Excellent write-up and wonderful research nirvana. I have just two points to add, the contract of the rig belonging to Mah Seamless will end in May 2025. It was implicit from the recent Concall of seamless that shareholders are not really happy with the transaction. Any view on that?

I did some research and found that GE shipping has 4 own jack-up rigs and all of them are relatively new 2 from 2009 and 2 from 2013-14. The company also has around 4000 crores of net cash. Interms of relative valuations and ownership of rigs don’t you think GE shipping would be a better bet??

Thanks

3 Likes

The management has indicated that the cash that they generate will go towards purchase of the rented rigs and bring them to their books. From the Mah Seamless also selling the rigs might make sense from business point of view but such cross holdings in related companies are not uncommon in business families. I would not worry too much at this point.

The issue with GE is that you have to deal with the shipping parts of the business. The charter rates were good until now but as the wars and crisis are reducing the charter rates would come down and through rigs business might fire the Tanker business might not do that great. The book “The Shipping Man” beautifully explains the maritime business and the intricate complexities.

Disc: Invested recently

12 Likes

Is today’s drop due to the EV import duty being slashed to pave the way for Tesla? Seems a bit overblown.

No

Today’s drop is highly likely because of this:

- Big shareholder sold 2% of co.

- Still holds 6.6%

- Worry is they may sell more

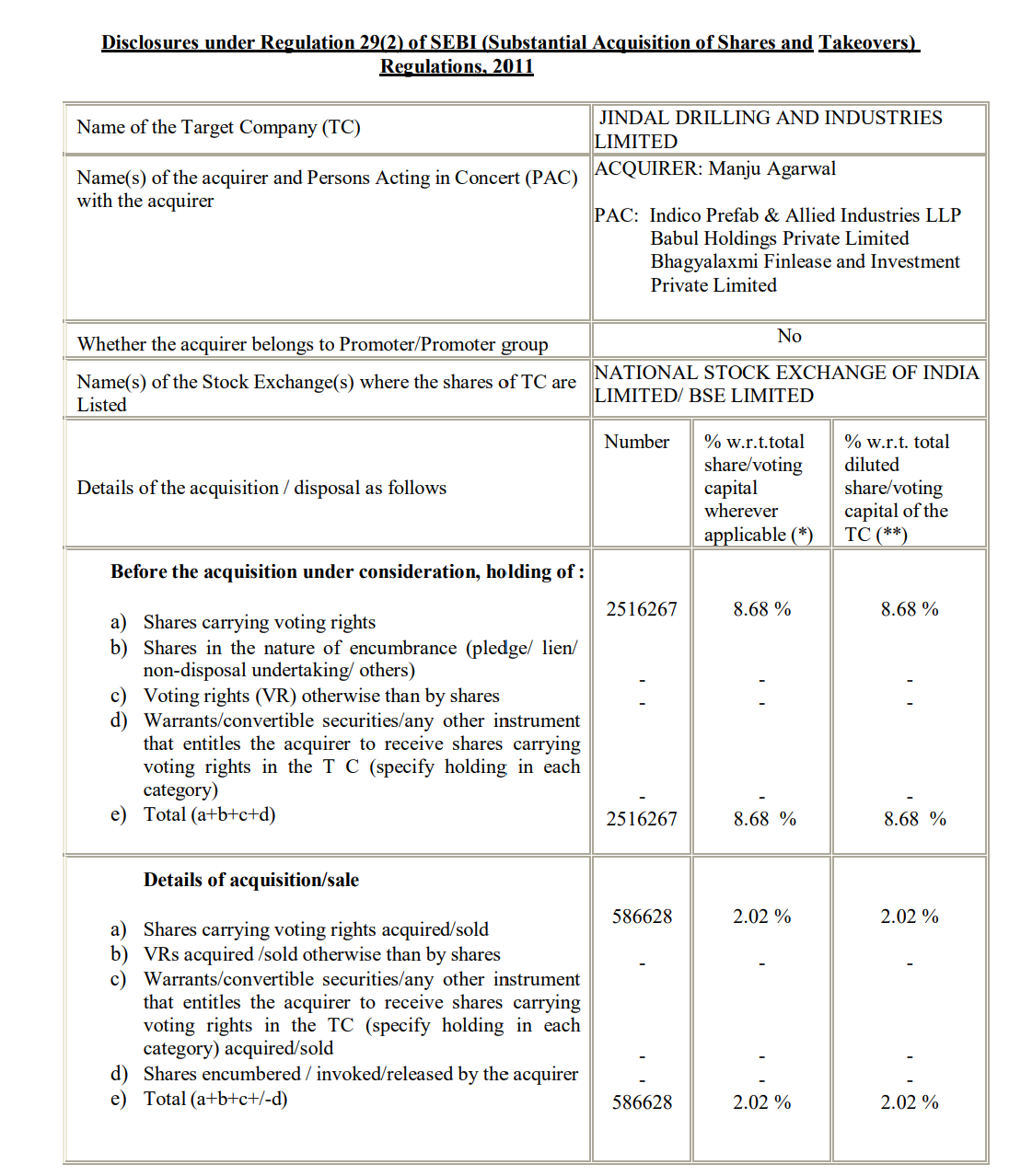

- Does any one know who “Manju Agarwal” is?

2 Likes

This filing is although recent but at least a week old. I don’t think, after one week this filing would have an impact of this degree. This fall is most likely due to some other reason, which I don’t think us retail investors are aware of yet.

Well that was previously but they could be selling more today. Manju Agarwal seems to be associated with the large public shareholder Bhagyalaxmi Finlease & Investment Pvt Ltd. and Babul Holdings Pvt. Ltd.

This entity indeed seems to be associated to promoters. So most likely it is just an internal restructuring of holdings, from what it appears. This shouldn’t be the reason of a sudden fall.

1 Like

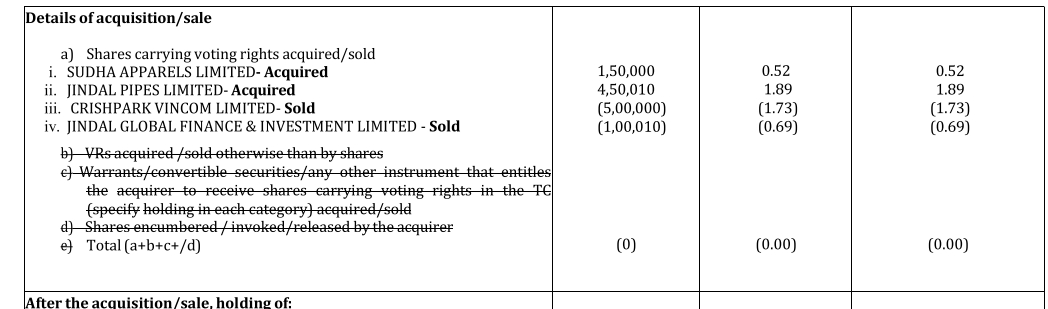

Agreed it shouldn’t. There has been an internal share swap between promoter entities Jindal Pipes Ltd and Crishpark Vincom Limited this month as well.

2 Likes

Has there been any particular news which has cause almost 20% fall in past 2 days ? Appreciate your inputs .

2 Likes

Crude oil sharp price drop, that may have led to to this reaction, read the above posts in threads to understand why does it matter

2 Likes

Regarding the share swap between promoter entities not sure why they were carried out as market sales and purchases. Can anyone throw light on this?

I am new to the industry . Have tried to do a very basic projection on numbers basis past trends and comments in concall . Please comment if my assumptions are in line or i need to look into further details .

| Financial Metric | FY24 (Actual) | FY25 (Projected) | FY26 (Projected) | FY27 (Projected) | FY28 (Projected) |

|---|---|---|---|---|---|

| Revenue (INR Cr) | 617.01 | 827 | 975 | 1,150 | 1,300 |

| EBITDA (INR Cr) | 139 | 225 | 320 | 380 | 430 |

| 23% | 27% | 33% | 33% | 33% | |

| Depreciation (INR Cr) | 63.63 | 70 | 85 | 95 | 105 |

| Interest (INR Cr) | 15.32 | 15 | 10 | 10 | 10 |

| EBT (INR Cr) | 60.05 | 140 | 225 | 275 | 315 |

| Tax (25%) (INR Cr) | 37.56 | 35 | 56.25 | 68.75 | 78.75 |

| PAT (INR Cr) | 114.09 | 217 | 263.75 | 306.25 | 336.25 |

| 18% | 26% | 27% | 27% | 26% | |

| EPS (INR) | 39.37 | 74 | 91.01 | 105.68 | 116.03 |

| ROE (%) | 4% | 15% | 19% | 22% | 24% |

| ROCE (%) | 7% | 12% | 17% | 20% | 22% |

| Shares Outstanding (Cr) | 2.898 | 2.898 | 2.898 | 2.898 | 2.898 |

| P/E Ratio | 18.42 | 20.00 | 20.00 | 20.00 | 20.00 |

| Market Cap (INR Cr) | 2,244 | 4,289 | 5,275 | 6,125 | 6,725 |

| Capital Employed (INR Cr) | 1,278.26 | 1,400 | 1,540 | 1,680 | 1,820 |

| Price | 725 | 1480.00 | 1820.20 | 2113.60 | 2320.60 |

2 Likes

Key Points

- FY25 PAT: Adjusted to INR 217 Cr based on current run rate and Q4 projections.

- FY26-FY28 PAT: Increased, reflecting higher revenue, efficient cost management, and the full impact of the Jindal Pioneer acquisition.

Potential Upsides and Considerations:

- Contract Renewals: Securing contract renewals at favorable rates is critical for sustaining revenue growth [1].

- Jindal Pioneer Acquisition: Successful integration and enhanced PAT contribution from Jindal Pioneer are essential [2, 3].

- Market Conditions: Stable oil prices and demand will support continued profitability [4].

- Operational Efficiency: Continued focus on cost management and operational efficiency will drive EBITDA and PAT growth.

3 Likes

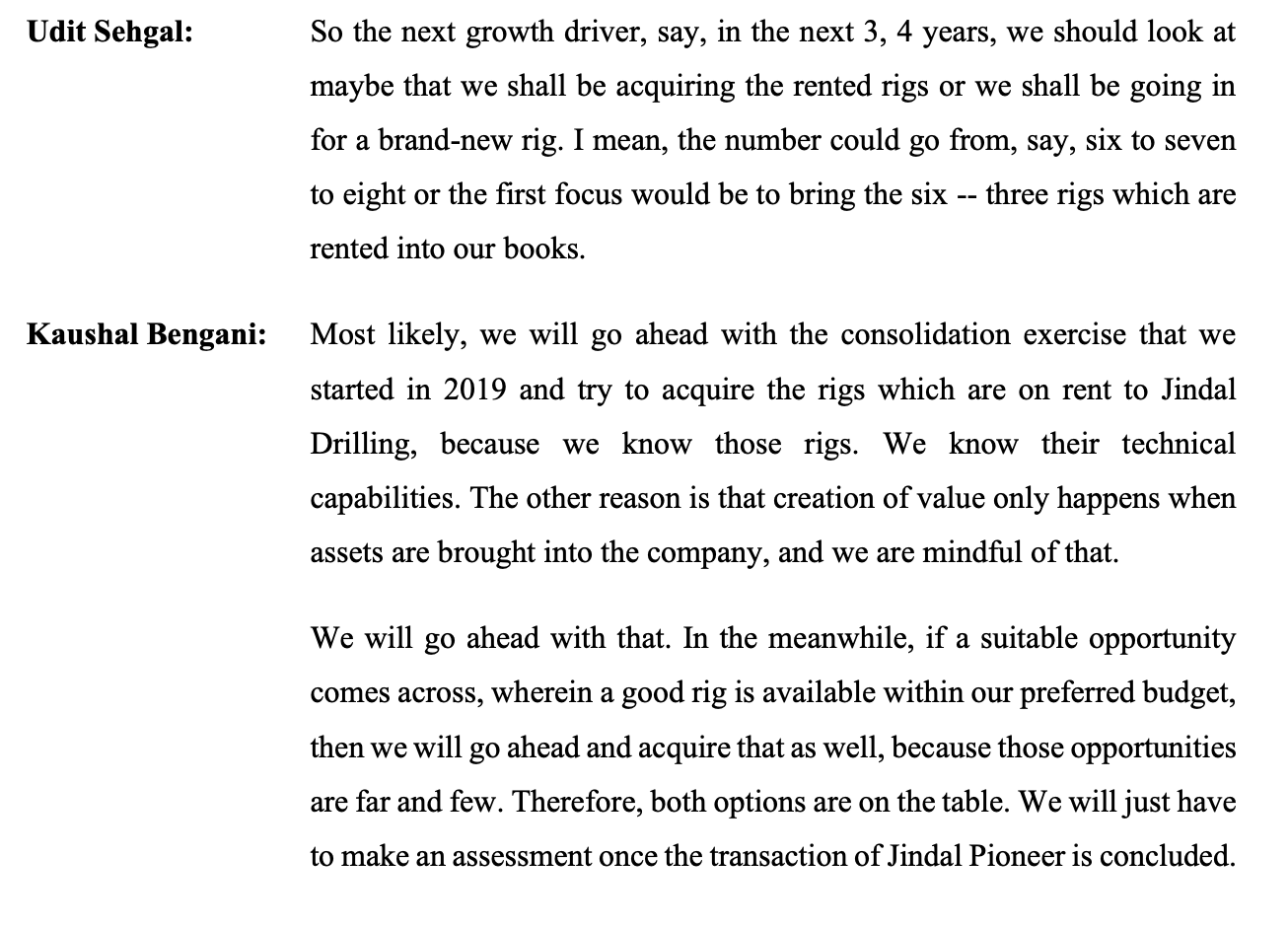

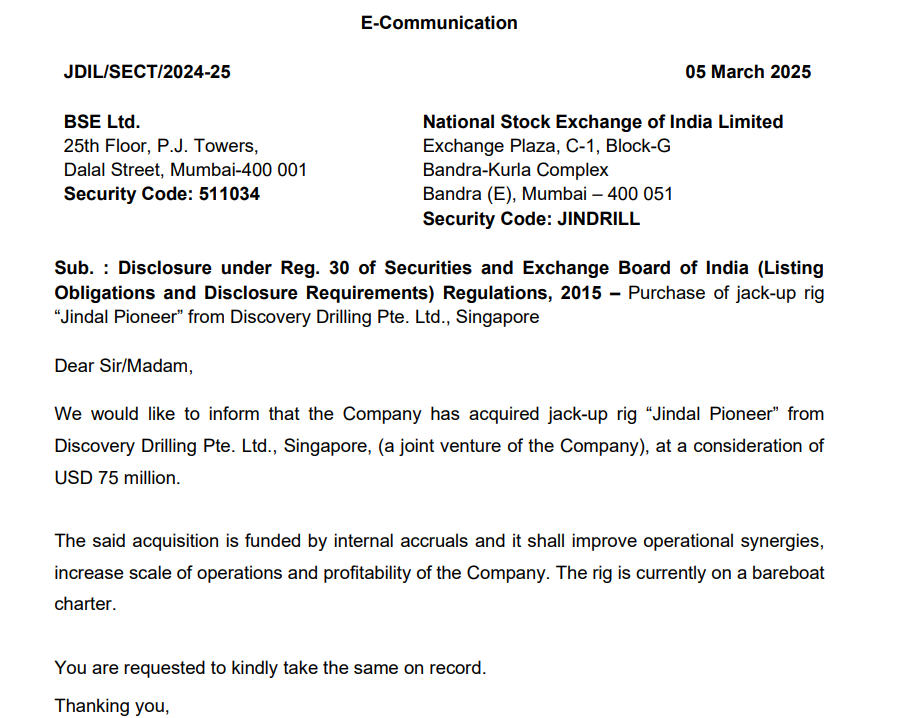

The long awaited acquisition of Jindal Pioneer is finally done. By my calculations, this should start adding 10Cr incremental PAT to consolidated quarterly PAT nos starting Q1 FY25.

18 Likes

If you see my above reply 15 day ago, You can see Discovery drilling is in losses for the past 5 years, So does it really contribute positively?

Please go through the concalls - management has discussed unit economics of Pioneer in the current contract in detail. The rig was on a bare boat charter rate of 35k USD per day till Dec 24, from Jan rate is supposed to increase to 40k USD per day. Since it’s a bareboat charter contract, the JV or Jindal will not bear any operating costs. Hence most of the revenues flow through to EBITDA. I am calculating PAT assuming 30k USD per day EBITDA and 20% tax rate, which comes to about 20Cr per Q. By virtue of their 51% stake in the JV, about half the profits were getting added to the consol numbers, now the full profit will get added. Revenue and EBITDA from Pioneer will also get added to Jindal consol numbers. Hope this clarifies.

For further queries you can reach out to company IR.

13 Likes

Yes I already read about Pioneer’s economic but reported number is saying different story, Thats why I asked

Perhaps you missed Note no 4 in Q4 FY24 earnings release. That should explain most of the FY24 losses in Discovery Drilling. JV PAT has been quite consistent in the last 3Qs and management has indicated this will continue. Only 50% share of PAT in Virtue Drilling can’t contribute 17-20Cr PAT at Jindal consol level, so Pioneer must surely be contributing. My guess is about half the profit is coming from Pioneer and half from Virtue, but don’t ask me what basis I have for this guess, I don’t. It just seems likely to me given what we know about Pioneer’s charter rates.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/8b02eb3e-63c4-4a8e-8bc1-d2bb564fa95e.pdf

5 Likes

Hi, Thanks for your appreciation. Although @GourabPaul has replied to you, let me also share my 2 cents.

I think Maha Seamless shareholders want the company to sell the asset and rightly so, given its an unrelated business. I’d love for Jindal Drilling to buy the asset. They will generate enough free cash flows in the next 5-6 quarters to buy another asset after Pioneer. In the reply given to you Gourab, he has shared the relevant concall snippet where management has clearly said their intent is to consolidate all Group rig assets into Jindal Drilling. Let’s hope we get to hear something positive here closer to AGM season.

GE Shipping is an excellent company. They are masters at capital deployment, buying ships in downcycles and selling them in upcycles. But they are not a pureplay offshore company because the bulk of their revenues comes from dry bulk shipping and oil tankers. These are spot market businesses with huge volatility and hence a completely different kind of business.

If you are interested in offshore plays and don’t mind US equity exposure, I’d urge you to read the Praetorian capital note shared earlier in this thread. There are jack-up rig as well as deep-water rig and drillship companies which are listed in the US which may have good value right now. As the note argues, the market seems to have unjustifiably punished them since early 2024.

12 Likes