coming days. Cheers!!

Disc: Invested and biased. Not a SEBI registered advisor. Do your own due-diligence before investing.

20 Likes

Growth is not an issue, margin is where the oscillation is high - coupled with froth building , Life science Chemicals margins QoQ from 24% to 13%, it was 10% in Q1 21, this segment contribution being high. Uncertainty is out now on LSI base case margins - can only get better from here or stabilize, and future Capex is more in higher margins segments, healthy balance sheet helps further.

10 Likes

1QFY22 had Rs80crs of inventory gains in life sciences segment and could not have got repeated. So the QoQ fall was expected in life science EBITDA and consolidated profits consequently.

It is surprising despite this the stock corrected to so sharply. A large part of this could be because of the midcap and small cap sell off in the last 2 hrs of the market.

4QFY21 EBITDA was Rs203crs, 1QFY22 EBITDA was Rs287crs and 2QFY22 EBITDA was Rs202crs

9 Likes

Noticed in Result declaration Page 38

“Though Acetic Acid price during end of quarter increased sharply however during the

quarter it was lower in comparison to Q1-FY’22” - This means Margin can decrease even further in Q3 before getting back to normal in Q4 if situation improves. Acetic Acid prices are still high.

7 Likes

Correct. This further opens up a hole in the way they have negotiated the existing contracts. Major division LS is cyclical . Is there any sales data where finished products are sold from LS 71% domestic I understand . In that they are not able to pass on increase in RM costs to local customers why Not having a clear cut contracts upfront with customers does not speak high of management they cant run after their customers now after the price rise. We need to understand more about the chain in LS.

1 Like

This means Margin can decrease even further in Q3 before getting back to normal in Q4 if situation improves.

Any reason for assuming that the raw material price will remain on higher side?

Further, if you notice, the life science business has grown multiple times and with capex it’ll continue to grow further. So, I assume that despite margin fluctuations, the growth story will remain intact.

Couple of interesting points from the Q2FY22 Investor’s Call:

- Most of the capacity of the upcoming Diketene plant is already being booked up by existing customers who currently source other products from Jubilant Ingrevia.

- Most of the new CapEx is coming up in Specialty Chemicals and Neutraceuticals which have higher margins than the overall company margin. Hence, going forward we should expect much improved margins from the current levels.

That being said, the company plans to double its revenue by FY26 (expected CAGR of 15%). With margin improvement, we could see PAT growing at around 20%-25%.

19 Likes