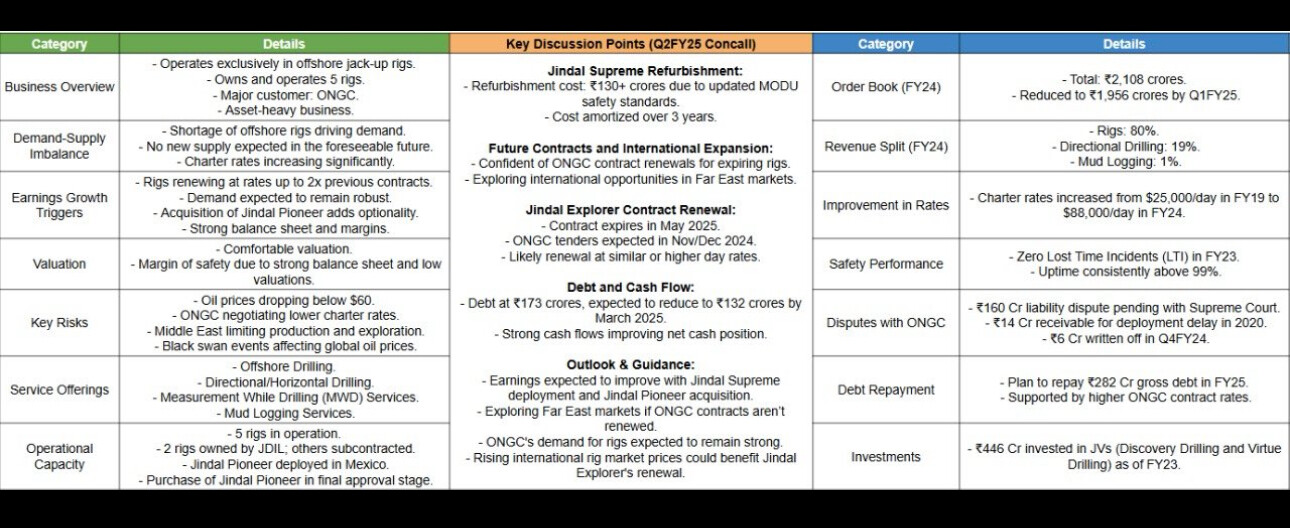

About the company

Jindal Drilling is an upstream oil and gas services provider in the offshore oil and gas segment. It provides offshore rig services to exploration and production companies like ONGC. Jindal Drilling is promoted by the DP Jindal Group (https://www.jindal.com/) who also own Maharashtra Seamless.

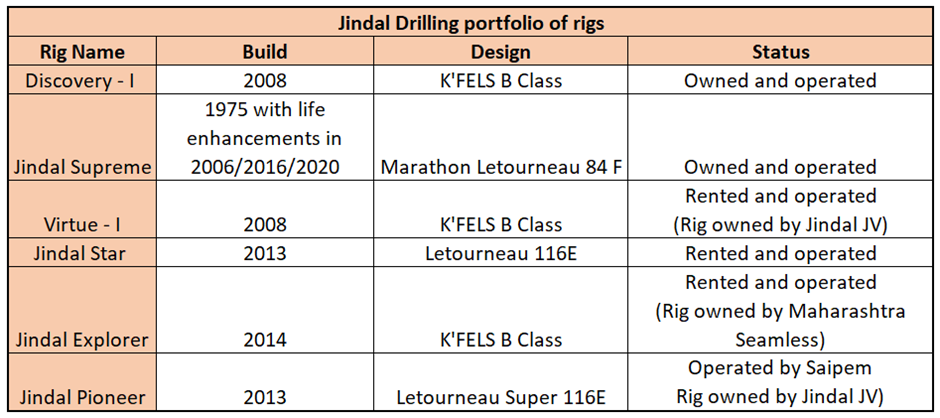

Jindal Drilling currently operates 5 jack-up rigs in India with ONGC. It owns one more rig via a JV which is currently deployed in Mexican waters and is being operated by Saipem. Of the 5 rigs Jindal Drilling operates, 2 rigs are owned and the rest are rented. The company makes the best EBITDA margins on owned rigs as there is no rental cost involved.

Details of Jindal Drilling’s rigs are given below

Rigs are contracted out to E&P (exploration and production) companies on a daily charter rate basis which are denominated in USD. The current day charter rates for these contracts are as follows

Jindal Supreme and Jindal Virtue I have been re-contracted recently with ONGC at much higher rates than previously while the other rigs are still on the last contract cycle rates.

Jindal Drilling’s fleet of rigs are benign shallow water jack-up rigs. These rigs can be deployed up to a maximum seabed depth of 300-350ft. All of Jindal’s rigs are deployed in the Western offshore basin of India except for Jindal Pioneer which is deployed in Mexican waters. As can be seen from the table above, Jindal’s fleet is quite modern except for Jindal Supreme. Jack-up rigs have a typical life of 30-40 years which can be enhanced by significant periodic rehaul and refurbishments (as in the case of Jindal Supreme). Modern rigs have lower operating and maintenance costs and are more readily acceptable by E&P companies such as ONGC.

I think Jindal Drilling has strong near-term earnings spike visibility which can sustain for several years if the global demand-supply dynamics in the upstream offshore oil and gas segment remains as robust as it is right now. There seem to be structural supply dynamics in place which favour an extended upcycle for upstream oil and gas service providers. Detailed industry dynamics and outlook will be discussed below.

Offshore oil and gas Industry landscape

The oil and gas industry has gone through severely tough times in the last decade. Oil prices saw tremendous strength between 2011-2014, with prices consistently sustaining beyond 100$/barrel. This bull cycle led to a lot of overinvestments in the industry with little regard for capital efficiency or outlook.

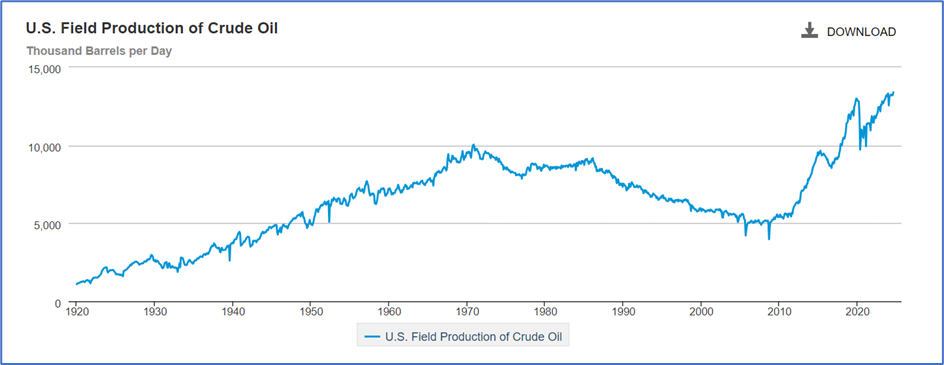

This bull cycle for oil was punctured for good in 2014-15 when US shale oil production started hitting new highs due to advances in hydraulic fracturing and horizontal drilling. US oil production zoomed from 5.5mn barrels/day in 2011 to almost 10mn barrels/day by 2015.

This resulted in a massive oversupply of oil into a slowing global economy. To make things worse, OPEC decided to maintain its production levels to retain market share instead of cutting production to stabilize oil prices. This supply glut caused oil to plunge to 35$/barrel in Dec 2015. Just as oil prices were starting to recover and stabilize around the 70$/barrel mark after 2018, Covid hit and brought the entire oil and gas industry to its knees.

The offshore oil and gas industry is especially susceptible to such sustained downturns in oil prices because it’s a very capital heavy industry. An offshore jack-up rig which can be deployed in ocean depths of up to 400ft costs can cost between 180-220mn USD. Semi-submersible rigs which can drill at depths of 1500-3000ft can cost as much as 500mn USD and drill-ships which can drill at depths of 10000ft can cost as high as 800mn USD.

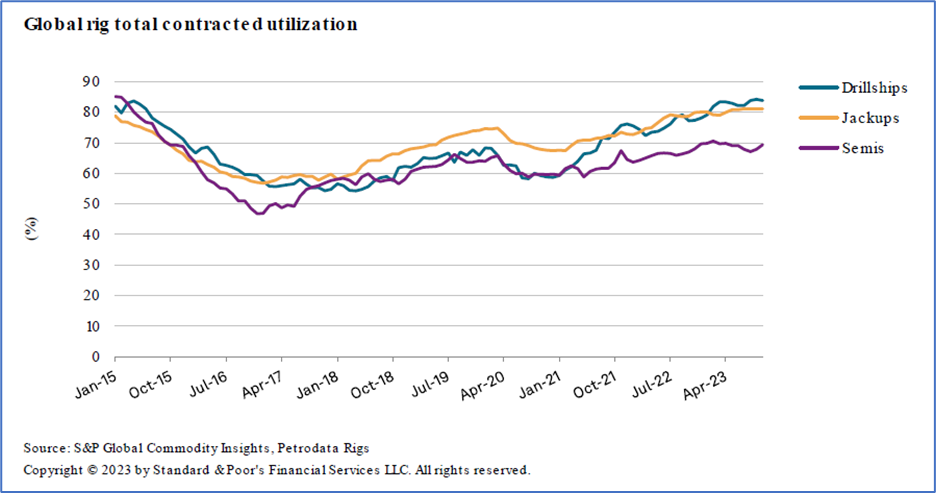

During this extended downcycle from late 2014 to 2021, the offshore rig industry went through very tough times. Some of the largest global offshore rig companies went through bankruptcy post Covid such as Valaris, Seadrill, Noble Corporation, Diamond Drilling, Pacific Drilling etc. There were also a host of mergers as the industry consolidated. This period saw many offshore rigs being cold stacked (complete deactivation of rigs to save running costs; It takes considerable time and capital to get cold stacked rigs back up to working condition) and many older rigs getting scrapped as the higher maintenance costs stopped making sense. Jack-up rig day rates plunged from 150k USD/day to 40k USD/day and the global jack-up rigs fleet utilization dropped from the high 80%s to low 50%s.

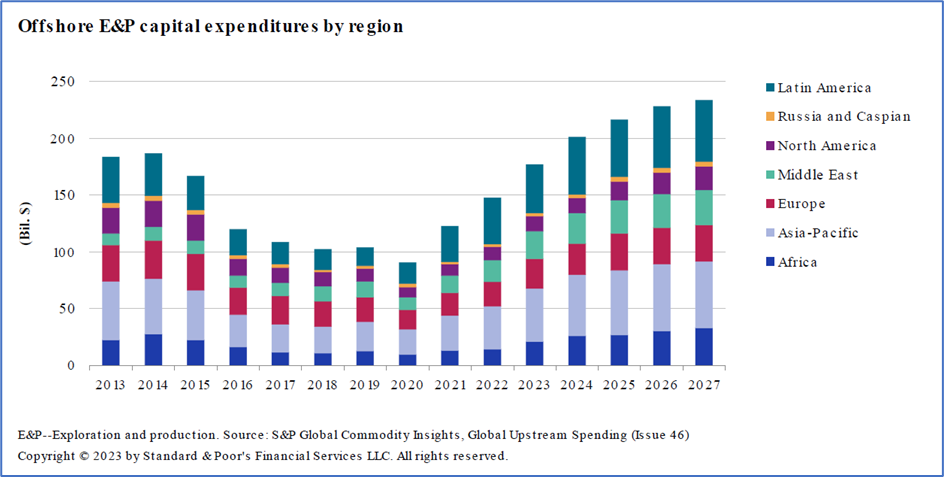

Since 2021, the oil and gas market seems to have come into better balance. Offshore spending by E&P companies has been steadily rising since 2021 with Middle East, Asia Pacific and Latin America taking the lead. Offshore spending on oil and gas is expected to be robust for the upcoming years with relative stability in global oil prices and maturing US shale production which has high oilfield decline rates.

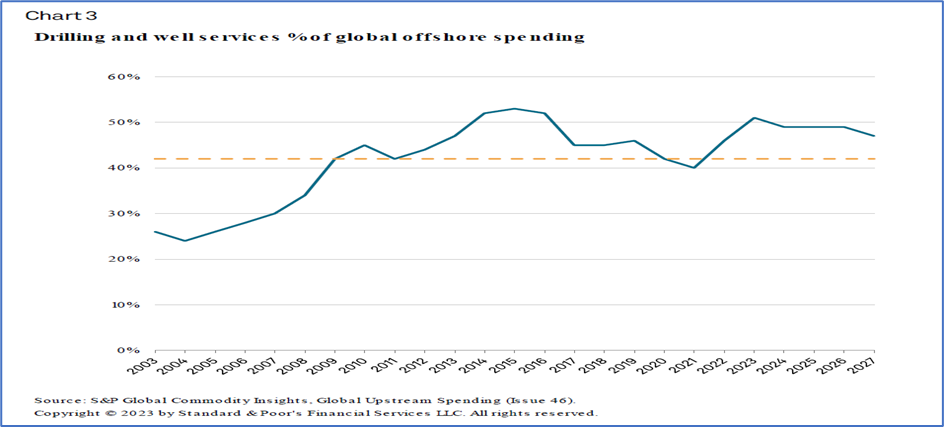

Drilling and well services comprise about 46% of the total global offshore spending.

The painful 7-year downcycle and the rise of renewables in the 2010s has caused some fundamental changes in the capital deployment approach of E&P companies. Earlier, in the early 2010s, E&P companies were happy to overspend and undertake exploration projects which were remunerative on return on capital basis. Since going through the downcycle and an industry-wide consolidation and bankruptcies, oil and gas E&P companies are now far more discerning about the projects they choose to invest in. You will see most companies in the oil and gas upstream value chain talk about return on capital and return of cash to shareholders in their investor concalls and annual reports. The lingering uncertainty about future oil demand in the wake of the renewables boom has also caused upstream companies to be very cautious with new capital deployment.

This change in attitude has brought a lot of discipline to the supply of upstream oil and gas assets such as drilling rigs. This seems to be structural in nature and if it persists for the medium term (3-5 years), then existing working-condition assets in the upstream oil and gas space should see limited supply and therefore strong charter rates.

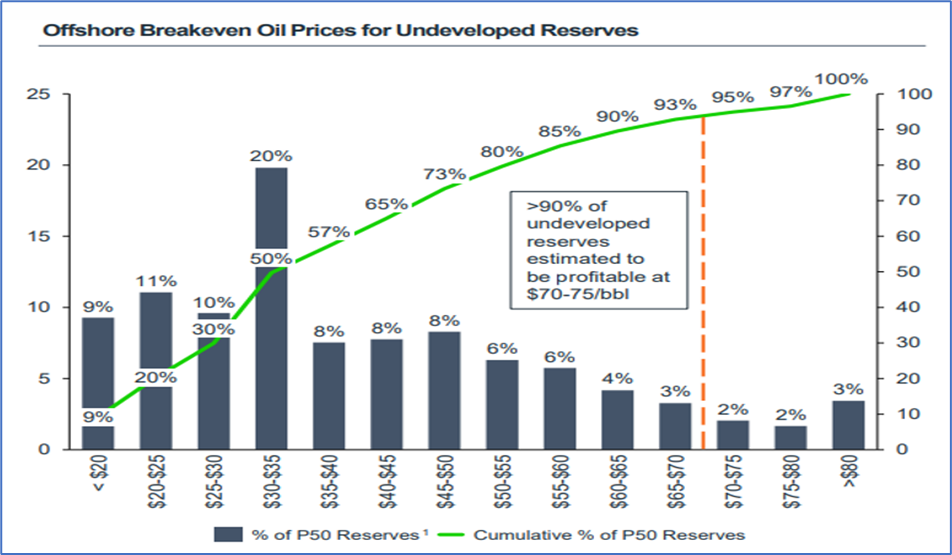

While there are lingering concerns over the near-term price of crude oil, it is interesting to note that ~90% of P50 offshore oil reserves are profitable if crude oil price is above 60$/barrel in the medium term. P50 oil reserves are those where the probability of actual oil reserves exceeding the estimated reserves is expected to be 50%. Thus, unless oil prices see a sustained downturn below 60$/barrel, E&P companies are unlikely to stop or curtail their offshore well drilling plans.

This suggests that barring a Covid like event, the offshore oil and gas drilling industry maybe in a structural upcycle for the medium term.

Jack-up rigs market landscape

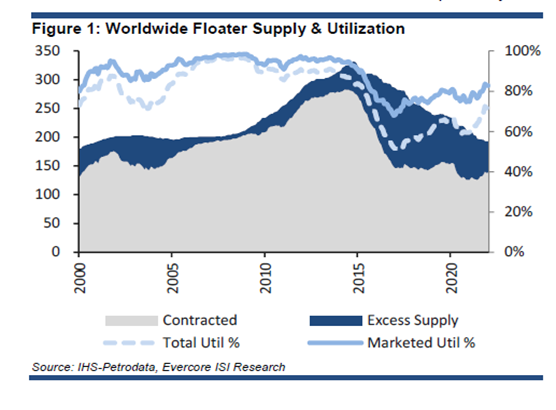

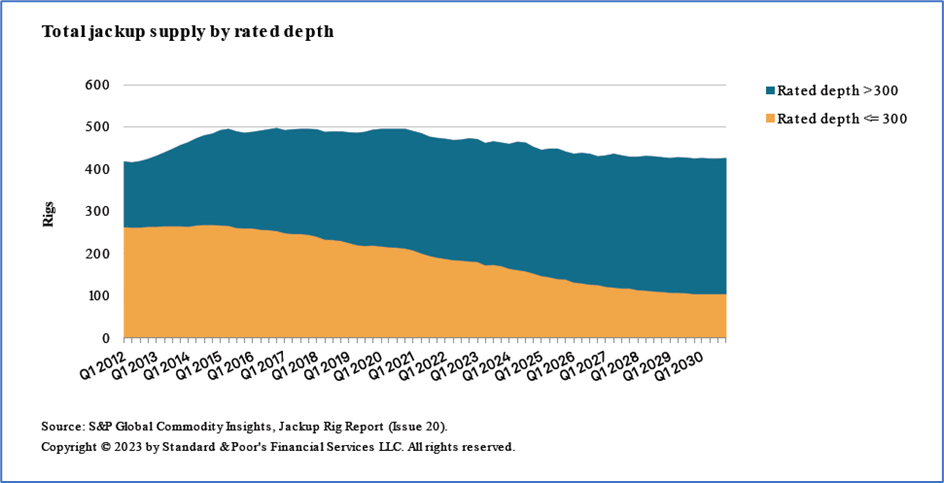

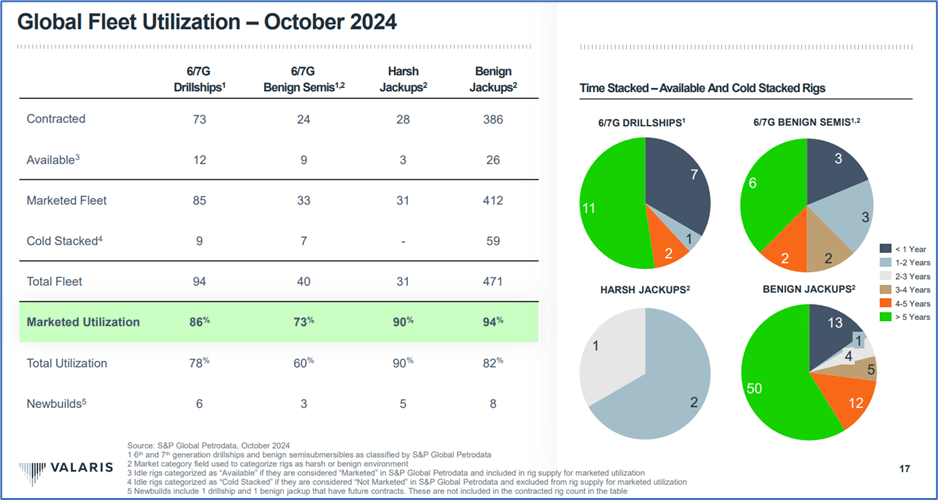

The global supply of jack-up rigs is around 471 nos. at present. This number has been steady over the last decade and is expected to remain in a similar range through the rest of the current decade.

Although the nos have remained similar over a decade, the quality of the global fleet has improved with a bulk of the current fleet now having capability to drill beyond 300ft depth.

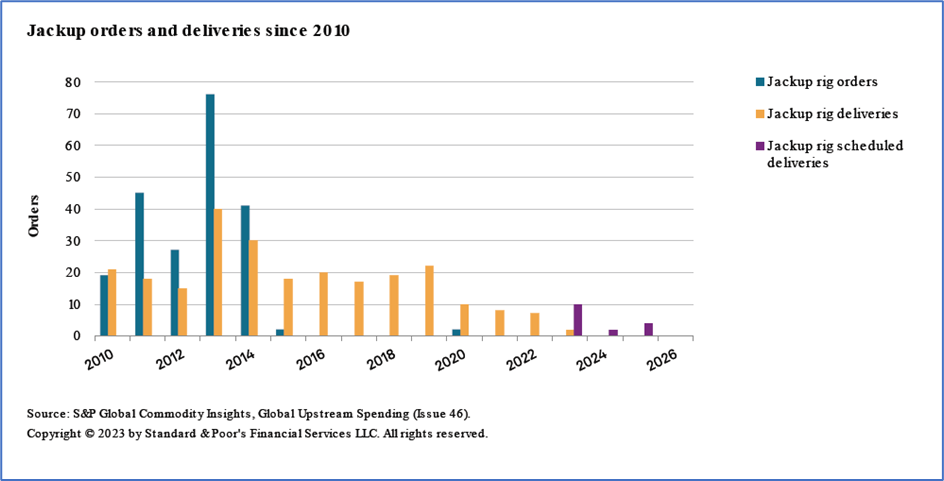

There have been practically no new jack-up rig orders placed with shipyards since the last cycle peak in 2015. The total no. of rigs undergoing construction as of late 2023, was 20 in number. These are expected to come into supply over the next few years. However, they represent less than 5% of the existing fleet size of 471 and are therefore not expected to impact supply dynamics materially at all. This is in sharp contrast to the previous cycle peak in 2013-2014 when 120 newbuild orders were placed with shipyards.

Due to the persistent underinvestment in new jack-up rigs over the last decade, 30% of the current fleet is over 35 years old and is nearing end of life. This means that 30% of the current fleet may not be in contention for a lot of new contracts which demand modern rigs with higher specifications.

The tight supply conditions illustrated above, coupled with steady offshore E&P demand has resulted in utilization rates for offshore rigs going up significantly.

Out of the total fleet of 471 jack-up rigs, 59 are cold stacked and only 412 are actively marketed globally at present. The utilization rate for the marketed benign water jack-up rigs is 94% as of October 2024. High utilization rates are expected to sustain as new rig builds are low in number and the cold stacked rigs are only expected to come into supply if there are contracts in hand for them.

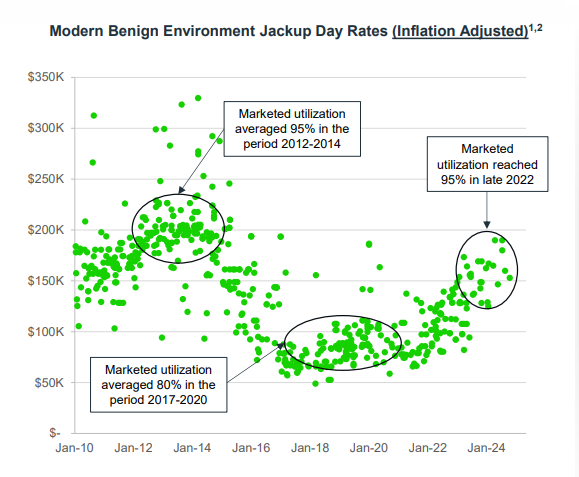

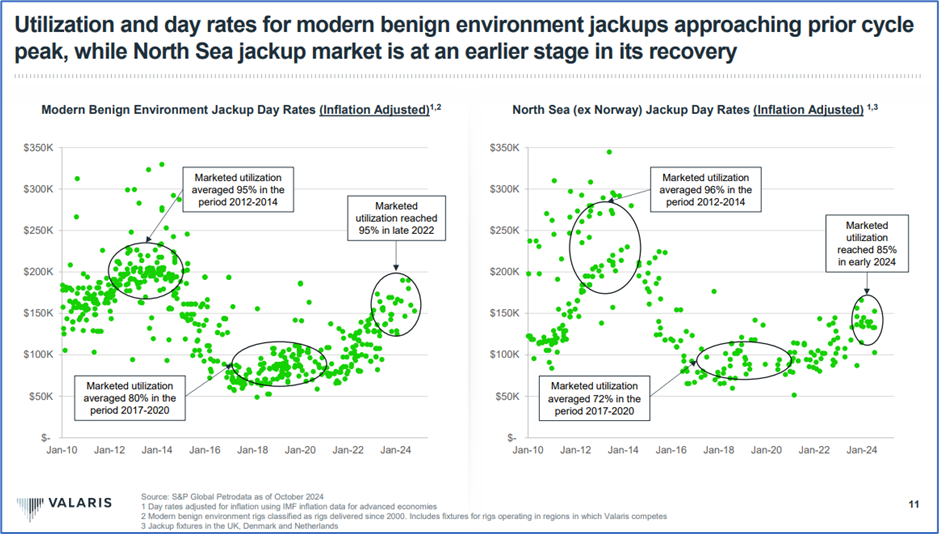

Charter rates for modern (built post 2000) benign environment jack-up rigs have increased significantly post Covid. However, they are still well short of the prior cycle peak (Left hand side chart below)

Indian jack-up rigs market landscape

As of Aug 2024, there are 37 contracted jack-up rigs in Indian waters with a bulk of them being contracted by ONGC. Of these 37 rigs, 32 are hired by ONGC from 3rd parties like Jindal Drilling while 5 are owned and operated by ONGC. Apart from ONGC, smaller E&P operators who contract jack-up rigs from time to time are Reliance, Cairn Oil and Gas (Vedanta), Oil India and HOEC.

The key players in the jack-up rigs market in India are Shelf Drilling (Global MNC currently operating 9 jack-up rigs), Jindal Drilling (owns 4 rigs outright/via JVs/via related parties and operating 5 jack-up rigs) and Greatship India Limited (Subsidiary of GE Shipping, owns and operates 4 jack-up rigs). Apart from these, Jagson International also owns 4 jackup rigs but all of them are quite old with build years ranging between 1975-1982. Aban Offshore also owns 4 jackup rigs but the company is deeply troubled with a negative net worth and hence may not be in a position to actively compete for new rig tenders.

ONGC awards offshore rig tenders on a 3-year basis. Once contracted, both parties are bound by the terms of the agreement and contracted day rates cannot be arbitrarily modified or the tender cancelled by either party.

The present Indian Govt has shown an increasing intent to push domestic oil manufacturers to increase the domestic production of oil and gas to reduce import dependency. The oil and gas minister has recently said that E&P projects in India offer an investment opportunity of $100bn USD by 2030. While these projects will take time to materialize into revenues for companies like Jindal Drilling, there is a clear push from the Indian Govt on companies like ONGC to maintain and increase their domestic oil production.

The no. of wells ONGC has drilled over the years has been quite stable with little dependency on the price of global crude oil as can be seen in the table below. Govt owned companies like ONGC often prioritize strategic national interests over profit maximization or return on capital. Energy sufficiency is a key item of national interest for India. This bodes well for companies like Jindal Drilling.

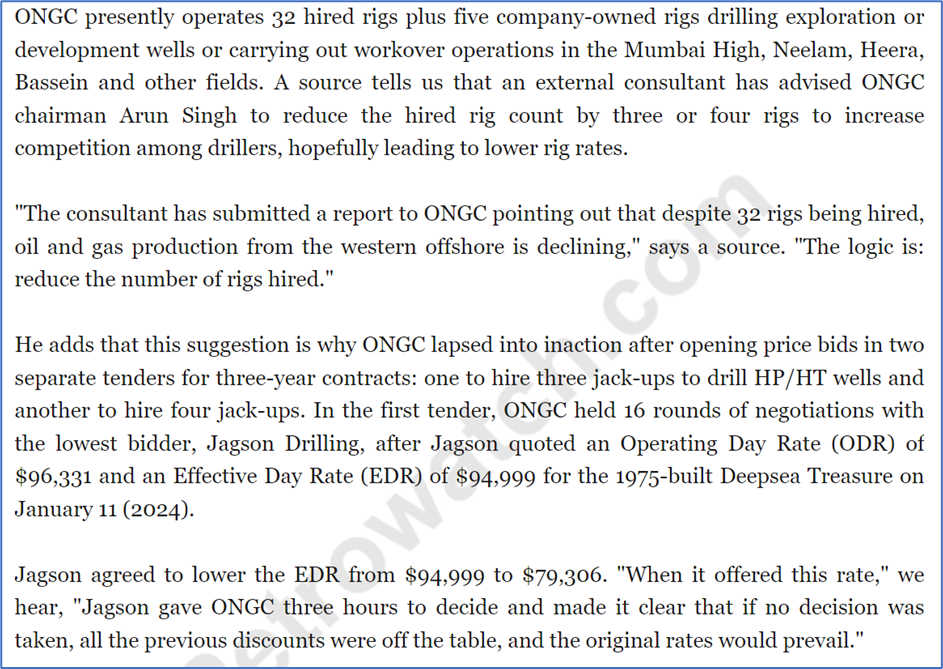

The domestic jackup rigs market got a little spooked in June and Sep 2024, when ONGC decided to cancel or postpone negotiations for re-hiring 7 jack-up rigs over two rounds of negotiations. Industry insider speculation suggests this is a tactic from ONGC to bring down day-rates to more acceptable levels. A snapshot from the article is presented below.

Industry participants expect the posturing by ONGC to be of limited impact as global supply of jackup rigs and day rates both remain tight and ONGC cannot afford newbuild rigs owned by Indian companies to leave Indian waters from a strategic point of view. Industry participants expect new day-rate contracts to be awarded in the near term to continue to be in the 65k USD/day-90k USD/day price range.

Jindal Drilling outlook

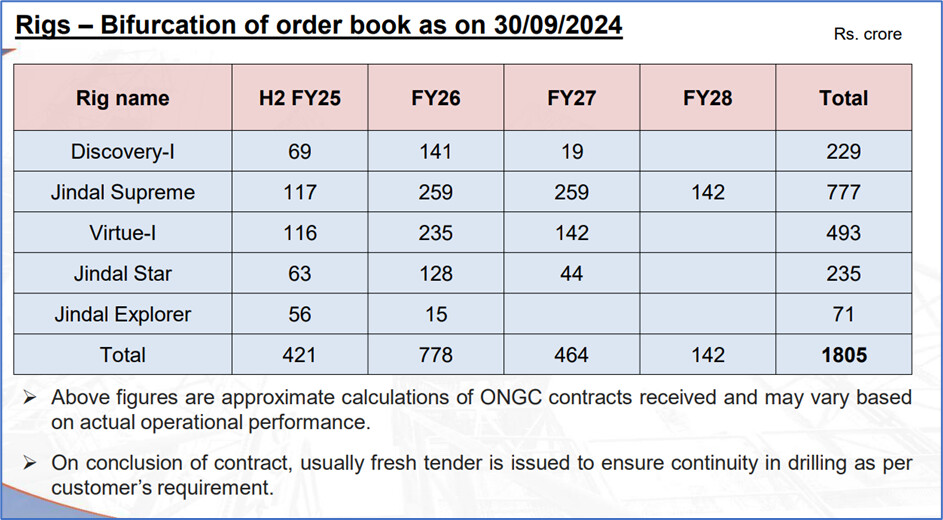

Starting H2 FY25, Jindal Drilling has a very strong earnings outlook for the next 2 years as depicted below in the order book breakup presented by the company.

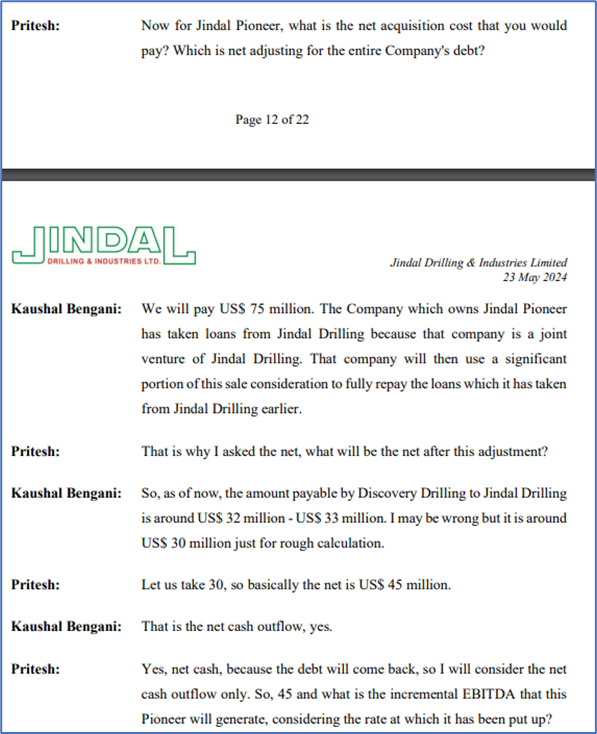

This outlook does not include the impending purchase of Jindal Pioneer by Jindal Drilling. Jindal Pioneer is currently owned by Jindal Drilling’s JV, Discovery Drilling Pvt. Ltd. Jindal owns 49% in the JV and therefore recognizes only half the profits the Jindal Pioneers in its books at present. Once the acquisition is complete, Jindal Pioneer’s full profits will start reflecting in the books of Jindal Drilling.

Jindal Supreme – The key asset

The key driver of strong profits for the next 8 Qs is going to be Jindal Supreme, which started work under a 3Y contract with ONGC from 10th October 2023. This asset was previously contracted at a rate of 40700 USD/day with ONGC. Since undergoing refurbishment from March-Sep 2024, the asset has now been re-contracted for a period of 3 years at 88859 USD/day, more than double its earlier rate. Jindal Supreme is one of two wholly owned assets of Jindal Drilling and hence does not incur any rental costs for operation. This asset was earning ~10% EBITDAM in its previous contract of 40700 USD/day. With the rate increasing to 88859 USD/day, almost all the incremental day rates will accrue directly to EBITDA. Hence this asset can start reporting a quarterly EBITDA of INR 37-41 Cr starting Q3 FY25.

Since Jindal Supreme is an old asset (Build year 1975), it had to undergo major refurbishment before entering this new contract. The total expenditure towards refurbishment is upwards of INR 130 Cr as confirmed by management in the Q3 FY25 conference call. While the exact expense number is not known, I’d think it to be in the proximity of INR 200 Cr. A bulk of this refurbishment expense is capitalized by the company and is amortized quarterly over the period of the contract. Assuming INR 20-25Cr of the 200Cr refurbishment expenses were taken directly into the P&L in H1 FY25, that would leave about INR 180Cr to be amortized over the next 12 Qs (3-year contract duration). This would lead to an INR 15Cr Quarterly refurbishment amortization expense, leading to a net quarterly EBITDA from Jindal Supreme in the range of INR 22-26Cr starting from Q3 FY25 (Gross EBITDA of INR 37-41Cr minus refurbishment expense of INR 15Cr)

Jindal Pioneer – A purchase optionality about to play out

Jindal Pioneer is owned by Jindal Drilling’s JV entity Discovery Drilling Pvt. Ltd. with Jindal owning a 49% share of the JV. The rig is currently offered on rent to Saipem for drilling operations in Mexican waters since 2019. The charter rate for the rig is 35000 USD/day at present which will increase to 40000 USD/day starting Jan 1st 2025. This is a bare-boat charter contract where all operating costs are borne by the operator, Saipem. As a result, almost the entire day rate flows to EBITDA for the JV entity and a bulk of the EBITDA flows to PBT. The JV entity seems to be reporting a PAT in the range of 18-20Cr per Q. 50% of this is reflected in Jindal Drilling’s consol PAT numbers i.e. about 9-10Cr INR per Quarter.

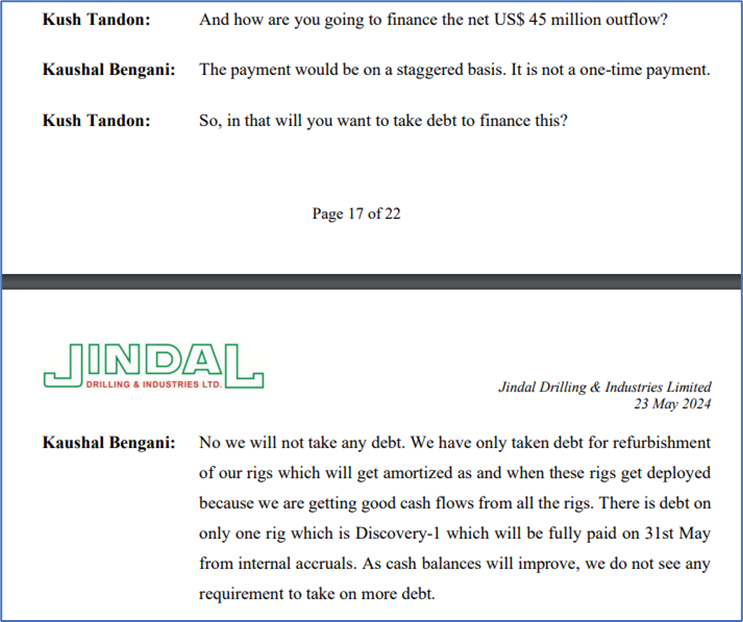

Jindal Drilling is on the verge of buying out Jindal Pioneer from the JV entity for 75 million USD. The transaction has already been approved by shareholders and is awaiting certain regulatory clearances which are imminent. Once Jindal Pioneer comes on the books of Jindal Drilling, the PAT contribution from this asset to Jindal Drilling will jump from INR 9-10 Cr range to INR 18-20 Cr range. This transaction is likely to go through before the end of this year. The net cash outflow for the purchase deal is expected to be around 45 million USD only which will be paid in tranches from internal cash flows without raising any external debt (Specifics of the transaction explained in the snapshots below)

Quarterly PAT can show significant upside starting Q3 FY25

As per estimates, Jindal Drilling can start reporting INR 50-60Cr quarterly PAT starting Q3 FY25 for the next 6-8 quarters straight. Let us see how we arrive at this number

-

Base case standalone PAT – Let us consider the Q4 FY24 standalone PAT numbers as our base case. This was a Quarter in which all 5 assets were operational (Jindal Supreme was operating under old rates of 40700 USD/day and stopped operations on 24th March, 2024). The base case standalone PAT is INR 32Cr.

-

Additional PAT from Jindal Supreme - As discussed above, Jindal Supreme can report a quarterly EBITDA of INR 22-26Cr from Q3 after netting off the amortization of refurbishment expenses. Most of this EBITDA should flow down to PBT and should contribute INR 15-18Cr of additional PAT per quarter.

-

Optionality from Jindal Pioneer purchase - At present, the two JVs DDPL (which owns Pioneer) and VDPL (Which owns Virtue-I) are reporting a Quarterly PAT of INR 9-10Cr each at the level of Jindal Drilling consolidated. If Jindal Pioneer is outright bought by Jindal Drilling, then its PAT contribution to the company’s nos will double leading to an additional INR 9-10Cr of PAT.

-

Taken together, item nos 1-3 illustrate that Jindal Drilling can start reporting a Quarterly PAT of INR 56-60Cr starting Q3 FY25 for the next 6-8 Qs at least.

Outlook beyond the next 6-8 Quarters

Jindal Drilling has three rigs finishing their existing contracts in the next 2 years. Jindal Explorer finishes in May 2025 and Jindal Discovery I and Jindal Star finish respectively in May 2026 and July 2026. These rigs are operating at low day rates presently in the range of USD 39k-45k/day.

As discussed earlier, while the recent rig contract cancellations by ONGC have caused some concern in the industry, the broader global industry dynamics dictate that ONGC should come around to re-contracting these assets for the next cycle at rates between USD 65k-90k/day. If it does not do that then it risks these rigs leaving Indian waters to seek fairly priced contracts in other strong offshore markets such as SE Asia and Latin America. Therefore, it is not unreasonable to assume that all 3 rigs will find significantly remunerative and EBITDA accretive contracts for the next cycle where day rates will be far superior to the current day rates for these assets.

If the robust offshore environment persists, then Jindal Drilling has the optionality to also purchase the other JV rig, Jindal Virtue 1 in the coming few years. This should help increase the company’s PAT and cash flows similar to how the acquisition of Jindal Pioneer is likely to do the same in FY25.

Hence, the medium term (3-5 year) prospects of Jindal Drilling look quite stable with a high probability of sustained high cash flows and PAT. Jindal Drilling has a very comfortable balance sheet and increase cash flows from the repriced contracts should help maintain their balance sheet strength going forward.

Valuations

On a rolling 4 quarter basis starting Q3 FY25, based on the contracts in hand, Jindal Drilling seems to be trading at a forward PE multiple of 8-9x (Based on current MCap of 1974Cr and rolling 4Q PAT expectations of INR 225-240Cr). With a strong balance sheet and expected strong cash flows from the higher rate contracts, there doesn’t appear to be much of a downside risk to stock prices at current levels.

Material risks to be aware of

-

A Covid like disaster which pushes global oil prices below 60$/barrel on a sustained basis leading to cancellation or non-renewal of drilling contracts by global E&P majors

-

In 2024, there have been some concerns about the rig contracting environment after Saudi Aramco decided to release 27 jackup rigs (6% of global jackup rigs supply) from contracts in H1 CY24. However, 8 of them have already re-contracted in other markets and 1 has been scrapped while about 10 others are thought to be internationally uncompetitive and hence not likely to be a source of supply disruption

-

ONGC being adamant about rates, successfully negotiating lower than expected rates for Jindal’s assets which are coming up for re-contracting in FY26 and FY27 leading to lower than expected profitability. Although Jindal Drilling has the optionality of taking its rigs to international waters in that case, as it had done with Jindal Pioneer in 2019, which was taken to Mexico

-

Management has not explicitly called out the refurbishment expense for Jindal Supreme. I have assumed it to be INR 200Cr and hence calculated Quarterly amortization expenses of INR 15Cr. If the refurbishment expenses are materially higher (Unlikely, in my opinion), then there is an upside risk to the amortization nos and a downside risk to the Quarterly PAT projection of INR 56-60Cr.

Sources

- Jindal Drilling concalls (There are only 5 till date, should be an easy read)

- Annual report FY24

- S&P Global Offshore Energy Sector Outlook

- Valaris Limited Q3 CY24 Presentation and Conference Call

- Shelf Drilling Q2 CY24 Presentation

Disclaimer: I have investments in the stock as part of my portfolio and hence I am biased. Offshore oil and gas is a cyclical sector, so please do your own due diligence on sector outlook for the next few years. My analysis can always be wrong and I may change my view or portfolio allocations at any time.