hello everyone.

While going through annual report for FY 24 i came across below

I have below queries. requesting members to please help in understanding these details.

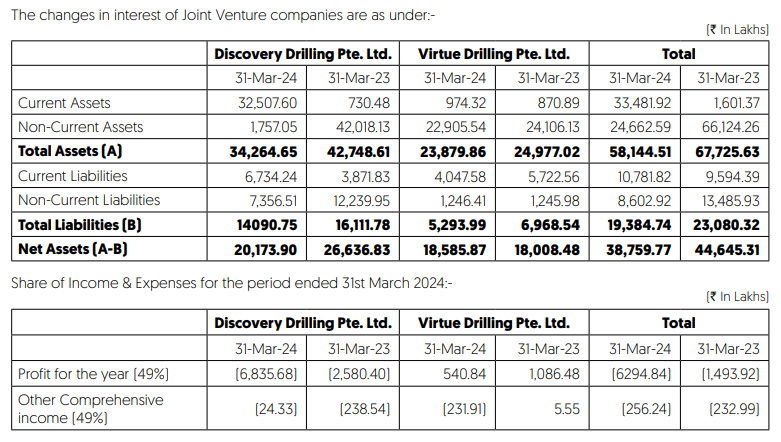

- The net asset mentioned are only 49% asset of JV.(Attributable to Companies shareholding?

- If so, it means 49% of rigs is valued around 200Cr . hence complete RIG book value may be around 400Cr. This seems pretty low. (Jindal is paying 650Cr for 51% of Rig. How come its own share is only worth 200Cr). What am i missing?

- Profit from Virtue Joint venture for FY24 is only 5.4Cr (I understand its only for 2 Quarter). Still it seems pretty low (2.7Cr/Q). So if Jindal will buyout Virtue, it may only add 10Cr annually?

4)Is there any source to go through reports of JV in more details?

Disclosure: Invested