Thanks for this great analysis @nirvana_laha . Since Pioneer has been acquired, what kind of depreciation contribution are we expecting from it ?

The 10cr incremental PAT is after the depreciation expense only, right?

1 Like

How lower crude prices impact future profitability of Jindrill can anyone share thoughts?

Lower crude prices may encourage E&P companies to drill more or refurbish existing wells and Let’snot forget Trump slogan "Drill baby Drill’.

In either scenarios, Rig demand should hold itself.

2 Likes

But ONGC might not increase the daily rates in the new rig contracts if the crude prices continue to stay at lower levels. So the topline growth beyond what we saw in Q3 is going to be tough ahead.

2 Likes

I assume all such renewals are basis long term plans of country for Oil production and short term variation in prices may not influence such decision . Rates should be mostly basis availability and market rates , small negotiations may happen due to ONGC being sole user but they can’t be way off market rates . They should be definitely way higher than current rates .

4 Likes

In addition, IMO Natural gas prices should be given equal weightage as Crude Oil.

Natural gas prices has formed good base and is on the rise. I reckon this can compensate subdued crude oil prices.

All in all favourable scenarios for Jindal drilling.

Disc - Invested

1 Like

Crude prices have dropped below 70$ per barrel. Sustained lower prices can impact drilling activity negatively.

2 Likes

I think- you have not understood JD’s business model yet, these r all fixed contracts…as of now…

2 Likes

They are only fixed till expiration. To make sure the contracts get renewed at higher rents, the gas and oil exploration/extraction needs to remain profitable for ONGC. The US counterparts of Jindal Drilling are facing lack of orders right now. If the crude prices keep dropping we might see this scenario in India as well.

8 Likes

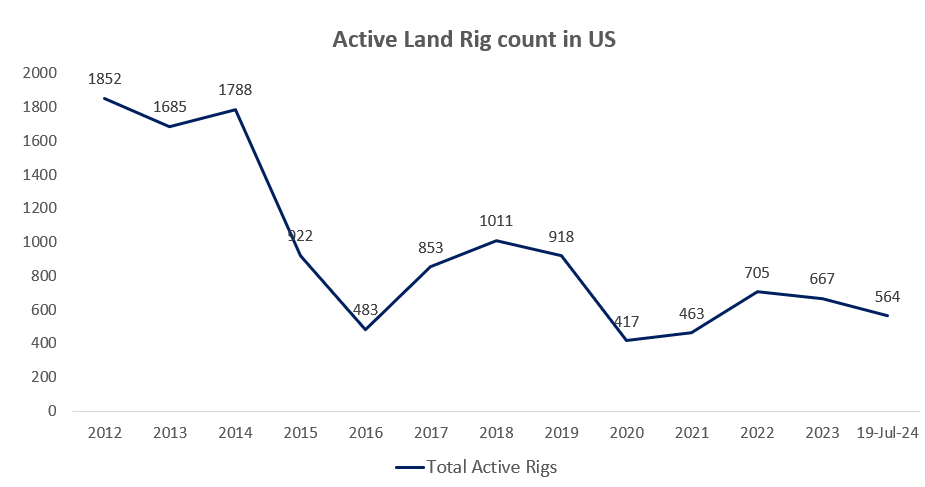

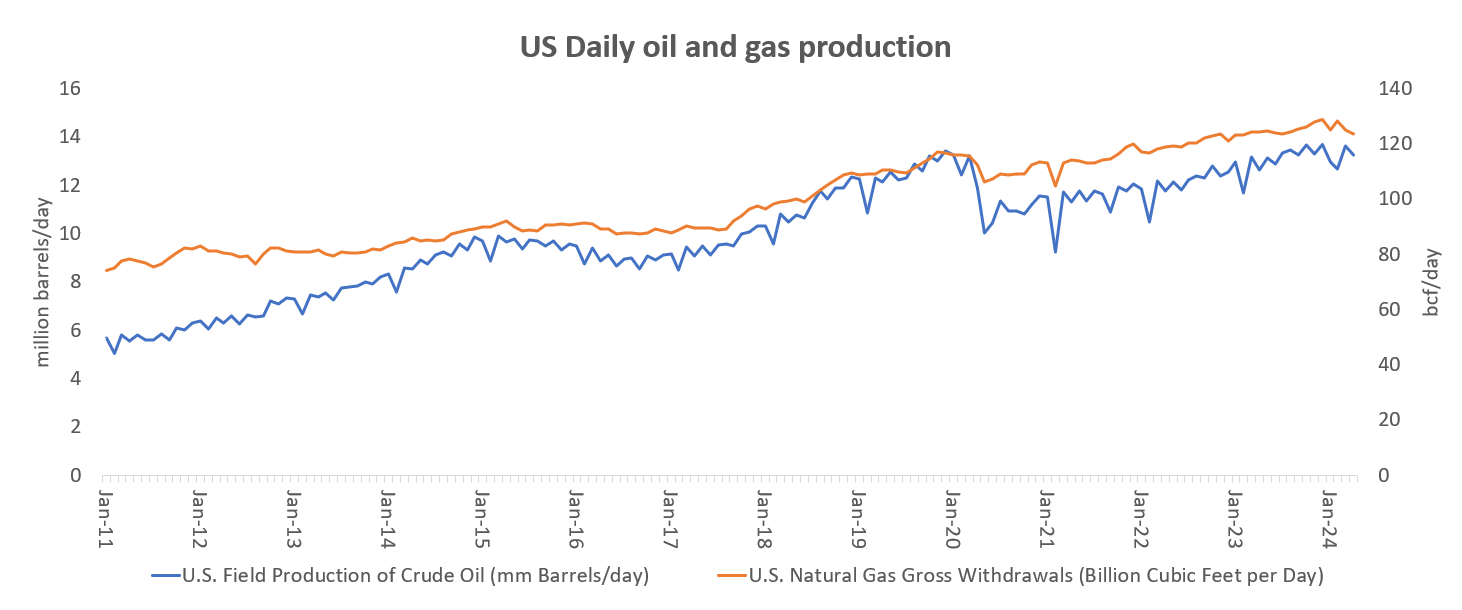

The observation is correct that the efficiency of the rigs have materially improved in the last 10 years or so. Below is the chart of the total land rig count in the US. In 2014, there were 1700 active land rigs which have reduced to almost 580 now.

In the meantime, the total oil production in US has increased from 8.5mm barrels per day to 13.5mm barrels per day.

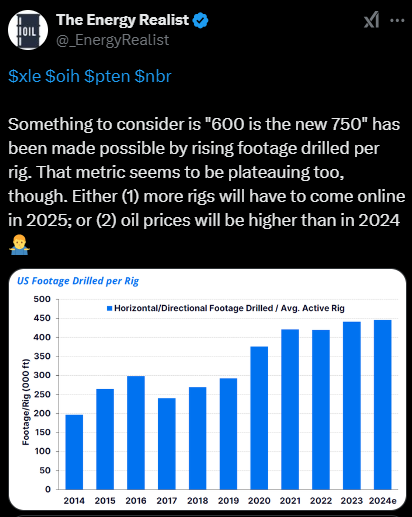

Land rigs are now able to drill 10,000 feet horizontal which is 2-3 times more than what it was 10 years ago. This has also led to higher day-rates and margins for these drillers despite utilization being low, so not all is bad. (Lower 48 means United States). The figures are for on-shore drilling company, Nabors, but are representative of the industry.

The key question is how much of the efficiency improvement can happen further. If you see the trends from the recent years, it appears that the efficiency improvements are plateauing. While this would mean that while rig count should remain stable, but so will the day-rates.

I would say the key driver for these companies is nothing more than oil price. Everything else takes care of itself.

4 Likes

If the utilization rates decrease, the company would still factor in the full depreciation cost of the un utilized or underutilized rigs. So even if the average day rates improve, it might not directly lead to increase in net profit. This is also an optimisation problem one might want to look at.

1 Like

You never know!

I came across this recently:

Full link:

https://www.ft.com/content/0d24dcf4-b53b-48e5-b49c-99606958a96d

With my half knowledge, I am not able to decide.

1 Like

Are natural gas prices not good enough to keep Rig bussinesses afloat?

Per this the US administration wants oil to be at 50$ per barrel and their bouts . If this happens it could hurt the prospects of drilling companies . However OPEC and even shale producers don’t want the prices to fall so much. Looks like a bit of catch 22

5 Likes

To get a view on oil price, I can recommend reading the quarterly commentary by Goehring & Rozencwajg, who are natural resource investors based in US. 2 times in the last 50 years, oil prices went between 7-10x in the span of a decade (1970-1981 and 2000-2008). What was common both the times was that the supply from non-OPEC countries had started to peak and the pricing power shifted to OPEC countries. Their theory is that we are entering a similar setup now. US (non-OPEC) is the largest oil producer in the world with 13.2mm bpd of crude oil production, largely through shale, which is peaking. This figure used to be around 6mm bpd around 2010, when shale was discovered. One sign is is that the oil production growth is tapering. Another sign is that the associated natural gas production from shale wells is increasing. From a shale well, when the production of associated natural gas increases, it means that the well is maturing. The attached document has more details.

Can Trump lower the oil prices by increasing oil production in US? The answer is no. No oil and gas E&P will want to increase production if oil were to trade in the $50-60/barrel range, regardless of the “Drill baby drill” rhetoric. To be invested in these companies, one needs to have a directional view on oil price. If oil price were to keep going down, demand for these rigs will take a beating.

2024.Q1 GR Market Commentary–Final.pdf (565.4 KB)

13 Likes

How will the earnings be affected, if the dollar weakens against rupees? Since the contracts and the realization are in dollars.

In my opinion, learning will not be affected much. All companies with majority forex earning hedge their earnings against fluctuations in currency movements .

1 Like