This is the first time in company history that all the rigs are operated simultaneously.

After completion of the 3 years contract rigs go for refurbishment which can take up to 4-6 months and significant money. Rigs are operated 24 hrs a day 365 days a year. Before getting into new contract recertification is necessary. Reasonable amount of money is spent in refurbishment. Jindal Supreme is a very old rig and company spent north of 130 crs to refurbish it. (Q2FY5 concall)

If someone wants to buy a new rig cost is nearly 2400 crs and waiting time is 3 years. So supply of new rigs in market is very limited. New rigs are not being manufactured because even at current rates payback period is > 10 years.

Jindal Explorer Tender is submitted and waiting for outcome.

Jindal Supreme operated only for 75 days in Q3. It will operate for 90 days in Q4 so further upside in profitability is expected. My Estimate is 5 crs.

Jindal Pioneer acquisition should conclude this quarter. If that happens then additional profit of 9-10 cr per Q. Although depreciation will also increase.

For this acquisition payout is 75 Million Dollars. 30 Dollars is already given as loan to JV partner. So net cash outflow is 45 million dollars which will be payable in tranches over the years with internal accruals and no term debt.

From 2021 company has brought 2 rented rig under its own balance sheet. Going forward also this will be the focus. Because O&G upcycle is here and opportunity for acquisition are virtually close to zero.

For rented rigs rents are also renegotiated when days rates are negotiated.

Jindal Pioneer will be bought to India unless it gets a day rate of 1,80,000 dollars. Operating costs are very high in international waters.

Nice write up @nirvana_laha. Makes for a convincing case for investing in the business. While going through this, one of the things that caught my attention was the below paragraphs from the document shared by @sougataG above:

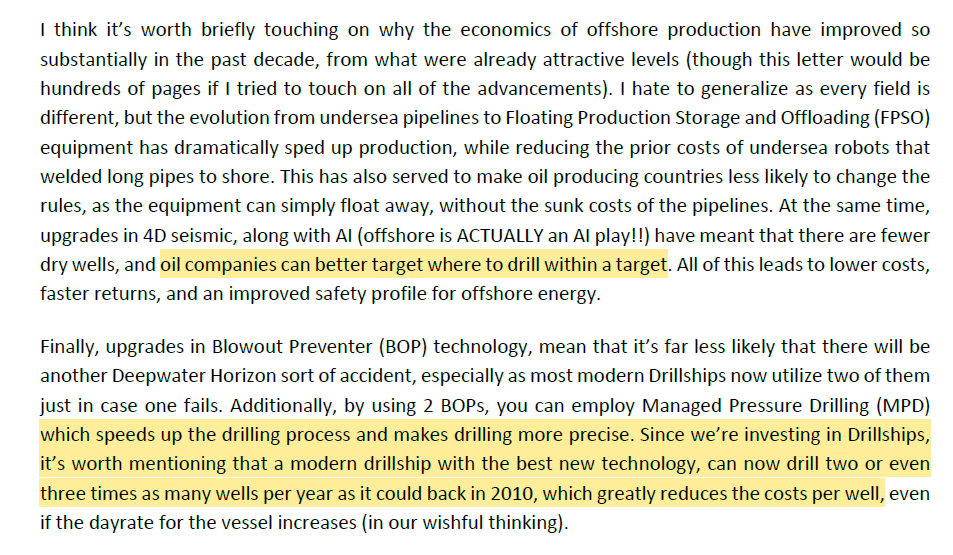

Here my thought is - will not the above (as well as any other) advancements in technology reduce the demand for drilling rigs, making the demand - supply equation less skewed than what it seems at first sight? I have seen this paradox in many industries such as lubricants and refractories, that as products get better and better, you need less and less of them to achieve the same result, impacting demand. Some searching on the internet revealed this is not just a figment of my imagination, there is indeed such a possibility (from this article):

Hi @Chandragupta, The note from Praetorian Capital focuses mostly on drill-ships because their investments are in companies that deploy drill-ships. Jindal Drilling deals with jack-up rigs. I don’t have enough knowledge to determine whether these advancements for drill-ships would apply also to jack-up rigs or not. Maybe industry veterans can chip in here.

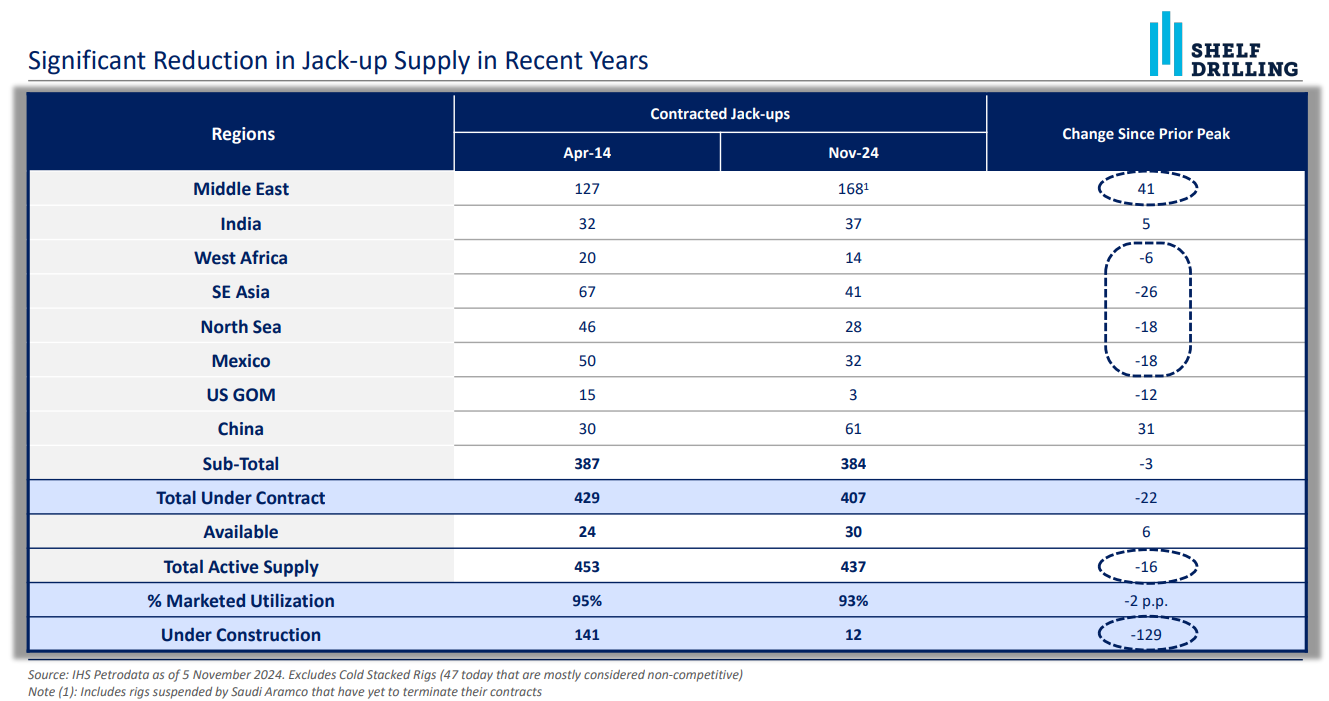

But even if that is the case, the current marketed fleet utilisation of 93% and prohibitive cost of newbuilds give me comfort about the supply side of the equation. You can refer the below slide from the presentation of Shelf Drilling, I think they are the largest jack-up fleet owner in the world.

Hi, Thanks for the clarification, I missed the two are different (new to the subject !). Need to see whether similar factors apply for jack-ups also. But even in the table above, the “available” has increased from 24 to 30, which needs probing further. I am not disputing the overall thesis but just wondering if this is one additional risk factor one should keep in mind (that less can do more, so less is good enough). Otherwise the overall case is well made out. Thanks.

ONGC signs a contract with BP to enhance O&G production from Bombay High. There is a clear push from Govt and ONGC to increase domestic O&G production which bodes well for drilling companies.

Whether this contract will have any direct positive impact on drilling demand in Bombay High or not is not immediately clear to me. It could be that BP will help increase efficiency of existing fields being drilled and this may not result in incremental demand for drilling rig operators, or it could be the opposite. We will find out during the next investor call I suppose.

Wanted to share this interview with the ONGC chairman relating to this announcement. This is a good question for management on the next call. Specifically with regard to their recovery percentage and if BP can add value if at all.

Does the topline of company have any relation with the USD/INR exchange rates?

Since the daily rate of each rig is mentioned in USD in the company presentation, is it possible that rising USD(compared to INR) would positively affect the topline, and vice-versa.

Any idea how are currency exchange rates accounted for in the billing, is it considered on daily basis, or are the terms decided when a contract is agreed upon. The INR was depreciating every day for the entirety of Q3, and even in current quarter, the INR/USD rate has been very high for the quarter thus far, higher than highest it went in Q3. Does it mean, it gives the Q4 topline an unintended boost?

And are the expenses also dependent on forex rates?

What is your topline expectation from Q4, the management commented that PAT is going to be similar to Q3, but shouldn’t Revenue and PAT both improve because the newly commissioned rig will be working for full 90 days, compared to 75 days in Q3.