Yes, most likely for them the expectation was not good from Q1 and they booked profit on 30% in anticipation of impact of 2nd wave. Tough to comprehend the reasons for selling.

Strangely, even with such huge volumes in the past days, we do not see any bulk/block deals and all the shares or traded as normal transaction, We will only get to know after the updated shareholdings are disclosed.

I hope its the retail investors increasing their holding here like it happened in last Qrtr?

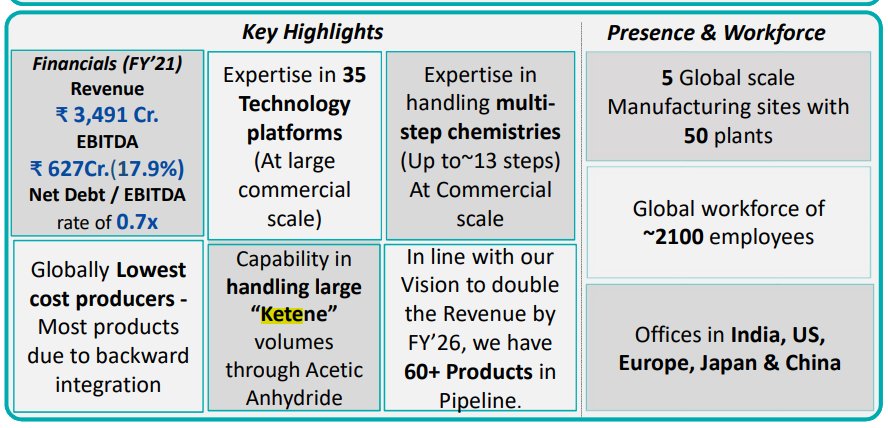

Demand scenarios very robust for all three divisions, Capex reflects the confidence

Spec chem -margins sustainable and value Added products planned as well as CDMO investments to add in future growth, on being asked about competetion in the products they operate - very few products has some competetion, largely niche and only manufacturers

capacity utilization at 85 yo 90%, on going s all Brownfield expansion/ debottlenecking to help double digit volume growth till Capex start to contribute meaningfully in FY 22.

RM prices elevated and some passed and some being passed on Spec chem can do double digit growth and confidrnt of maintain/margin expansion in short to med term

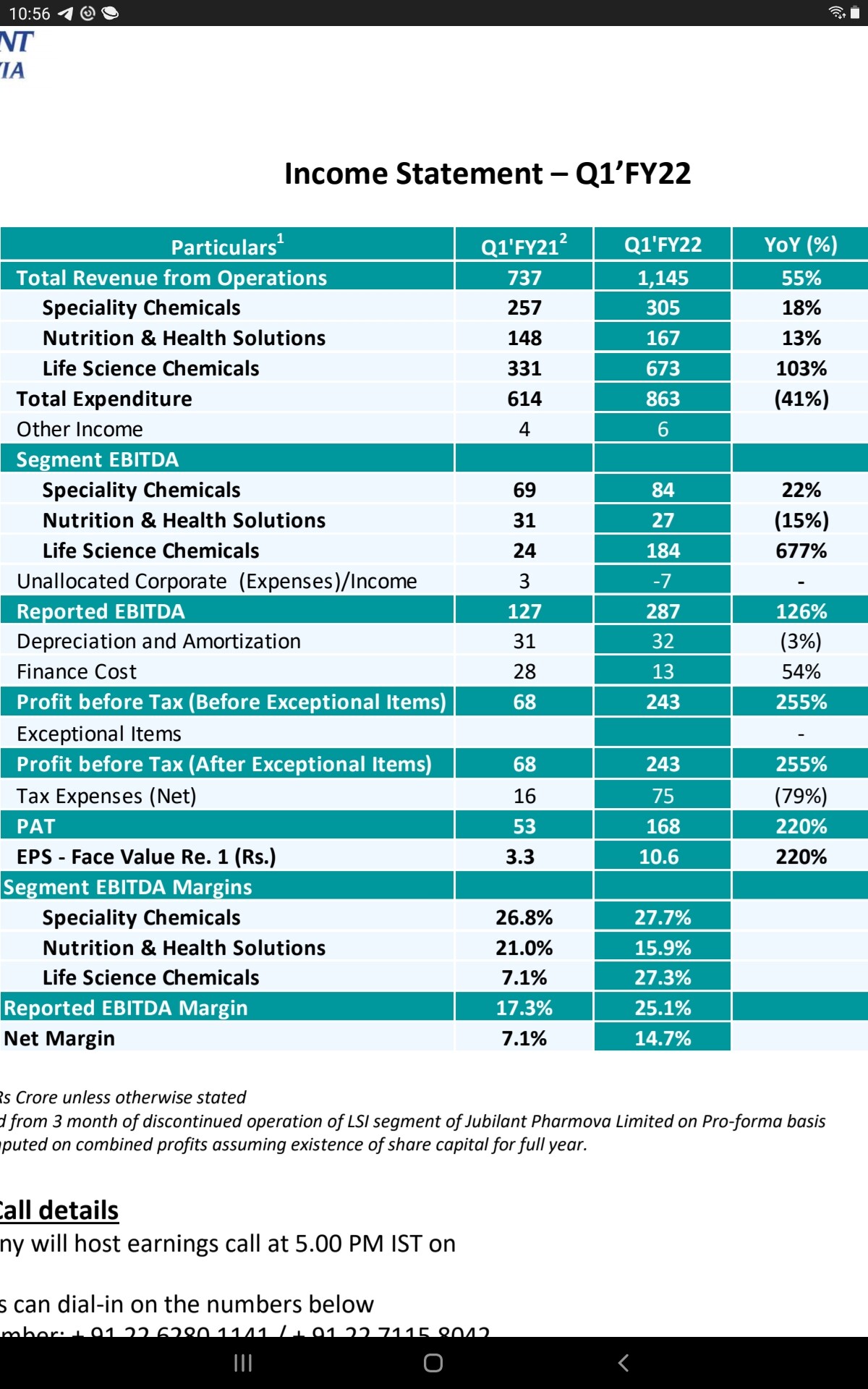

Numbers/Valuations - Spec chem division

Qtrly 305 cr revenue/84 cr EBIDTA/50 cr PAT - Annualized can do 1300-1500 cr revenue and 350 cr - 450 cr EBDITA/ 225 to 250 cr PAT for FY22. - At a conservative 25 -30 PE(15 % - 18% rev growth and 20-25% profit growth basis) this segment itself would be at 7000 - 8000 cr MCAP.

Peer Laxmi organics at 1750 Cr sales and 125 cr profit for FY21 is valued at 6800 cr mkt cap

Nutrition & Health

some disruption in Qtr hence margin dip , believe can do double digit growth as well as margin normalization, capacity utilization 75% type hence can accommodate near term growth, planned Capex will aid future growth and is around higher margin food grade products which will increase margins

Numbers/ Valuations

QTRLY 167 CR Rev/27Cr EBDITA(normalized ebidta at 20%+ would be 34 cr)/ 16 cr PAT( normalized PAT to be 22 cr) – Annualized can do rev of 650 to 750 cr/ EBDITA of 130 cr to 150 cr range/ PAT of 75 to 90 cr range Again at a conservative PE of 25 , a 2000 cr type Mkt cap, margin expansion to play out with focus on food grade Capex ( currently 70%+ is feed grade)

LSI chem

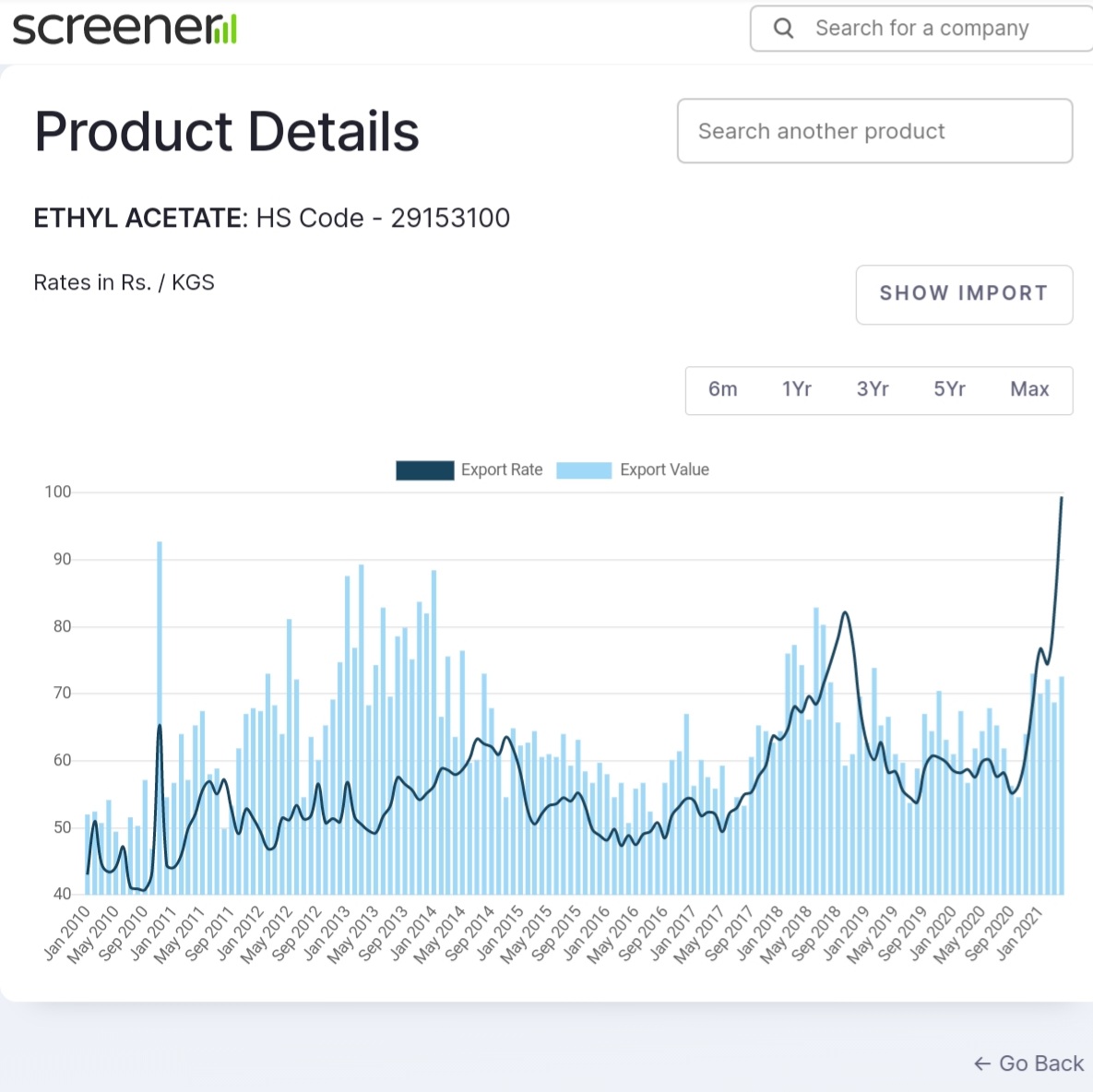

Mgmt was not at all comfortable on sustainability of this quarter run rate of revenue/margins - ethyl acetate prices/ton has been upward $350 in Q1 21, $750 in Q4 21, $1000 in Q1 22 and $1150 at June 22 end.

Need to better understand triggers for price rise - one point seem to be disruption due to cyclones in Americas? But that would be for few months only - does fellow VPers have more info around same?

Capacity also was 90%+ and are bring added as part of Capex plans, to come online in FY22-FY23

It suffice to say that current margin and prices are going to moderate but they may still be able to do 2000 cr + rev/ 500 to 600 cr EBIDTA( mid range of 18-20% compared to 27% Q1 22 and 7% Q121 - utilization will remain high hence operating leverage with plants running at full capacity)/ 350 to 400 cr PAT doable.

Even at conservative PE of 15 - a 6000Cr mkt cap.

Consolidated summary

Sum of parts would be 15 to 16K mkt cap for current biz - current mkv cap is 9.3K cr - a higher marging Capex program of 360 cr is underway and Diketene to come online in Q322. A significant upside potential clearly visible.

Invested from listing and added in last 30 days. Technical charts also near BO with high volumes.

Just to add couple of points, the co is consistently reducing the debt on books and have reached to a comfortable position. Also from the management call it appears they will not raise any debt for capex, everything will be from internal accruals.

Quick note on same - East Bridge seems to have got Ingrevia shares during demerger and their overall India listed companies investments seem to be on down trend across board - one can see same on screener for June holdings - they have reduced across the board - Jubilant twins, Natco, Piramal…many more…Given market euphoria some profit booking. On result day further reduction could be a factor on signs of global correction.

Volume absorption yesterday is indeed interesting without block deals.

There is too much euphoria now in social media about Jubilant Ingrevia. Time to sit back and relax. Regarding no bulk/block deal I think it is the same East Bridge and other FPIs who have been selling and the retailers are buying. This may continue for some time as East Bridge still has large stake to sell. Thanks!

Thanks for sharing

All worth 60 pages ,Each and every details what investor want’s to know for better understanding the business is provided

Like business overview of all 3 key segment, product offerings and application in verious industry, growth strategy ,capital to be allocated

Business outlook , opportunity size

Really very helpful

Thanks

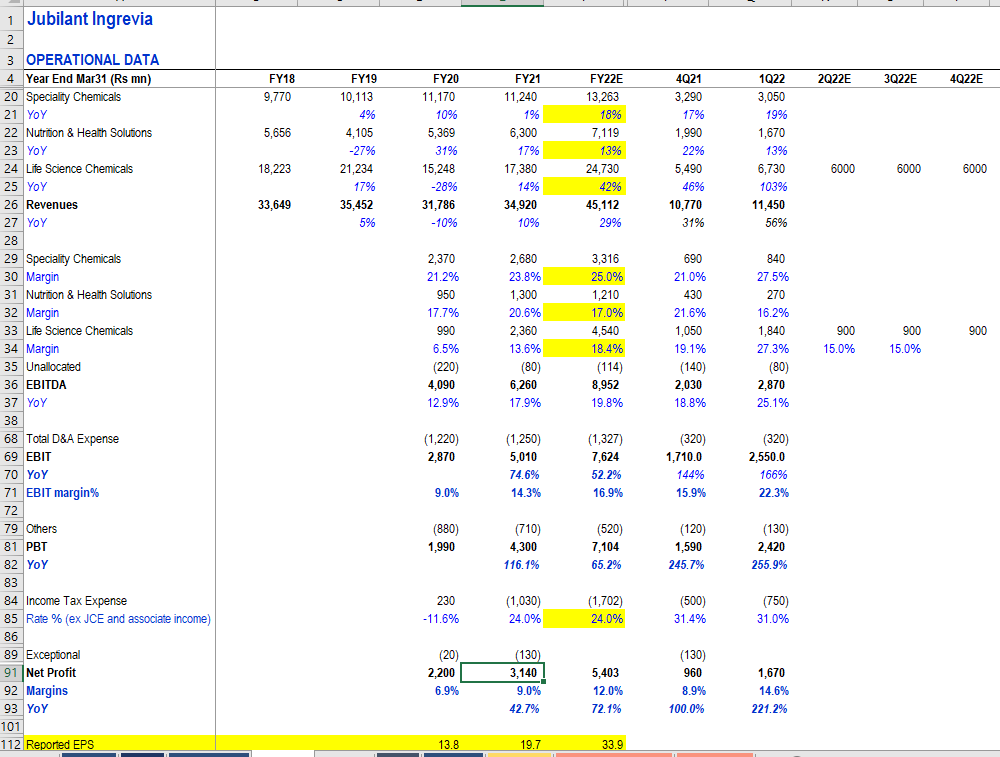

2QFY22 had some amount of inventory gains from acetic acid (as acetic acid derivative prices shot up) as can been seen from the life science vertical EBITDA. Even if one assumes 2Q, 3Q and 4Q EBITDA for FY22 are lower than 4QFY21 one arrives at an EPS for Rs34 for FY22E. Stock at Rs714 trades at 21x while most chemical companues trade at 40x and 50x P/E on FY22E.

Currently operating at 90% utilization in life sciences, 80-85% in speciality chemicals and 75% in nutrition segment

Can still grow volumes in speciality chemicals and life sciences by doing debottlenecking on quarterly basis besides big bang addition from Rs9.5bn

Rs9.5bn of capex over the next 3 years will have asset turns of 2x to 2.5x which can add Rs24bn of revenues in 3-4 years on FY21 revenues of Rs35bn in FY21

Outlook good for all 3 segments. Speciality chemicals will have both volumes increase and margin improvement (due to high margin CDMO increasing in quantum). Nutrition also should do well.

Market don’t give higher valuation till it is certain of cash flows. You can check even in the case of Deepak Nitrite, market is giving it valuation around 30 PE even though EPS is continuously increasing so I guess same will be case here for next few quarters.

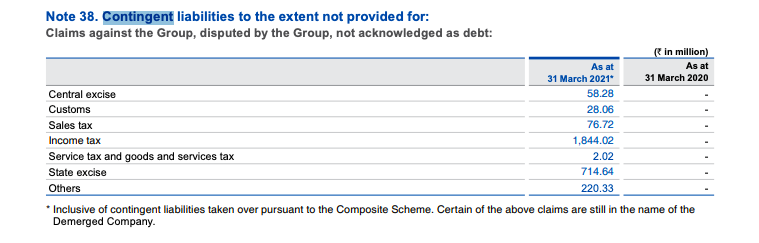

As per the FY21 AR, the contingent liabilities to net worth ratio is pretty high (around 15% on a consol. basis). Is this a big red flag?

Contingent Liabilities 294.4 cr

Net Worth 1922.9 cr

I wouldn’t worry too much abt contingent liabs especially cos most of them relate to taxes and GoI has a good track record in losing bulk of the litigation at higher levels. Also the auditor is GT and I know (as a big4 tax guy having given multiple such clearances) that auditors take external and internal opinion to confirm the provisioning needs.

Have been studying the business over the last few days and have to say it ticks all the boxes of a massive wealth creator in making: Fast revenue growth, increasing margins, reducing debt and potential rerating.

However, I had a few questions which need answering to complete my thesis. Would be obliged if someone can throw some light.

(1) What are the steady state margins from the LSI division going to be? Historical margins in the business seem to be around 8-10%. IOLCP also makes ethyl acetate and they have said in their concall that margins should come back to normal in a few quarters. If this is true plus given that fact that capacity utilisation numbers are already at peak, are we looking at ₹150cr steady state EBITDA from the division? Some of the estimates above look overly optimistic.

(2) Assuming ₹360cr additional EBITDA (taken from the Monarch report) from the new capex of ₹950cr over the next 5 years actually flows in, is there any further juice left in the current capacities? LSI numbers seem like they will surely come down massively. What about the current capacities of the Spec chem and Nutrition division?

(3) Is it fair to look at the extreme overvaluation of Laxmi Organics to build a re-rating thesis on Ingrevia? A lot of the posts above seem to be talking about that. There seems to be mispricing in the entire chemical sector and comparing current multiples of different players might not be useful for long term investors. Would it be more prudent to look at the exit multiple of ingrevia 5 years down the line (say 2026 or 2030) and comparing it to the present and see if we get any rerating between the two numbers?

P.S - Forgive me if the questions are too forward looking. I always try look at the maximum upside and maximum downside in a stock before entering. Here, I feel getting answers to these questions will help calculating the true upside potential. The Downside has been well captured by @Chins in his brilliant analysis.

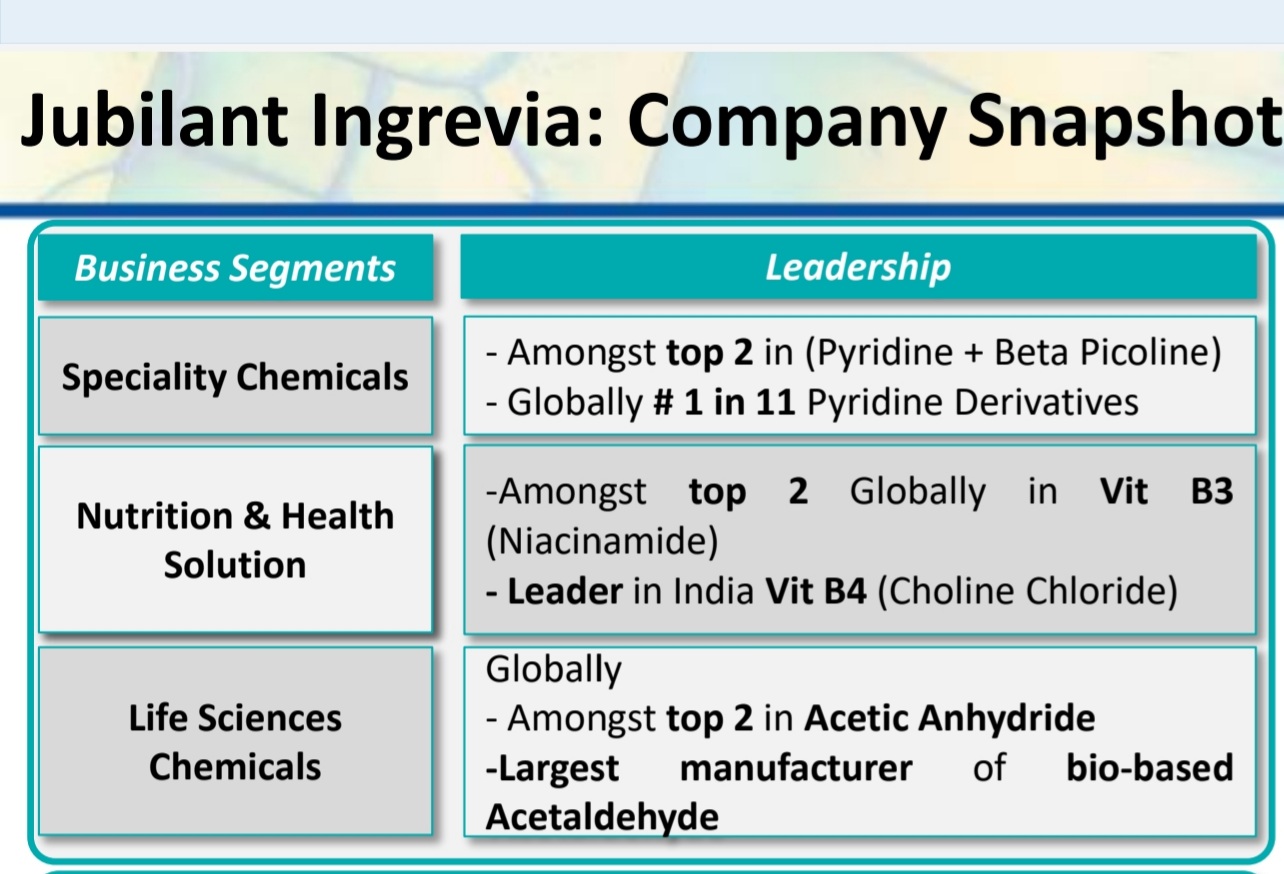

Beta picoline : The largest application of Beta Picoline is in the manufacturing of Vitamin B3 (Niacinamide) . Beta Picoline is a significant intermediate for agrochemicals like Chlorpyrifos, Haloxyfop, Fluazifop Butyl and also for Pharmaceutical Intermediates.

Pyridine : Pyridine is used to dissolve other substances . It is also used to make many different products such as medicines, vitamins, food flavorings, paints, dyes, rubber products, adhesives, insecticides, and herbicides. Pyridine can also be formed from the breakdown of many natural materials in the environment.

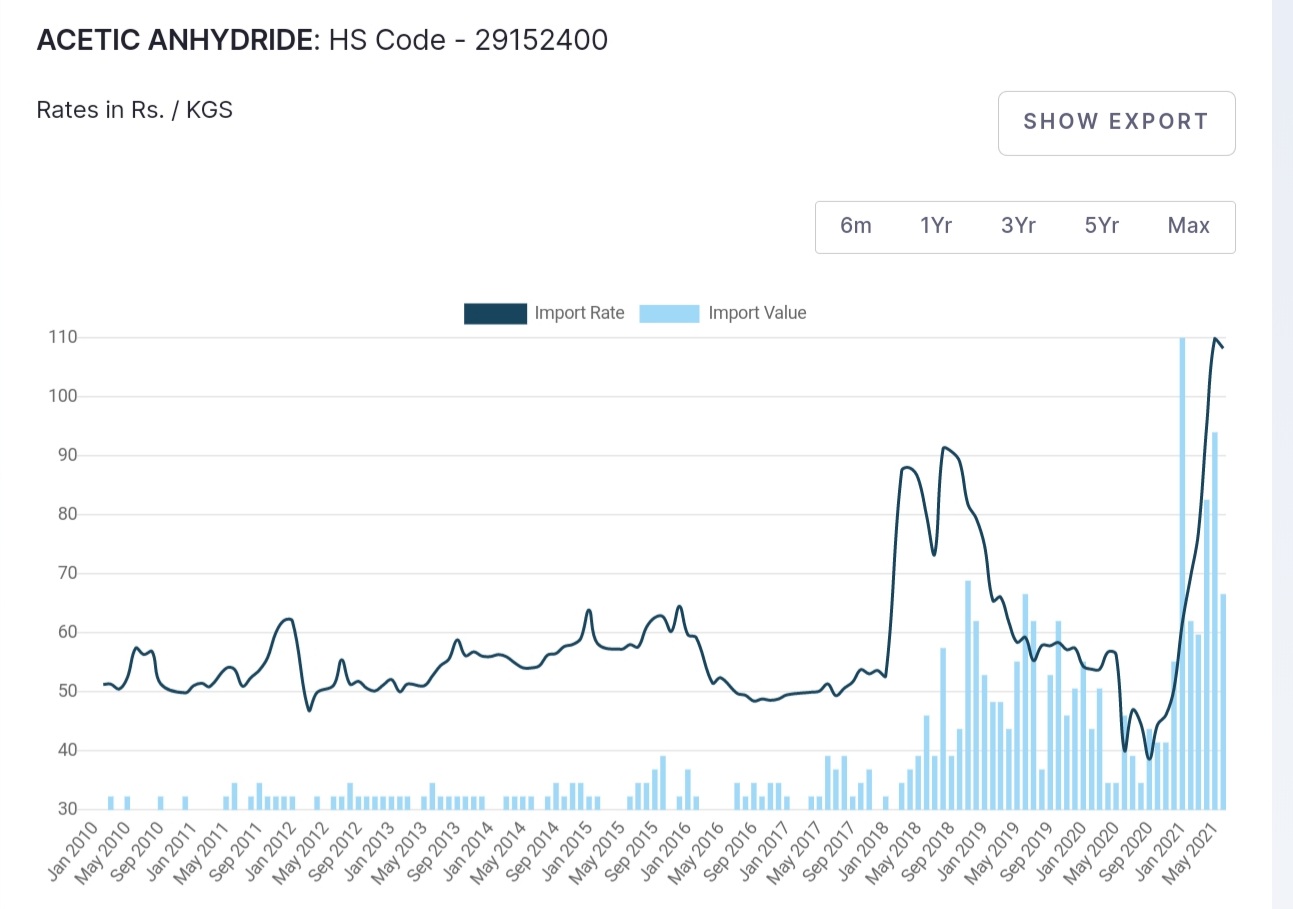

Acetic anhydride - Acetic Anhydride is a clear liquid with a pungent, penetrating vinegar-like odor. The largest volume use for acetic anhydride is as a raw material for cellulose acetate fibers and plastics. It is widely used as an acetylating agent or in chemical synthesis.

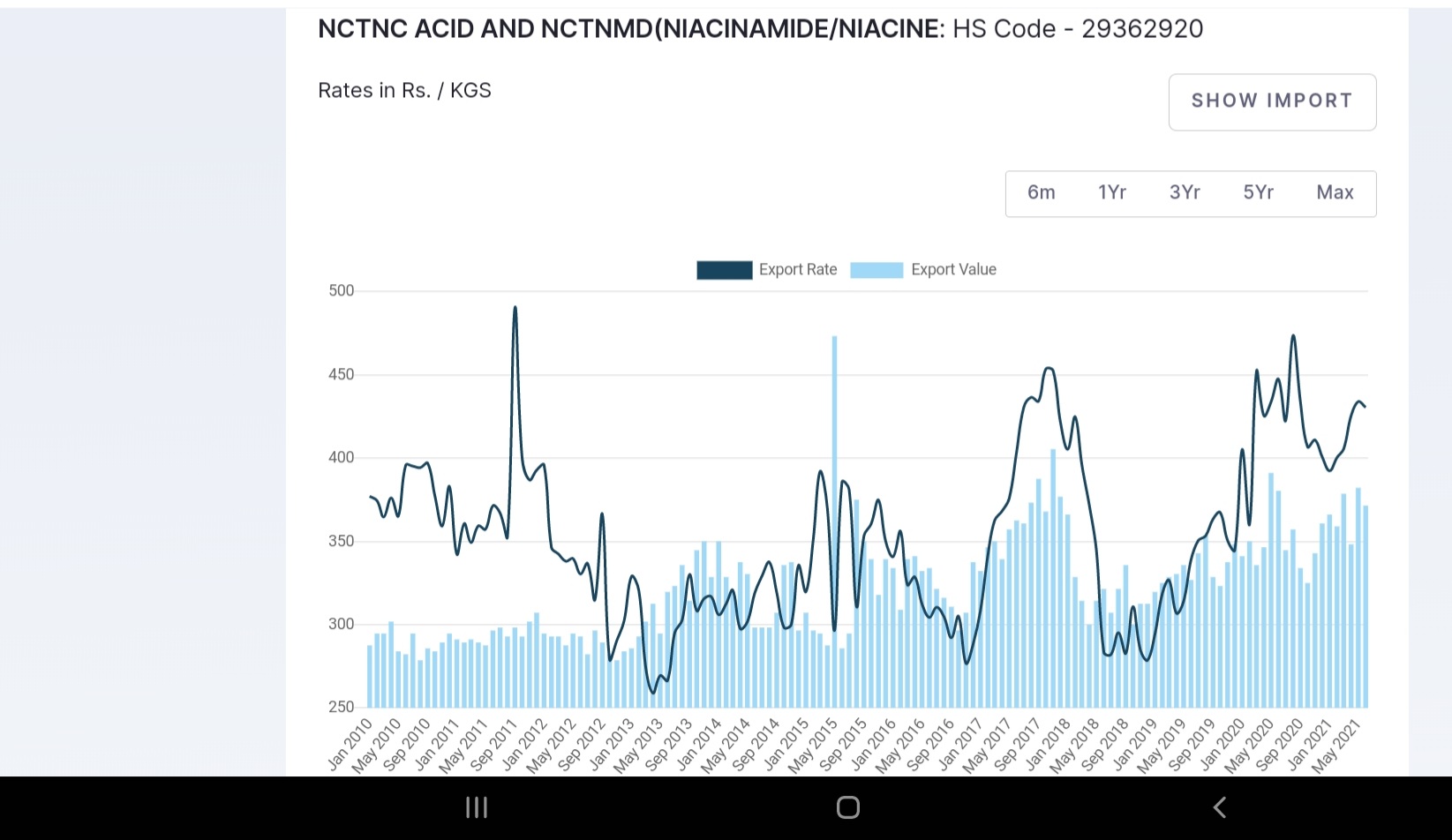

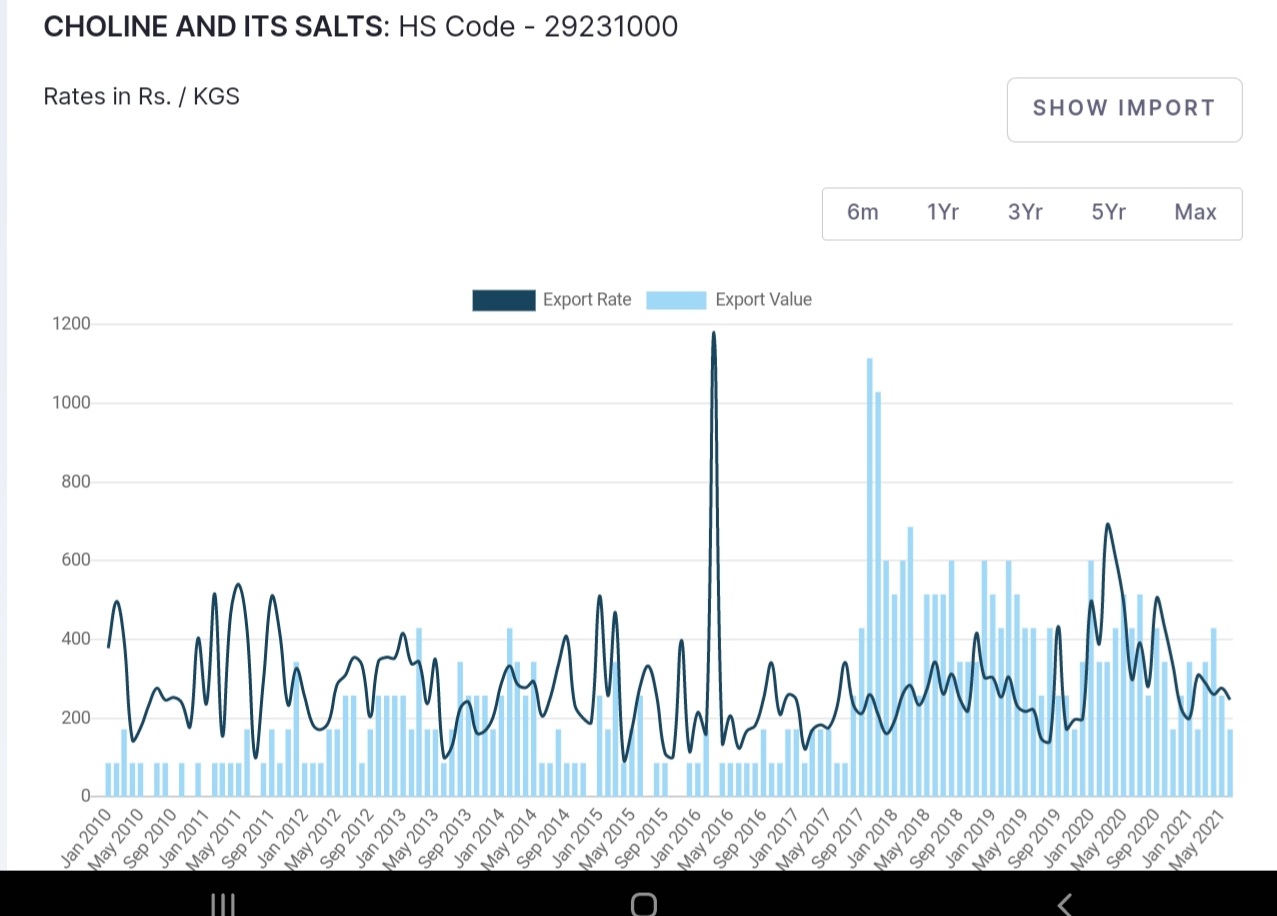

Summary: None seems one offs, life science Chemicals where margin sustainability is Q( they have contributed in high proportion in recent performance) - we can see both volume and price action in acetic anhydride starting FY 18 onwards, trend is structurally strong if taken at yearly levels. Acetaldehyde seems to be steady.

Mgmt. replied this point in last concall, capacity is not a fixed thing, double digit addition to capacity keeps happening regularly by debottlenecking and still there is scope to contiue doing this. So this is in addition to new capacity by way of capex.

Another easier way to look at capex and revenue potential is, this year they have committed to spend ~350 cr in capex and revenue potential from that is 900 cr (at current product prices) at 100% utilization and 100% utilization typically happens at about 12-18 months post capacity coming onstream. Typically they expect 2.5x Asset turns.