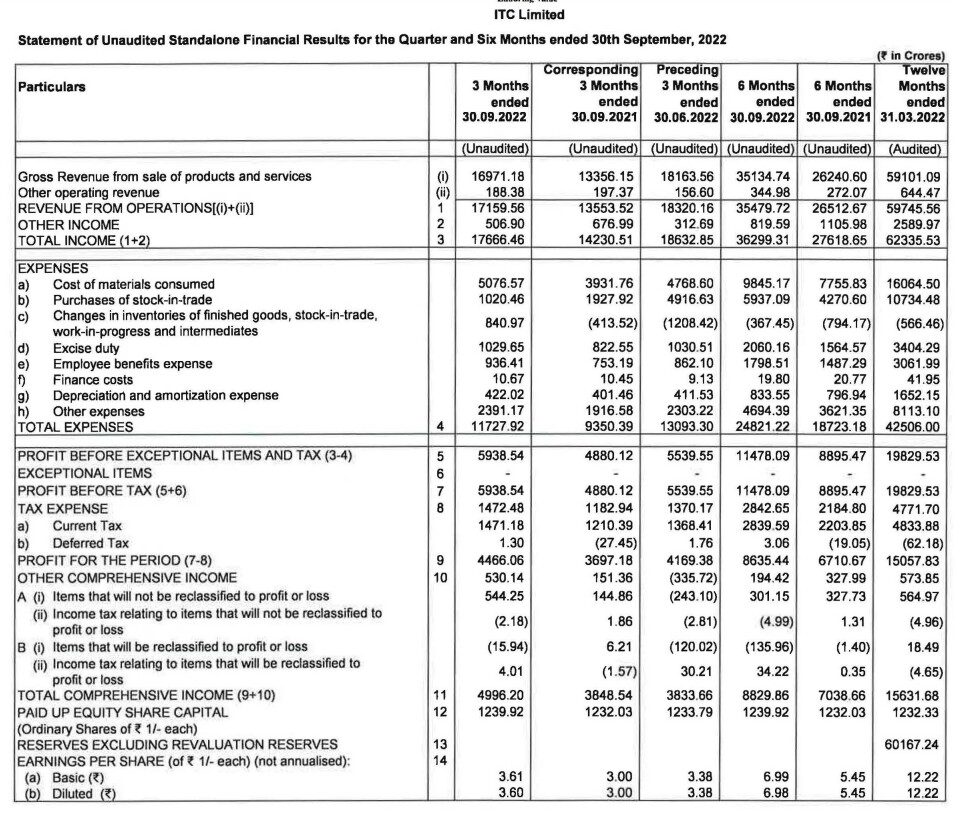

Indeed good quarter for ITC. However FMCG other margin has shrunk to 7.8%, I think it was around 9% in previous quarter and 8% previous year. But still good one considering high inflationary environment. Let’s see how next coming quarters unfold in terms of FMCG other margin.

Revenue from agri beat revenue from cigarette in the current qtr.

Net profit from paper is now much higher than agri and FMCG.

FMCG others business is lagging on every parameter. Requires hardwork and concentrated effort. FMCG results have been disappointing.

Hotels have had a good turnaround. Sentiments will change if the profitability rises.

Itc infotech results are in-line with other it cos. The management is looking to divest but I am of the opinion as a shareholder that the divestment should not happen unless ITC Infotech is beating LTI, LTTS, Mphasis and Mindtree on most parameters.

ITC’s strategy of backward integration has served them well over time and company is doubling down on it through expansion in their MAARs network.

ITC plans to spend 3000 cr. on capex annually with 70% going towards FMCG.

There might be hit in topline in the future as some topline growth recently has come from large trading opportunities in agri commodities segment which come at very low margins

FMCG strategy is to create mega brands and once done, expand through offerings in adjacencies

Currently have 6 mega brands (1000 cr.+ annual sales) and hoping to add a couple more brands in this club

Currently in discussion with another D2C brand in mother and child space

With more stable tax regime on cigarattes in the recent past, should be able to claw back some market share from unorganized players

Disclosure: Invested (position size here, sold shares in last-30 days)

Itc launches Candyman xl chocolate. The pricing and packaging seem to be in direct competition to Cadburys dairymilk. I have seen a lot of dairymilk chocolates being sold at Pan Parlours/ smoking shops. Makes for a good opportunity to exploit cigarette distribution to increase sales for Fantastik XL range.

Commercial for Candyman

Paves way for Fabelle to fight with premium sweets and chocolates.

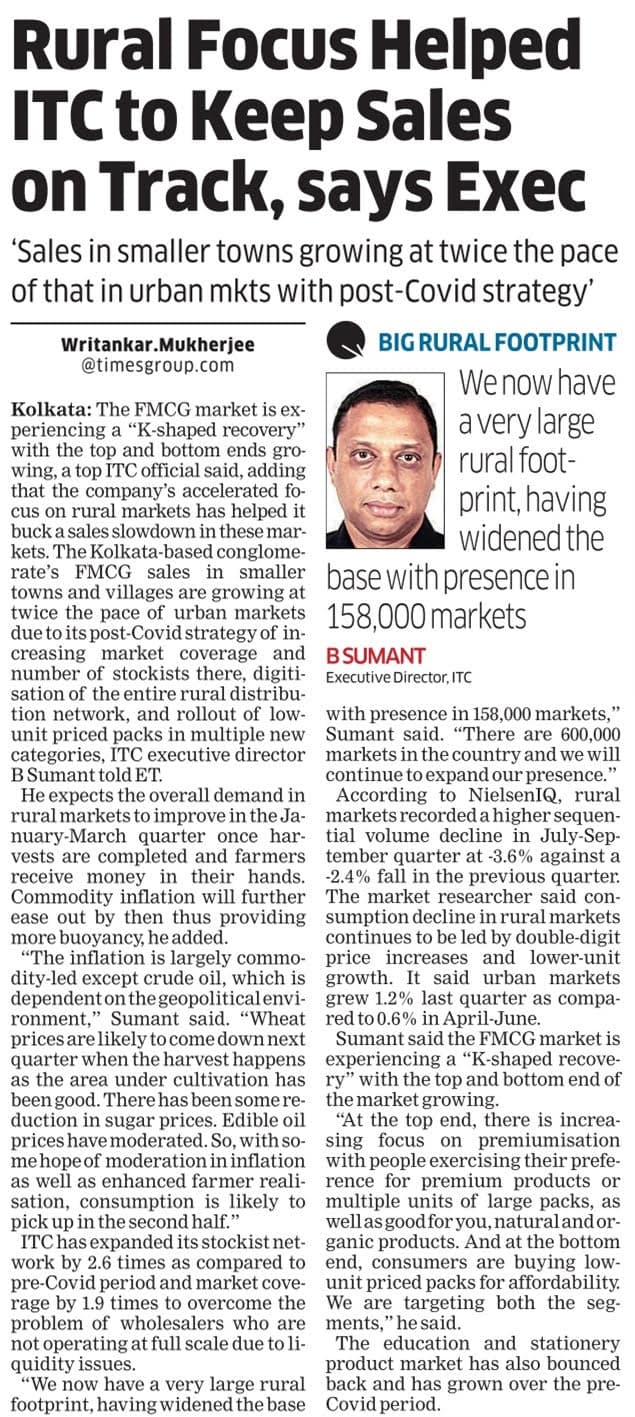

Interesting news appear in ET about rural focus of ITC FMCG business. I see this as the most critical variable beside Cigarette tax for long term wealth creation of ITC.

ITC seems to be doubling its efforts in the hotels segment rather than bowing to a segment of investors who wanted to demerge hotels business. Although, their strategy to go asset light seems to be paying off.

ITC currently seems to be the second largest Hotel brand in India after Indian hotels (Tata).

I think I did read about their interest in hotels in this thread itself. Perhaps it is true that no matter what, they will not leave this segment, even if it were to bring some losses. And I guess right now, there will not be any backlash considering the CMP. Investors are happy.

Also, even if the management’s actions are seen unfavorable regarding hotels segment, if other segments are growing, and if that growth is reflected in the price, and along with the almost given dividend yield, I guess everything will be fine.

ITC focuses on sustainable food safe spices. The new factory that was inaugurated recently is a fully backward integrated factory covering from seed to product. Its important to note that ITC is working with the farmers around this region for many years.

About ITC Global Spices processing Unit Spices : Chilli, Turmeric, Blended organic spices Area : 6 Acres Capacity : 20,000 Tonne per annum ( phase I ) production lines : 4 lines ( Tropical spices, seed spices, High VO spices and sterilised products ) certification: BRC, FDA FSMA, FSSC 22000, USFDA Organics, NPOP

When the Phase II is completed it would be 38,000 Tonnes. They are also working on spices competitiveness with farmers using agri full stack application ITC MAARS. WIth such a scale and automation I expect them to be efficient and may bring costs down compared to competitors. There is also a huge scope of export markets.

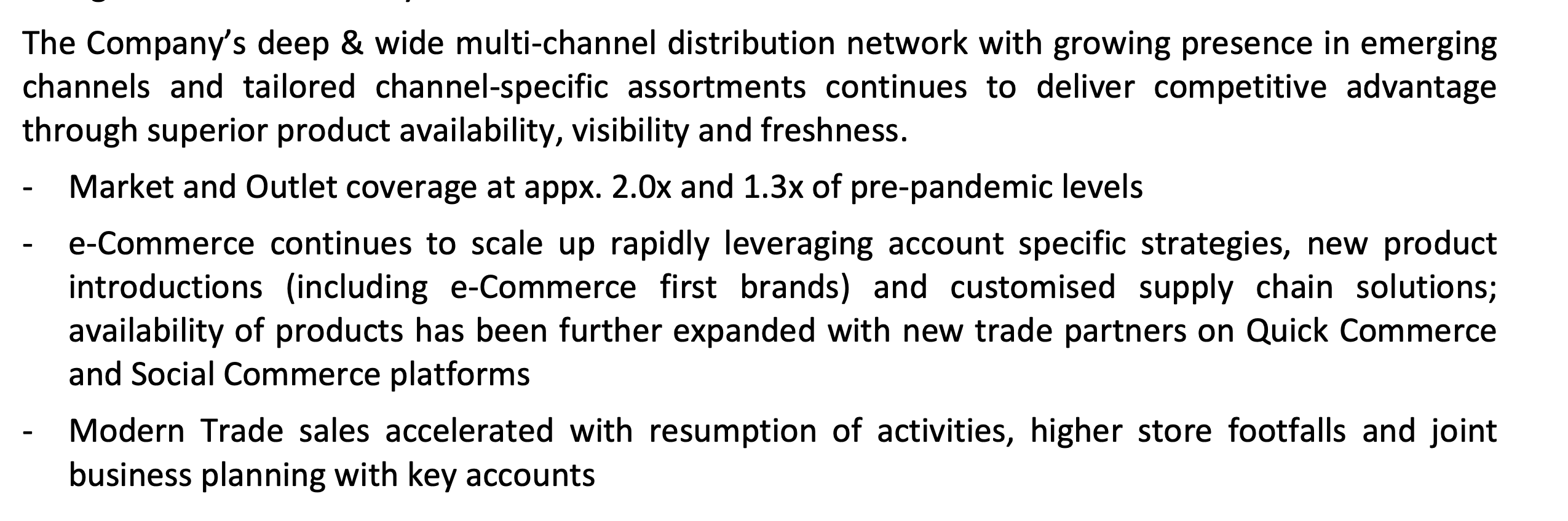

ITC distribution Network :

I did and scuttlebutt and wrote about increased rack space for ITC products in tier-2, tier-3 cities. Covered here.

with recent article saying that ITC is focussing on the Rural areas, our conviction on improved distribution is validated.

In the last quarter report company has claimed that ‘Fiama’ and ‘Vivel’ has got a good traction.

One of my good friend who works in FMCG says distribution is the King when it comes to selling FMCG. ITC seems to be more aggressive in distribution compared to earlier. They always had good connections due to their cigarette business. But with FMCG they are now more and more visible and gaining shelf space in markets.

This is from the tier-3 rural side. I was quite happy to see Fiama/Vivel got almost same shelf space as Pears.

Overall happy with aggressive efforts and pushing more distribution to reach end retail stores. My observations are mostly from southern part of India. Conclusions may vary depending on your location. So please take my observations with a pinch of salt.

PS:

This is not an investment advice. Holding same as of last post. No transactions last 30 days.

ITC had invested Invested 20cr for a 16% stake in Mother Sparsh in 2021. The revenue was15.57crores.They targeted to hit 40cr in 2022 but did 33.53cr when ITC invested another 6% for 13.5 crores.

ITC also invested 39.37cr for 10% in MYLO (Bluepin technologies). MYLO clocked a revenue of 1.39cr in 2021. Its 2022 revenue is not available online.

Now, ITC has invested 175cr for 39.4% in Yogabar with MOU to invest more. Yogabar did revenue of 68cr in 2022.

None of these new age brands are on sale at ITC store and neither is Mother Sparsh on MYLO. This is not surprising since ITC has not been able to utilize its cigarette network to push sunfeast biscuits and Bingo chips, a space completely taken over by Balaji and Britannia/ Parle. Cross Selling is one of the biggest boons in FMCG business.

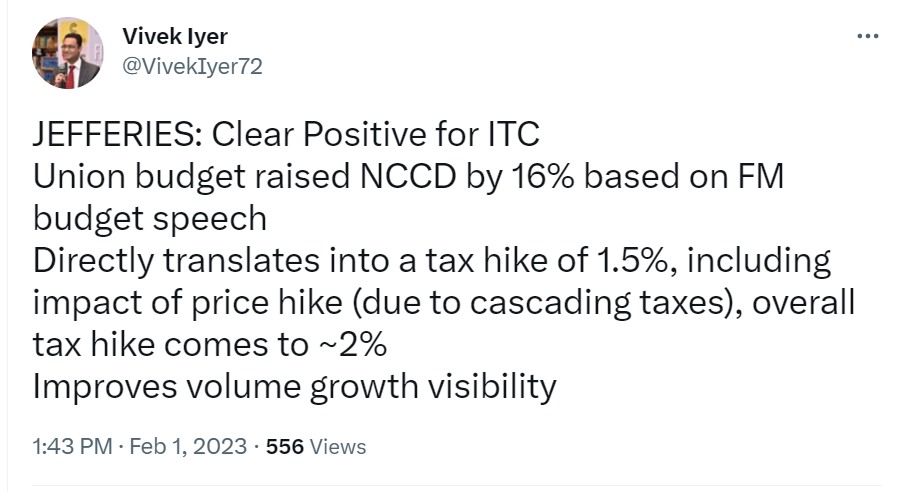

The 2% tax hike shall be passes on to consumer, that is positive bcoz the price hike of cigarette shall directly increase in revenue by 2% without volume growth. And the volume growth shall be additional.

A fellow member sought my view on ITC on personal message. The query was as under

"I wanted to ask you about ITC. I feel most of the concerns that were raised when it was getting lower valuation are still there (too much diversification, non availability of products, investment in hotels). Just that price has hidden all problems. Still 80% profit is cigarettes and that doesn’t seem likely to change in near future. Also, Reliance’s planned foray into FMCG is likely to affect most ITC FMCG products which already sell at a discount to market leaders (except Aashirwaad atta).

Wanted to know your thoughts."

In my view, neither decline nor increase in price is reflecting fundametal change in business. There was some ECG concerns and also immediate negative due to COVID which resulted in decline in price. Now, from Agri to Paper to Hotel business, outlook is favourable and price were relatively low which again driving interest in ITC. Having said that, if tomorrow, say for instnace, SUUTI decide to sale ITC stake, price may again see volatility.

I would consider following points in my decision to be invested in ITC

Dividend distribution and growth. The management promosed 70-80% dividend payout 3 years back and they are walking to talk. In addition, while they have done some small expansion and required capex, broadly capital allocation is reasonable in my view. Hence, I am not concerned on that front.

Business prospect: While we may have different opinion, One thing ITC management has ensured is maintianing quality of whatever business they are present at probably highest level. It is very difficult to differentiate quality in Chips and other eatable products, but they are consistent. Also, quality of Wills Lifestyle shirts and Fiama soap, of which I am personal consumer, was excellent in my subjective assessment. This is my personal view and may not be factually correct. However, while business is competitive, the management has ensured till now one important point, providing good quality stuff to consumer (at least in FMCG business), even if it may not result in superior profitability. It might not be great in short to medium term, but in long term, in my view, that shall help. It is not simple in Indian market, to scale business from nil to Rs 16,000 Cr business in 20 years (adding Rs 3,800 Cr FMCG sales only in FY22).

On competition from Reliance and other Players, I feel the Indian market is like sea and growth is also expected to be in line in GDP. Further, there is scope from premiumisation with increase in per capita income. One can refer to Mr Mehta, CEO of HUL again and again talking same point in HUL con call. Hence, I do not see that market becoming saturated. However, whether ITC gain from it or no, only time will tell. Till now, ITC has gained market share (as moved from nil to positive value). Hence, do not see any specific reasons why it cam continue to do so.

Profit being generated mainly from Cigarette

The concerned raised is valid. However, I would not see revolutionary change in FMCG profit share going up. It would be slow and steady improvement. We under estimate benefit of operating leverage in a business of FMCG. With more than 6 mn unit outlet reach, ITC has achieved major milestone in my view. Also, as compared with other peers, ITC share in backward integration is relatively higher. That can result in lower financial ratios,but at core, would improve sustainability of business. Classic example being using production facility of Engage perfume to manfuacture Salvon spray during Covid period.

So, I would continue to hold ITC in my investment at current valuation. Will look at today results but would not be resulting in major change in my thought process.

As ITC approaches life high, I would also like to share various memes on Social media on stable price of ITC shares. Just for bringing smiles to readers face and realise how sentiment changes by 360 degree within months.

Disclosure: ITC is my highest equity holding. My view may be biased. Not a SEBI registered advisor. Not suggesting any investment action to the reader, No trade in last 3 months.