I think most market participants agree that it is a question of when and not if that ITC will be split.

Ashirvaad atta has a few value added variants like multigrain and multimillet and they regularly feature among best sellers on amazon. Also, other than fortune, there’s no nationally recognized brand in atta and therefore I do not believe this commonly held belief that atta is low margin business. It could be low margin in general, but I don’t think it is or will remain for long for ITC.

Digestive and 5 Seed Digestive look alike, also because of the shape of the pack along with the colors. While 5 Grain Digestive and Veda Digestive are of different shapes, so a consumer will not get confused as human brain will not just see the colors but also the shapes. Nevertheless 5 Seed Digestive should have been different, this is wrong on ITC’s part. The department which takes care of these things should have done their research as to know if anyone has already done a similar one before or this could be deliberate and if it is, it is pathetic. I remember seeing similar copycat packing with some other FMCG companies, it was oil or something.

It is understandable if a small company does this gimmick, but reflects poorly on ITC, judgement in favor or not.

I understand that these are not great tactics but they very much work in the marketplace.

Also I don’t think this matters overall to the ITC investment case. I think we all know they don’t have a great FMCG division, they are trying to be one. Just have to wait and watch.

What is surprising to me is how ITC has such poor packaging. Anyone know what this is all about? They can’t be trying to save money on the packaging surely?

Is it? I am not aware of that. If this is standard industry practice why did Britannia went to court? Standard industry practice or not, this certainly is cheap. I don’t consider this as good marketing. As even bad publicity is publicity, these gimmicks may make the products get noticed and will reflect in sales. Gain in quantity, maybe yes, quality in practice, no.

They spend 1000 crores for A&P, might as well spend a few more crores and come up with differentiating packaging like Yippie.

Most product packaging in CPG is all about the positioning. If you look at Dark Fantasy, it is all brown/purple/red to showcase richness and relative premium positioning. When it comes to the other mass market brands like marie, nice, etc, there is already a deep impression in a consumer’s mind - they look at the colour and pick it up. So new brands need to either stick close to the market leader’s packaging or do something drastically different. ITC sadly chose the easier option.

Source: Market Research done as part of course work.

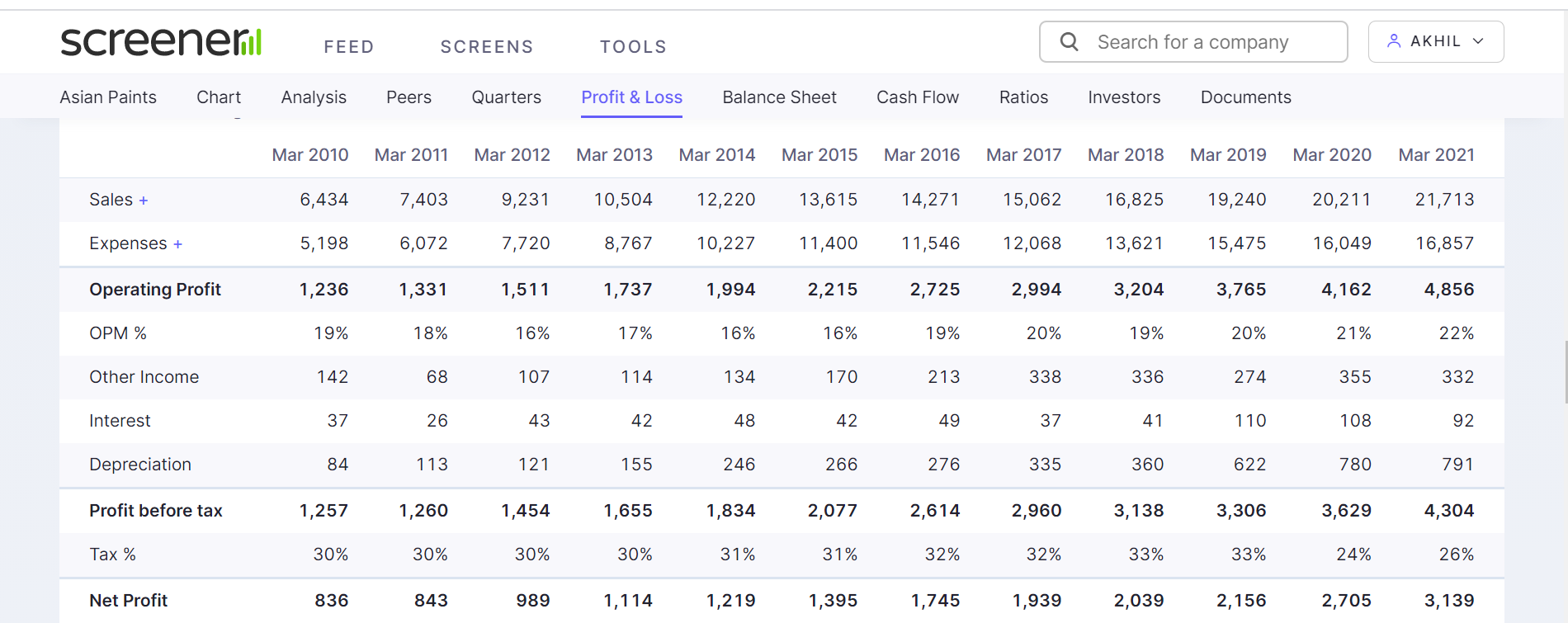

With the recent debate on High PE vs Low PE stocks, I thought of comparing ITC (low pe) with a High PE stock just as an acadmeic excercise. Let’s look at how ITC has fared against Asian Paints in the last decade. They both currently have around the same Market Capitalization (Asian Paints around 10% higher than ITC)

ITC

Asian Paints

10 year Sales Growth

10%

11%

10 year PAT Growth

14%

14%

10 year ROE

27%

28%

Even though they trade at drastically different multiples, ITC and Asian paints have had exactly similar jouneys in the last 10 years. Their Sales, PAT and Roe rates are exactly similar. Now here is the interesting difference.

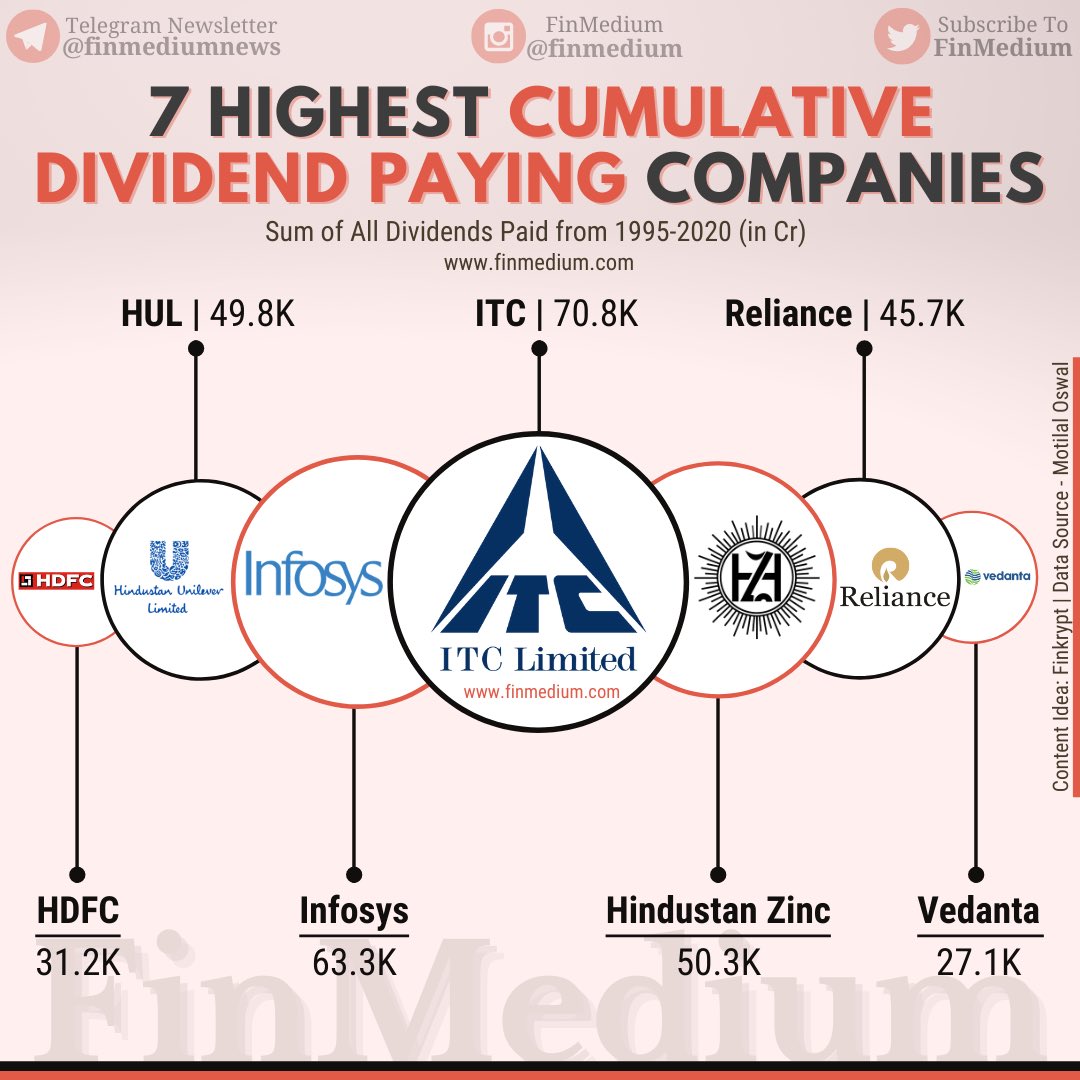

Cummulative PAT for Asian Paints over the last decade (2011-2020) has been around 16k crores. ITC’s PAT in 2020 itself was 15,000 cr. Huge difference.

Now I understand that markets are forward looking and hence let’s look at an extreme scenario for the next decade. Let’s say Asian Paints continues to grow PAT at 14%, just like they have for the last decade and ITC has 0 growth rate in the future.

Asian Paints PAT in 2030 - 10,000 Cr

That is still just 66% of ITC’s current PAT and ITC will still keep producing the 15k PAT every year for a decade even with 0 % assumed growth rate. (This is an extreme case assumption. I do not see any of these playing out at all)

Another interesting information bite - ITC earned 2400 cr from their Investments in 2020 (Other income), while Asian Paints total PAT for the year was 2700 cr.

Yet the market thinks they both deserve the same market cap.

You can do the same analysis with Cash flows and the number will more or less be the same. There is no fancy analysis required here to understand that clearly something isn’t right. You can form your own judgements from this

Look at below data why ITC stock is not moving up. FII’s are dictating its movement.

Its demand and supply that is deciding the fate of ITC.

Major buyers are MFs and other institutions and they are only buying at low price as they already hold big % in ITC. they are not ready to pay premium to it

Retail shareholding did not change that much in this period.

Good data. ESG funds pulling out has been a drag on the stock price of ITC.

Excellent comparison Akhil. ITC 10 year Sales Growth, PAT growth, ROE Growth matches that of Asian Paints. ITCs PAT in 2020 is Asian Paints 10 year PAT put together. ITCs investment income is more than Asian Paints PAT!!

ITC is a great pick for value investors. One who believes in its value has to ‘buy and hold’ it till market realizes its value. That will happen over time:

(1) ITC goes for de-merger and that could result in value unlocking

(2) ITC FMCG plays out

(3) ITC uses the 35000 INR crore cash on its book to buy-back shares increasing the EPS

Key concern with ITC has been the excess cash on its books, the capital allocation towards hotels and industry structure where cigarettes are taxed so highly. The management of ITC is top notch with it being a preferred IIM day-0 company and the management can be trusted to move the needle over time.

Cigarette business is degrowing around the world not because people are giving up tobacco but due to vaping. Media (since its main objective is grabbing eyeballs, gives headlines like “cigarette smoking will end in 10 years”). In India vaping is officially banned. Even if the ban is removed later, I think it would be more appropriate to consider ITC to be in the tobacco industry and not cigarette industry. Before the ban, ITC had infact started to sell vaping devices.

So I think there is a high probability of cigarette or tobacco cash flow continuing for the foreseeable future.

Company generating lots of cash certainly has some value. Market may not value it highly during a phase when money is cheap (like present), but that could change not only due to growth visibility but also a change in interest rate environment (which seems probable as a result of inflation).

I am not not picking, just taking up these two points since they seem to be part of the reason ITC is valued currently the way it is. And as you said, it will be a test of patience.

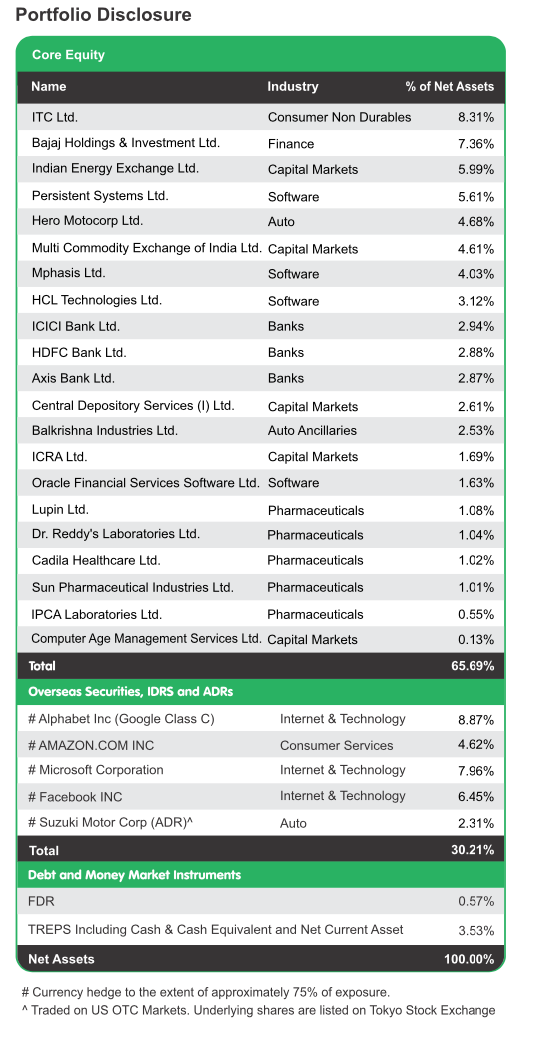

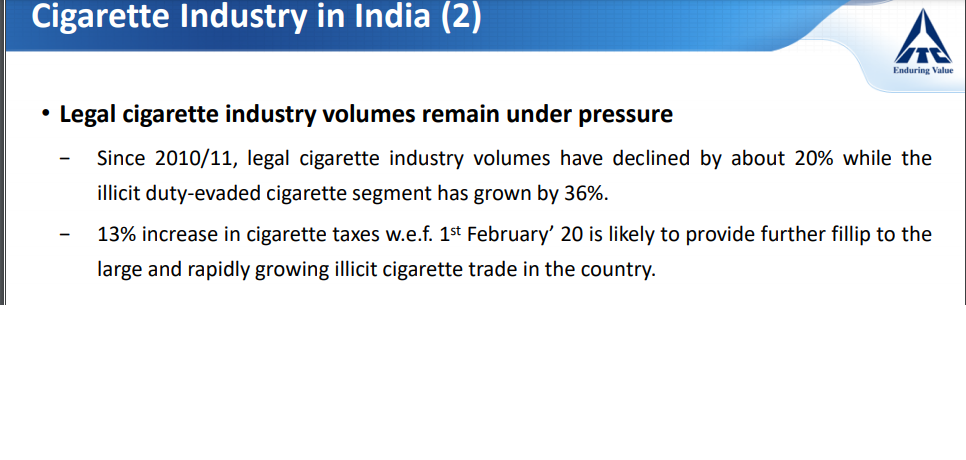

I tend to disagree here. Vaping was only a small part and could have hardly moved needle for the size of ITC. See the last 10 year data of cigarette business in India (lets not get global) and see how the volumes are declining for ITC (or may be 1%-2% growth here and there). May be health or social reasons. This is not the case with alcohol which is growing at a decent pace. This shows that consumption of cigarette as such is coming down. ITC 2019-20 investor presentation -

I am not saying cigarette will be banned or extinct in next ten years. Like buffet says, “I don’t think the Internet is going to change the way people chew gum”. So cigarettes are going to stay and be here for long. But it can hardly contribute incrementally volume wise to the topline. Price increase may then only be the way to maintain margin, and if one sees it, the same is also steadily coming down as every cost cannot be passed on. So being realistic here, cigarette will never see growth in the next decade.

In every portfolio some part needs to be allocated to safe bank FDs/RDs etc., and for me ITC is that stock, which gives more than FD returns by way of dividend, without much downside (hopefully!). But if FMCG engine starts firing up, it will be an added bonus.

I believe the volume degrowth has direct connection with rise of taxation and illegal cigarettes. If the government realises this (which we know it already has) a more realistic tax structure could see volume taken away from illegal cigarettes and consequent volume increase for listed players.

I wish that be the case and I’d be willing to give up whatever money ITC might make for me if that is the case. But I see increasing social acceptance of drinking AND smoking (including for females). Infact increasing social acceptance of addictive things in general (whereas even tea being slightly addictive was scoffed at some years ago.)

Before GST, cigarette was leviable to Central Excise Duty, NCCD and other cesses and state sales tax. We still remember the days we used to be glued to the screen how much duty would be levied on tobacco products and cigarette during the union budget. Come GST, the situation is not the same. We now have GST plus compensation cess. The GST council under the law itself is required to meet once a month and several recommendations during this to hike/lower taxes is made. So what was an annual affair is now a monthly affair. This gives impetus to the Government to play with the duty structure, which was not there earlier. Any crisis be it covid or cyclone, the burnt has to be borne by someone and this industry is at the forefront. When you have to raise tax, you raise it, the question of it indirectly making way for illegal cigarettes are never a concern for the Government.

Data doesnt support this. Unless there is data, it will only be a narrative.

Everyone is requested to stick to the fundamentals & value additive posts. Repetitive & irrelevant posts does not add any value but it will be looked up as violation of discipline and the offenders may be dealt with stricter actions. So please maintain decorum on this forum.

Cigarette volumes recovered to nearly pre-Covid levels towards the close of the year : This is interesting data point - > Smokers habits have not changed dramatically / there has been market share gains : This is good performance inspite of lower EBIT margins

Hotels business turned EBITDA positive in H2 + 3 addition of asset light management contracts : OCF from Hotels can be interesting in coming years as revenue inflation increases … while capex tapers off

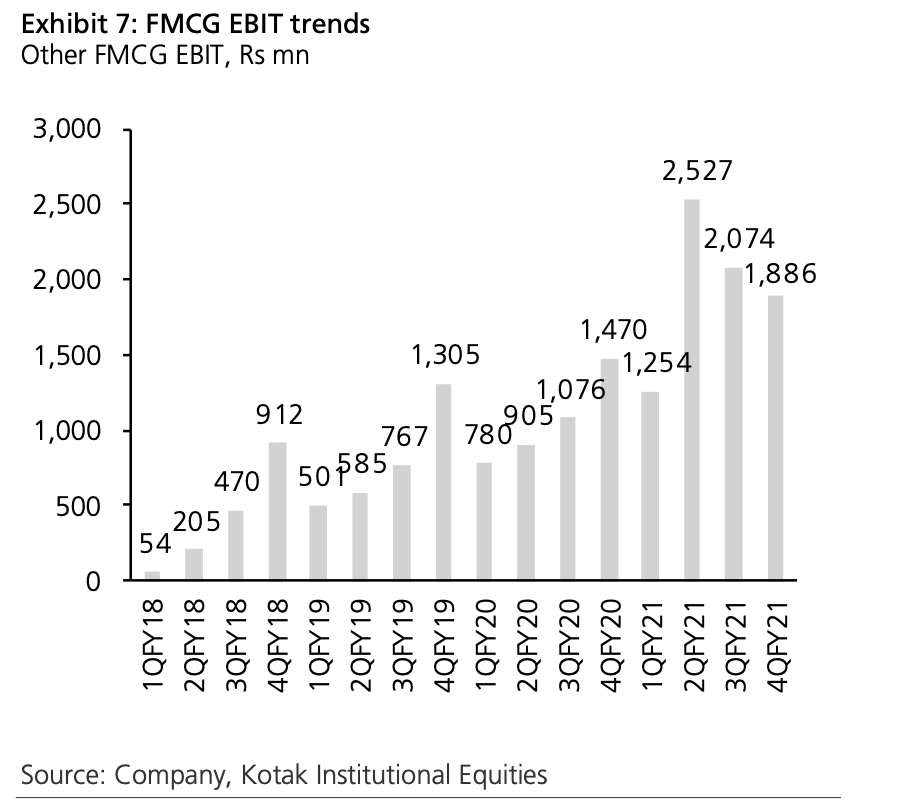

FMCG others

FMCG Quarter growth trends indicates – Normalised FMCG growth will be around 11% to 16% depending upon inflation - In lower inflation scenario FMCG will grow at 11% and higher inflation @ 16% - Thats is not so great considering smaller FMCG companies like Dabur / Marico are in this range …

FMCG others need to crank attest at 20% + Gr and margins should go up as operating leverage unleash … If that is not happening there is cause of concern .

Paper 13% Profit Gr & Agri at 40%+ were decent performance - In inflationary scenario these business should do well …