So does Sunrise and Ashirwad spices :). They are small compared to existing players, but there is a large head room to grow. Sunrise had a revenue of 600 Cr end of FY21. I have no idea how much revenue Tata sampann earns.

ITC has been trashed by many analysts for doing it all themselves and not out sourcing production for better returns ( HUL for example). If one need to serve different states with milder variations, its efficient when company has its own factory and responses to micro market modifications are quicker.

Its certainly not gonna be easy for any player. In the past many MNCS tried and failed, Thats why I feel ITC will fair better as they exhibited this quality in the past. I will give you an example of atta. They have four different blend for north, east, west and south. Also consumers themselves are different. when it comes to northern India its about shifting behavioural choice of customers from non branded to branded and educating them about quality of packaged food compared to buying in loose. In southern India penetration is already higher so health benefits needs to be added/highlighted to product ( for example fiber content/multi grain). So challenges are different for different regions even for atta. When it comes to spices its gonna be even more challenging.

ITC has about 29 manufacturing locations across India, allows them to do such region specific customisation. They have built about 9 ICMLs across India that will be a game changer for FMCG business.

75 % of market right now is simple spices and about 25% is blended spices. its expected that it will be complete reveres in next 5-7 years.

I didn’t do enough research on Tata consumers, so my view may be biased. Please do due diligence.

Disclo: holding since ITC was part of HUL thread. No fresh additions in last 2 months.

Here’s why ITC is not promoting BNatural. The brand has less than 8% share.

Another brand acquired from Johnson and Johnson, shower to shower is nowhere to be seen in the ads or on the market while India is facing its harshest summers. I am seeing similar results with fabelle.

A brand loses its presence in a crowded shelf once the company stops marketing it.

Truly agree. One area ITC should focus is on to identify the growth areas, put the entire marketing engine behind that through active brand building exercise and capitalize on the existing well known brands.

Wills and Aashirvaad have a good brand following but in my opinion ITC failed to capitalize on that. Today in most shops Wheat/Atta is synonymous to Aashirvaad but they did not exploit the brand for other groceries like pulses and rice. While they have Gulab jamun, vermicelli, ghee and spices under the same brand, I don’t get to see them in prominent places in any of the store shelves.

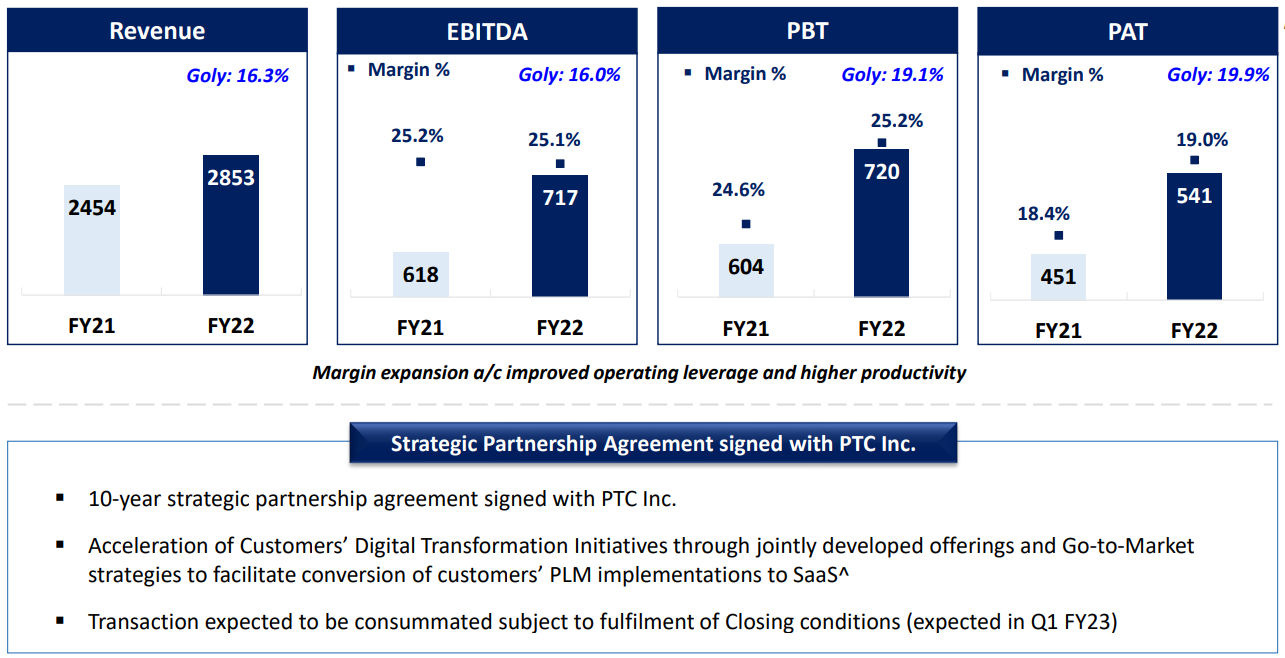

ITC has recently acquired one of the business verticals of PTC and it will be the sole provider of such services to PTC clients going forward. Interestingly LTTS who is already an established bigger player in the ERD space and was in the race lost out to ITC. We have to wait and see if ITC can being a formidable player in the ERD space like HCL, LTTS and KPIT

Sanjiv Puri, the current MD of ITC was once heading ITC Infotech

I am personally seeing their cash can actually be easily transferred to less mature businesses and can do massive acquisitions as l&t did with Mindtree that have made their overall returns to the shareholders be better over time and have made for a better case.

They have the largest cash even more the all of them that you said.

ITC is lacking in promotion and advertisement… Savlon had huge demand during covid Pandemic. They had launched few products under savlon brands and launched 1 and for each product. After few days the ads where stopped and the product started to disappear from shelves…

Shower to shower is selling in the market due to old brand name… ITC did not do anything to promote after it acquired…

I don’t understand why ITC could not spend much in TV and social media advertisement. Atleast they could re telecast the same as again and again…

ITC focus only on sunfeast, Aashirvaad, yippee and does no promote much of their below brands

Fabelle

BNatural

ITC master chef

Kitchens of India

Dermafique

Charmis

Fabelle is a good quality chocolate which they had good opportunity to rank next to Cadbury. But Amul smartly promoted their products… even Hershey’s were aggressive in last few years…

Big opportunity in India even now, if any big brand wakes up to chocolates…

Selling premium chocolates require a different skillset and thought process as compared to selling Atta…not sure if ITC is currently that flexible in thought scale and also has that kind of talent mix as it is still a very new FMCG company and conglomerate has other business responsibilities as well

…but this is a good gap to have to fill eventually…

Add candyman to it. It has lost shelf space even in big hypermarkets. I saw a few on the top most row when I wanted to try a few new things. Dominant products even the ones I haven’t heard have better shelf space.

The banned wheat variety is Durum wheat only. Others seems to be still on. Durum is used for macaroni and pasta.

And this seems to be more diplomacy oriented, where the GOI directs exports on Country to Country basis rather than individual trade between private traders, presumably to prevent price gouging down the road in their respective countries.

It sounds good on paper but the admin overhead in getting approvals may prove to be something different.

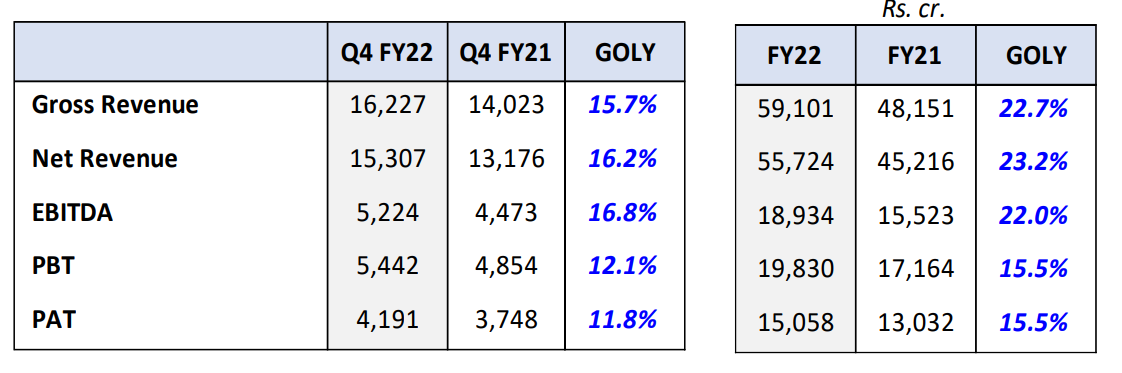

Results are out and its largely in line with expectation. See the presentation here.

Some Interesting excerpts from the presentation:

Full Year Revenue and EBITDA up 22.7% and 22.0% respectively; surpassing pre-pandemic levels - largely on account of Cigarettes volumes surpass pre-pandemic levels - Net Cash Generation from Operations stood at over Rs. 13000 crores (+32% YoY) - Note that the full year profit is still below the numbers for FY 2020.

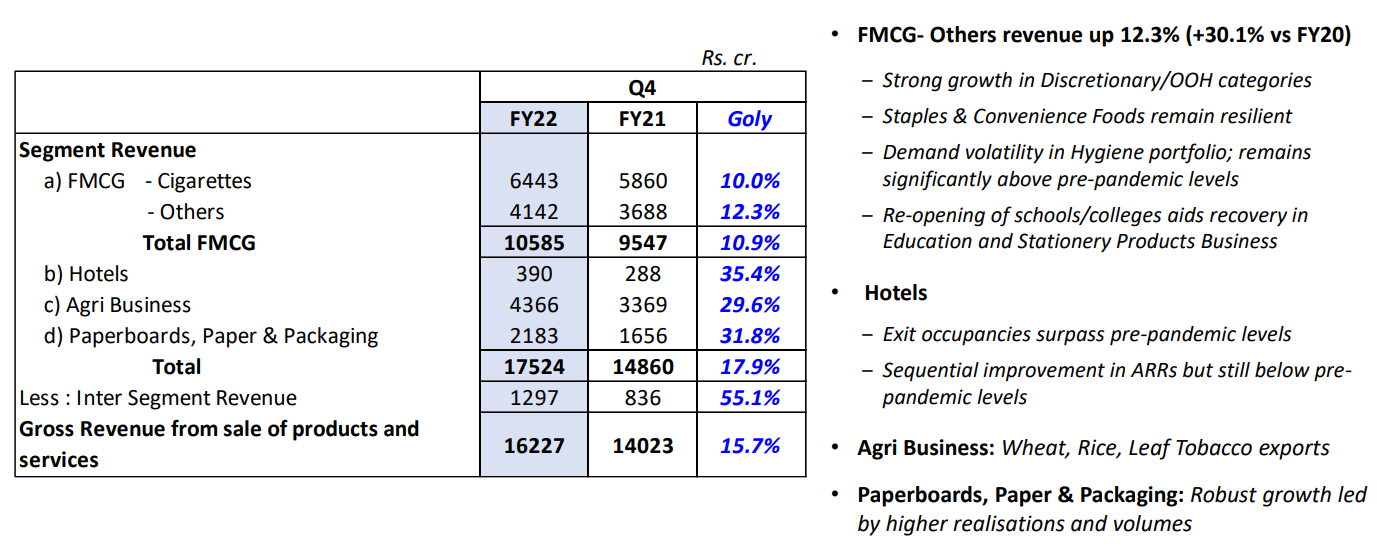

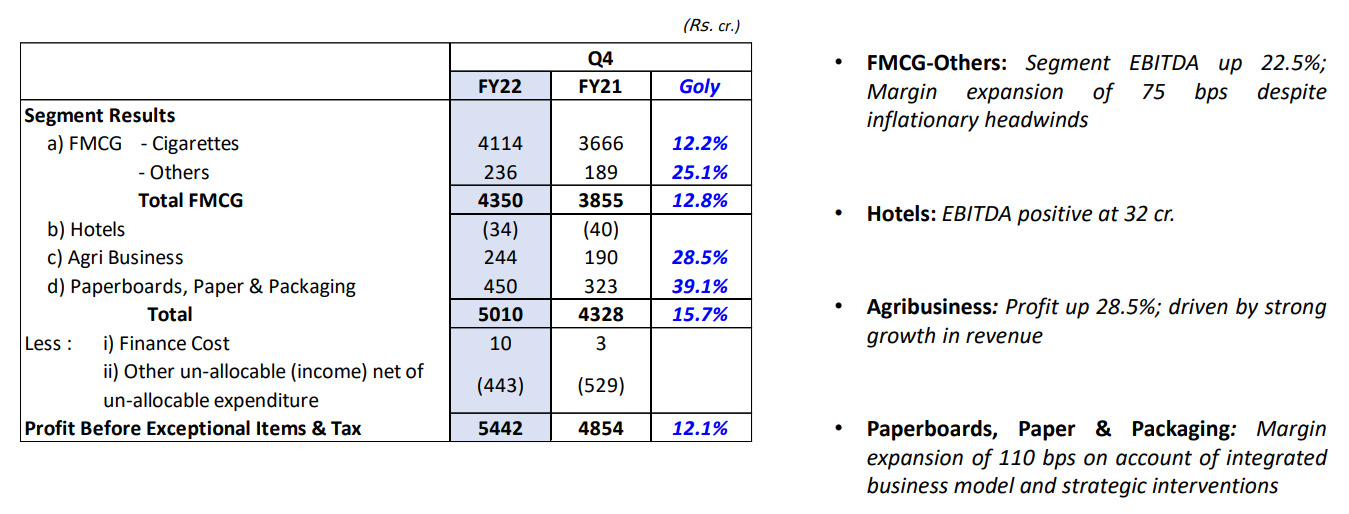

FMCG revenue +12.3% on a relatively high base (+30.1% vs. FY20); EBITDA Margins at 9% (+75 bps YoY) despite unprecedented inflationary headwinds. For the year, FMCG Revenue up 8.6% YoY on a high base (+24.5% vs. FY20) - EBITDA Margins at 9.1% despite unprecedented inflationary headwinds - 110+ innovative products launched - across hygiene, health & wellness, naturals and convenience categories.

Sharp growth in Q4 Agri Business Segment revenue; up 29.6% y-o-y driven by wheat, rice, leaf tobacco exports leveraging strong customer relationships, investments in sustainable value chains, robust sourcing network and agile execution.

Hotels witnessed smart recovery in spite of the third wave impacting recovery momentum in Jan/Feb’22; exit occupancies surpass pre-pandemic levels - Note that this business continues be loss making - expect a better Q1.

Paperboards, Paper and Packaging Segment delivers strong performance; Q4 Revenue up 31.8% y-oy along with margin expansion of 110 bps - Paperboard volumes at record high; robust growth aided by demand revival across most end-user segments; sustainable products portfolio continues to be scaled up - this is one business i believe has a potential to get listed during the next few years - very impressive product innovation helping it grow and I believe this is poised for double digit growth for the foreseeable future.

Total dividend for the year at Rs. 11.5 per share. Final Dividend of Rs. 6.25 per share announced.

‘ITC e-Store’, the Company’s exclusive Direct to Consumer (D2C) platform is now available in 15 cities and continues to receive excellent consumer response.

ITC Infotech’s performance as you can see below is not very impressive compared to other mid tier IT companies - I believe they should be a targeting a growth in excess of 20% YoY. Margins continues to be resilient and industry leading.

Background:

Main reason for market to punish and re rate ITC started happening after 2017. On July 2017 it touched 367 and in downtrend since then. ITC cigarettes volume growth has been abysmal mainly due to higher taxes. consumers shifted to illegal cigarette mainly being them so cheap.

Can ITC get back to its old growth in cigarets:

ITC management has demonstrated to Finance ministry that although they had heavily increased the taxes, it has collected lesser taxes from cigarettes than years before. Meaning illegal cigarettes market have grown multi fold and consumers also switched to that being super cheap and every one ITC + government has lost revenue.

In the recent years finance ministry seems to understood this and didn’t increase the taxes on cigarettes. And that lead to increase in volume for ITC ( of course covid re opening also played a role, no doubt). So ITC could very well get its volume growth back. ( Note: here this doesn’t mean there will be new smokers, this simply means shift towards legal cigarettes from illegal ones ).

Since ITC has improved margins, any additional revenue on cigarettes will bulk up the bottom line. OPM for cigrattes are about 60 % now.

Opportunity size:

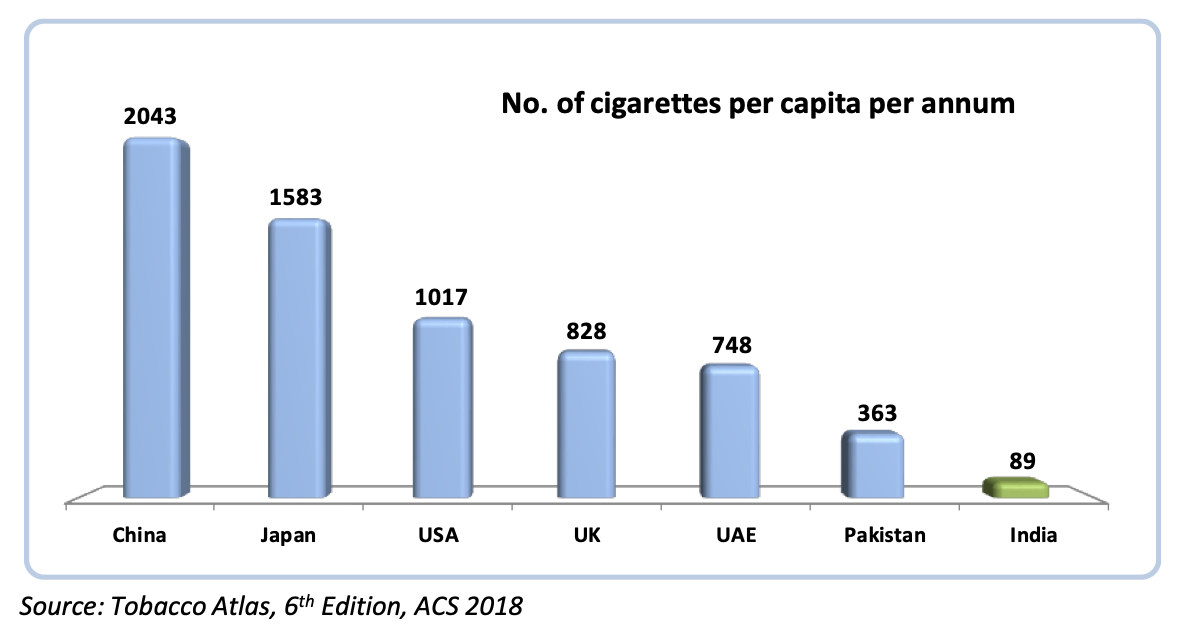

Cigarette consumption is not high compared to other countries

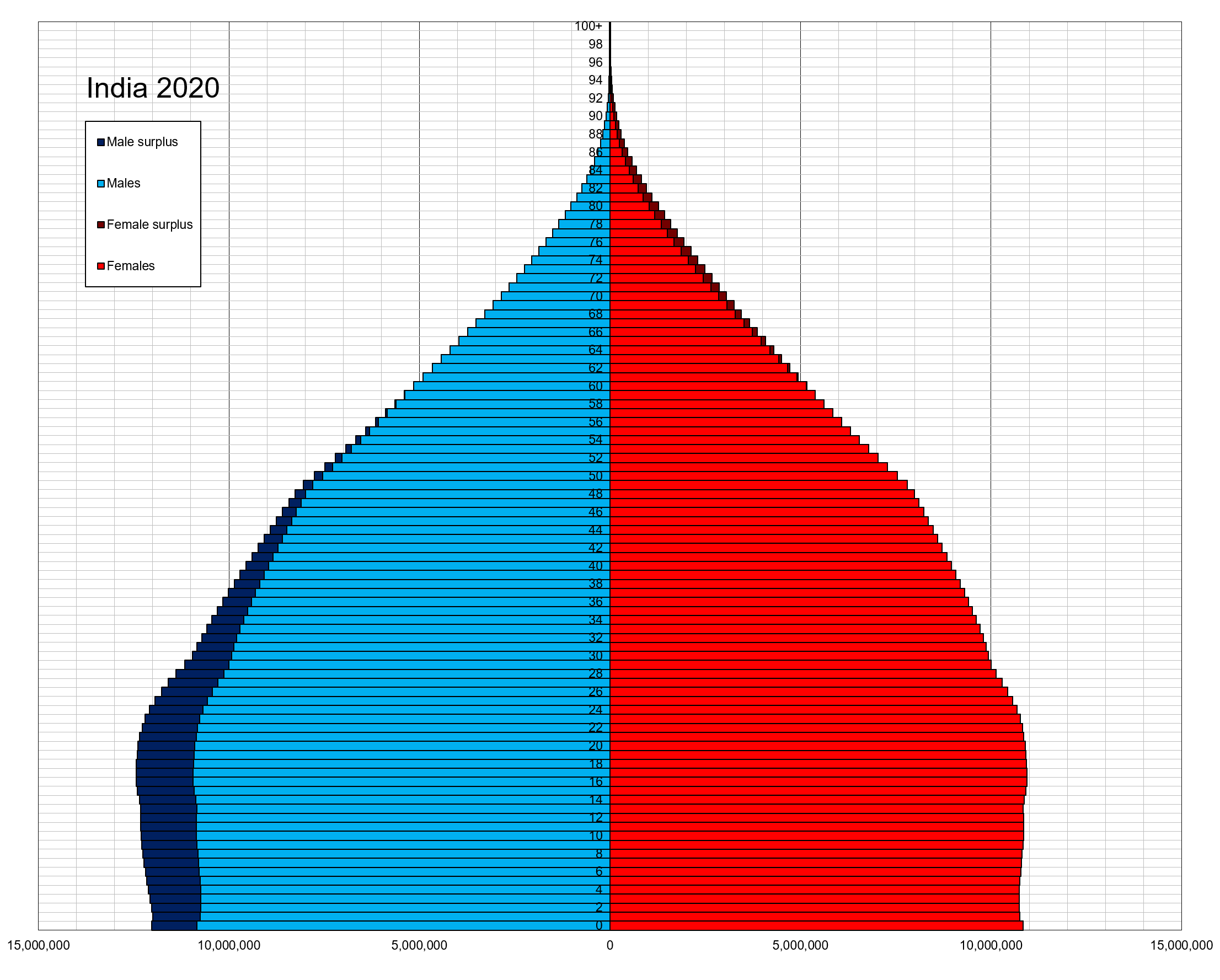

We have one of the youngest population in the world ( Im not batting for youth to smoke more, but many young persons smokes during college days and leave it after that ( me being one example of that)). Indian demography is such that peak population is around 16-18.

So there is enough head room to maintain the revenues.

ITC plan for Future:

ITC is always looking forward in its prospects adopting Industry 4 as well as sustainability. ITC realised that other forms of nicotine consumption are on the rise that could act as a replacement to smoking. To capture the growing demand for oral and vaping products in the US and EU markets ITC has setup ( in the process of building ) a nicotine production plant in Mysore using a new subsidiary “indi vision” in Mysuru. This is expected to put ITC as one of the manufacturers of purest nicotine in the world (stringent US and EU pharmacopoeia standards for use in pharmaceutical products). This plant will produce nicotine and nicotine salts mainly for the purpose of exporting to US and Europe markets. Hence it will also bring lots of dollar revenue.

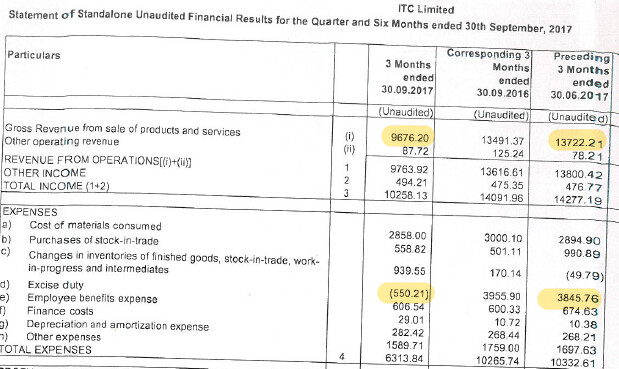

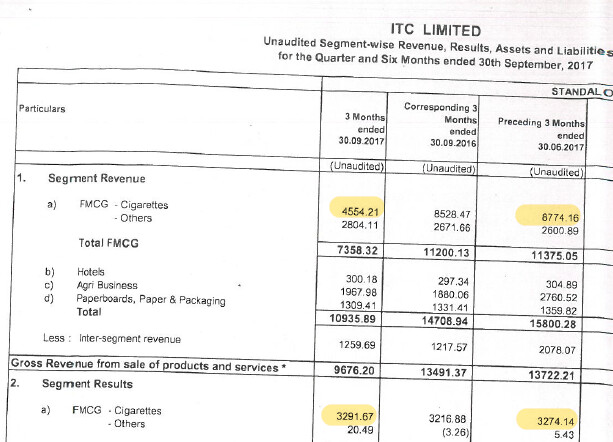

Thanks for sharing your detail working. However, the decline in Cigarette revenue in FY18 in value terms has more to do with GST (excise continue to be imposed but was lower amount as compared with previous year.)

Find enlcosed screen shot of September 2017 results (standalone, first quarter from which GST implemented) We can see material decline in Revenue as well as excise duty number in September 2017, Sep 2016 and June 2016 number. So, in my limited understanding, this has more to do with accounting adjustment then only pure decline. There could be decline in sales but not as material and high as indicated by the sale figures, in my limited understanding.

As compared with June 2017 quarter, Cigarette sale in Sep 2017 declined by Rs 4200 Cr, but EBIT was almost same level. So decline in sales was more to due change in GST which needed Sales amount to be net of all taxes. Since VAT, Cess and Other levies, where accounting for very large portion of sales revenues, same were netted during September quarters from sales figures. There was virtaully no impact on EBIT despite almost 50% drop in revenue . In my limited undestanding, that was reason for major in Cigarette revenue ,almost 50% drop in Revenue over quarter.

Thanks for your efforts in putting acorss your view point.

Discl: My highest holding, No investment in last 6 months. My view may be biased. Not recommeding any investment action. Not SEBI registered analyst

I see this company fit perfectly with ITC. Firstly. It helps in ESG scores. Secondly the paper, mosquito repellants and tobacco compost can be part of ITC paper, ITC fmcg and ITC agri businesses. Soft toys and pillows can be used to donate to the underprivileged kids. Such efforts re what a democracy like India needs.

Read this article and I remember there were discussions earlier in this thread that vaping could gradually be the next growth driver for tobacco companies abroad in markets where it is allowed. Also, if I am not wrong, ITC was working on exporting ingredients to such players…

This articles looks contradictory to above as vaping looks like an even more faster dying industry abroad as regulators are removing products, which they have not done for even cigarette also?

Anyone with insights can provide more details - Is vaping really a future industry or dying industry?

Why regulators are more strict on vaping as compared to cigarettes abroad?

Looking at above article, it seems India’s decision to not allow vaping has been more mature? Any insights? Thanks