Dear @kb_snn

What could be the possible reasons for decrease in fmcg others ebit.

Thanks

Dear @kb_snn

What could be the possible reasons for decrease in fmcg others ebit.

Thanks

Raw material inflation : Palm oil prices is main culprit …

Most FMCG players have gone behind volumes in last quarter and hence price hikes has been lesser than desired level … So competition is second main reason

Third is Product Mix issues …

Fourth is S&GA would have risen as people started to move around which was restricted in first half

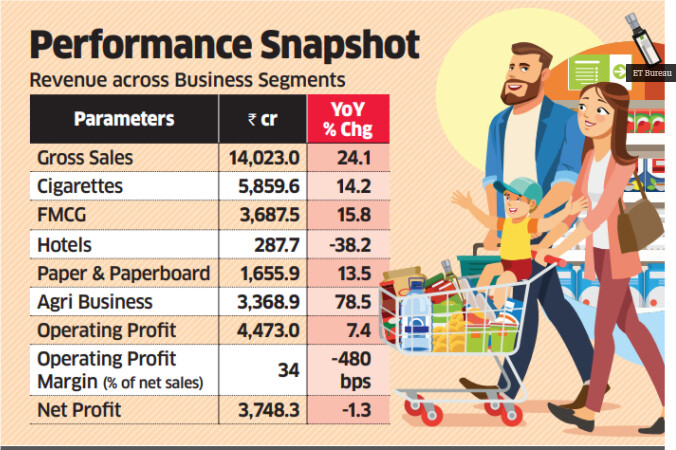

With an overall modest Q4 performance, the ITC stock that had gained nearly 9% through last month is likely to be under pressure in the near term. Pandemic-induced lockdowns during the current quarter — even if regional — hurt several key segments of the company: Cigarettes, stationery and hotels. In such a scenario, if FMCG and agribusinesses don’t perform strongly, the overall growth would suffer.

With an overall modest Q4 performance, the ITC stock that had gained nearly 9% through last month is likely to be under pressure in the near term. Pandemic-induced lockdowns during the current quarter — even if regional — hurt several key segments of the company: Cigarettes, stationery and hotels. In such a scenario, if FMCG and agribusinesses don’t perform strongly, the overall growth would suffer.

ITC is one of the rare blue-chip stocks that is still trading at its 2013 price levels — even as the benchmark indices are scaling new highs. The scale and potential of each of the company’s businesses segments are keeping investors invested in the stock. The possibility of a demerger of any of the segments could be a growth trigger ITC share price: ITC can be more than a puff of hope if FMCG, agri light up - The Economic Times (indiatimes.com)

Great Twitter thread by Dinesh Sairam & Prof Sanjay Bakshi on ITC & Demerger.

I follow them & value their insights, so thought of sharing here.

(Pls flag if you feel this is not appropriate.)

Disc : Invested.

Thank you for sharing. Always learn something new from Prof. Bakshi.

The circumstance in India seems to be different. There are no class action cases or such against tobacco companies. I haven’t been able to find anything as such. Most of the cases are around the warning signs than anything else. There have been calls for action against tobacco companies, even from academic circles (legal, etc.), but I don’t think there is anything. A good summary of legal issues till 2017. ITC’s AR also has company specific issues also mentioned.

Does anyone know anything about legal aspect of tobacco in India?

Cigarettes and Other Tobacco Products (Prohibition of Advertisement and Regulation of Trade and Commerce, Production, Supply and Distribution) (Amendment) [Bill 2020]

Central government drafts law to raise legal age of smoking to 21 years.

These r the two recent laws related to tobacco

Parle is foraying into the Indian packaged atta market. Aashirwad has another competitor now.

I have seen Parle’s atta on shelves in Kuwait. It will be interesting to see how ITC addresses this market. On one hand they are pushing into premium value added products like multigrain, millets, pulses etc. Now Parle’s entry will force them to focus on mass market products as well. One thing I am not sure about is how their teams are structured - do they have enough focus on all the segments they compete in?

Disclosure: Invested, largest holding.

Adani is already in the market with Fortune, we have other large players including Pillsbury and inhouse brands from large players including Aditya Birla, Spar, Reliance(not sure about this one) and umpteen number of regional players. Atta is a staple and we have more than enough space for all of the players to grow.

On a lighter note, why will Parle invest into a crowded market if they do not see adequate long term returns.

Aashirwad is the undisputed leader in this space and they have gained this position not via mere luck. The product quality along with the right customer mining is the trick. For a good number of households I know, atta means Aashirwad and that makes all the difference.

AJ

Disclosure: Invested

Invested.

Parle already has procurement infrastructure in place as RM for their biscuits, and a ready distribution channel (even 1/4th of outlets selling their biscuits translates to > 20 lakh points of sale). This sort of adjacent diversification is relatively easy (vis-a-vis going into a different segment with different supply chains).

On the market size I agree with you sir, my observation is that of late ITC has been on a premium drive (perhaps seeding & testing these products on online market places). Whether they are doing this with sufficient focus on each segment is my doubt. To understand this, a reasonably deep picture of the org structure will be helpful.

Wheat flour ( all derived flours ) market is estimated at > 2 lac crore

Out of which organised players ( national players, with a market leaders like Aashirvaad, Pillsbury, Nature Fresh, Annapurna, Shakti Bhog, Patanjali, Fortune etc. and more than 500 regional brands and private label brands together forming the organized market ) is just 20000 crores ie just 10% of total market .

Thus there is already a very big existing market … It is just not organised … But is tough business esp when you don’t have scale …

Buying scale / warehousing / logistics / export optionality/ derivative product optionality / innovative disease management etc are critical to maintain margins as Raw material cost is big part of overall selling price unlike personal care products where packaging & branding cost can as high as RM cost

A lot of talk has been going on the ITC counter on various threads, blogs, videos and tv. Some include FMCG growth, overall underperformance or Demerger. Here is my take on it.

The demerger will not happen. A demerger will mean higher tax rates and channeling of funds from the Cigarette business to other businesses. Will British American Tobacco as the controller of ITC’s cigarette business want to pay more taxes, cess and levies and fund other businesses? Again, are the other businesses really that strong to survive by self? The pandemic has shown the effects it has on businesses such as Hospitality and stationary. Even the FMCG business is not exactly having a stellar performance. Secondly, the share capital of ITC is already huge. A demerger will be tough to manage.

So why not buyback shares rather than pay dividends? Yes, buybacks are also being discussed on several channels and blogs. ITC’s control is basically a tussle between Government through LIC, GIC, New India and Oriental and British American Tobacco through Rothmans, Myddleton and tobacco manufacturers India. A buyback will mean that BAT’s stake will increase overall and that is not in the interests of the Govt of India which is currently desperate to divest from most businesses. This will have repercussions in the future but for now, no buybacks.

Why is ITC still running hotels? It is a capital intensive business and not generating enough returns. Why is still functioning? firstly, Hotels are a small part of ITC business. Those making big noise about it know this too. ITC"s management has diverted their strategy to being asset light. One should give them time to work on profits from this sector. Secondly, selling the hotels business post the pandemic is not the best option. Rather let the management work it out. Hotels can be a profitable business as displayed by Sinclairs and Advani hotels. One should not just shut down businesses if they are making lesser profits than other businesses unless the underperformance has been constant without any further efforts possible. This is my viewpoint and I totally respect if you think otherwise.

ITC is now an FMCG company and should be rated as one, do you agree? No, even as per the latest Q4 2021 results, EITDA from Cigarettes was 12720Cr vs. 833Cr from FMCG, 821Cr from Agri and 1099cr from paper and boards.

Also, while many of its brands are performance superbly, most of its other brands are failing big time.

ITC had launched FIama di wills and vivel Shampoos a decade ago but failed.

ITC’s products such as ultra mintz, gumon minto and candyman are not available anywhere I checked (including online and offline.)

It is peak summer and ITC’s Shower to Shower talc powder are not available online on most stores.

ITC superia gangajal has not been accepted by consumers and is out of the market. Soaps and shampoos are not available online of offline.

Fiama di wills soaps and bodywash have a good brand recall but ITC chose to expand the portfolio with handwash products rather than shampoos and conditioners.

There is not much info on Dermafique and the brand also lacks marketing and availability. Others can provide feedback on this.

Essenza di wills is a washout. They are not available at most perfume stores (including ones at the airport even before the pandemic) and they lack any brand recall.

Fabelle chocolates have been launched. The excitement of trying a new chocolate doesn’t exist as most consumers (except ITC shareholders) do not know it exists.

Bnatural juices were last covered in the news in 2018. The recent investor presentations have chosen not to divulge market share of the juices vis a vis Real and Tropicana.

Additionally, There have been a lot of attention given to ITC"s strength at distribution but the FMCG business has not really seen a positive impact of this. most cigarette shops have Balaji (excellent distribution), dairy milk chocolates and other confectionary but not ITC products. I literally tries various shops for Fabelle chocolates, BNatural juices, ITC confectionary, Shower to shower and other products but to no avail. Most stores (10-15 shops) only had Sunfeast biscuits, Yippee noodles, engage deo, fiama di wills and Aashirvad aata. Even mainstream products such as Savlon and Vivel were not available. I will consider this as a huge drawback as it is not only the situation in one city as mentioned by many. How does one view the non-availability of majority of products in a major city for such a prominent corporation?

Also, there are glaring gaps in its FMCG portfolio. ITC does not have many high margin essentials like Shampoo and conditioners, toothpastes, Detergents, Shaving products, malt drink powders. The reason I am pointing this out is because there was recently an article on how ITC should monetize its estore. ITC e-store can help push entire range of FMCG products: report

Sadly, the store has been accessible from before the pandemic times but it is not accessible anywhere except the major metros. (I tried pin codes for Ahmedabad and some tier 2 cities.)

At a time when Reliance is pushing Jiomart and Tata is pushing big basket, ITC e-store can be a gamechanger. how should we react to the non availability of ITC products pan India?

So, while there is noise on the hotels business, why have investors chosen to stay quiet on the underperformance and weaknesses of the FMCG division when ITC has been pushing so much resources on this business?

This article is critical of the ITC’s many businesses but I am positive on the long term outlook and hope that my opinion (if correct) reaches the management and they make immidiate course correction.

PS: This post is based on my research and understanding. Your opinions can differ and I would love for others to share theirs so we all can learn.

Disc’: Invested with a positive outlook.

The above findings of @devarshi84 was more or less covered all the products, so if communicated there may be a response.

I did not find anything except for Savlon hand wash which I found to be less foamy compared to Dettol hand wash. I have to use it again to confirm.

Individual experiences and perceptions if alike will culminate into collective decisions and will reflect sales, so at least that will indicate something.

I request you to please forward this to the management and also try on Twitter. Also want to ask experienced members if they think investor activism has scope in India. ITC seems to be a very fit case for investor activism and I’d like to believe that enough people voicing their concerns can make the management take notice.

On a lighter note, if ITC doesn’t work out, I’m done with “Value investing”

Being a hotelier myself, I find it a welcome move by Welcomhotel, specially running the property on management contract.

Even this is a intrsting move by ITC Infotech :

Disc : Invested

Not sure how long you have been holding ITC. True value investor would hold it till value is unlocked or forever. There isn’t any problem with ITC business as such. Govt is putting more and more taxes on cigarettes which is impacting their growth but they are still growing at 8% which is decent for big organization like ITC. I am buying ITC and would wait till they grow FMCG others as much as other pure FMCG players (Current margin is 8.5% and growing QoQ) and agri business.

They are paying 5.2% dividend which is better than FD rates what is the problem? ITC was never supposed to be a multi bagger. I will simply forget about this investment as some sort of FD. If they could increase their FMCG other margins to 15% then multiple expansion would come into play. It is just a wait game you have to play.

These are things people say to console themselves. Last 5 years returns are -13% according to google. If we add dividends, it may be flat. So it has actually performed worse than even FD. Nifty is up almost 100% in last 5 years. Assuming Nifty doubles again in 5-7 years, ITC will need to do exceptionally well to even beat or match index returns. What’s the point of buying individual stocks if you don’t even get index returns?

Alright so you buy a large cap stock which was trading at 35 PE (For 8% Growth) and call it value investing? You buy quality stock with potential to generate enough FCF to support future growth, Dividends and buyback at cheapest possible multiples (I am buying at 14X times FY23 earnings) so that your downside is limited.

I am buying ITC because of below reasons:

I am moving my debt portfolio to ITC so that it earns exact same returns (In the form of dividends) for little more risk with potential upside in case any one of the scenario plays out. I am confident that management can generate 8% FCF growth to support dividends.

I believe as we move forward returns from bonds continue to decline so it makes no sense for me to hold any bonds(They are turning out to be risky anyway with all the defaults).

| dividend | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

|---|---|---|---|---|---|---|---|---|---|---|

| 10.30 | 10.82 | 11.00 | 12.00 | 12.60 | 13.23 | 13.89 | 14.59 | 15.32 | 16.08 | 16.89 |

I have taken analysts estimates for dividend up to 2023 and there after calculated with modest 5% increase and it turns out to be that we get around 17 rs as dividend in 2030 which turns out to be 8.5% yield at the current share price which i assume should be more than bond returns as we move forward.

If company can unlock value in the form of demerger then you hit jackpot or let’s say margins of FMCG others continue to grow then also you hit jackpot.

I am buying just 25% at the moment and let’s see if all this noise of Inflation and interest rate hike plays out so that i will move all my debt investments to ITC. It is definitely cheap at current valuations but economic conditions are changing so i don’t see much upside in stocks in general in coming months so will wait bit more so that i can acquire shares at cheap price so that yield can be optimized

Hey, Understand but i am still very young so i really don’t want to park my money in debt funds but the same time don’t want to put my money in high risk crazily valued growth stocks (My risk specific portfolio is in growth stocks already) so i perceive ITC to be low risk stable dividend stock which can give spectacular returns if any of the above scenarios plays out otherwise i am very happy to get just the dividend.

Some of the risks i do foresee is -

So essentially I want all my money (Except Emergency funds) in stock market and I put my equity portion into more risky stocks while debt portion into least risky stocks. I believe ITC with all the cash and business which is still generating enough cash with favorable valuation is least risky for me but having said that I am just putting only 25% of money because of all the talk of Inflation and Interest rate hikes I do believe stock market may go nowhere hence i assume ITC might be available for cheaper price down the line. If it ever comes to price where i perceive downside risk is negligible and div yield is like 8% of FY23 then i will move rest of the money.

Thanks for the suggestion

ITC_Nov2020.pdf (3.0 MB)