Here are my notes from their presentation which is again very detailed.

Before we get too excited, its important to consider that the commodity life science chemicals segment accounts for 50% of sales and FY21 saw sharp margin uptick from this division due to higher demand for Ibuprofen/paracetamol leading to jump in acetic anhydride demand.

• CFO: 680 cr. (vs 316 cr. in FY20), Capex: 122 cr. (vs 221 cr. in FY20), FY22 capex estimated to be 300-350 cr.; Net working capital days: 55 (vs 73 days in FY20)

• Gross debt: 548 cr. (vs 1295 cr. in FY20), net debt to EBITDA ~ 0.7x, net d/e ~ 0.22

• ROCE ~ 20.2% (vs 12% in FY20), ROE ~ 16.4%; Asset turns ~ 2x (vs 1.8x in FY20)

• First phase of Diketene derivates in on

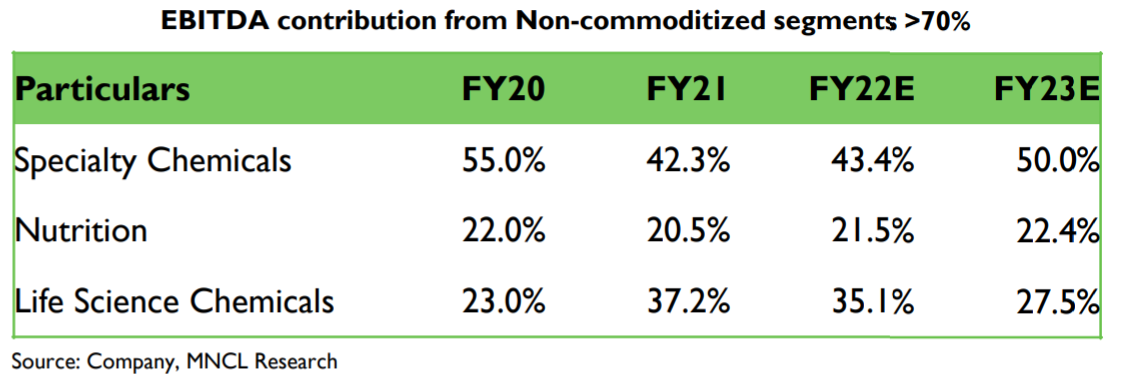

• Specialty Chemicals (32% of sales; EBITDA margin of 23.9% vs 21.4% in FY20)

o Demand continued from Agro chemical and Pharma Customers + new CDMO projects

o Paraquat ban in Brazil and Thailand resulted in lower demand of Pyridine, which resulted in lower prices during the quarter

o 45% of pyridine and picoline volumes are consumed in-house for value-added products and for Vitamin B3

o Six new products commercialized in FY21, Chromium and Zinc Picolinates for Health Supplements for US market

• Nutrition & Health Solutions (18% of sales; EBITDA margin of 20.7% vs 17.7% in FY20)

o Better product mix + pricing growth in Niacinamide

o For Vitamin B3 (Niacinamide & Niacin), 100% in-house sourcing of Beta Picoline

o Demand in Animal Nutrition segment got impacted due to COVID-19, especially in Poultry segment

o During the quarter, Animal Nutrition and Health business have achieved higher volumes of Choline and Speciality premixes

• Life Science Chemical (50% of sales; EBITDA margin of 13.6% vs 6.5% in FY20)

o Acetic acid price increases have been passed out to end consumers

o Higher capacity utilization across plants (90%+) driven by high demand in domestic as well as Global market (especially for acetic anhydride and ethyl acetate)

o Higher acetic anhydride demand due to enhanced demand for drugs like Ibuprofen, Paracetamol, Aspirin due to COVID-19 along with higher demand for Agrochemical products due to shift in manufacturing of end products to India

o Commercialized a new product, Propionic Anhydride, which is majorly consumed by Agrochemical industry

o 25% of overall volumes are consumed in-house by Specialty Chemicals segment

Disclosure: Invested (position size here)