Vaping has been found to be more harmful than cigs. You can do a google search for the same.

6 Likes

Thanks, yes we understand this now, but my question is until just couple years back, the idea was different, why? Is this a sudden realization because of any particular reason? Vaping was supposed to provide people option to leave more harmful cigarette earlier…

how, why & when this new realization happened? And what does it mean for Vaping industry in US/Europe/UK, any future vaping industry in India & Cigarette industry globally?

1 Like

Well, it takes time for a new harmful product to show its effect on the human body. The clinical research only came later when many youngsters started reporting lung infections.

3 Likes

2 Likes

As a consumer i agree if we ignore Maggie classic most of there other flavour are very disappointing and not have catch-up that well.

As a foodie Maggie classic is still the best overall but if you want something else itc and other are actually better in developing better taste overall and also itc is more likely to have better aquisition policy then other FMCG players.

3 Likes

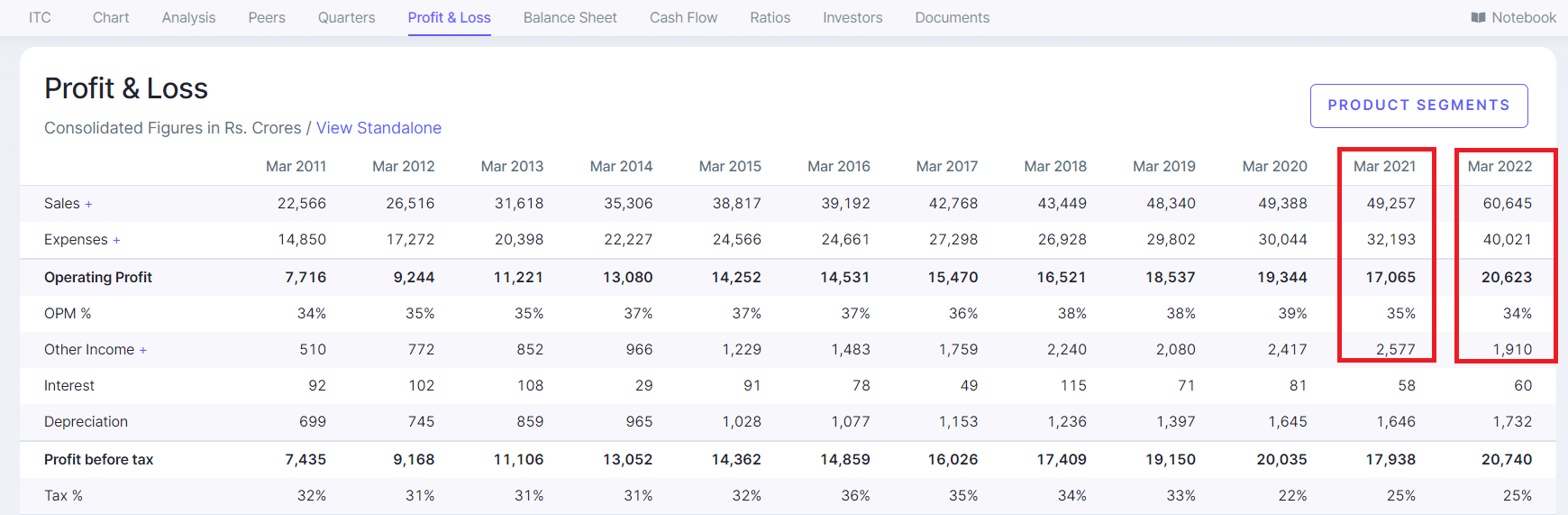

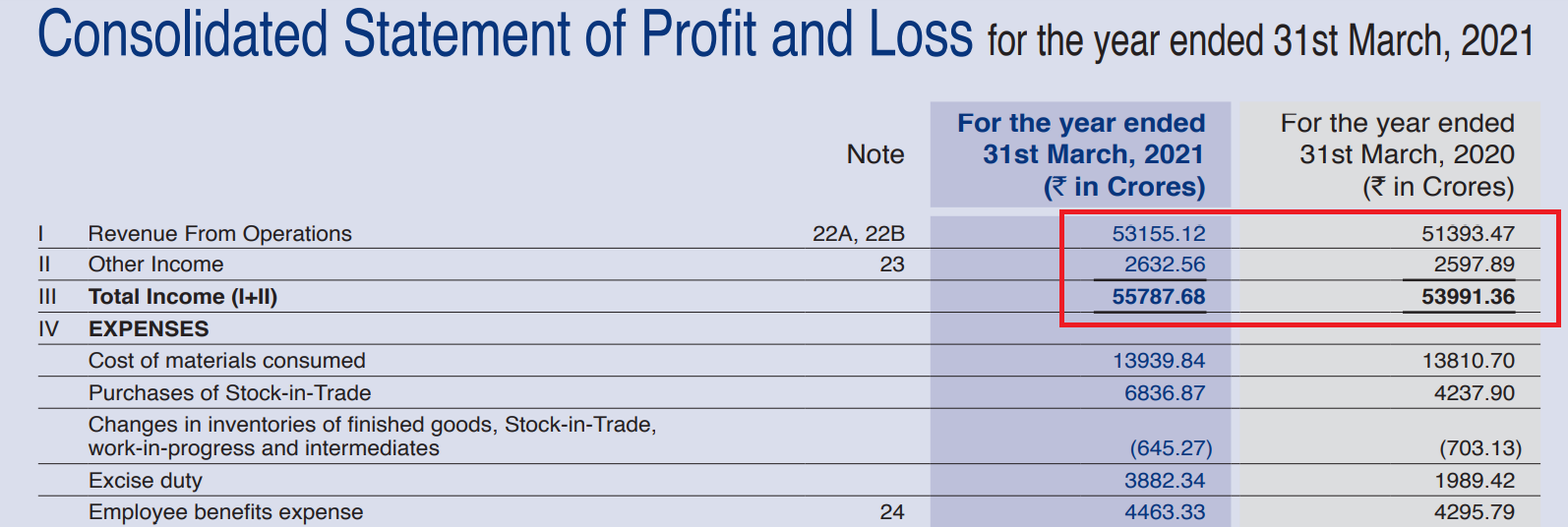

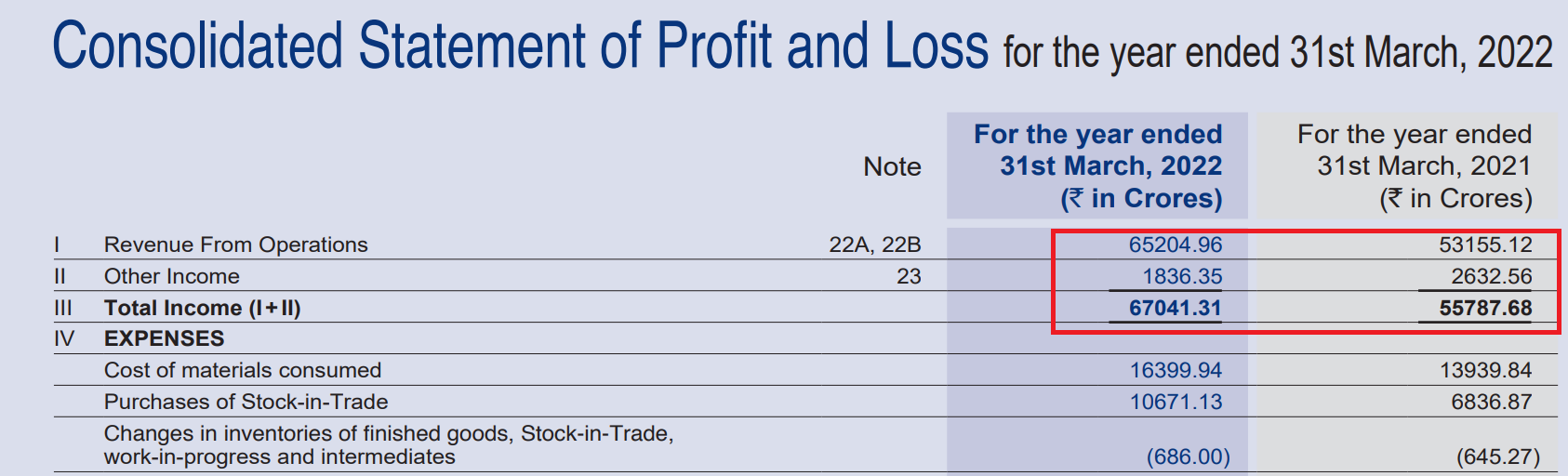

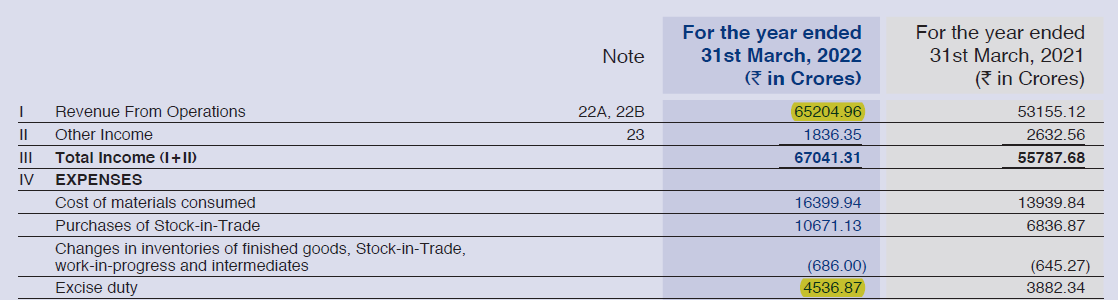

Any idea why the revenue figures for ITC on Screener do not match those declared in the Annual report? There’s a delta every FY.

AR FY21

AR FY22

Deduct excise duty amount of ~Rs 4,500 Cr from Revenue from operations and you would be able to reconcile the figure broadly.

10 Likes

Most of the complaints about ITC FMCG was that its products doesn’t have a shelf space in stores. I have revisited my hometown ( tier-2 city ) after two and a half years. Last visit was pre-covid end of 2019 and this time I have travelled around. My observations here are limited to two southmost states and please pay attention before extrapolating it for pan India.

Yippee

Yippee certainly has about 70 % of shelf space of Maggi ( No surprise that Maggi still tops the sales and shelf space). Maggi had a dedicated rack in addition to what’s shown above. Good thing is that its much more than what I have seen in my last visit. And my nephews ( one in college and another in school ) both knew about yippee ( which wasn’t the case last time).

As one can see there is cult following for Yippee as well as it triggered a massive arguments over internet.

That also augments well with the kind of growth that company has shown in the past 10 years. Habits take time to establish and Yippee may very well be in a good direction.

B-Natural

I must admit, I didn’t expect it to be popular at all. But I found many elders drinking the B-natural Guva flavour and it had as much shelf space as Real. I also don’t remember seeing it at all last time that I have visited.

B-Natural is number 3 in the market with and number 2 in the modern trade (e-commerce). Although it seems to have penetrated households, still some distance to cover. But I have seen them in the domestic flights in Indigo that could certainly play a good role in covering middle class population.

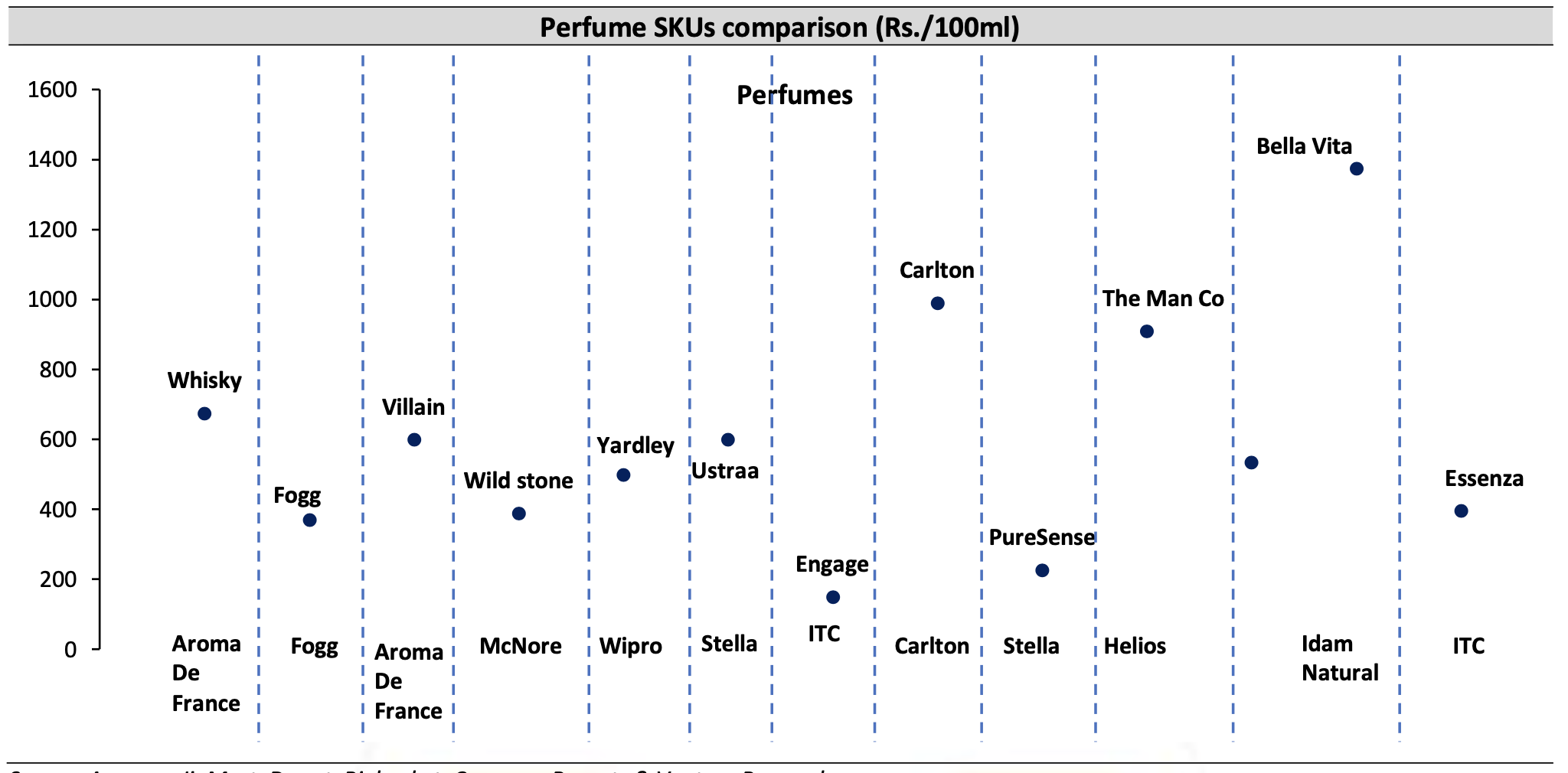

Engage Deo and Perfumes

Engage has about 12% market share compared to market leader Fogg that has 16% market share. Brand Engage was bought to market about May 2013. so in roughly 8 years they could bring the brand to number 2 position. As one can see there it has prominent space. I also found them everywhere including pharmacies. Its also favourably priced compared to others

Fiama body wash gel and Vivel

Indian showers are still dominated by detergent bars rather than liquid wash, but its expected to grow 15% cagr next decade. I myself tried Vivel and found it to be refreshing. One can also see shower to shower in the bottom shelves. But when it comes to soap HUL owns almost every brand and there is absolutely no competitions whatsoever. Although I was happy to find Fiama and Vivel soaps.

Sunfeast Biscuits

Moms Magic is a big hit and a good competition to Good day from Britainia. Sunfeast bounce also caught up pretty fast and moving well. I certainly see much more shelf space for sunfast than my last trip. But I must say Parle-G has certainly upped the game expanded to many categories. Now there is Parle Marie as well as Sunfeast Marie light.

Britania and Parle lead the market with 28% market share while ITC has about 11% market share. Given the late entry of Sunfeast compared to established players like Parle and Britainia ITC seems to have done well.

But whole section has lots of overlaps with even the packages looking similar to each other. Dark Fantasy also has a cult following, but Britania also came up with similar product including packing. If at all I worry I see than Britania is under pressure from Parle and ITC.

Bingo

I haven’t seen a single shop without Bingo chips. Mad angles seems to have better taste than generic chips but not many seems to be aware of it. In Kerala Bingo is number 1 for sure. I have seen shops without lays but not without Bingo. Pepsi has about 22% market share in western snacks while ITC has about 13 % market share. Recently it was reported in moneycontrol that Bingo is gona bring ethnic snacks like Aloo Bhujia and other things. This would be good accretive as brand Bingo seems to be well known.

Source: ITC reports, articles and Ventura Research

Disclosure: ITC is one of my biggest holdings, so my views are certainly biased. Please do your own due diligence.

40 Likes

It is good and heartening to see that ITC is doing a good job in grabbing more shelf space since it is a key requirement to increase the market share in these segments.

However, I still believe that ITC is not fully capitalizing the established brands like Ashirvad (cereals, sugar, salt), Sunrise (oil) and Savlon (hygiene). Dettol, Himalaya, Marico and even Godrej is coming up with innovative products in this space but is hard to see Savlon anywhere though it was once the #2 player in the market.

Likewise, while Ashirvad atta is available everywhere, you don’t get to see salt or other items.

Oil is another lucrative market but there is not much push from ITC. Saffola and Fortune are ruling this space.

It takes a lot of investment and time to establish and sustain a brand. But if they don’t exploit the full potential of such brands, they will lose out to the competition.

Disc: invested

2 Likes

One thing which I just noticed today is Mr. Devraj Lahiri is CEO of ciggarates division. He has worked with VST industries for 2 decades and used to be MD there post 2017. We have seen good execution by VST in last 2 decades. So, I think Mr. Lahiri leading ciggarates division is a good move.

4 Likes

Sundrop brand owned by Agro Tech was actually promoted by ITC. It was known as ITC Agro Tech Ltd. In 1999-2000, the business was transferred to ConAgra after it had acquired a controlling stake. Agro Tech is looking to reduce its dependence on oil completely and looking to increase its food business. Edible oils is not an easy business.

I would prefer if ITC concentrate and expands on what it has and not spent money just for the sake of innovation, more copy cat brands. ITC Fabelle was positioned as premium, instead they should have targeted the mass market and taken on Cadbury. Then should have moved to breakfast cereal segment and target Kellogs.

5 Likes

ITC has oil under its Sunrise Brand.

To my understanding ITC goes for complete self reliance… meaning they like to cover from seed to finished product. They want to have complete control and backward integration. So I really doubt if they would expand in this sector.

9 Likes

I went through 75% of this thread over the weekend (Will finish the remaining 25% by this week hopefully). Really thankful to this community for the depth of research (Especially scuttlebutt) in the thread. I get this feeling over and over when I deep dive into a new thread on ValuePickr ![]()

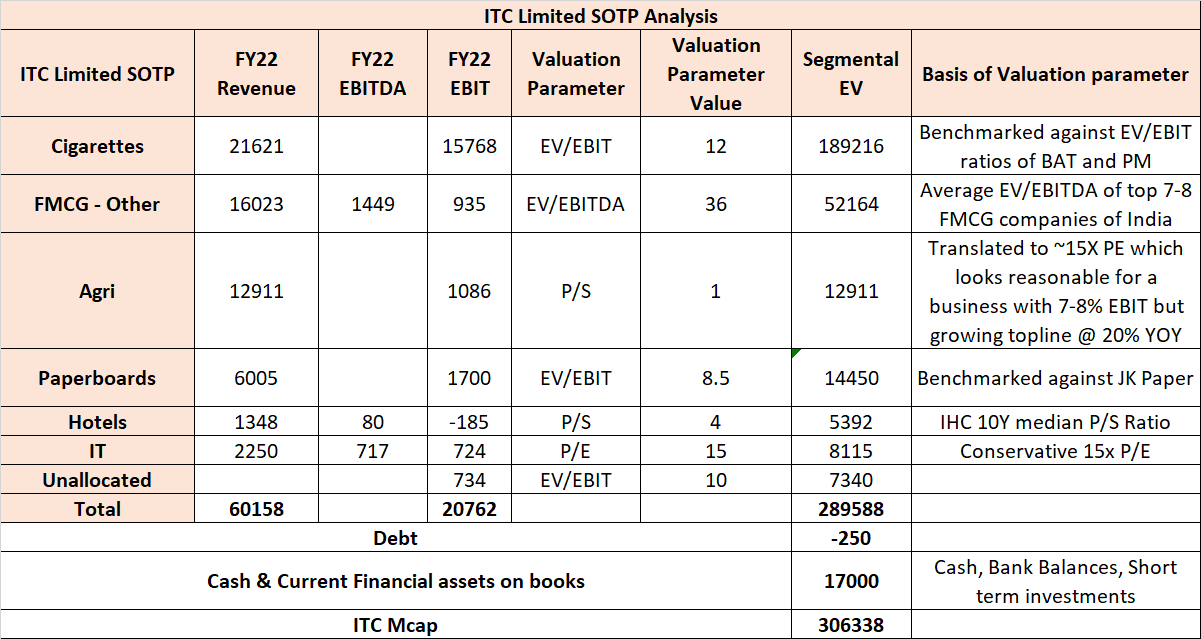

I did not see a valuation attempt undertaken for ITC in the thread, so here is my attempt at a sum-of-parts SOTP valuation of ITC. Your inputs on the approach taken and suggested improvements would be very useful. I will take those on-board and post a revamped valuation.

Going by this valuation framework, ITC at the moment seems to be overvalued by ~15%. Of course it is clear that FMCG others is grossly undervalued right now because I have valued it basis EV/EBITDA and EBITDA is subdued because ITC is still in heavy investment mode in this segment. If we value FMCG Others as per P/S (According to me this is premature. Let ITC stabilise margins at 15%+ before we take this approach) and assign a P/S multiple of say 8x (Average of top 7-8 FMCG companies in India), then the segment would be valued 2.5x higher than it is valued right now.

12 Likes

Markets always value it for the future and hardly for the current. Having said that @harsh.beria93 did a wonderful write up on this in his portfolio page

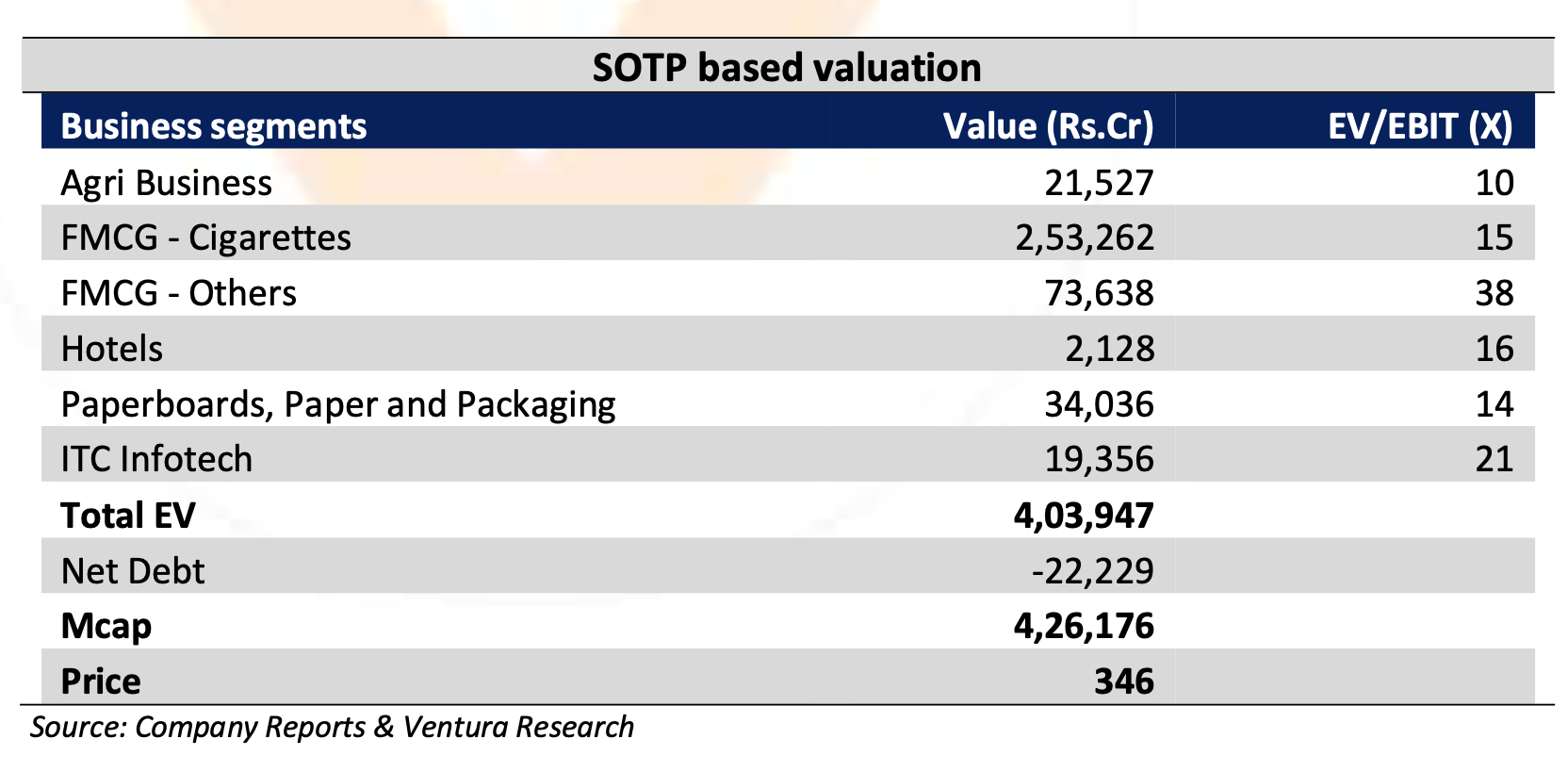

Attached SOTP valuations from Ventura below

5 Likes

Yes, my broad conclusion is consistent with yours. Markets are forward looking and the FMCG business is artificially undervalued right now if valued using an EV/EBITDA metric. As operating leverage plays out in the segment, the FMCG EBITDA will stretch its arms and take the entire company valuation much higher.

7 Likes

Recently visited this place. “Coffee by Us” is a Unilever brand. It mostly sells ice creams, shakes, chocolates and sandwiches. One of the few places in Ahmedabad to have kwality walls icecream. ITC has a complete portfolio with

Sunbeam coffee

Yippe noodles

MasterChef instant frozen foods

Fabelle chocolates

Yippee and bingo snacks and

Sunfeast milk products

Such brand outlets can also provide visibility to lesser known ITC food brands.

12 Likes

https://myneta.info/party/index.php?action=all_donors&id=3

https://myneta.info/party/index.php?action=all_donors&id=1

Why is ITC given political donations every year to both the ruling party and the opposition every year?

Also using ITC Infotech to donate

5 Likes

Not just ITC, many listed companies have donated to both the ruling and opposition parties. These are some of the big names from the links you have given, in top down order. Didn’t check all, didn’t need to. And you can see some big names in both categories.

Ruling party

Cadila Healthcare Limited

Lodha Developers Thane Pvt Ltd, Lodha Constructions

Century Plyboards (India) Ltd

Larsen & Toubro Limited

Mahindra & Mahindra Ltd.

Jkumar Infra Projects Ltd

Capacite Engineering Private Limited

Uflex Ltd

Muthoot Finance Ltd.

Cromption Greaves Ltd

Paradeep Phosphastes

Torrent Pharmaceuticals Ltd.

Torrent Power Ltd.

Bharat Rasayan Ltd

Kalyan Jwellers India

Srf Ltd

Opposition party

Larsen & Toubro Ltd

Mahindra & Mahindra Ltd

Muthoot Finance Ltd

Torrent Power Limited

Ambuja Cement Ltd.

Hindustan Construction Co.Ltd.

Wockhart Ltd

Videocon Industries Ltd

HEG Ltd

Bharat Forge Limited

Crompton Greaves Ltd.

Adani Enterprises Limited

Torrent Phamaceuticals Ltd

Som Distilleries Pvt Ltd

Nesco Ltd

Zydus Candila Healthcare Ltd

Punj Lloyd Limited

Ballarpur Industries Ltd.

Gayatri Projects Ltd

Kalyani Steels Ltd;

Birla Corporation Ltd

Mahindra Life Space Developers Ltd

So it is a fairly regular practice for companies both listed and unlisted to donate, although I do not know if these donations get mentioned in the financial statements, like CSR or such related work.

And as some of ITC’s fortunes are directly tied up with policies I guess, ITC’s donations are in a way to protect its own interests. ITC donates to ruling and opposition parties, lobbies with the government, and may get something in return, perhaps not always but many times and we cannot know about this unless such lobbying gets reported in the media, or ITC itself discloses of such activity and I don’t remember this.

The donations got increased disproportionately, more than inflation, more than ITC’s stock return at 24% or so over the years, but compared to the size of the company, this is small and the donations to opposition party have been less compared to the ruling party.

So just part of the business, even in the developed countries. And if lobbying were an industry in India like in the US, ITC’s fortunes would have turned long ago.

15 Likes

ITC AGM Key Highlights: FMCG business, new launches, export potential & more

4 Likes

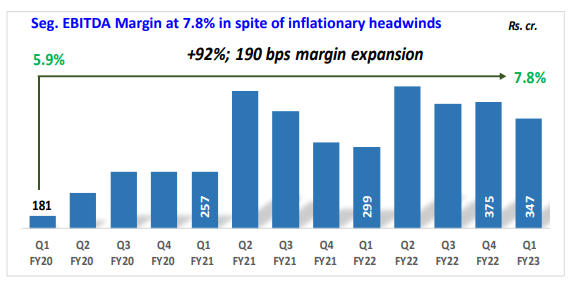

Stupendous Results from ITC for Q123, Also investor presentation here

The most sought after metric - FMCG margins ![]() . Very gradual improvement.

. Very gradual improvement.

13 Likes